Article

Digital Banking Maturity 2020

How banks are responding to digital (r)evolution?

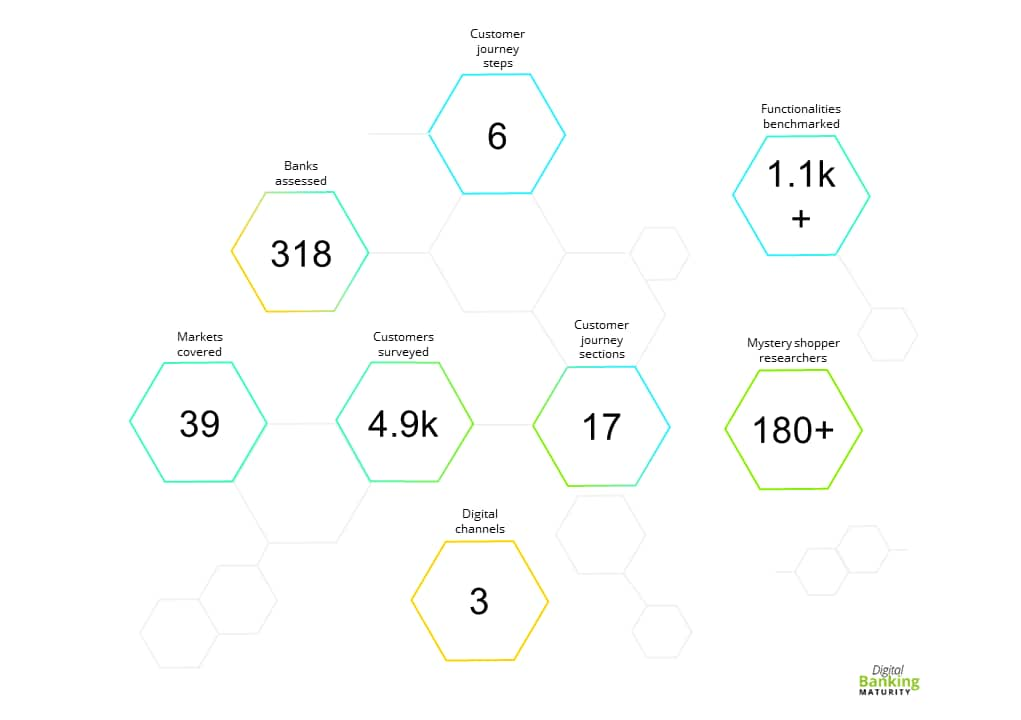

Global benchmarking study of 318 banks in 39 countries on 5 continents.

Digital Banking Maturity 2020 is the 4th edition of largest global benchmarking of digital retail banking channels, answering what leaders are doing to win in the digitalization race. It is providing a comprehensive outside-in ‘mystery shopper’ assessment of retail banks’ digital channels and furthering discussion about future developments.

Digital Banking Maturity is a global accelerator helping banks respond to change

Digital Banking Maturity is the biggest global digital banking study, providing a comprehensive outside-in ’mystery shopper’ assessment of retail banks’ digital channels and furthering discussion about future developments.

Key takeaways

Digital Banking Maturity report 2020

Digital Banking Maturity report 2020

About the study:

DBM analyses digital retail banking channels of 318 banks from 39 countries. In order to compare digital maturity between banks we assessed three components:

- Functionalities benchmarking.

Analysis of 1108 digital functionalities through ‘mystery shopper’ approach on real retail current accounts in each bank.

- Assessment of 6 customer journey steps

- Analysis of digitalization of 13 core banking products

- Functionalities library with world’s leading practices

- Customer needs research.

Survey-based research (4.9k Customers surveyed) focused on identifying 26 most important banking activities and preferred channels (branch, internet, mobile).

- Customer preferences between channels in terms of most common banking activities - User Experience Study.

Supplementing analysis of customers perception of user experience.

- 19 UX scenarios reflecting 10 areas of customer activity form all of the stages of relationship with a bank

- UEQ survey covering a comprehensive impression of UX of mobile apps

If you would be interested in a in-depth findings regarding your financial institution – please contact our experts (contact data available below).