Noncontrolling interests has been saved

Perspectives

Noncontrolling interests

On the Radar: Interpreting the accounting guidance

Consolidation of a subsidiary may require reporting on equity-classified instruments that the parent doesn’t own. Between complex capital structures and varying levels of guidance, the accounting principles for these noncontrolling ownership interests can be difficult to apply.

A challenging aspect of US GAAP

Once a reporting entity concludes that it is appropriate to consolidate another legal entity, the reporting entity must evaluate the accounting for equity instruments that are not owned by the parent. Only equity-classified instruments that are not owned by the parent are noncontrolling interests.

The objective of accounting for noncontrolling interests is to present users of the consolidated financial statements with a clear depiction of the portion of a less than wholly owned subsidiary’s net assets, net income, and comprehensive income that is attributable to holders of equity-classified ownership interests other than the parent. In practice, the combination of complex capital structures, multiple sources of authoritative guidance on accounting for noncontrolling interests, and multiple policy elections available to reporting entities can make this objective difficult to achieve.

ASC 810-10-20 defines a noncontrolling interest as the “portion of equity (net assets) in a subsidiary not attributable, directly or indirectly, to a parent” and further states that a “noncontrolling interest is sometimes called a minority interest.” This definition applies to all entities that prepare consolidated financial statements.

Although the accounting principles related to noncontrolling interests have been in place for many years, they can be difficult to apply. The relatively brief guidance on nonredeemable noncontrolling interests (ASC 810-10) has resulted in diversity in practice, while the guidance on redeemable noncontrolling interests (ASC 480-10-S99-1 and ASC 480-10-S99-3A) is highly prescriptive and contains multiple policy elections. For these reasons, accounting for noncontrolling interests is a particularly challenging aspect of US GAAP.

On the Radar: Noncontrolling interests

Identifying noncontrolling interests

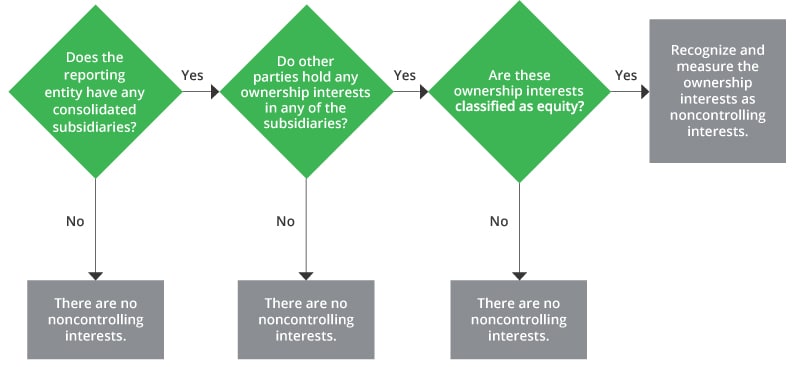

The decision tree below illustrates how to determine whether a reporting entity has any noncontrolling interests.

Since a noncontrolling interest is defined as a specific “portion of equity” (emphasis added), the first step in the identification of a noncontrolling interest is to establish whether such ownership interest in the subsidiary is appropriately classified in the equity section of either the subsidiary’s balance sheet or the parent’s consolidated balance sheet.

Key areas of focus

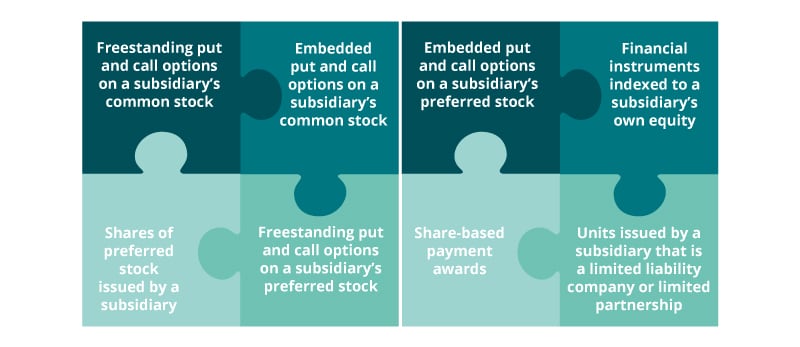

For simple capital structures involving only equity-classified common stock, the noncontrolling interest is the portion of the subsidiary’s equity not owned by the parent. For more complex capital structures, a reporting entity will need to use considerable judgment when determining whether an ownership interest represents a noncontrolling interest. While a legal-form liability is never considered a noncontrolling interest, not all equity instruments may be considered noncontrolling interests. Interests that require judgment include, but are not limited to, the following:

It is important to note that the scope of the noncontrolling interest literature begins with the identification of an instrument as an equity interest and the instrument’s classification as such on the balance sheet.

Continue your noncontrolling interests learning

Deloitte’s Roadmap Noncontrolling interests comprehensively discusses the accounting guidance on noncontrolling interests, primarily that in ASC 810-10 and ASC 480-10-S99-3A. For extensive analysis of whether a reporting entity should consolidate another legal entity, see Deloitte’s Roadmap Consolidation—Identifying a controlling financial interest. Entities should also consider Deloitte’s Roadmap Distinguishing liabilities from equity, which provides extensive interpretive guidance on the appropriate classification of equity instruments within or outside of the equity section of a reporting entity’s balance sheet.

Let's talk!

Learn more about this topic

|

Andrew Winters |

|

Andrew Pidgeon |

Get in touch for service offerings

|

Jamie Davis |

|

Recommendations

A guide to consolidation accounting

On the Radar: Identifying a controlling financial interest

Distinguishing liabilities from equity

On the Radar: Financial reporting impacts of ASC 480