Pandemic observed risks and preparedness

The unprecedented Covid-19 pandemic swept the world putting most of the globe into containment measures and threatening the global economy with slowdown or even worse, shrinking.

The unprecedented Covid-19 pandemic swept the world putting most of the globe into containment measures and threatening the global economy with slowdown or even worse, shrinking. Now, measures are starting to lift gradually and provide more flexibility with expected almost return to some normality by June, however the situation is still difficult and the fear is for a return of the outbreak in autumn. All this poses a threat to the Albanian economy with enterprises suffering the losses from the total lock-down until now.

The government prepared two main economic packages to help the economy. Nevertheless, it followed in the aftermath of the earthquake that hit the country in November 2019, which caused considerable economic damage and reallocated many funds to recovery and reconstruction. This coupled with other easing measures to hold collection of some revenue streams to the budget and uncertain foreign help donations will further limit the ability to pour extra cash in the economy.

In such conditions and future ambiguity, preparing for the worst-case scenario is imperative. Enterprises should take decisions swiftly and timely as the situation evolves. In this article set forth the background for more in depth analysis of the implications and responses that need to be taken from Albanian enterprises in order to be resilient to upcoming difficulties.

1. The main risks and scenarios

Some of the main contributors and growers sectors to the GDP, are also some of the most affected by the crisis: Agriculture, Trades, Production, Leisure & Accommodation. Apart from that, Tourism is a main contributor to improving the trade deficit we develop. Therefore, apart from GDP slowdown and decrease, our payments balance may take a hit as well due to the nature of our economy based on mainly imports. But going into enterprises operating level, other risks become threatening.

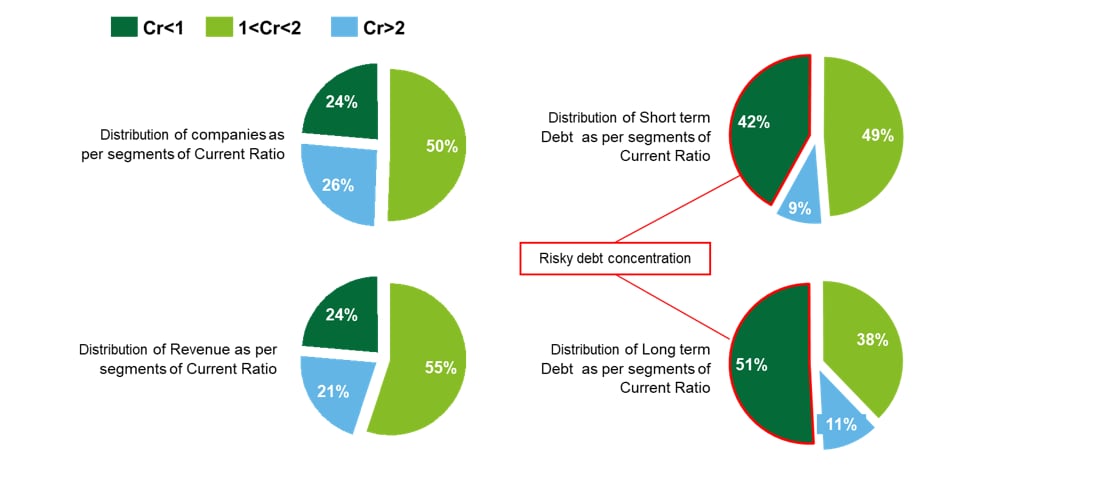

In 2018, we have released the Benchmarking & Financial Health Study (2014-2016) for 230 biggest companies in Albania. Due to economy developments, we do not expect many changes in the structure of companies’ financials and operations. The conclusions of the abovementioned study remain relevant, thus they help us in the analysis of current events impact and resilience actions.

Our main finding was that “companies in Albania operated at volatile cash flow”. Account payables and account receivables held the greatest share of respective short-term debt and assets. Overall, companies were focused in managing profits and not cash flow, revealing difficulties covering short-term debt through operating cash flows. Deducting from this we concluded that supply chains were highly interconnected. Due to this, a major hit could be transferred along the whole supply chain like a domino effect.

Poor cash management shown may mean that enterprises are vulnerable to major hits to financial stability. Tirana & Durres regions, which concentrate also the vast majority of enterprises, experienced also the bulk of the earthquake shock, increasing the risk of financial disruption. Intertwined ties within supply chain through high percentages of mutual debt in the form of payables and receivables may expand the financial threats, especially associated with low financial health performers throughout the market. In addition, from our study, 81% of biggest companies, classified as medium to poor financial health. This increases the risks of short-term financial difficulties extending to the whole supply chain and affecting good performing companies as well, despite their size.

The current situation is expected to hit all industries in the short term and probably affect greatly in the midterm as well. We predict 3 main overall risks that will be associated.

Time and money

Length uncertainty is the greatest risk that leads enterprises to vulnerable decision-making and whose impact will be felt on all aspects and especially financial stability of enterprises. Even more threatening is the risk of a re-emergence of the virus during the second half of the 2020. This will hit hard on enterprises cash and reserves forcing them to face perilous decisions. In the worst case scenario, enterprises may fail to generate enough cash to operate and service their debt leading them to facing failure.

As per our benchmarking analysis, top companies in Albania generally operate at positive short-term debt coverage. However, a considerable part of short-term debt and most of long-term debt were concentrated in companies operating in poor liquidity ratios. Coupled with the short-term debt mainly being payables and receivables, cash difficulties of these “risky” companies can start a chain reaction in the whole market.

Customer behavior and demand

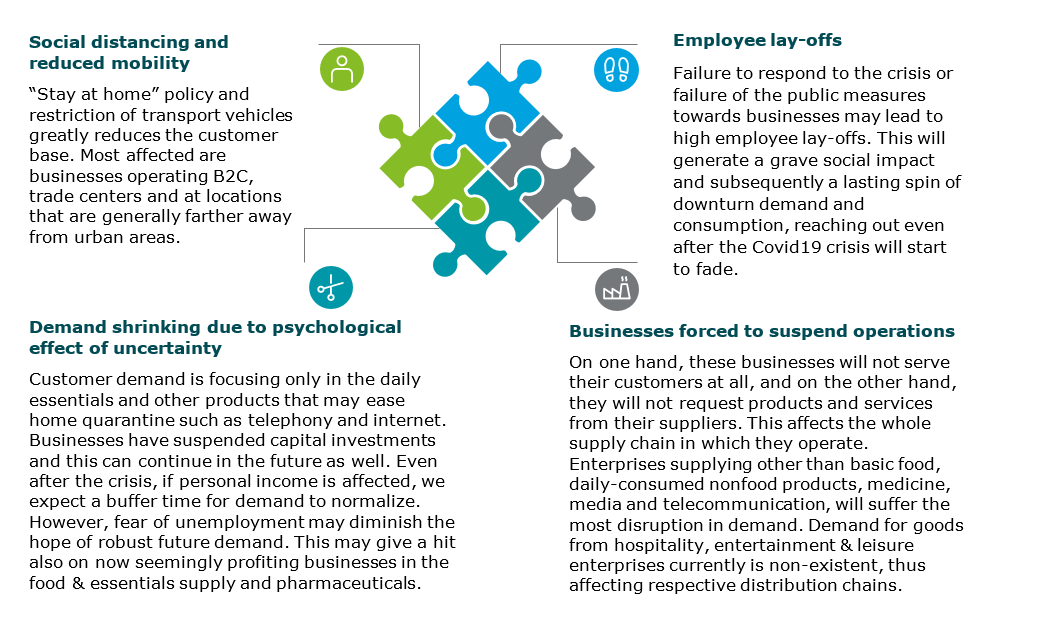

The evolution of the situation and the events of the days since the quarantine enforcement, four main factors showed to affect customer behavior:

If markets enter such a downturn vicious circle of diminishing income, leading to diminishing demand and vice versa, all businesses will be affected in the long-term.

Supply chain disruptions

Inducted disruptions from international trade slow down have not yet shown full effects on our economy. However, even without significant barriers on international trade, the economic effects and demand diminishing may affect the producers globally. This in turn will disrupt supply chains in Albania as well with lack of raw materials, machineries and products. Furthermore, suppliers may exert pressure to Albanian enterprises to liquidate payables or pay upfront for new orders leading to worsening cash position and supply disruption.

Internally, more imminent threats derive from the above-mentioned risks. The most vulnerable are industries operating in seasonal products, intangible goods and fast product cycles. This also means that some of the most important contributors to the GDP are mostly threatened: agriculture, trade, production, especially those that produce for export. Also one of the top growers, Hospitality & food service, with uncertain predictions for tourism influxes this year, risks to disrupt the whole HoReCa supply chain.

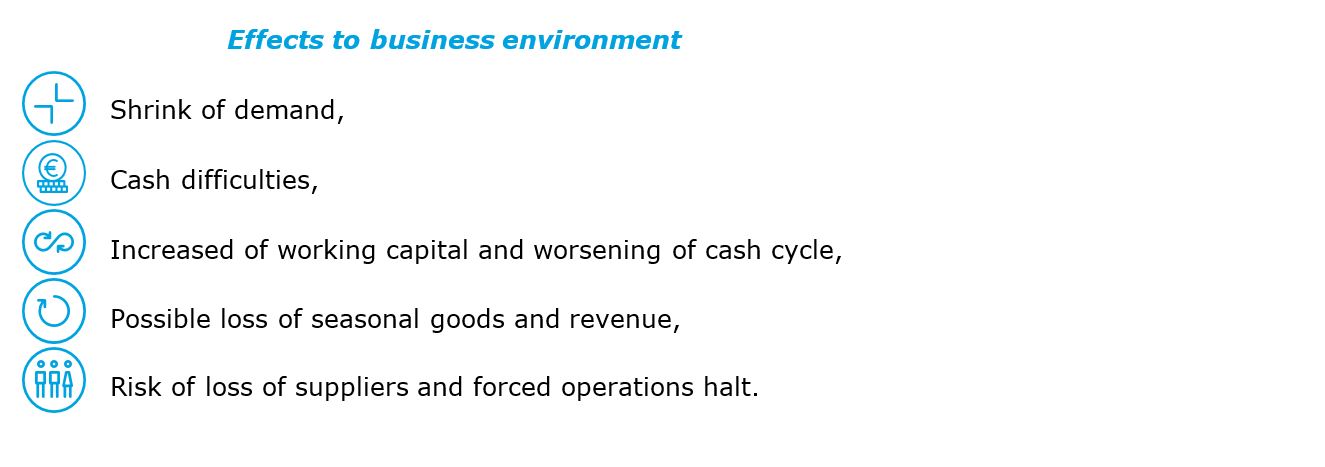

In the mid and long-term, even in the best-case scenario, we can expect serious effects to enterprises environment.

2. The crisis evolution

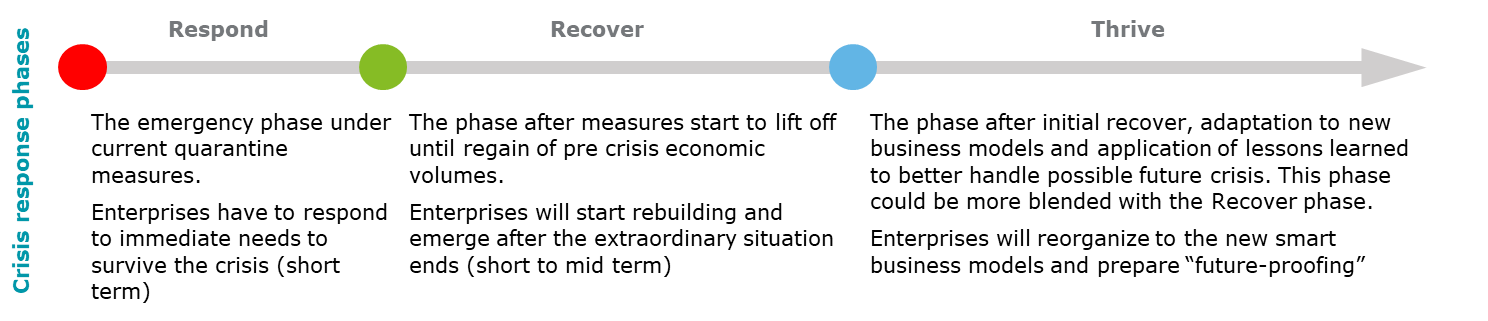

Based on our extensive global experience in working with enterprises across industries and in multiple geographies, as well as on crisis management and lessons learned from previous events, we can distinguish 3 main phases that this crisis will unfold.

3. Company readiness

We expect that companies with robust risk management measures and business continuity plans will handle better the effects of the crisis. Such companies, if operated with good cash management and inventory strategies, may overcome short-term difficulties and focus on the longer term impacts. In addition, companies operating under group structures, where the group has diversified supply chains and product portfolios, can cover for losses and supply disruptions, thus better responding to the crisis impact.

Enterprises that have put in place robust processes supported by technology and smart ways of work have better responded to the crisis and quick decisions for change that they faced. Such companies have a better understanding of their business and supply chain. Implemented technologies allow them to have prompt information, analysis and quick strategic adaptation.

We expect companies that will struggle the most are mainly small family run businesses and SMEs. This group, due to their size and market position, did not have the need to design supply chain, cash and risk management strategies. This does not spare bigger companies and corporations, which as well have not employed such optimizations to their business though. These companies may also feel the impact of the crisis more in the long-run, as cash reserves start to deplete and market operations disrupt, the lack of clear strategies, planning, processes, risk management and Information Systems support may prolong the operating difficulties long after the full lift of containment measures.

Get in Touch