Solutions

Deloitte Downturn Detector: From EBA’s downturn publications to concrete results

Guidance for a downturn LGD estimate in compliance with EBA regulations

For IRB models, the European Banking Authority (EBA) has specified the treatment of the economic downturn for LGD models in two publications: 1. The final draft RTS on the specification of the nature, severity and duration of an economic downturn (EBA/RTS/2018/04) , and 2. The final report on Guidelines for downturn LGD estimation (EBA/GL/2019/03) . Our downturn solution tool Deloitte Downturn Detector supports institutions in clarifying the new regulations. The tool makes it easy to walk through the above-mentioned papers in a structured way by breaking them down into workable pieces. Furthermore, the Deloitte Downturn Detector provides relevant economic time series, which can be amended by further data if necessary. Its visualisation capabilities and structured approach make documentation tasks user friendly. Moreover, our expert advice will support you through the whole process. It makes sure that the interpretation of the above-mentioned regulations is conducted with the specific requirements of your institution.

Deloitte Downturn Detector (DDD): The impact of regulatory requirements on your portfolio

The Deloitte Downturn Detector (DDD) contains a step-by-step guide through the paragraphs of the RTS on the specification of a downturn and the final report on Guidelines for downturn LGD estimation (EBA/GL/2019/03). It incorporates the recommended estimation approach according to the guidelines and provides:

- the base set of macro factors;

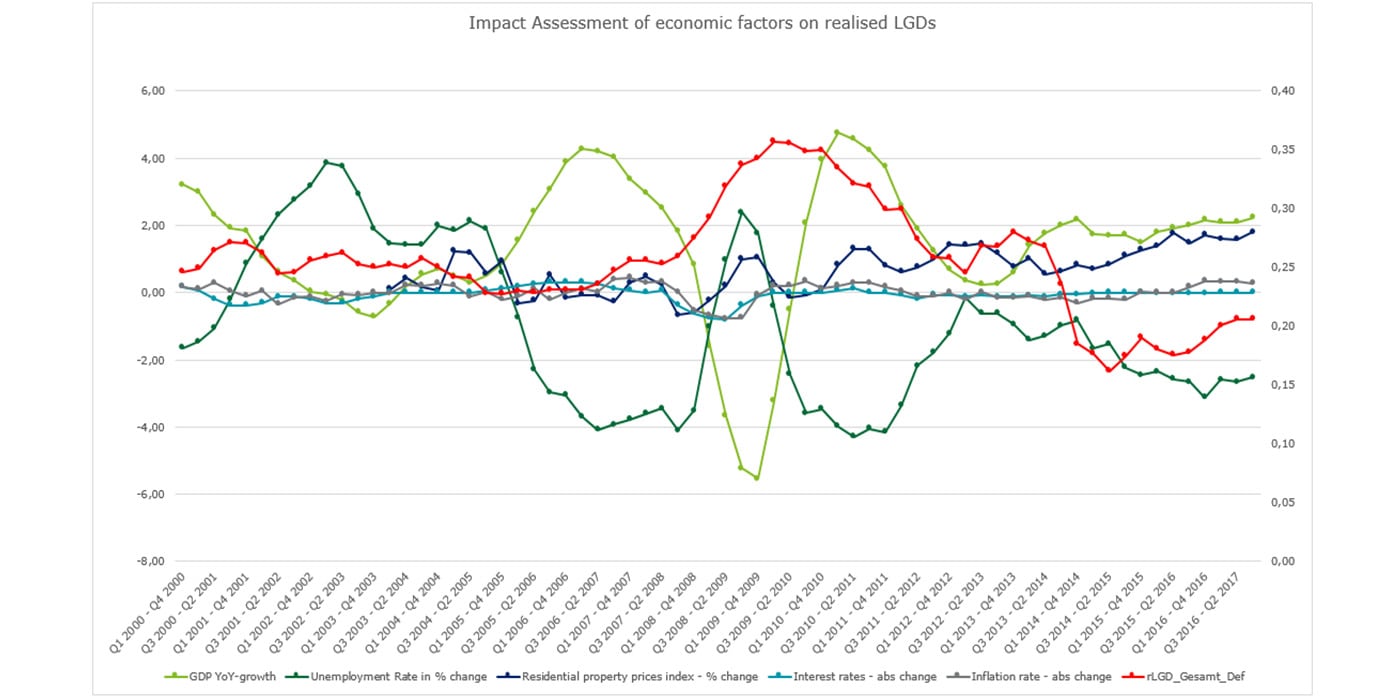

- visualization of the selected time series;

- detection of nature, duration and severity of downturns relevant to your institution;

- inclusion of statistically backed impact analysis;

quantification of historical downturn LGD, which is used as calibration target; and - explicit examples for the LGD downturn estimation.

Furthermore, DDD features a transparent workflow, data analyses and a documentation platform.

The DDD solution is an ideal starting point for the RWA impact assessment of the tailored downturn LGD estimate determined by your modelling needs. In combination with our expert advice, DDD helps you to implement an appropriate downturn estimation.

Identifying economic downturns according to EBA RTS

In order to identify an economic downturn, there are three relevant dimensions according to the RTS:

- nature,

- severity and

- duration.

The nature dimension looks at different exogenous time series with a 20-year history. Depending on the exposure type, different time series become mandatory. DDD includes several mandatory and optional time series.

After selecting all relevant time series, DDD supports you in correctly identifying the severity of the downturn by determining the most severe values in the data of each time series. The RTS encourages the use of the data with higher than annual frequency. However, it allows the use of annualised data when data with higher frequency is not available. Furthermore, DDD can work with both: annualised and quarterly data.

After the assessment of the duration, the identification of an economic downturn is complete. If the relevant time series exhibit overlapping or adjacent peaks (or troughs), a key task is to analyse whether or not there are multiple downturn periods. DDD’s visualisation capabilities support you determining the occurrence of downturn periods and their relation to each other.

Because of DDD’s structure and step-by-step description, the process of creating the documentation will require only minimal additional effort.

Setting an appropriate downturn LGD estimate according to EBA Guidelines

Depending on data availability, the EBA proposes three approaches for the quantification of downturn LGD. The two main approaches are

i. estimation based on observed impact on realised losses, and

ii. estimation based on estimated impact on realised losses.

If neither of the above-mentioned approaches is applicable, institutions may calibrate their downturn LGD estimates by using their institute-specific modelling approach, which includes a margin of conservatism (“MoC”) as set out in the EBA Guidelines on PD and LGD estimation. When using our DDD solution, our Deloitte credit risk experts support you in choosing the appropriate modelling approach for you institution.

The calibration of Downturn LGD based on the observed impact requires an analysis of the realised losses in downturn periods. The challenge here lies in the quantification of the different drivers behind these losses. After providing DDD with a time series of realised losses, the tool automatically calculates summary statistics like standard deviations and correlations, thus making it easier for you to assess and quantify an impact on realised losses.

When too little or no relevant historical data on realised losses is available, LGD downturn estimates are based on an estimated impact. Within this approach, the EBA prescribes two methods, namely the “haircut” approach and the “extrapolation” approach, which can be used separately or in combination with each other. Of course, DDD helps you choose the most appropriate course of action depending on the types of exposures under consideration.

After having selected the suitable approach, DDD outlines exemplary methods to arrive at the concrete calibration target for the downturn LGD estimation.

The Guidelines do not explicitly specify the method for quantifying the calibration target. This particularly applies to the circumstance under which historical data on realised losses is not available, and neither of the above-mentioned approaches can be considered for an appropriate downturn LGD estimation. In this situation, institutions may calibrate the downturn LGD by using an approach of their choice. At this point, we are looking forward to supporting you when it comes to determining the correct method for setting the downturn LGD estimate.

Please feel free to contact us regarding a consultation. We would be delighted to get in touch and offer our exclusive DDD solution for the new regulatory requirements concerning downturn identification and Downturn LGD.

Ihre Ansprechpartner

Dr. Thomas Moosbrucker

Partner | Financial Industry Risk & Regulatory

Auch interessant

The future of non-financial risk in financial services

Building an effective non-financial risk management program