Retooling wealth management for the digital age has been saved

Perspectives

Retooling wealth management for the digital age

A look at consumers’ digital propensity

Much has been written about a new generation of investors and their needs and preferences. We are told that these investors are digitally savvy, and want to consume advice and interact with wealth management firms in new, often digital ways. In our new study, we analyzed the digital interactions investors want, and their propensity to adopt digital offerings and use digital channels.

Digital preferences

We surveyed 2,700 retail investors across various wealth tiers and age groups. We asked them about their digital preferences and measured their responses along various psychographic attributes. We found that:

- Both Mass Market and Mass Affluent investors have relatively high, and similar, digital propensities relative to more affluent segments.

- The key difference between Mass Market and Mass Affluent investors is in the types of digital interactions they prefer, and take part in.

- Within Mass Market and Mass Affluent segments, digital propensity varies more substantially across behavioral sub-segments.

- Based on four psychographic attributes, the Mass Market and Mass Affluent investor base could be segmented into six segments with varying digital propensity.

- Wealth management firms who tailor their digital strategies to these six segments will likely be more successful.

What is Digital Propensity and why does it matter?

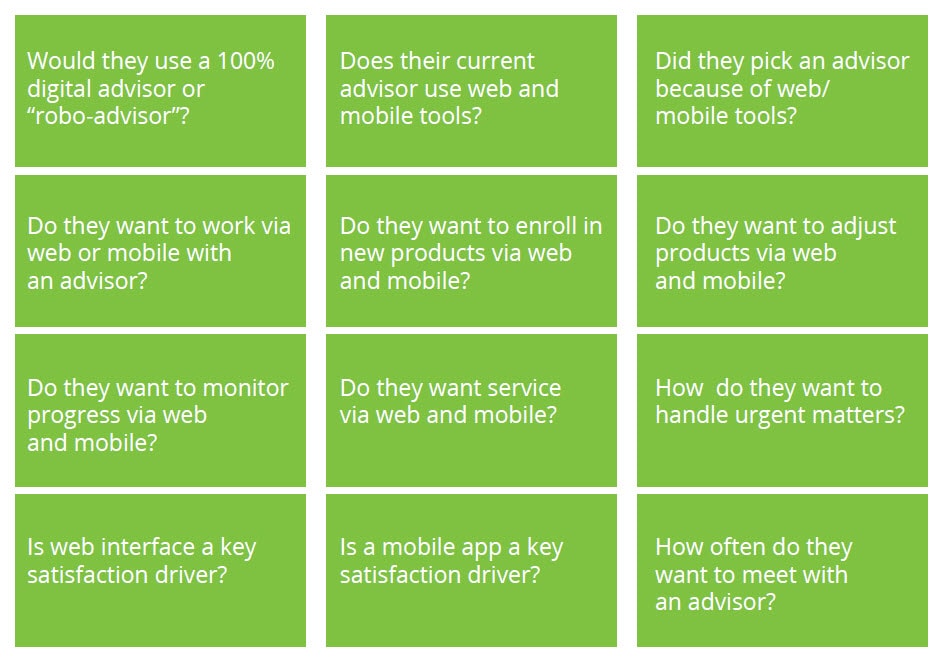

We asked respondents across segments, age groups, genders, and geographies about their desire for digital interaction (via app, mobile, and web) with their wealth manager (current or prospective). We did so with a set of 12 questions and used responses to arrive at a “Digital Propensity” score. The Digital Propensity score is a composite measure of how much, and how often, an individual or segment would prefer to engage with a wealth manager via digital channels rather than via traditional face-to-face or phone channels.

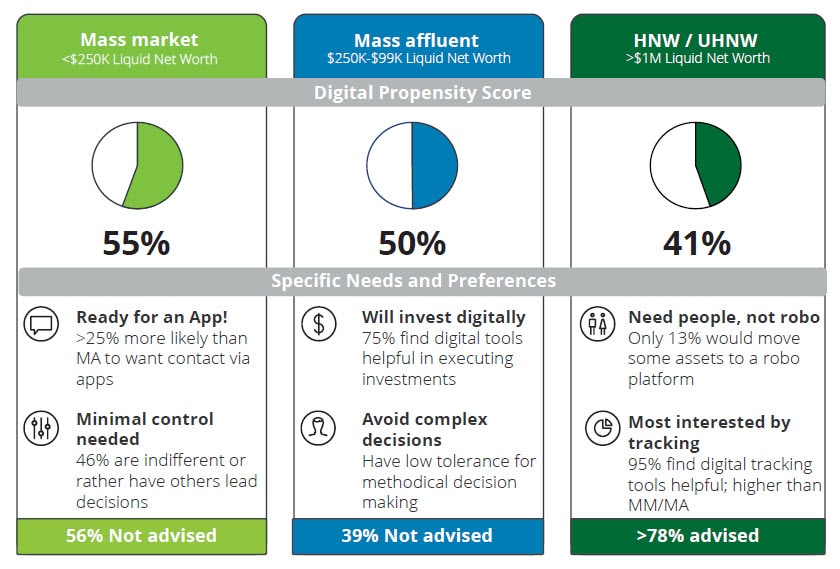

The survey results strongly suggest that the Mass Market and Mass Affluent segments were far more open to the use of digital tools being applied by their wealth manager or advisor than more affluent investors. Readiness for digital does have nuance and variation across the Mass Market and Mass Affluent; however, by and large they are open to the technologies that will allow advisors to serve them effectively.

Survey of investor digital propensity

We measured the degree to which 2,700 consumers prefer to use web and mobile tools to manage their wealth … use web and mobile tools to manage their wealth to get a holistic view of propensity to use digital tools and channels across the customer lifecycle.

Digital needs and preferences by wealth tiers

Understanding how segments think: Four psychographic attributes

To understand the motives and thought processes behind each segment, we asked a series of questions about Future Orientation, Locus of Control, Financial Optimism, and Need for Cognition. We focused on these four attributes because of their relevance to how and why investors think financially.

- Future Orientation is the degree to which an individual has and uses long-term-vision. High Future Orientation indicates a tendency to consider and prioritize the long-term implications of a decision

- Locus of Control is the degree to which an individual prefers to be in control of situations. High Locus of Control indicates a desire to be the decision maker

- Financial Optimism is the overall satisfaction and confidence an individual has in his or her current financial standing. High Financial Optimism both Digital Propensity and psychographic traits. Because of this, we decided to move forward with a deeper sub-segmentation of the Mass Market and Mass Affluent populations. indicates a feeling of readiness for the financial future

- Need for Cognition is the degree to which an individual wants to undertake complex problem solving. High Need for Cognition indicates that someone can and does take a long series of methodical, thoughtful steps to solve a highly complex issue, versus feeling too busy to do so

Six Segments (across Mass Market and Mass Affluent)

- Newcomers are highly digitally capable, but tend to be financially insecure due to lack of experience with personal finances. Many have just entered the workforce and are earning less than several of their peers. Newcomers seek the comfort of an advisor, but do not feel entitled to white-glove and in-person service. In fact, almost half of Newcomers sealed the deal with their wealth manager entirely online. They can be served in a nearly-entirely digital manner–highly interactive mobile applications and digital platforms are a must and over 65 percent want the ability to review/adjust their portfolios themselves, digitally, and 24/7.

- Up-and-Comers want to take ownership of their financial lives. They value themselves as a client and believe they should receive the same financial opportunities that High Net Worth (HNW) or Ultra High Net Worth (UHNW) clients receive, which can make them slower to commit. Up-and-Comers will spend time researching online and meeting with multiple potential wealth managers. Once committed, Up-and-Comers continue to demand a combination approach between high-touch interactions and digital. These clients are savvy and confident; up to 75 percent desire the ability to contact their wealth managers digitally for urgent matters, while over 60 percent want to review and adjust their portfolios digitally.

- Modestly Plateauing clients tend to feel less confident in their own financial ability, and subsequently are more emotional about their financial happenings. Our research shows that highly-emotional investors tend to rely on high-touch interactions more. Still, 66 percent of Modestly Plateauing clients want some digital interaction, and only 28 percent want their primary method of contact to be digital. These preferences are echoed in the client groups’ desire for digital capabilities. While 60 percent want to view and adjust their products digitally, they still desire high-touch interactions to aid in their decision making. They want to feel enabled to access their account themselves, but secure that someone will keep them from making the wrong decision.

- Top-of-Their-Gamers are confident in their financial success. They want personalized service paired with digital self-service, as they are highly confident in their own abilities. In fact, over half of this client segment would consider using a fully automated robo-advisor for their Wealth Management needs. Over 72 percent of Top-of-Their-Gamers desire digital interaction with their wealth managers as well as the ability to adjust their portfolios themselves via 24/7 digital access.

- Continued Accumulators clients have sustained lower levels of financial success, which have bred self-service desires. They do not trust the system because they have not experienced success within it. However, they are unfamiliar with hi-tech–this group had the lowest relative demand for digital. Only 35 percent of Continued Accumulators want to adjust their own portfolios online and receive a digital service channel.

- Wealth Transferers have shifted their portfolio priorities and now place a high priority on preserving wealth for their family and heirs. They are emotional investors. The high level of emotion surrounding their wealth necessitates a certain level of human intervention. Even though this client group is focused on the highly emotional goal of leaving wealth to posterity, the most commonly requested capability by 58 percent of clients is to interact digitally with their wealth managers.

The bottom line

The research substantiates the fact that all ages and wealth strata are ready for digital capabilities in some way, shape, and form. It also shows that traditional attributes can help identify where, when, and how to grow digital tool sets for advisors. As digital channels mature and new digital-first and digital-only entrants make their names in the marketplace, traditional advisors with strong brand names run the risk of being left behind in the dust. This is an easy trap to fall into, but an easier one to avoid. By accounting for the thought processes, needs, and preferences of clients and prospects with scalable solutions like digital advice and reporting, large traditional advisors can modernize intelligently and equip their businesses to continue to grow assets under management (AuM) and share of wallet in largely untapped and highly sought after marketplaces, like the Mass Market and Mass Affluent.

Meet the authors