Article

CEE Insurance M&A Outlook

The stage is set for an active deal-making environment

About the study

Leveraging on the success of our NPL study which provides an overview on non-performing loan markets in 12 countries across CEE and the Baltics, we decided to introduce a new study on insurance M&A dynamics with the same geographical scope, covering Poland, Czech Republic, Slovakia, Hungary, Romania, Slovenia, Croatia, Bulgaria, Serbia as well as Estonia, Latvia and Lithuania.

Recent performance of the insurance industry in CEE has been reassuring, the average penetration (GWP compared to GDP) remained stable over the last three years with paid claims increasing the same time. These positive dynamics were fostered by stable economic growth accompanied by improving labour market conditions in the region.

Besides insuretech solutions, another long-awaited trend picking up momentums market consolidation, which is driven by non-core exits and acquisitive growth strategies to reposition business and optimize economies of scale.

Key Findings of the Study:

- In 2017 the average gross written premiums (GWP) increased by 12.1% in the region on a yearly basis. All countries of the region demonstrated a stable growth, but this high increase rate is mostly due to the significant increase in the Polish market.

- The average GWP penetration remained stable at around 2.5% over the last three years in the examined twelve countries. In addition, GWP/capita increased to an average EUR 360.

- Paid claims increased 17.0% in the CEE region in 2017, mainly due to Poland’s large increasing claim volume.

- Non-life insurance experienced higher growth than life insurance at 15.6% compared to 6.5% year over year.

- Both life and non-life insurance markets can be considered competitive. Typically, the markets of each each country are dominated by 3-5 insurance companies, and, as certain major international insurance groups own several insurance companies on the same market, the concentration of the markets might be higher.

- The top 10 leading life insurance groups in the CEE region cover around 67.8% of the total life gross written premiums. A typical top 10 group is present in 4-5 CEE countries in the life insurance sector owning EUR 879m GWP in total. In the case of the non-life business line, the top 10 leading insurance groups cover around 67.8% of the total non-life gross written premiums. They are typically present in 5-6 countries and have an average gross written premium of EUR 1,516m.

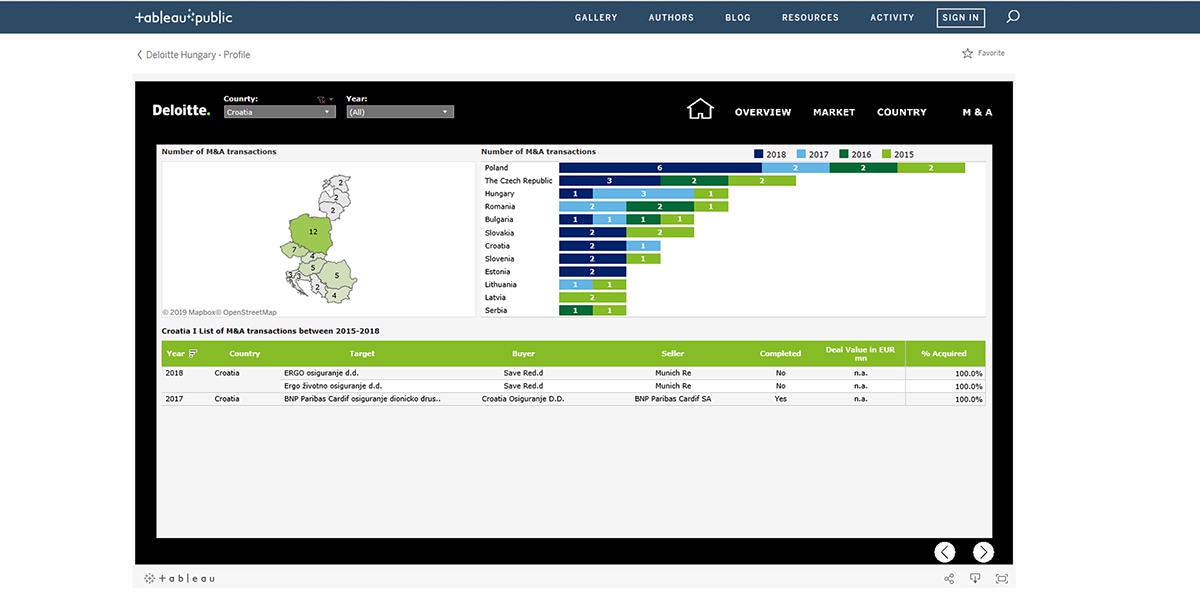

- Considering the number of transactions, the most active markets in the region between 2015 and the end of 2018 were Poland (12 transactions), the Czech Republic (7), Hungary (5), Romania (5), and Slovakia (4).

- The most active buyers in the region were Vienna Insurance Group (VIG), with 8 transactions, followed by Fairfax Financial Holdings with 6 between 2015 and 2018.

- The most active sellers in the region were AIG with 6 sales, followed by Munich RE (ERGO) with 3 sales.

Press release:

The stage is set for an active deal-making environment

As a result of the large number of insurance companies operating on the local markets and at the same time multinational groups repositioning their presence in the region, in a tightening regulatory environment, we expect an increase in the number of M&A deals in the forthcoming years.

- Vedrana Jelušić Kašić, Partner in Financial Advisory Services