ETA's Explanatory Instructions no.78 of 2023 has been saved

Insights

ETA's Explanatory Instructions no.78 of 2023

In a concerted effort to bolster trust and foster cooperation between the Egyptian Tax Authority (ETA) and taxpayers, and in alignment with the Ministry of Finance's steadfast dedication to streamlining processes, bolstering investment, and ensuring the effective enforcement of tax legislation, the ETA released Explanatory Instructions No. (78) in September 2023. These elucidatory instructions serve to provide comprehensive clarification on the stipulations concerning the pricing of transactions involving related parties, as outlined in Articles (12) and (13) of the Unified Tax Procedures Law No. 206 of 2020.

To ensure clarity and seamless implementation of the rules, ETA is taking proactive steps by addressing frequently asked questions with enhanced explanations supported by examples.

Key highlights from the explanatory instructions

1. Local File Submission Deadline

It is vital for taxpayers to understand the specifics, particularly when it comes to the submission of the Local File in relation to the Corporate Income Tax (CIT)

return as explained below:

- According to this explanatory update, taxpayers are mandated to submit the Local File within a timeframe of two months commencing from the date of submission of their CIT return, in accordance with the provisions delineated in Article (31), paragraph (c) of the Unified Tax Procedures Law.

CIT Return Deadline |

TP Documentation Deadline |

30th April |

30th June |

30th June |

30th August |

31st July |

30st Sep |

- Furthermore, in the event of an amended CIT Return submission, the deadline for submitting the Local File remains consistent at two months from the date of filing the amended return. Nonetheless, it is worth noting that the Local File submission deadline will be subject to adjustment should the amended CIT Return be submitted within 30 days from the date of the original CIT Return filing.

To provide a concrete example, if a taxpayer initially files its original tax return on 30 April and subsequently makes amendments to the CIT Return, re-submitting the amended CIT Return by 30 May, the Transfer Pricing (TP) documentation submission deadline will be recalculated starting from 30 May. Consequently, the revised TP documentation submission deadline in this scenario will fall on 30 July.

2. Late Payment Penalties

The latest instructions from ETA offer a critical clarification regarding late payment penalties in relation to TP none compliance penalties, significantly simplifying the compliance process for taxpayers.

- The updated instructions states that late fees, as specified in Article (110) of the Income Tax Law, do not apply to TP none compliance penalties, as outlined in Article (13) of the Unified Tax Procedures Law as amended by law no.211 of 2020.

3. Dividends

To clarify matters further, the ETA has reemphasized the treatment of dividends in relation to related party transactions as highlighted below.

- It is important to note that dividends are not considered part of related party transactions.

This distinction clarifies the dividends treatment and ensures that they are not subject to the TP regulatory framework as other related party transactions. This will also ease the compliance burden on holding companies with dividends transactions only.

4. Transactions Impacting the Balance Sheet

Comprehensive and accurate reporting is key in navigating tax compliance. Considering the provided explanatory guidelines, this section examines a critical aspect which is the reporting of related party transactions that impact balance sheet accounts.

- Related party transactions that impact balance sheet accounts should be meticulously reported and disclosed in Table No.508 of the annual CIT Return. It's crucial for taxpayers to be aware that what needs to be disclosed are the movements associated with the transactions that influence the balance sheet, rather than the balances themselves. This ensures accurate and transparent reporting of related party transactions in compliance with the regulatory framework.

The above clarification will require Egyptian taxpayers to carefully identify their related party transactions that have an impact on the balance sheet.

5. Payments on Behalf

Transparency and accuracy in financial reporting are crucial elements in maintaining tax compliance. Within the context of the explanatory instructions, under this section ETA clarified the requirement of disclosing payments made on behalf of another related party.

- It is imperative to highlight that payments made on behalf of another related party, including profit element (if any), are subject to mandatory disclosure. These payments should be diligently recorded in Table no.508 of the taxpayer's CIT Return, as well as in the Local File.

This dual reporting mechanism serves as a testament to the commitment to adhering to TP regulations and ensuring a high degree of transparency.

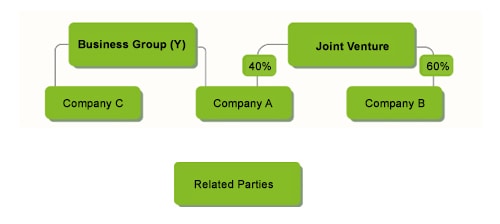

6. Joint Ventures involving Related Parties

Joint ventures are a common form of collaboration in business, especially when it comes to executing specific projects. In this section, the essential aspects of joint ventures, including their structure, composition, and responsibilities is illustrated by the ETA. Additionally, it delve into the vital consideration of related party transactions within joint ventures, which involves specific reporting requirements to ensure transparency and compliance with tax regulations.

- A joint venture is a contractual agreement formed between resident individuals, branches of non-resident companies, or a resident individual and a branch of a foreign company. The agreement is structured based on the proportional shares held by each participant in the project's profits and is exclusively designed to execute a specific project. It is important to note that the joint venture's existence is directly tied to the project's duration, and its core responsibilities revolve around the equitable allocation of gains and losses stemming from its undertaking.

The joint venture can include the following:

* Resident persons;Branches of non-resident companies; and

* Resident person and branch of a foreign company.

- However, a crucial aspect to consider arises when a joint venture involves related parties, as defined under the Unified Tax Procedures Law, and operates within a conglomerate of affiliated companies. In such scenarios, all transactions between the joint venture and other entities within the group must be transparently disclosed in the tax return, specifically in Table no.508. This disclosure requirement extends to both the participating company within the joint venture, up to the extent of its share in the joint venture, and the group company involved in transactions with the joint venture, up to the value of the transaction with the related party and fellow member of the joint venture. This regulation ensures comprehensive reporting and adherence to tax regulations within the context of joint ventures operating within a group structure.

Example:

In Egypt, two resident construction companies, (A) and (B), have joined forces to undertake a collaborative construction project via a joint venture. The distribution of ownership shares within this joint venture stands as follows:

* Company (A): 40% ownership

* Company (B): 60% ownership

- Company (A) is part of a business group (Y). This business group encompasses a multitude of companies engaged in various industries, rendering them interconnected and categorized as related parties within the context of this collaboration.

- Within the business group (Y), one of its affiliates is Company (C), a subsidiary primarily engaged in the provision of construction equipment supplies.

- In the course of the joint venture's project execution, a contractual agreement was established with Company (C), a subsidiary within the business group (Y), for the supply of construction equipment essential for the project. The total value of this equipment procurement by the Joint Venture amounts to 10 million EGP.

- Under the prevailing circumstances, the disclosure requirements for transactions involving related parties within Table No. 508 of the tax return are as follows:

- For Company (A): Given that Company (C) qualifies as a related party due to its affiliation within the business group, Company (A) is mandated to disclose its transaction with Company C. This transaction is valued at 4 million EGP, representing Company (A)'s 40% share of the overall transaction value with Company (C) facilitated through the joint venture.

- For Company (B): In contrast, since Company (B) does not have a related party relationship with Company (C), it is not obligated to disclose any transactions pertaining to this collaboration in its tax return.

7. Subsidiaries of Free Zones Companies

In situations where a parent or holding company operates within the Free Zones system, mainland subsidiaries that fall under the umbrella of such parent or holding company are mandated to prepare and submit the Master File concurrently with the submission of the Local File. This regulatory requirement ensures comprehensive documentation and compliance with transfer pricing regulations for entities associated with the parent or holding company benefiting from Free Zones status.

Conclusion

These recent regulatory updates have been implemented with the primary objective of enhancing clarity and simplifying compliance for taxpayers involved in related party transactions while reemphasizing the importance of following TP regulations. By clarifying submission deadlines, assuring the position of late payment penalties with regards to TP compliance penalties and deadlines, and outlining specific reporting obligations for different types of transactions. Obviously, the ETA aims to streamline the overall process and foster transparency in TP reporting.