2024 oil and gas industry outlook

The oil and gas industry should look to uphold capital discipline and prioritize viable low-carbon projects to help successfully navigate the changing energy demand landscape.

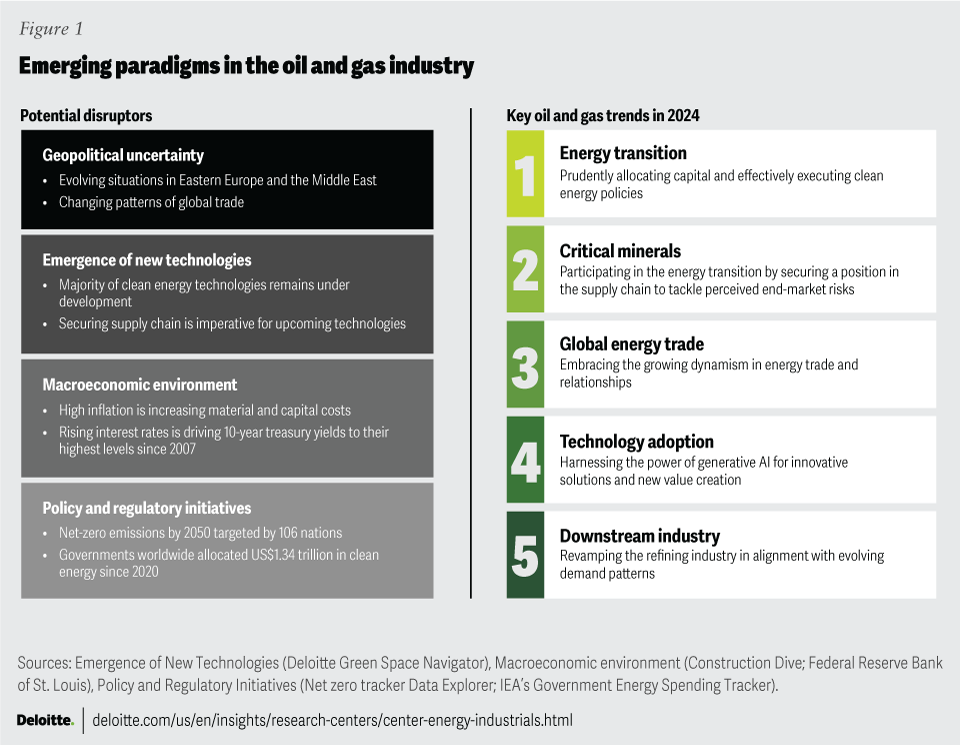

The energy landscape continues to be shaped largely by four disruptors: geopolitical factors, macroeconomic variables such as high interest rates and rising materials costs, evolving policies and regulations, and the emergence of new technologies (figure 1). These disruptors can have a significant impact on demand and supply, and trade and investment within the crude oil and natural gas (O&G) industry. The addition of OPEC+’s output cuts of 2.5 million barrels per day (mbpd) pushed Brent oil prices past US$90/bbl,1 while US Henry Hub natural gas prices rebounded to US$3.50/mmBtu in early November 2023.2

Despite these disruptions, global oil demand remains on track to grow by 2.3 mbpd in 2023 and cross the 100 mbpd mark for the first time in history.3 At a global level, electric vehicle (EV) sales grew by over 35% in 2023, with one in seven cars sold being an EV.4 This simultaneous growth in both petroleum-powered vehicles and EVs reflects regional disparities in demand structure, infrastructure readiness, technology adoption, regulatory policies, and socioeconomic considerations.

{kind=link}

The industry is expected to have a solid start in 2024 due in part to its strong financial position and high oil prices, barring further deterioration in the macroeconomic environment. This strength of the industry will likely enable it to finance both investments and dividends, and thus support its disciplined capital program and shareholder-focused strategy. The global upstream industry, for example, is projected to maintain its 2023 hydrocarbon investment level of about US$580 billion (an increase of 11% year over year) and generate over US$800 billion in free cash flows in 2024.5

However, this continued financial strength of the industry is likely to raise expectations of investors, regulators, and other stakeholders, who may anticipate further progress in emissions reduction, augmented investments in low-carbon energies, and amplified returns for shareholders. These expectations may serve as a driving force, spurring companies to focus even further on both emission reduction and economic performance. The 2024 oil and gas industry outlook explores five trends and industry drivers that are expected to play an important role in shaping the strategies and priorities of O&G companies in the upcoming year:

- Energy transition: Prudently allocating capital and effectively executing clean energy policies

- Critical minerals: Participating in the energy transition by securing a position in the supply chain to tackle perceived end-market risks

- Global energy trade: Embracing the growing dynamism in energy trade and relationships

- Technology adoption: Harnessing the power of generative AI for innovative solutions and new value creation

- Downstream industry: Revamping the refining industry in alignment with evolving demand patterns

{kind=link}

1. Energy transition: Prudently allocating capital and effectively executing clean energy policies

O&G companies are increasingly exploring clean energy avenues. However, their direct spending on low-carbon fuels and technologies, excluding investments aimed at boosting productivity and reducing emissions from operated assets, constitutes only 4% of their upstream capex.6 The global upstream industry is expected to generate US$2.5 trillion to US$4.6 trillion in free cash flows from its hydrocarbons business between 2023 and 2030—so, lack of capital is not an issue.7 Instead, the central challenge is scaling innovation while maintaining profitability and shareholder value.

Intricacies of energy transition

The dynamics steering the clean energy advancements of O&G companies are complex, as each company should weigh their own set of benefits and risks of investing in green initiatives. Progress at the company level and subsequent capital allocation are often influenced by internal as well as external considerations.

1. Internal considerations: In Deloitte’s survey of O&G executives in July 2023, 60% of respondents stated that they would invest in low-carbon projects if the returns on these projects exceed 12% to 15% (figure 2).8 For context, in 2022, returns on major renewable electricity projects ranged between 6% and 8%.9 Thus, the O&G industry would likely focus its 2024 spending on:

- Initiatives aimed at improving operational efficiency and reducing emissions, with more than one-third of surveyed O&G executives citing operational efficiency and direct emissions (scope 1 and 2) reductions as pivotal metrics for assessing energy transition progress;10 and

- Low-carbon fuels that are adjacent to their core or complement their primary operations, with around 37% to 44% of surveyed O&G executives citing natural gas, carbon capture and storage (CCS), biofuels, and hydrogen as critical to their low-carbon investment strategies.11

{kind=link}

2. External considerations: Since 2021, many new clean energy policies have been adopted or proposed worldwide, including the Infrastructure Investment and Jobs Act and the Inflation Reduction Act in the United States; and the proposed European REPowerEU Plan and the proposed Net-Zero Industry Act in the European Union. Similarly, renewable energy targets in Asia-Pacific and significant renewable energy auctions in South America seek to spur clean energy adoption.12 However, the effective execution of these policies or progression of these proposals remains important for attracting capital and reducing investment risks. For example:

- Delays in environmental reviews and permission for liquid natural gas (LNG) and CCS development, along with public acceptance challenges related to critical minerals mining and renewable power projects, could impede the pace of clean energy progress. For instance, the writing and publishing of environmental impact statements for solar and wind projects in the United States require around two and a half years, on average.13

- Policy alignment, particularly for emerging low-carbon technologies such as CCS and hydrogen hubs, is vital at the national and regional level. Consequently, some US states have formed coalitions to jointly bid for regional hydrogen hub development in line with Infrastructure Investment and Jobs Act’s US$7 billion hydrogen hub funding.14

The O&G industry’s disciplined, high-return capex strategy may initially yield gradual shifts. But if policies are swiftly implemented and consumers rapidly adopt practices that bolster the scalability and commercial viability of low-carbon solutions, it could fundamentally reshape the medium- to long-term capital allocation strategies of O&G companies.

2. Critical minerals: Participating in the energy transition by securing a position in the supply chain to tackle perceived end-market risks

Global clean energy investments crossed the US$1 trillion milestone in 2022, propelled by favorable policies and open trade of energy resources and critical minerals.15 This growth in renewable energy is driving a surge in demand for critical minerals, with lithium demand tripling between 2017 and 2022, and cobalt and nickel demand increasing by 70% and 40%, respectively, during the same period.16 However, as investments in renewables pick up pace, especially against the backdrop of a shifting geopolitical landscape, they not only heighten the reliance on these minerals but also underscore the urgency to strengthen their ownership and supply chains. This imperative may be particularly notable for nations with ambitious clean energy targets and a substantial dependence on imports (figure 3).

{kind=link}

What’s in it for O&G companies?

Securing feedstock supply is crucial for the O&G business model, and it has often involved backward integration or long-term contracts. However, with renewables, whose returns are relatively modest, global O&G companies face additional challenges relating to mineral production and processing concentration. Indonesia dominates nickel mining and processing. China, on the other hand, dominates the market in graphite (100%), lithium and cobalt (65% to 75%), and rare earth elements (90%) processing (figure 3).17 To strengthen their control over the supply chain, nearly 80% of surveyed O&G executives are considering securing clean energy manufacturing and critical mineral rights, thereby leveraging their expertise in subsurface and reservoir management and their regulatory knowledge.18 In addition, participating in the clean energy supply chain can allow companies to continue participating in commodity markets, instead of taking on additional risks in end markets.

Furthermore, rising lithium demand, which is expected to double over the next two decades, is contributing to the interest of O&G companies in lithium extraction from brine (an oil field byproduct), which offers higher margins compared to conventional hard rock minerals.19 For instance, Occidental Petroleum, via its joint venture TerraLithium, and ExxonMobil are securing US acreage for brine-based lithium extraction.20 This may offer significant investment potential for technologies such as Direct Lithium Extraction (DLE) that offers lithium recovery rates up to 90%. Some estimates suggest that around 13% of world’s lithium could be produced using DLE by 2030.21

Proceed with caution

Fostering capabilities in critical minerals, especially lithium, can present O&G companies with synergistic opportunities. However, to capitalize on these emerging opportunities, the companies need to develop mitigation strategies for certain risks:

- Low water resources: Over half of the current lithium and copper production is concentrated in regions facing high water stress levels.22

- High lead time: Developing a new mine is often a time-consuming process due to various regulatory and technical challenges. Owing to these, the average lead time from mineral discovery to first mineral production is estimated to be around 16 years.23

- Lack of diverse supply sources: High concentration on a few countries for resources increases risk exposure. This concern is heightened for lithium, cobalt, and rare earth elements, for which the top three producing nations account for over 75% of the global supply.24

- Delays in permitting processes: Delays and protracted permitting processes, along with litigation battles, are impeding the mining of critical minerals. The average time for permit approval stands at 4.5 years, and this duration can be significantly longer for projects involving critical minerals and mining.25

- Changing demand patterns: Technological innovations can slow demand growth for some critical minerals or even cause cessation of use altogether. For example, different EV battery designs have led to shift from the use of nickel-manganese-cobalt cathodes to lithium-iron-phosphate cathodes.26

3. Global energy trade: Embracing the growing dynamism in energy trade and relationships

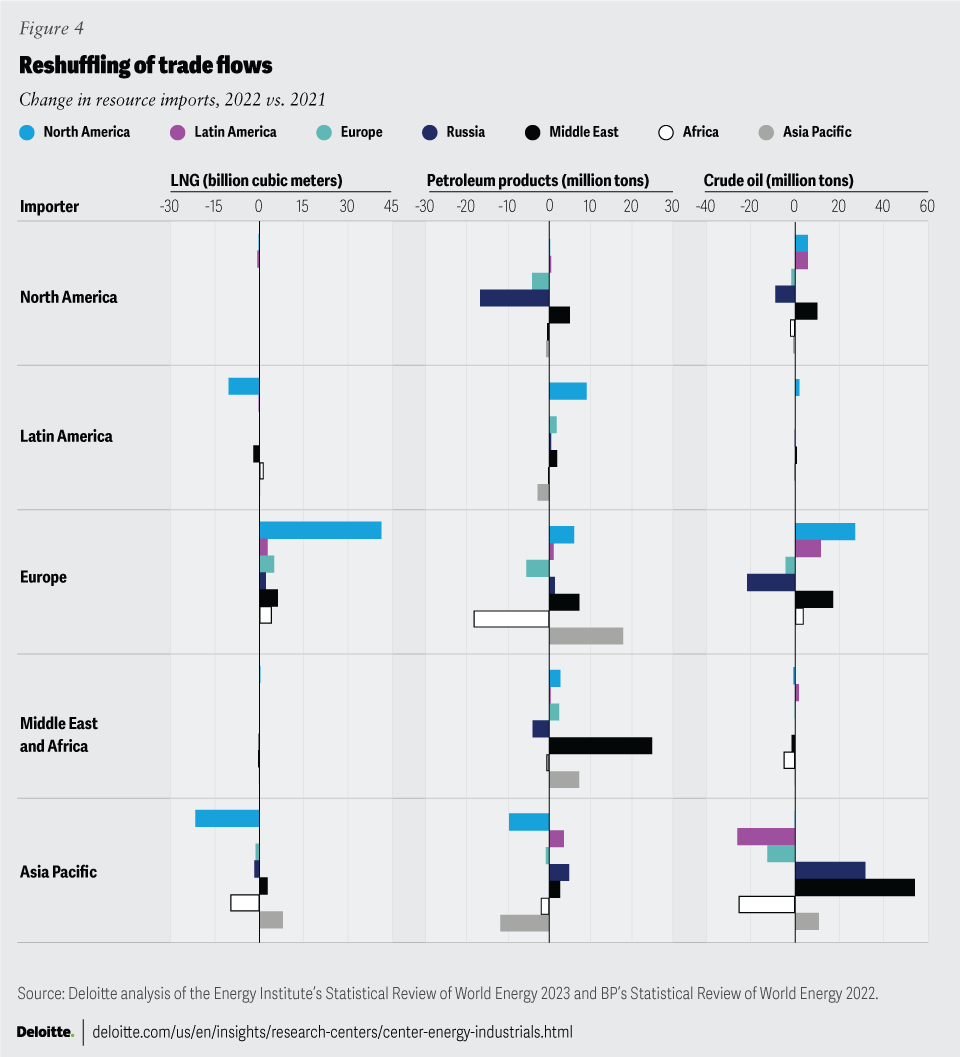

Traditionally, energy trade flows have been driven by market forces, specifically the interplay of supply and demand and the availability of storage and transportation infrastructure. But since the onset of Russia-Ukraine war, we’ve seen disrupted trade flows that have led to new energy trade flows, which, in turn, have affected price differentials and regional industrial competitiveness.27 However, most recently, the situation evolving in the Middle East may emerge as a significant geopolitical risk to oil markets (figure 4). In particular, market observers highlight major implications for trade if the situation in the Middle East were to escalate.

{kind=link}

Evolving energy landscape

The growing dynamism in energy trade and relationships is influencing three key factors:

- Changing energy trade flows: In 2021, Russia accounted for 27% of the EU’s oil imports and 45% of its natural gas imports, primarily through cost-effective pipelines.28 But the EU’s sanctions on Russian energy exports have increasingly driven the exports toward Asia-Pacific, primarily through seaborne trade.29 For instance, the share of Russia’s crude oil exports to China and India has increased from 20% before the war in Ukraine to 70% in November 2022.30 On the other hand, the United States’ LNG exports to Europe have increased by 141%, or 4.0 Bcf/d, compared to 2021, while the United States’ distillate fuel exports to Europe increased by 146% during the first half of 2023 compared to the same period in 2022.31 As Europe continues to lessen its reliance on Russian energy, a surge in maritime energy trade can be expected, with some analysts estimating 90% utilization for both crude and product tanker fleets compared to 88% and 84% in 2023 and 2022, respectively.32 Moreover, the evolving energy dynamics in the Middle East may contribute to sustained energy price volatility in 2024.

- Widening price differential between markets: Following the sanctions, the price differential between Brent and Urals crude oil widened from US$3/bbl in 2021 to more than US$37/bbl in April 2022. However, it has narrowed since then and, as of late 2023, remains above US$17/bbl.33 Similarly, Dutch TTF-to-US Henry Hub natural gas price ratio has increased from three to eight between January 2021 and August 2022.34 This price differential between grades and regions has likely altered the competitiveness of refiners, chemical companies, and manufacturers worldwide. In fact, unprecedented divergence is currently exhibited in refining margins between developed and developing nations, ethylene crack spreads from ethane versus naphtha, and the purchasing manager’s index.

- Growing energy trade in multiple currencies: An increasing number of bilateral energy deals are happening in the local currencies of importing or exporting nations. Many Asian nations, for instance, have started settling energy trades in their own currencies.35 In fact, the alternative currencies trade such as the ruble-yuan increased eightyfold, albeit starting from a low base, between February and October 2022.36 As trade flows and geopolitical alignments continue to evolve, there could be a continued uptick in local currency settlements in energy transactions. This marks a potential transformation in the energy market landscape, which holds implications for currency markets and the trade balance of nations as well.

4. Technology adoption: Harnessing the power of generative AI for innovative solutions and new value creation

The O&G industry has often been at the forefront of adopting cutting-edge technologies to bolster operational efficiency, curtail costs, and advance safety and sustainability measures. In recent years, artificial intelligence (AI) has emerged as a transformative force for the industry, with applications across the O&G value chain, from initial resource exploration to the intricacies of refining processes. Among applications, AI-driven predictive maintenance is instrumental in achieving a multitude of objectives, including cost reduction, heightened productivity, and the assurance of operational reliability for the industry.37 The industry now stands at the threshold of a new AI frontier—generative AI.

Generative AI: The next frontier

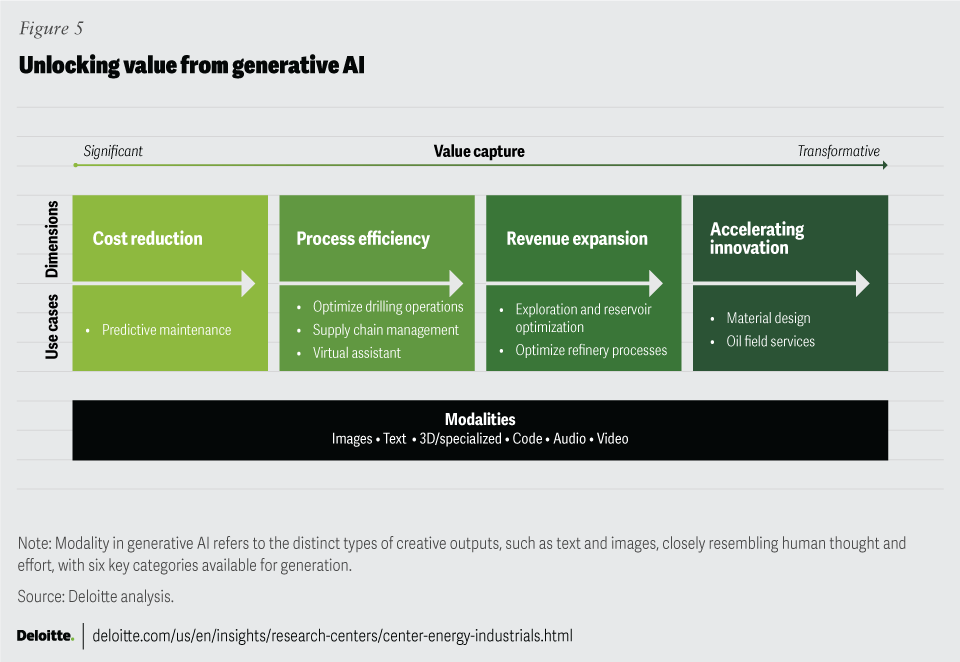

The Deloitte AI Institute defines generative AI as “a subset of artificial intelligence in which machines create new content in the form of text, code, voice, images, videos, processes, and even the 3D structure of proteins."38 The value of generative AI for the O&G industry can be categorized into four dimensions: from immediate cost reduction, to enhanced process efficiency, to the creation of new revenue streams, ultimately culminating in the acceleration of innovation-led change within the company (figure 5).

- Cost reduction: Generative AI-driven solutions could aid O&G companies in cutting operational costs, especially in addressing challenges related to unplanned downtime. For context, a 200,000 bpd offshore platform experiencing about 12 hours of unplanned downtime can result in deferred production worth up to US$8 million.39 Generative AI can go beyond traditional AI by generating comprehensive maintenance plans, task lists, and real-time recommendations. This helps not only curb unplanned downtime but also minimize resource wastage caused by equipment failures, thereby extending the life span of assets.

- Process efficiency: Generative AI could enhance efficiency by integrating and analyzing diverse data sources. It can help proficiently process vast quantities of data, including geological and subsurface information such as seismic surveys, well logs, and historical drilling records, leading to optimized drilling processes.

- Revenue expansion: Generative AI can help pave the way for increased revenue generation. It has the potential to optimize the exploration of high-yield reserves and enhance recovery from the existing ones. In seismic data analysis, generative AI could contribute to generating missing or incomplete samples, refining interpretation, and elevating overall data quality. In reservoir characterization, it can create highly detailed 3D models that simulate reservoir behavior for recovery maximization. The collaboration between Shell and SparkCognition, for example, employs deep learning for subsurface imaging, thereby unlocking new areas and drastically shortening exploration timelines from nine months to less than nine days.40

- Accelerating innovation: Generative AI can help expedite the development of new solutions by enabling rapid testing of new ideas and concepts. For instance, in the downstream sector, generative AI applications can accelerate the production of diverse materials with higher efficiencies and reduced energy and material consumption, fast tracking the experimental process. Moreover, a generative AI–designed digital twin model of planned pipelines can simulate numerous scenarios and optimize the design, thereby potentially reducing the need for physical prototyping and enhancing overall efficiency, safety, and sustainability. In fact, oil field services companies can leverage their existing technology relationships to develop and offer the technology solution as an add-on to their services within as well as outside the O&G industry.41

{kind=link}

Harnessing value across these dimensions using generative AI can enhance operational sustainability for O&G companies through carbon emissions monitoring, energy efficiency optimization, and waste reduction while also predicting emission intensities across their supply chain. The industry can likely benefit from proactively addressing cybersecurity challenges, adapting to evolving regulations, and ensuring data quality when integrating AI technology.

5. Downstream industry: Revamping the refining industry in alignment with evolving demand patterns

The four disruptors shaping the energy landscape (geopolitics, economics, regulatory, and technology) have also impacted the global downstream petroleum sector. This situation is likely further exacerbated by the decline in global refinery capacity, which shrunk by 4.5 mbpd since 2019, with the United States’ refining capacity falling by 1 mbpd since the COVID-19 pandemic due to numerous factors, including the pandemic’s impacts, hurricane damages, weaker future demand forecasts, high operations costs, the inability to complete sales, or conversions to produce more renewable fuels.42

The refining industry now faces a pivotal moment, as the industry is producing and bringing to market new products to offset expected longer-term decline in transport demand for fossil fuels and, thus, adopting even more of a customer-centric or end market–oriented approach. Therefore, a blend of low-carbon fuel alternatives, from biofuels and hydrogen to chemicals, alongside a redesigned forecourt experience catering to evolving fuel mix and customer base is becoming important to the success of the downstream industry.

Global oil demand is projected to slow down in the long term, rising annually by only 0.4 mbpd until 2027, compared to 1.6 mbpd until 2023. Meanwhile global biofuels demand is projected to rise by 44% between 2022 and 2027 as it increasingly substitutes for petroleum-based products.43 In addition, the share of EVs in global car sales is expected to range between 62% and 86% by 2030.44 In response, many global automakers are reorienting to electrify large portions of their product portfolios.

Crafting niche capabilities

The gap between rising low-carbon fuel alternatives and slowing but still positive oil demand expansion can offer a window for refiners to plan their transition without risking the disruption of financial stability. Therefore, refiners could play a transformative role by crafting strategic pathways and cultivating new capabilities within the following distinctive realms:

- Biofuels: O&G refiners already operate nearly 80% of the current global renewable diesel capacity.45 However, they may grapple with the task of effectively leveraging subsidies and grants for strengthening the biofuel supply chain. Therefore, considering strategic steps such as securing a consistent feedstock supply, handling grade fluctuations, and optimizing transportation expenses and emissions can facilitate the efficient expansion of biofuels and set refiner performance apart. A case in point is Marathon Petroleum Corporation’s joint venture with ADM, which involves a specialized soybean processing facility to yield refined vegetable oil feedstock for renewable diesel production.46

- Hydrogen and ammonia: Green hydrogen and ammonia could present refiners with a compelling opportunity to not only curtail emissions but also decrease heating expenses, while broadening their product portfolio for industrial clientele. In fact, BP is reportedly mulling green hydrogen production at its Cherry Point facility, which could help reduce emissions by around 460,000 tons carbon dioxide equivalent per year.47

- Electric vehicles: In addition to deploying EV charging stations and offering new mobility services at their retail outlets, leading refiners have a unique opportunity to explore various applications within the EV sector. For example, Phillips 66 is leveraging specialty coke to craft high-performance anode materials for the production of lithium-ion batteries.48

- Chemicals: Amid increasing electrification, leading refiners could reconfigure their product portfolios, prioritizing items such as chemicals that have fewer readily available low-carbon alternatives. For instance, ExxonMobil plans to boost distillate and chemicals production at its Singapore and UK refineries, while reducing fuel oil and high-sulfur petroleum production.49

- Carbon capture, usage, and storage (CCUS): Refinery and chemical organizations can leverage carbon capture for mitigating emissions from units such as steam methane reformers, catalytic crackers, and combined heat and power systems. For instance, Air Liquide, Air Products, ExxonMobil, and Shell are targeting to capture 2.5 million tonnes/year at Porthos CCUS in Rotterdam.50

In conclusion, downstream players that adapt their strategies in alignment with evolving demand trends and prioritize the security of the supply chain could achieve success in the energy transition.

What can the industry expect in 2024?

Given the healthy cash flows, robust financial health, sustained capital discipline, and rapid technological progress in the industry, O&G companies seem relatively well positioned to increase focus on the energy transition in 2024. This may entail concerted efforts to curtail emissions from hydrocarbons while augmenting investments in scalable and economical low-carbon solutions. In 2024, O&G companies should consider the following in their key decision-making:

- State of the economy: Any sharp movement of the US dollar against other currencies, combined with the trajectory of manufacturing activity and consumer spending, could impact inflation, thereby also influencing energy prices in 2024. Additionally, strong job growth could impact wage increases and contribute to higher inflation. These factors could play a role in shaping the dynamics of energy trade and influencing the competitiveness of energy-dependent downstream sectors worldwide.

- Shifts in geopolitical and regulatory landscape: The interplay of OPEC and its partners in managing energy supplies, alongside the situation in the Middle East, can significantly influence the equilibrium of hydrocarbon supply and demand. Other trends to watch include the level of hydrocarbon exports, especially LNG from the United States, and any regulatory changes that could impact clean energy initiatives.

- Technology affecting automotive and mobility trends: The trajectory of EV sales worldwide (which is exhibiting some signs of weakness, as reflected in rising EV inventories, despite price cuts by automotive companies), shifts in mobility patterns, innovations in battery technology, changes in the EV value chain encompassing raw material sourcing and manufacturing, and advancement in engine technologies, including internal combustion engines, may influence the business models and investment strategies of petroleum refining and marketing companies.51

- Deployment of upstream capital: How and where global upstream players deploy their capital in 2024 will likely signal fundamental changes in their investment and payout strategy, portfolio composition, and fuel priorities for years to come. Additionally, the market is expected to closely monitor how companies distribute their green capital between renewable electricity sources and alternative low-carbon options such as energy storage, CCS, hydrogen, and biofuels.

- Rig and supply responsiveness impacting operational efficiencies: As of October 2023, the US O&G rotary rig count stood at a yearly low of 623,52 demonstrating limited responsiveness to recent changes in energy prices. However, in 2024, the market will closely monitor the rate of and lag in operators’ responses, especially those of private operators. In addition, the availability of rigs and the contractual rates for these rigs will help gauge the level of activity and operational efficiencies in the US shale.

- Merger and acquisition and joint venture activities: The proposed acquisitions of Pioneer Natural Resources by ExxonMobil and of Hess Corp by Chevron Corporation for $64.5 billion and $60 billion, respectively, may usher a new era of megadeals and consolidation in the US upstream industry.53 Strong O&G prices and limited drilling inventory (notably, as of October 2023, the number of drilled but uncompleted wells in the United States shale basins stood at 4,524, a 10-year low) may prompt a few large buyers to acquire new acreage and pursue enhanced operational efficiencies through mergers and acquisitions.54 Meanwhile, amid regulatory and geopolitical uncertainties, coupled with elevated capital costs, other entities may opt for a cautious wait-and-see strategy. An analysis of recent upstream deals reveals that, following company mergers, both buyers and sellers have collectively downsized their rig fleet by 30%.55