Opening up the opportunities within Commercial Banking has been saved

Services

Opening up the opportunities within Commercial Banking

PSD2 and Open Banking

A catalyst for innovation

The Competition and Markets Authority (CMA) announcement and the European Union’s decision to extend the scope of the original Payment Services Directive through PSD2, coupled with the Open Banking Standard set out by the UK government’s Open Banking Working Group, illustrates how the payments market will be opened to new entrants, driving further competition and accelerating innovation.

First-mover advantage provides an opportunity for commercial banks to act as the aggregator of deposit and asset information, improve customer experience via integrated products and provide clients with insight and a holistic view of cash-flow and available working capital. Commercial banks that succeed in leveraging the shift towards Open Banking will respond now, embracing the opportunities to collaborate with FinTech providers and proactively looking at ways to build a flexible integration and application programming interface (API) platform.

The rise of APIs

How can a commercial bank respond?

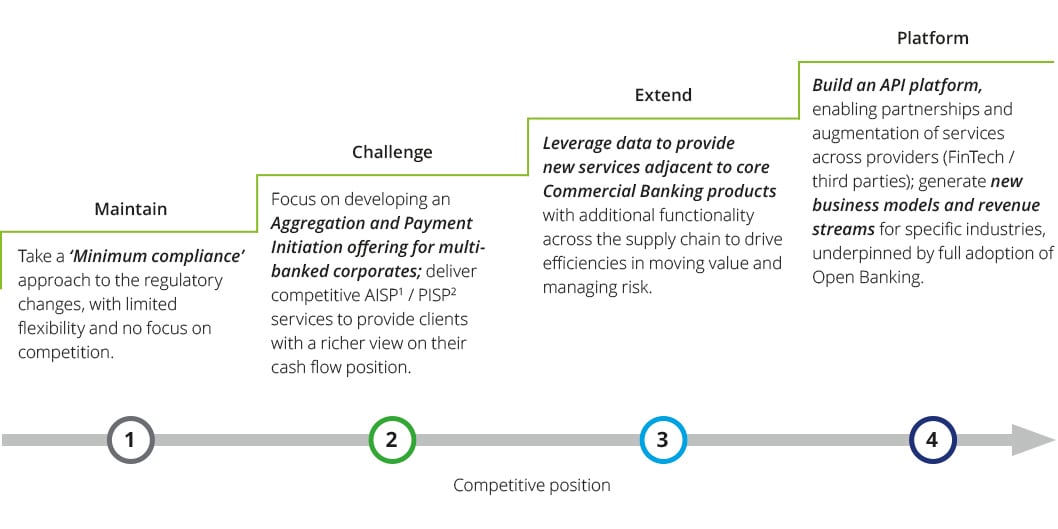

We have identified four ways in which commercial banks can position their response to the impending regulatory changes and the industry-wide adoption of API-enabled banking services:

Minimum compliance is not enough. There is significant opportunity to leverage PSD2 and Open Banking to unlock value through scalable and flexible API platforms. We believe that combining the traditional strengths of bank’s client relationships and core assets with Open APIs will enable new, innovative products and data-enabled services to be developed and monetised, opening up new revenue streams.

Strategic choices for commercial banks

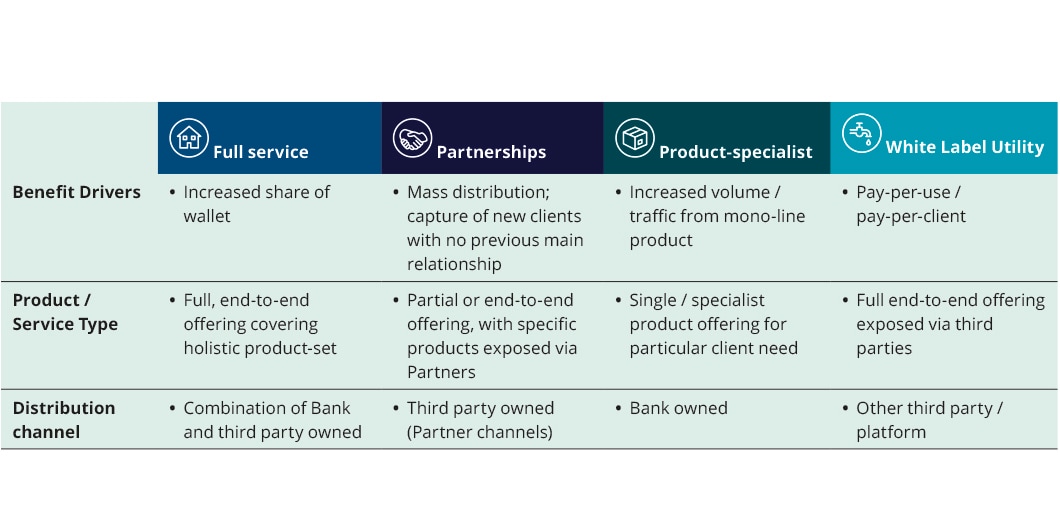

As we are seeing in Retail banking with the shift towards a Marketplace banking model, we believe the Commercial Bank-as-a-Platform model will become pervasive and both banks and FinTechs have a number of choices to determine what role they play and how they will collaborate to serve commercial clients. The expectation is that banks will not only adopt the Banking-as-a-Platform model, but will combine this with one or more of the roles below based upon their strategy, client-base, competiveness of their offering and their ability to respond quickly to changing client preferences.

Implications on the business model

Depending on the extent to which commercial banks choose to adopt the Commercial Bank-as-a-Platform model there will be specific implications and benefits seen across the bank. The table below outlines the

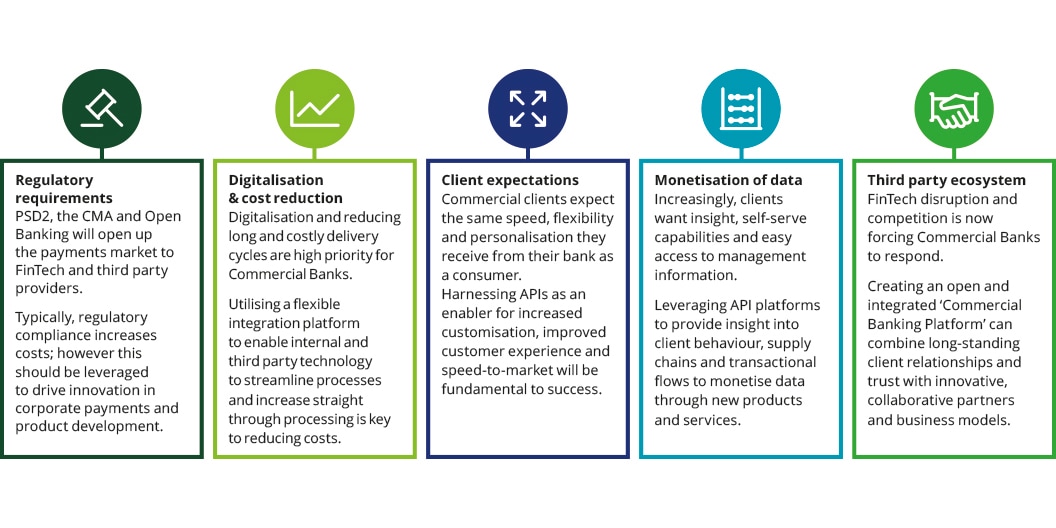

The importance of APIs and the opportunity for commercial banks

The importance of regulatory compliance and PSD2 / Open Banking implications for retail banks is widely publicised. However, we believe the potential use cases for API-enablement in Commercial Banking can add significant value to both banks and their clients.

The adoption of a corporate line-of-business and industry-focused API strategy can provide multiple opportunities to strengthen existing revenue streams, while also creating new ones. Some of these opportunities are explored here:

Our capabilities

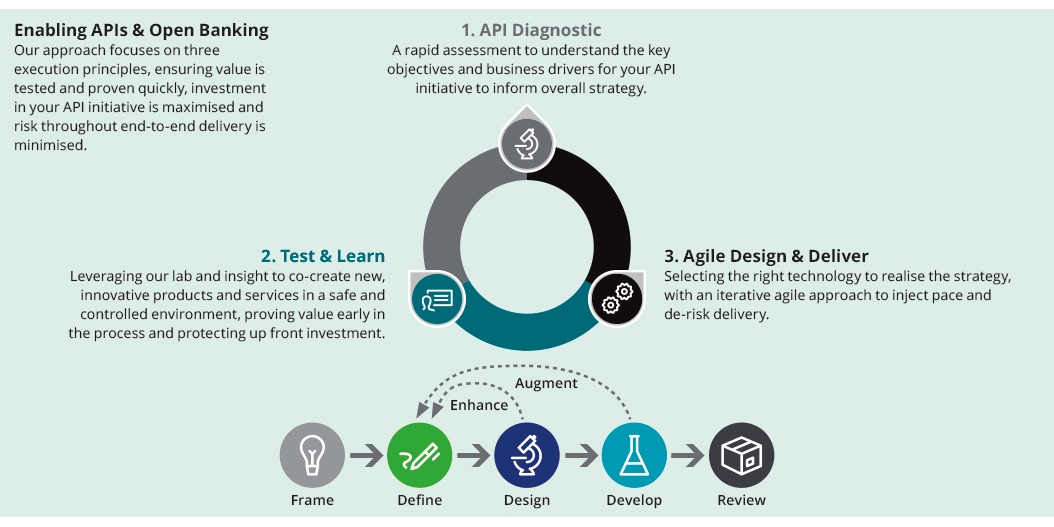

We offer a breadth of capabilities that can support you with the end-to-end execution of PSD2 and API enablement - from strategy through to platform implementation.

API diagnostic

- API strategy review

- Rapid capability assessment

- Vendor market scan

- Proposition development

Test and learn

- Development of new product and services

- Business case definition

- Solution architecture &

PoC testing

Agile design and deliver

- Vendor spec and select

- Functional and technical design

- Platform configuration and implementation

Key contacts

Recommendations

The future of Commercial Banking

The Deloitte Digital Commercial Banking Showcase

Trade Finance outlook

An exciting time for Trade modernisation