Asset Management Survey has been saved

Article

Asset Management Survey

The gold rush route for asset managers

As the world emerges from under the cloud of the COVID-19 pandemic, the asset management industry has not only weathered the storm but, despite significant challenges, emerged stronger. Deloitte Luxembourg, in conjunction with Deloitte Ireland, launched its biannual survey among European investment management industry players to gain a holistic view of recent challenges, understand today’s market needs, and to anticipate future trends.

The latest edition, focusing on asset managers, welcomed the participation of 11 global players headquartered in five countries across Western Europe with a combined €9.7 trillion of assets under management (AuM). The participants were a representative sample of the industry, covering a range of organizations including liquid-only or illiquid managers, those belonging to larger financial groups, independent firms, or insurance companies, and those who manage either in-house or third-party funds.

The main takeaways from this year’s survey included asset managers reporting a mostly positive impact of the pandemic with higher productivity, increased employee satisfaction, and accelerated digitalization contributing to 80% of those questioned seeing an increase in revenue in the past three years. In light of investor expectation and regulatory pressure, the interest in ESG and sustainability products continues to grow, whilst asset managers intend to more than double their allocation in real assets, in particularly infrastructure and commercial and residential real estate.

Find out more by downloading the EMEA Asset Manager Survey.

Find the alternative track

Investors are increasingly investing in low-cost passive funds which have reached nowadays the same return than active funds. Asset managers’ choice to survive now lies between specializing on high-end niche markets to justify higher fees or gaining scale to provide passive investments at very low cost. To face the fee pressure resulting, most of asset managers are going towards alternative products (Private Equity, Real Estate, Private Debt).

of asset managers are offering to investors passive or active ETFs today.

of respondents expect to increase significantly their offering of active and passive ETFs over the next 3 years.

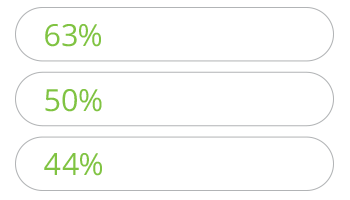

of asset managers are distributing Private Equity and Real Estate products today. The demand for this type of asset classes is expected to grow within 3 years, especially in 2 geographical area:

Engage in ESG – a game changer

However, investors are ready to sacrifice performance when they invest in active sustainable funds, which provide long-term impact and meaning to their savings.

of asset managers include ESG characteristics in their current portfolio, covered via all asset classes and specifically vanilla products

asset managers are using the top 3 below strategies in their Sustainable and Responsible Investments

of all asset managers intend to increase their proportion of Sustainable and Responsible Investments in the next 3 years

Data

remains the main challenge for asset manager when integrating ESG characteristics in their portfolios

of asset managers are using their own internal research team or/and relying on external data providers to collect the ESG data to support their decision-making process

of asset managers are using labels, certifications or flags to identify ESG investments

IS DATA THE NEW GOLD?

To build these customized portfolios with a thematic-approach, asset managers are trying to collect investors’ data, either depending on the data provided by their service providers or by increasing direct distribution to reach investors directly.

Asset managers are trying to improve their offerings’ customization through investors data collection

of asset managers consider investor information (age, wealth, etc.) and asset data (price, volatility, etc.) the most important data for their business

however this data lies within their service providers’ hands

of asset managers are dissatisfied with their service providers’ digital capabilities

As a result, some asset managers are considering to re-insource some activities thanks to technology

of asset managers would re-insource investor reporting or register maintenance if they had the appropriate technology in place

DATA COLLECTION THROUGH DIRECT DISTRIBUTION

of asset managers rely today on direct distribution

of asset managers cover more than 50% of their sales through direct distribution

of the asset managers are likely to increase their proportion of direct sales in the next 3 years

Get in touch

Recommendations

Integrating to add value in asset management M&A

More perfect unions resulting from industry M&A

Forward-looking solutions for tomorrow’s leading asset management firms

Ahead of the curve