The aging of the US labor force

The November 2023 Economics Spotlight explores the impact of a sluggish labor force participation rate. As the population ages, employers will need to rethink hiring strategies to offset the looming talent gap.

Picture a world in which over a third of the US population is over retirement age. This is the landscape the US economy will have to navigate in the future. To support Deloitte’s United States Economic Forecast,1 we modeled the impact of the aging of the population on labor force participation (see the sidebar, “Methodology”). The change in the US population is expected to drive a decline in the labor force participation rate—the proportion of Americans either actively working or seeking employment. Older people are much less likely to want or have jobs, so the aging of the population sets the stage for sluggish growth in the labor force and a persistent drop in the participation rate. Employers are likely to find the US job market of the future very different from that of the past.

Methodology

Our projection of the participation rate is based on US Census Bureau data and runs from 2023 to 2050. Census provides estimates of the actual population (through 2023) and projections for the years after that. We used the Census’s “middle series” as the basis for our projections. We assumed that the participation rate for each five-year cohort would adjust to a long-run value (depending on the scenario) over the next five years and remain at that value through the end of the forecast horizon. We made three assumptions for the long-run value, with the optimistic assumption leading to the highest participation rates and the pessimistic assumption leading to the lowest participation rates.

{kind=link}

In all three scenarios, we’ve assumed that the participation rate for those who are 65 years old and over remains at the 2022 level. That is close to the average participation rate of the five years before the mid-2010s, and slightly less than the peak in 2019. For the other scenarios, we made the following assumptions:

Baseline scenario: We assumed that the participation rate would return to the 2019 level over the next five years. In this scenario, the total participation rate drops from 62.2% in 2022 to 60.0% by 2035. It further falls at a slower rate over 2035–2050 to 59.5%.

Optimistic scenario: We assumed that for individuals who are 65 years old and below, the participation rate will converge to 1% above the 2019 level. In this scenario, the participation rate goes down from 62.2% in 2022 to 60.5% by 2035, and continues falling, at a slower rate, to 60.0% in 2050.

Pessimistic scenario: We assumed that for individuals who are 65 years old and below, the participation rate reverts to the average of the 2014–2019 levels (which is slightly lower than the 2019 level). Under this scenario, the participation rate decreases from 62.2% in 2022 to 59.3% by 2035 and continues to decline at a slower rate, reaching 58.8% by 2050.

In all three scenarios, the fall in the participation rate is caused by the aging of the population. The Census projection shows that an increasing share of the population is above retirement age (65–95 years) over our forecasted period (figure 2).

{kind=link}

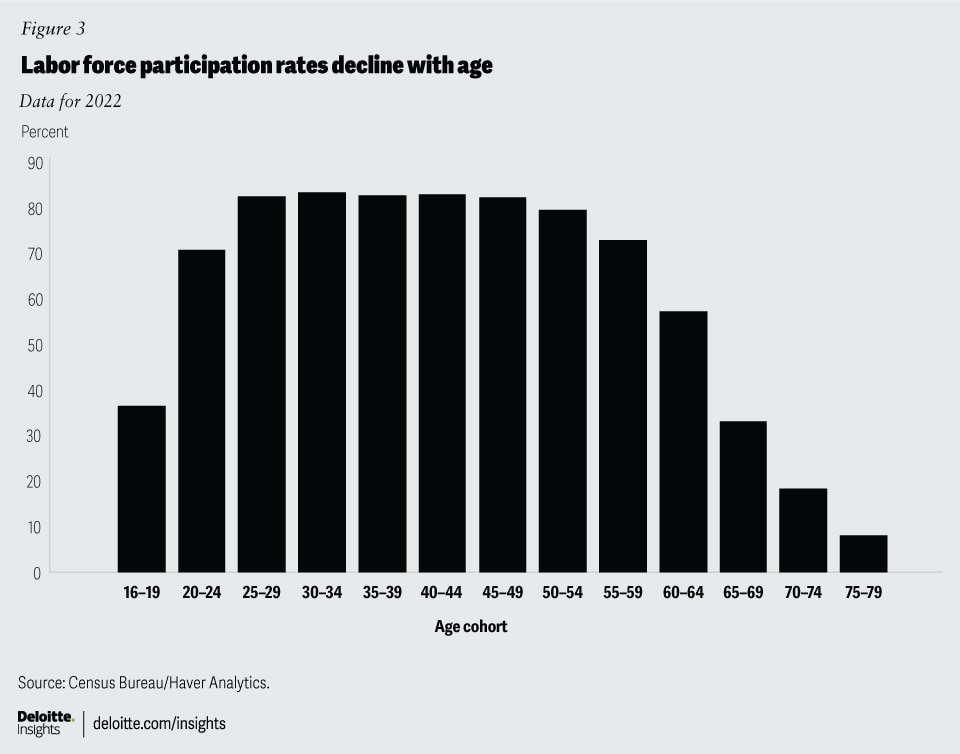

Participation drops sharply after age 65 (figure 3). We’ve assumed that these workers continue to participate at lower levels, which leads to a lower overall participation rate in the future. Even in our most optimistic scenario, in which participation of those below 65 years rises one percentage point above the 2019 level (which was already relatively high), additional participation of the younger workers is more than offset by the growth of the number of people at or above retirement age.

A rise in the participation of older workers could reduce, but not eliminate, the decline in the labor force. The official US Bureau of Labor Statistics projection of the labor force shows a decline in the participation rate even as the participation rate for people over the age of 55 rises.2 Our view is more conservative; participation among older workers will likely depend a great deal on whether the labor market remains tight and whether employers become more willing to hire older talent. Given the level of uncertainty about the state of the labor market, the relatively strong financial performance of retirement assets, and the comparatively fast rise of participation after the global financial crisis, we believe that it would be unwise to rely on projections of further growth in the participation of older workers.

{kind=link}

The near future presents a challenging labor market for employers. The labor force will continue to grow, but at much lower rates than in the past. Slower population growth and an older population will put a limit on the growth of labor supply, with only the possibility of higher immigration providing any suggestion of loosening on the supply side. That would place a speed limit on US economic growth, and GDP growth rates of as low as 1.5% per year may be enough to keep the labor market tight. Economic policymakers will have to adjust to a world of lower growth.

And it’s not just policymakers that face a challenge. Employers will need to future-proof their talent management strategies as labor force growth continues to slow. Strategies that worked to acquire and retain talent in the past may not be successful in the tighter labor markets of the future. And companies that wish to remain competitive need to pay close attention to what the slow growth of the labor market means for them.