Financial Markets Regulatory Outlook 2017 has been saved

Artigo

Financial Markets Regulatory Outlook 2017

A guide to navigating the year ahead

Our annual assessment from Deloitte’s Centre for Regulatory Strategy, EMEA, delves into the challenges and opportunities arising from the key regulatory issues facing the financial services industry in 2017. In analysing each issue, we also offer a sector-specific view on the impact for banking and capital markets, investment management and insurance.

Explore Content

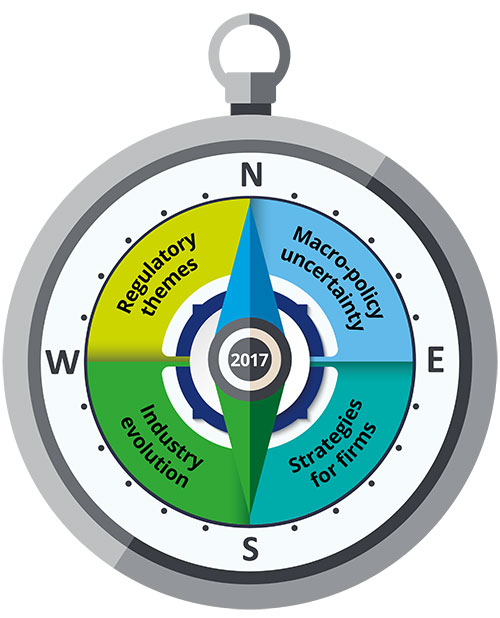

The regulatory outlook

2017 will bring significant challenges to financial services firms across EMEA in the form of heightened macro-policy uncertainty, the implementation of a demanding and still evolving regulatory agenda and other market developments putting pressure on the industry.

Use the compass to explore the issues, and identify ways in which firms can navigate them. A full analysis and sector-specific exploration can be found by downloading the complete report.

Regulatory themes

-

- Resolvability

- Europe test-drives bank resolvability

In 2017, resolvability will become the driving force behind structural reform in the EU. The SRB will push Eurozone banks to demonstrate their practical preparedness for resolution as EU and international regulators step up their work on CCP resolution. Resolution regimes for insurers, however, will be less of a priority.

Explore this issue in further detail in the full report

Further reading:

-

- Financial resilience

- Significant implementation challenges ahead

Following the BCBS's conclusion of most of its work on the risk framework early in 2017, the EU will deliberate how to adopt the new capital standards, while protecting the region's economic priorities. Banks will have to deal with uncertainty over the final shape of the rules as well as enhance balance sheet management capabilities for TLAC, MREL and IFRS9 implementation.

Explore this issue in further detail in the full report

Further reading:

-

- Conduct and culture

- Firms have yet to put misconduct truly behind them

A whole array of frameworks will be introduced to manage conduct risk, instil cultural change and improve product governance standards in 2017. Firms will also work to embed conduct risk appetite into their processes at all levels of their organisation. In addition, conduct risk will be increasingly monitored by prudential regulators as part of ICAAP assessments and stress tests.

Explore this issue in further detail in the full report

Further reading:

-

- Regulation of new technologies

- The tricky business of keeping up with the times

FinTech will continue to change the industry, along with Artificial Intelligence and data analytics. Innovative entrants will find more support from European and national regulators, who will also investigate the potential risks associated with them. While PSD II presents many business opportunities, both FinTech firms and retail banks will find its implementation challenging, in part because of the lack of specificity in some of its provisions.

Explore this issue in further detail in the full report

Further reading:

-

- Cyber and IT resilience

- More specific and more demanding

Spurred by a number of high-profile attacks on firms, supervisors will increase their focus on cyber resilience. Supervisory expectations will include more detailed planning for responses to scenarios such as cyber breaches and technological failures. Firms will increasingly use testing, war-gaming and red-team exercises to demonstrate the robustness of their resilience plans.

Explore this issue in further detail in the full report

Industry evolution

-

- Opening up markets

- Vulnerable incumbents

Increased competition and the higher degree of transparency and disclosure on products and pricing under MiFID II and PRIIPs will shift the ground for all firms providing investment products. In the UK, the introduction of pension freedoms will intensify competition between life insurers and investment managers in the retirement market. Banks will need to determine their strategic positioning following strengthened competition in the payments market.

Explore this issue in further detail in the full report

Further reading:

-

- Evolution of the trading landscape

- Decision time for trading strategies

The introduction of new trading venues and the entry into force of the clearing and margining requirements will reshape how firms develop and execute their trading strategies. The authorisations and registrations for trading venues in preparation for the implementation of MiFID II will further play a crucial role. Firms will also choose to clear an increasing volume of OTC derivatives centrally.

Explore this issue in further detail in the full report

Further reading:

Macro-policy uncertainty

-

- Brexit

- Prolonged uncertainty is here to stay

The picture for EU market access remains unclear for firms assessing the impact of Brexit on their business model and strategy. While supervisors in the UK and EU will be watching firms' preparations and actions closely, we do not expect regulatory changes while the UK remains a member of the EU. In the light of continuing uncertainty, firms may decide to start implementing their contingency plans during 2017.

Other drivers of macro-policy uncertainty:

- Low growth and subdued interest rates

- Political risk and policy volatility in developed markets

- Rising challenges to the free movement of capital and services across borders.

Explore this issue in further detail in the full report

Further reading:

Strategies for firms

-

- Controls efficiency

- The rise of RegTech

RegTech promises to enable firms to push down costs, rein in compliance risk and improve controls. However, the effective implementation of RegTech solutions will require up-front investment that may be hard to justify in the difficult commercial conditions that will prevail in 2017. For this reason we expect the adoption of RegTech to be gradual as firms seek to demonstrate how such investment will add value to the business.

Explore this issue in further detail in the full report

Upcoming Centre for Regulatory Strategy point of view:

- Managing conduct risk: Using innovation to address an ever growing challenge

-

- Governance strategy

- Too big to manage?

Boards and senior management teams will come under increasing pressure to show supervisors that they can effectively manage groups comprising a multitude of legal entities and activities spanning numerous countries. Questions related to organisational complexity will be raised, whether on the functioning of intra-group relationships or the ability of subsidiaries to operate independently of their parent company if the need arises. This, however, will be an opportunity for firms to reduce their complexity and, in so doing, become more manageable organisations.

Explore this issue in further detail in the full report

Upcoming Centre for Regulatory Strategy point of view:

- Too complex to manage?: Global bank governance in a structurally reformed world

-

- Business model sustainability

- Accelerating strategic change

In re-shaping their business models, firms hold the key to managing costs and restoring returns. As firms respond to the need to address new regulations and tackle increased macro-policy uncertainty, they will need to re-shape their financial resources to allow for strategic flexibility and efficiency. Supervisory and resolution authority discussions will add further pressure to integrate regulatory compliance, stress testing and resolution planning more comprehensively into business strategy and strategic planning.

Explore this issue in further detail in the full report

Upcoming Centre for Regulatory Strategy point of view:

- Balance sheet optimisation: Using regulatory change to power performance

Regulatory timeline tool

Access our interactive timeline tool to receive a high-level view of recent and upcoming regulatory milestones for the financial services industry. The tool also provides links to related Deloitte analysis and insights.

Webcast: Exploring the outlook

To discuss the Outlook’s predictions and their potential impact on the financial services industry in 2017, leading partners from Deloitte were joined by JP Morgan International Bank Chairman Clive Adamson and Standard Life Group CRO Raj Singh at the report launch for a webcast which can be viewed here.

About the EMEA Centre for Regulatory Strategy

The Deloitte Centre for Regulatory Strategy is a powerful resource of information and insight, designed to assist financial institutions manage the complexity and convergence of rapidly increasing new regulation.

With regional hubs in the Americas, Asia Pacific and EMEA, the Centre combines the strength of Deloitte’s regional and international network of experienced risk, regulatory, and industry professionals – including a deep roster of former regulators, industry specialists, and business advisers – with a rich understanding of the impact of regulations on business models and strategy.