US government debt: A US$33 trillion problem?

The October 2023 Economics Spotlight takes a deeper dive into the US government’s debt issue—while alarm bells aren’t ringing just yet, it’s a longer-term problem that needs a robust solution to ensure the economy’s financial stability.

“Annual income twenty pounds, annual expenditure nineteen, nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds, nought and six, result misery.” Mr. Micawber in David Copperfield by Charles Dickens

The US government has long ignored Mr. Micawber’s advice. While the consequences of overborrowing at the country level are quite different than those experienced by the spendthrift character of Charles Dickens’ imagination, who was thrown into debtor’s prison, there are penalties for countries that run up the tab and then fail to make the required payments. International capital markets close off (or at least become considerably more expensive), and often, the country’s government finds it necessary to rein in spending and raise taxes. And voters don’t particularly like higher taxes and reduced government services, which can lead to political instability.

Why hasn’t that happened to the United States? The value of all debt depends on the belief of lenders that the borrower will be in a position to repay the borrowed money. If that belief falters—even if it’s not Mr. Micawber’s exact fate—it could certainly lead to some type of crisis.

The growth of the US government’s debt is a long-term problem, but it is unlikely to bother anybody in the next few years

So far, lenders’ belief in the US government’s ability to repay hasn’t yet faltered. Yes, many people “know” that the current trajectory of the US budget is “unsustainable.” Evidently, however, investors—in the United States and abroad—believe that something will happen to alter that trajectory. As long as they continue to believe that, the US Treasury can continue to borrow. But if that belief becomes untenable, the US government’s finances and the US economy will likely be in trouble. And that means trouble for the global economy since US Treasury debt underpins the global financial system.

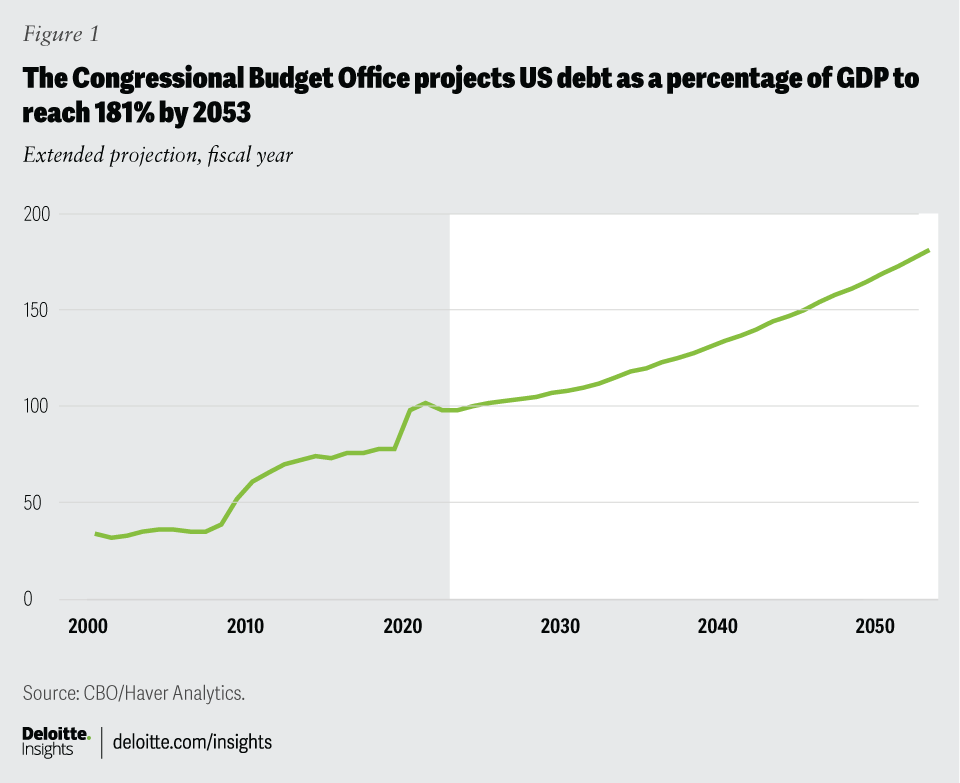

Figure 1 is the usual picture used to illustrate the problem. The Congressional Budget Office (CBO) projects that US debt as a share of GDP will reach 181% by 2053, up from about 100% today (for more details, see the sidebar, “How the CBO forecasts long-term deficits”). But this, by most measures, is something that would be difficult to pull off. At that point, interest on the debt would require payments of almost 7% of GDP, more than twice the current level. Such a high level of interest payments would squeeze out other federal spending and would likely require very large tax increases. Neither option appears good for the US economy nor is it politically palatable. Figure 1 is optimistic since the CBO’s projection is based on “current policy,” with an unrealistic assumption that “discretionary” spending—spending on things that aren’t transfer payments like social security, Medicare, and Medicaid—falls by about half of GDP. Under more realistic assumptions about future spending, debt reaches 250% of GDP by 2053.1

{kind=link}

How the CBO forecasts long-term deficits

The CBO is a nonpartisan agency tasked with helping Congress understand budget questions and their implications for the economy. Every year, the CBO publishes a 30-year projection of the budget.

To forecast the budget deficit, the CBO makes a number of assumptions about the growth of the economy and budget policy. The latest projection2 assumes:

- The US population will grow at an annual rate of 0.3% from 2023 to 2053, considerably more slowly than in the recent past

- Real potential GDP will grow 1.6% per year over the next 30 years

- The yield on the 10-year Treasury note will average 4.0%, and the interest rate on all debt held by the public will average 3.4%

Changes in these assumptions can have a large impact on long-term budget projections. Lower productivity growth or higher interest rates could cause the deficit to balloon faster than the CBO projects. Faster immigration, by allowing for a larger labor force and more tax collections, could help to reduce the deficit.

On top of those economic assumptions, the CBO’s projection also assumes that government policy related to the budget is unchanged. These assumptions may be unrealistic, since current law may not be a good guide to future tax and budget policies. The CBO also publishes a set of alternative projections showing what might happen under different tax and budget paths.3

On autopilot, this plane is expected to eventually crash, or as international finance experts say, experience a “sudden stop.”4 If global investors eventually come to the conclusion that the United States is not in a position to repay debts—and if others have the same point of view—they will scramble to sell US debt and refuse to buy anymore. The experience of other countries (like Argentina or Greece) shows that the US Treasury could indeed suddenly, and without much warning, find it impossible to complete Treasury auctions, and US interest rates would soar as global investors attempt to sell their holdings. Over a longer period of time, the country could experience high inflation, which is a common response to the inability to continue borrowing; for the United States, inflation would be especially tempting because the country’s debt is denominated in its own currency, so inflation would directly reduce the burden of past debt.

In the particular case of the United States, there would be global consequences as well. Attempts to sell US Treasuries would create a global liquidity crisis, which might be impossible to easily solve. Other major central banks, such as the European Central Bank and the Bank of Japan, would try, with difficulty, to offset the impact of the dollar’s collapse. The most likely longer-term impact would be a global recession of substantial length and depth until a replacement system for the dollar is accepted.

That, of course, is the reason for the thunderous rhetoric about how the United States really has to do “something” to change course. The recommended “something” may depend a lot on the preferences of the person behind the rhetoric—but the need for action does appear to be clear.

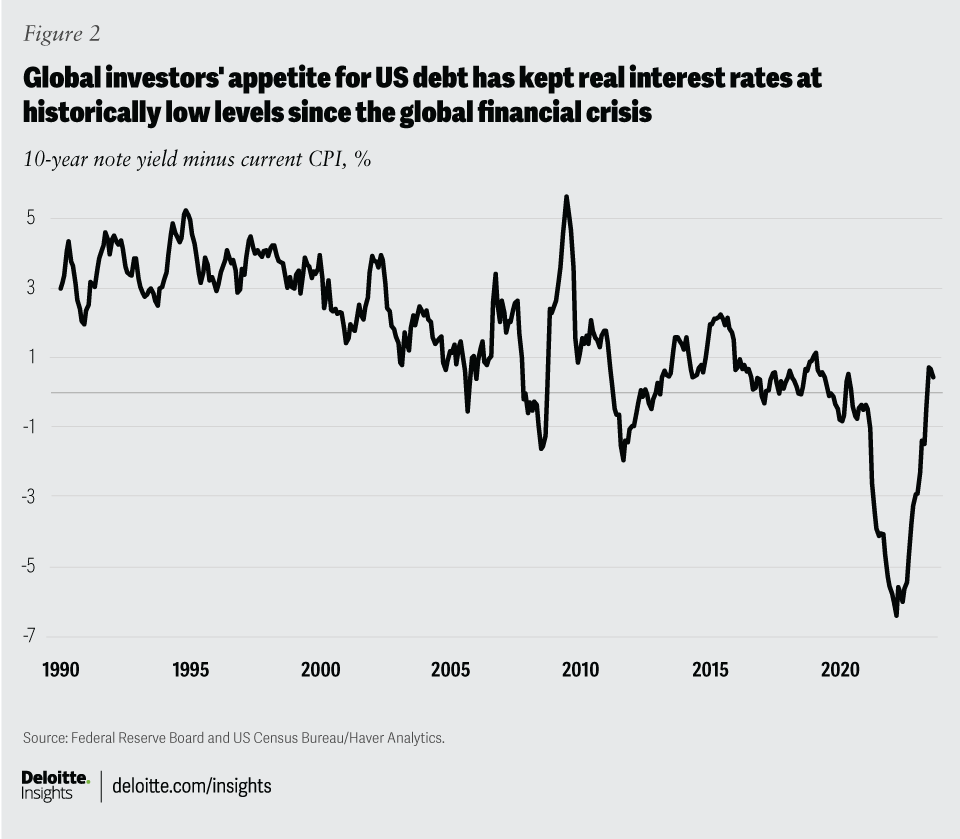

And yet, thunderous rhetoric aside,5 for the past 20 years, global investors have been hungry for US debt. Demand for Treasuries has kept real US interest rates at historically low levels since the global financial crisis (figure 2). Global investors are hardly ignorant of the long-term budget challenges the US faces. But they know that for the time being (10 years? 30 years?), the United States will have no problem making payments. And there aren’t a lot of alternatives to US Treasuries—no other currency provides deep, liquid markets, ensuring the ability to buy or sell easily, and a large, wealthy economy backing the currency.

{kind=link}

So, for now, US debt remains highly desirable, and the US Treasury continues to find plenty of interest in auctions of new debt. Someday the supply will likely overwhelm the interest of global investors, but it doesn’t look like something that will happen very soon.

Countries have experienced high debt/GDP ratios in the past while remaining central to the global financial system

Just when will the country need to fix the problem? The answer is that we don’t know. And the level of debt relative to GDP is a less reliable indicator than some have suggested. Around the time of the global financial crisis, some economists suggested that once debt increased above 90% of GDP,6 the probability of a crisis—of financial markets refusing to continue financing that country—rose. That might have been a useful metric for smaller countries borrowing in foreign currency, but it’s less useful for countries that are the center of the global financial system.

Admittedly, the sample is limited. There are only two countries that have held this position in modern times. Until the First World War, the United Kingdom was the center of global finance, the pound was the standard international currency, and Gilts—UK Treasury securities—were the ultimate “safe” bonds. Yet, in the early 19th century—precisely when the United Kingdom established itself as the global money center—UK government debt hit almost 200% of GDP. Although it slowly declined, the United Kingdom’s debt-to-GDP ratio didn’t fall to 100% until 1857. That didn’t prevent the City of London from becoming the global financial center of the time, and the pound from becoming the key global currency. What mattered was the reputation of the sovereign and the size of the market. UK government bond markets were (for the time) large, and the UK government paid its debts faithfully.7 British banks financed everything from US railroads to the Suez Canal. And they did it in pounds.

After the first and second world wars, the United States took over leadership of the global economy. Despite the hiccups around the end of the gold standard in 1971–73, the dollar has remained the center of the global financial system since 1945. Particularly after 1973, this reflected the US government’s repayment record and the relative size of US Treasury markets.8 And the current high level of US government debt has a precedent: In 1946, US government debt owned by the public totaled 118% of GDP.9

But there is a difference between today’s debt and those past examples. Both the United Kingdom and the United States ran up debt to fight huge wars. Once those wars were over, both governments were able to reduce their spending and reduce the relative size of their debts. The pandemic-level spending can be seen in this light. But with the pandemic over, investors might well expect the US government to return to improving the country’s long-term finances. The CBO’s projections of continued large deficits over the next 10 years show that is not the case. Instead, the United States is set to continue to add enough to the debt each year that the growth in debt will be faster than GDP.

Health care costs play a key role in the growth of the deficit

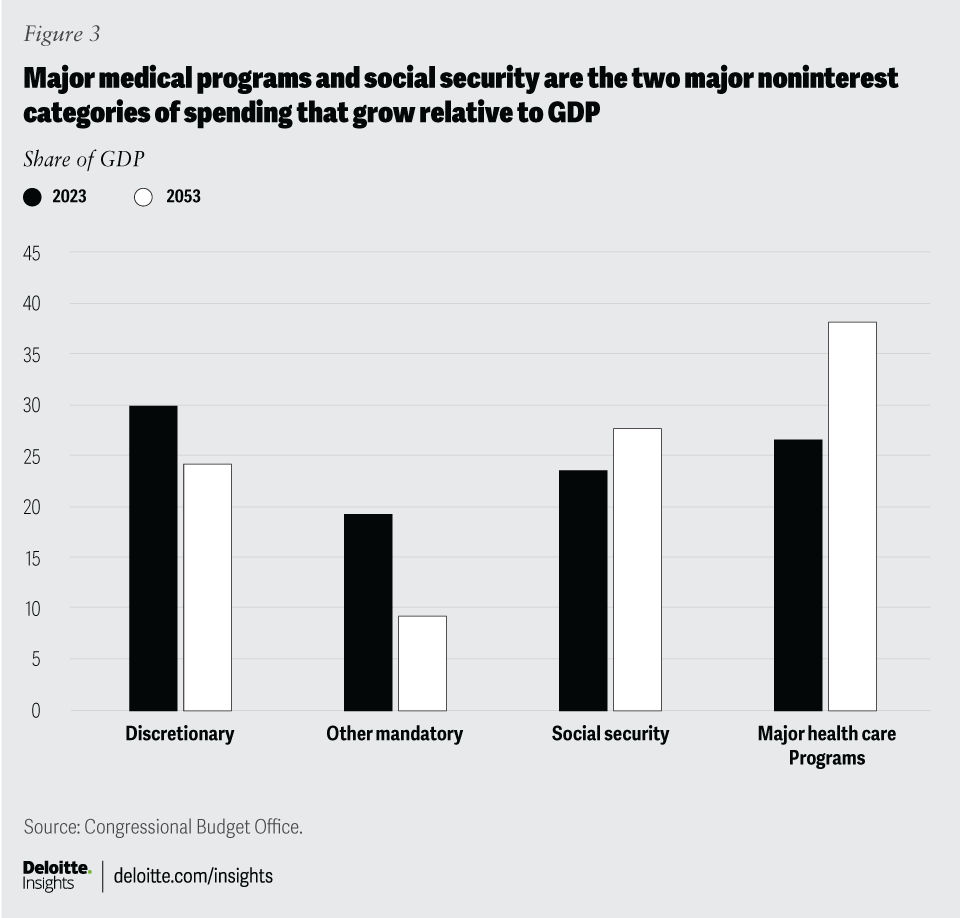

In the CBO’s projections, the only major noninterest categories of spending that grow relative to GDP are major medical programs and social security (figure 3).10 Outlays for these major medical programs rise some 9 percentage points of GDP, more than twice the rise in social security.

Health policy is therefore central to solving the deficit. While the aging of the US population can’t be avoided, the poor quality of US health outcomes relative to spending11 suggests that there is quite a bit of room for reducing costs while actually improving the health of Americans.12 The good news is that we can improve US government finances while actually improving our lives. It’s also a good way to separate serious policy proposals from those that are, like some unhealthy snacks, merely empty calories.

{kind=link}

There is some, but limited, room for tax increases

A lively debate is underway among economists about the impact of taxes on economic growth. A change in tax rates can impact the economy in three ways:

- In the short run, aggregate income will rise (if taxes are cut) or fall (if taxes are raised), increasing or decreasing demand as the money left in consumers’ and businesses’ pockets after taxes rises or falls.

- The short-run demand impact may be offset by the need for higher government borrowing (if taxes are cut) or lower government borrowing (if taxes are raised), which will raise or lower interest rates and affect interest-sensitive portions of aggregate demand like housing and business investment.

- Higher taxes reduce long-term returns to investment in physical and human capital and may affect the incentives to join the labor force. A permanent hike in taxes could therefore slow the long-term growth of the economy by reducing the growth of the capital stock, innovation, and the labor force—depending, of course, on the specific tax rates the government chooses to raise.

The first two impacts are likely to be significant only in the short run. The extra aggregate demand generated by a tax cut might be useful in an economy that is at less than full employment, and siphoning off some demand can, in theory, help prevent inflation from accelerating. But the reader should keep in mind that all this has nothing to do with solving the long-run problem of fiscal sustainability.

The long-run budget policy requires focusing on the impact of taxes on growth in the long term, not over the next year or two. And that’s a contentious issue.

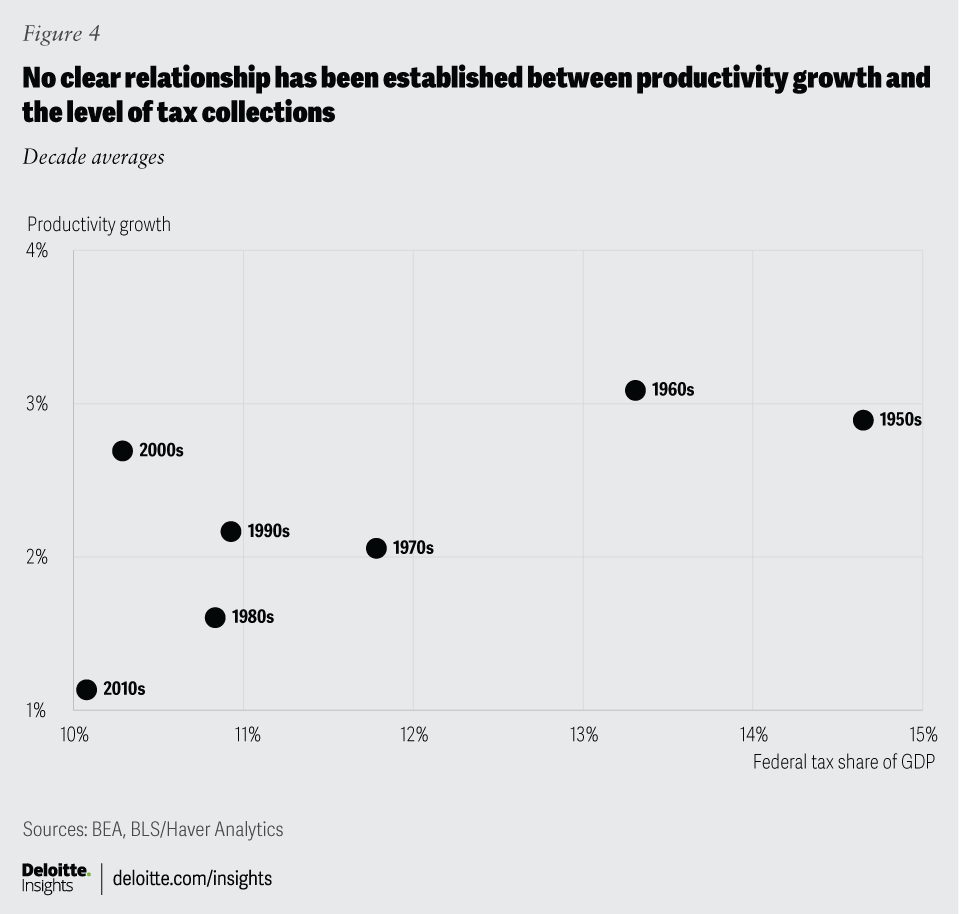

There is no consensus within the profession about the size of the impact of permanently higher taxes on economic growth. Historical experience doesn’t show an obvious relationship between productivity growth and the level of tax collections in the United States (figure 4).13

{kind=link}

If taxes do reduce long-term growth, that may be seen as the cost of long-term financial stability. Although improvements in the health care system can play a key role in reducing the deficit and long-term growth of the debt, the aging population will place limits on how much Americans are willing to reduce such spending. That makes raising some taxes an important part of the policy mix necessary to reduce the growth of government debt. Figure 4 suggests that based on the historical experience of the United States, tax increases in the neighborhood of 2% of GDP are unlikely to have a very large impact on growth. If tax increases at that level can help to achieve sustainable federal budgets (and perhaps to build a permanent coalition to maintain that stability), the price is probably worth paying.

Other policy initiatives may be helpful, but simply aren’t large enough to solve the problem without health care reform and additional taxes

There is a long menu of ways to save money or improve revenue collections that would help reduce the long-term deficit. More immigration would raise the growth rate and increase the federal government’s tax base. Raising the social security retirement age for some workers and further means-testing benefits might be part of a complete package to solve the problem. The growth of defense spending could be limited. But, alone, these measures simply can’t be large enough to lower the growth of US government debt to sustainable levels. Worse, some measures—such as cutting the federal government’s R&D spending or assistance to building infrastructure—might themselves reduce growth and the government’s revenues, thus simply adding to the problem.

We are challenged to look far into the future

The United States faces a difficult challenge over the coming decades. It’s particularly difficult because there is no short-term pressure to find a solution. For now, global investors are quite happy to load up on US Treasury securities, under the assumption that at some point in the future, a stable, mature democracy like the United States will meet its obligations. From an economic point of view, this is indeed the case. A wealthy and productive society like the United States can choose from a menu of options that are the envy of many poorer countries that have made a similar mistake (not to mention Mr. Micawber). But we must eventually choose from that menu of solutions. If we don’t do so, our children, years from now, may well face a crisis that will likely cost considerably more than the budget cuts and tax hikes we are now discussing. Readers familiar with Dickens’ David Copperfield will remember that Mr. Micawber and his family had a miserable time in debtors’ prison. We should work now to avoid the equivalent fate for future citizens of the United States.