India: Current account deficit has widened, but domestic fundamentals remain stable

12 October 2018

A rising crude oil bill and falling currency have widened India’s current account deficit. Nonetheless, domestic fundamentals remain stable.

Strong economic growth across the globe, especially in the United States, has created an imbalance for the emerging markets and put pressure on their currencies. India is no exception—with the rupee under stress and the crude oil bill on the rise, India’s current account deficit is widening and is expected to continue to do so in the near future.

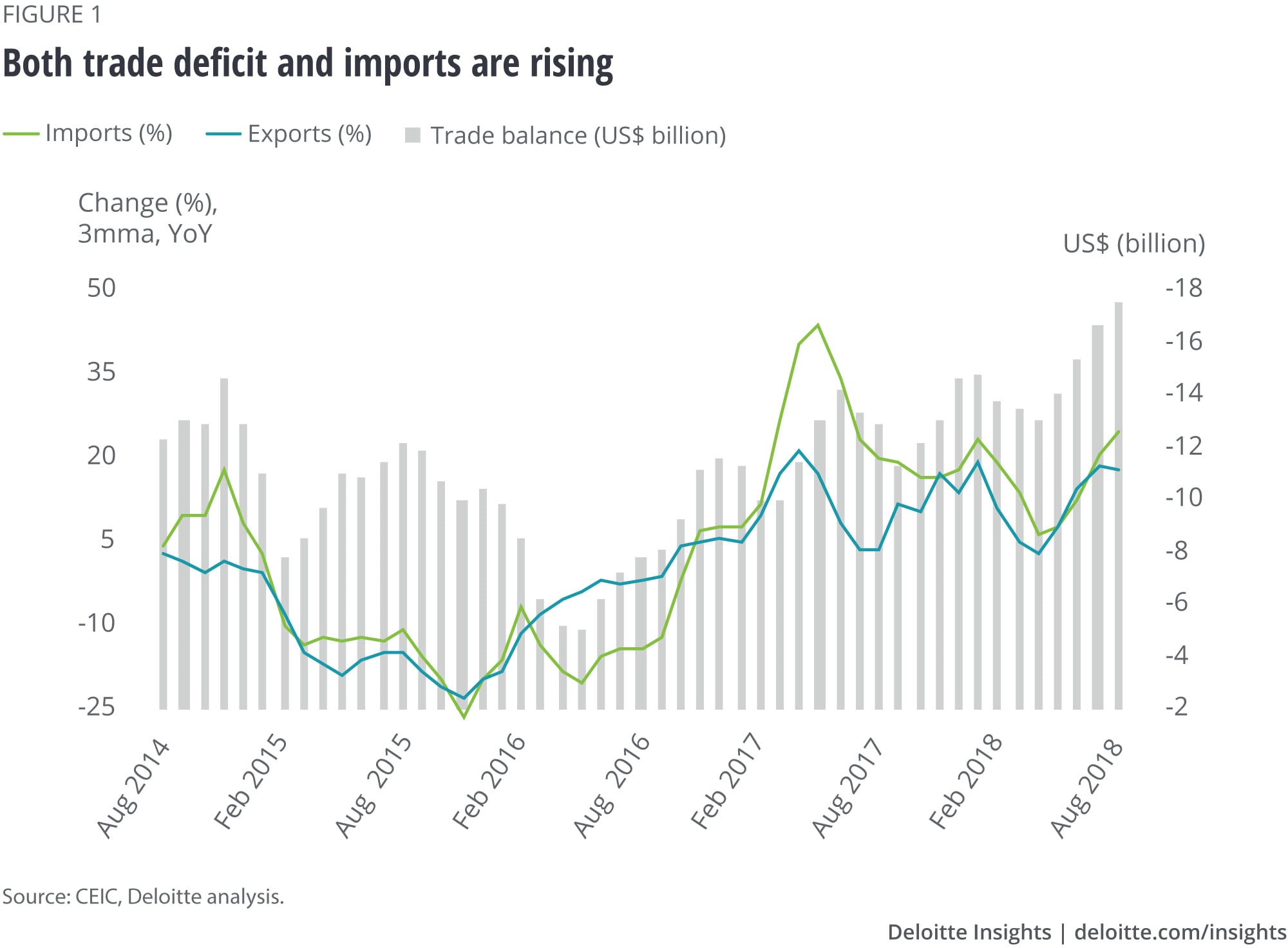

Historically, India has had a current account deficit, mainly because the Indian growth story is largely scripted on the strength of domestic demand, which fuels both domestic production and import consumption (figure 1). Over time, the composition of exports has remained unchanged, without any substantial shift toward high-tech exports. However, the composition of imports has shifted considerably from raw material to capital-intensive sectors, reflecting the needs of a consumption economy. This difference is at the heart of India’s structural challenges that need to be addressed through policy and incentives.

Learn More

Subscribe to receive more economics content

Explore more economics content: APAC Economics Collection

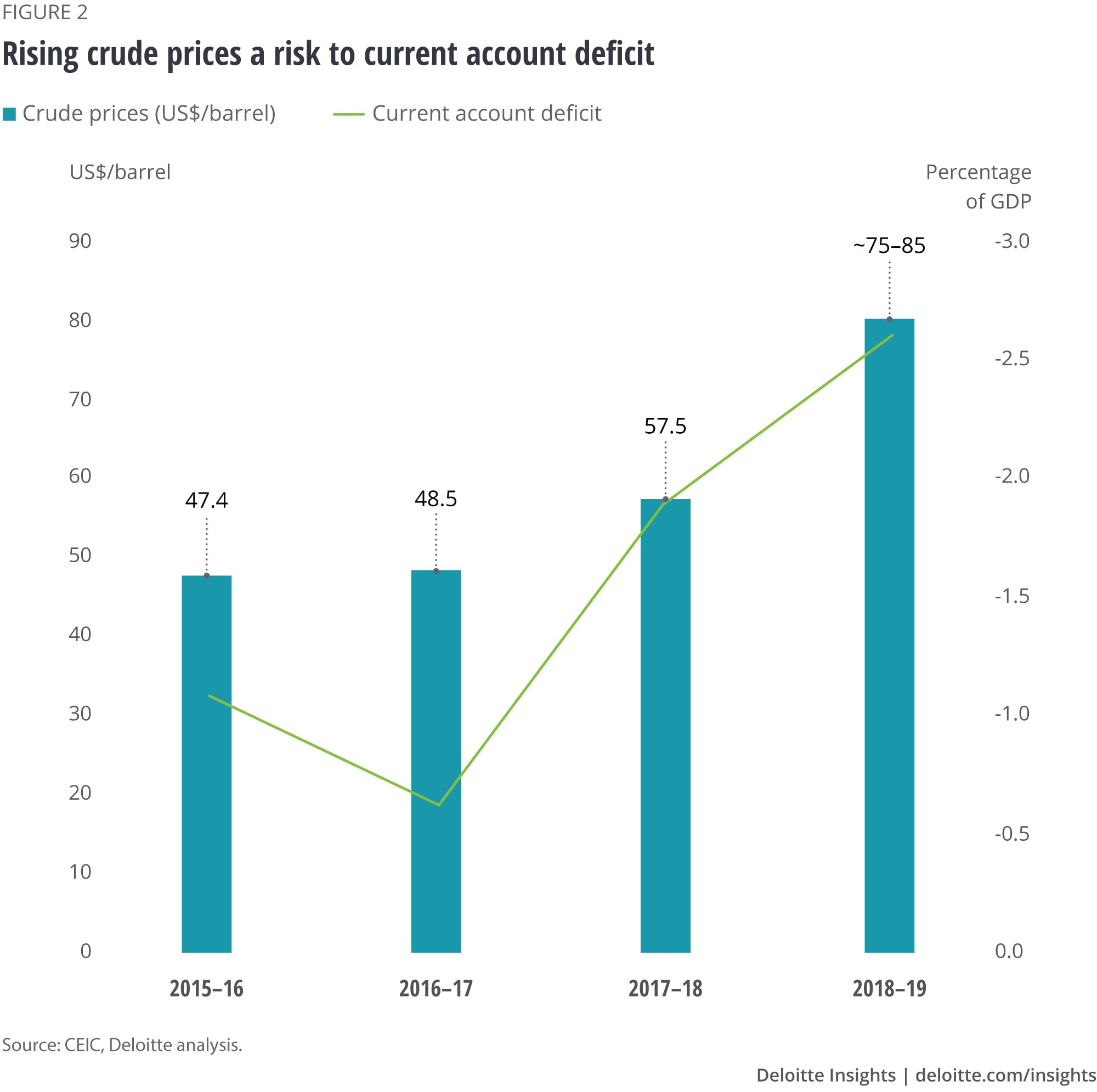

The recent widening in India’s current account deficit has largely come from an expanding trade deficit owing to increasing oil and nonoil imports, even as net income has remained somewhat stable. In the past, the government relied on net inflow of capital to partially bridge the trade deficit. Current account deficit reached 4.3 percent and 4.8 percent in FY2012 and FY2013,1 respectively, mainly due to a large trade deficit arising from imports of merchandise goods and a high import bill for oil and gold. Over time, as foreign direct investment (FDI) and foreign portfolio investment (FPI) increased and services exports rose, India was able to reduce the current account deficit. It remained below 2 percent between FY2014 and FY2018, when the country saw higher services exports and remittances as well as net capital inflows. There was also effective policy intervention to reduce import expenditure. Some of the notable interventions included a gradual rise in the import duty on gold from 2 percent to 8 percent;2 further liberalization of the foreign FDI policy, allowing Indian state-owned companies to raise foreign capital; and relaxation of restrictions on accessing foreign debt by Indian companies. Indeed, policy was supported, especially through 2015—2017 by softening crude prices, which also helped to substantially lower the oil import bill (figure 2).

The current stress on the CAD is a reflection of both external factors and domestic structural challenges that continue to affect Indian exports. Trade deficit was US$161.5 billion in FY2018, taking the current account deficit to 1.9 percent of gross domestic product (GDP). In the first quarter of FY2019, the deficit was 2.4 percent, and is generally expected to be more than 2.5 percent3 of GDP for FY2019. Oil imports alone resulted in net outflows of more than US$108 billion in FY2018, compared to US$87 billion in the year before. Currently, the market expects crude to remain at elevated levels. It is, however, important to note that oil is not the only factor contributing to trade deficit. The Indian currency has touched a historic low of about INR 74 to the US dollar, and is expected to remain within the INR 69–72 per US dollar range. Also, nonoil, nongold imports have increased in the double-digit range in the recent months.

As a result, we now have a net negative situation, where financing of the trade deficit through the capital account has become difficult as a result of capital rerouting from emerging markets due to a stronger dollar. While India has historically attracted sufficient FDI flows—US$45 billion in FY2018, up from US$43.5 billion in FY2017—the pace of growth is cooling. To add to this, FPIs have been cashing out of emerging markets, including India. In fact, since April 2018, FPIs have pulled out close to US$11 billion from the securities market—with the debt market accounting for a larger share of this flight.

Will exports help?

A weakening rupee can be seen to have a positive impact on India’s exports, especially in the current context of improving global demand. While this ought to happen, data reveals only limited positive impact. The rupee has fallen by more than 10 percent since the beginning of the year, in line with other emerging market currencies. Exports rose 16 percent in FY2018, up from 9.9 percent in FY2017, and have shown an average increase of 16 percent since April 2018. This double-digit export growth in the last few months is partly on account of a positive base effect, and so the degree of export growth attributable to currency depreciation may not be significant.

Managing the current account deficit in a scenario of high crude prices and weaker capital inflows will require policy stimulus (to boost exports) and structural reforms (to boost productivity and encourage import substitution in manufacturing).

Is a rising current account deficit a matter of concern?

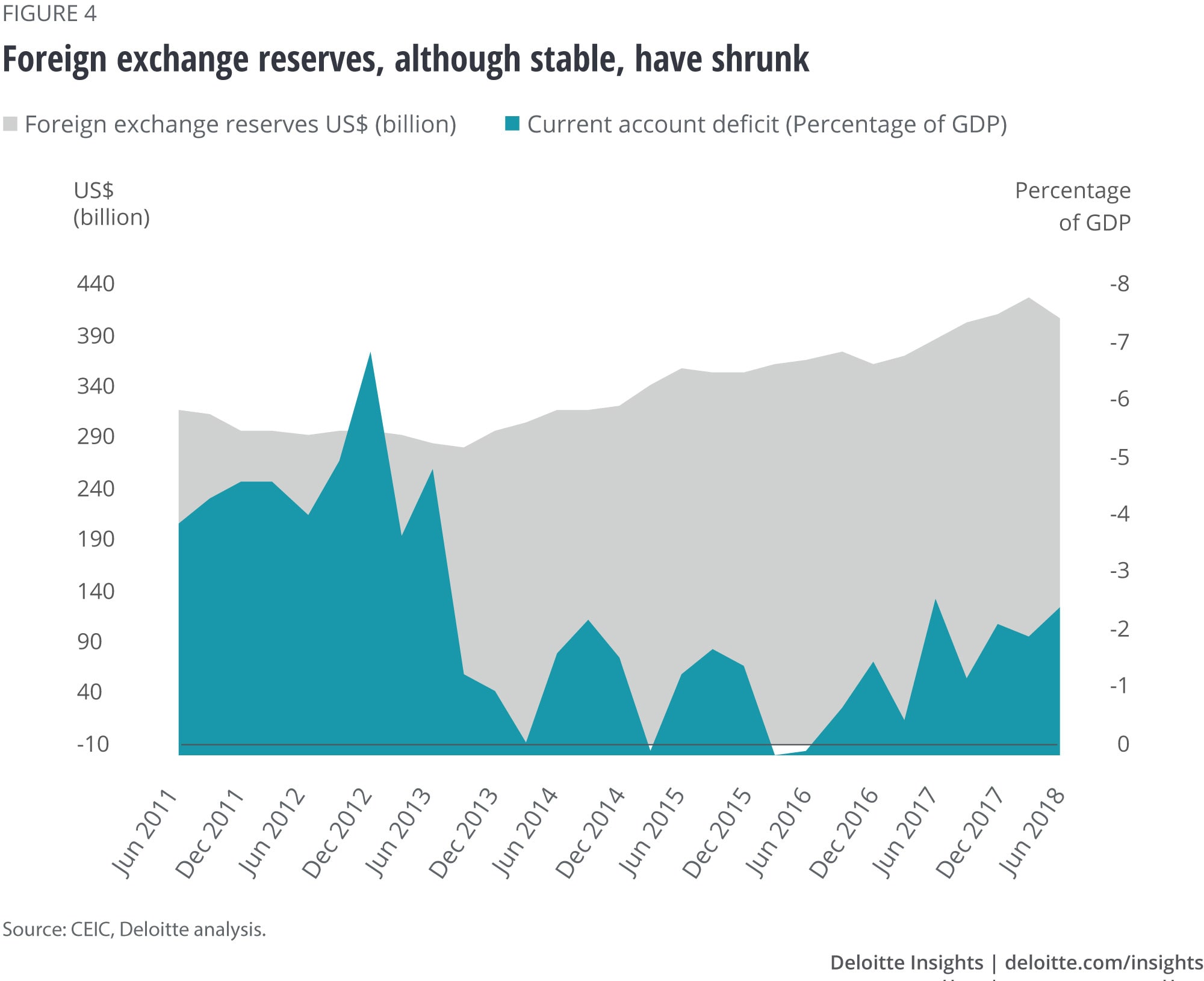

At present, the current account deficit is within the safe limit of less than 3 percent of GDP. Should it increase beyond 3 percent, there could be financing challenges.4 Foreign reserves, albeit stable, have declined while certain macroeconomic challenges (including high household inflation expectations, a subdued credit cycle, and rising fiscal pressure) can worsen the domestic situation. A more important facet of the trade and current account deficits is how both impact the fiscal deficit. The Indian finance minister has recently affirmed that the Indian government will not deviate from its stated fiscal deficit target.5 However, if exports do not rise commensurately or nonoil, nongold imports are not managed, then a growing current account deficit could feed into a rising fiscal deficit. Stable foreign reserves are expected to cushion any steep stretch in the current account deficit.

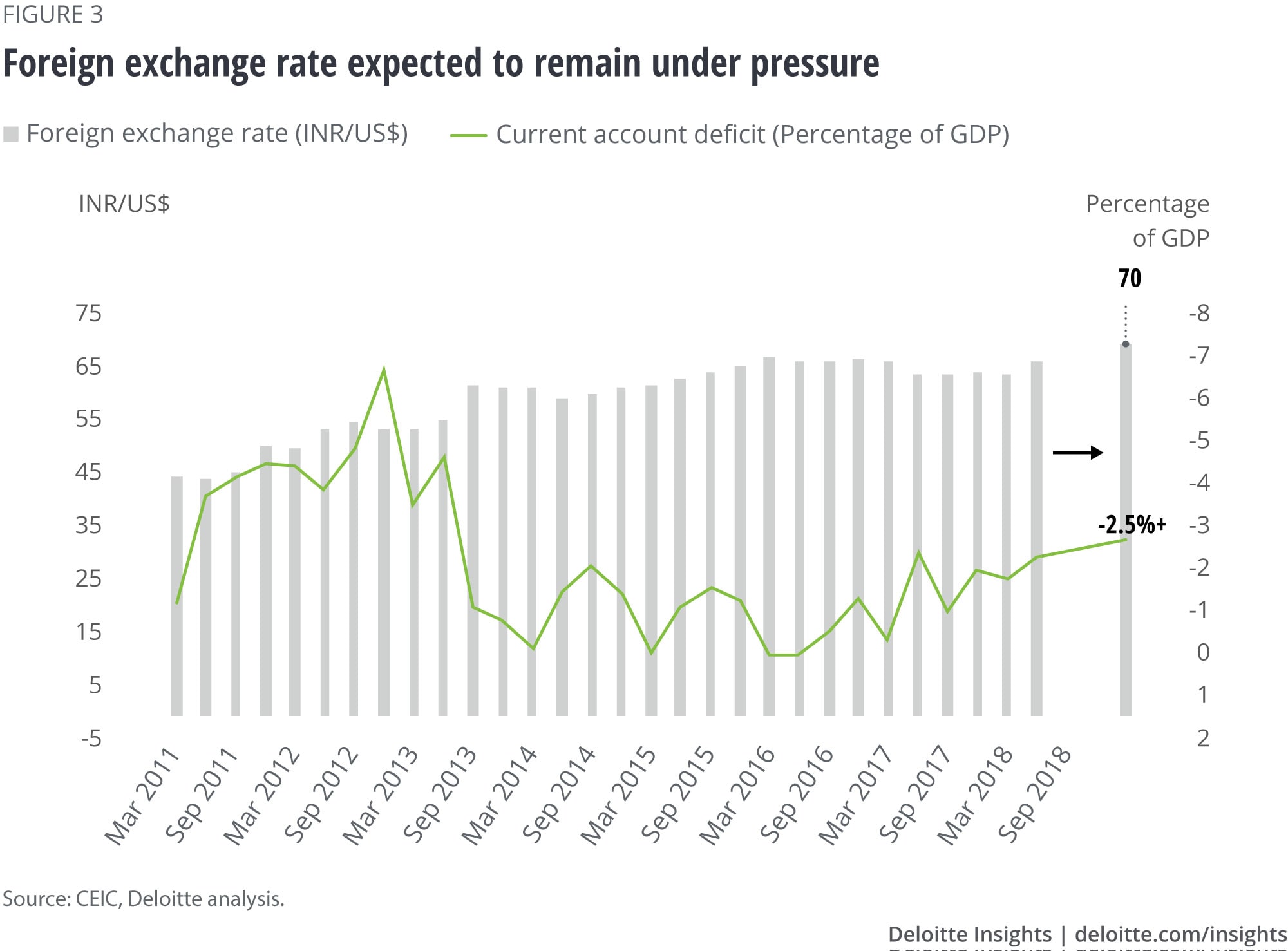

Nevertheless, the rising current account deficit is putting pressure on the INR–USD exchange rate (figure 3), which in turn is inflating the import bill at a faster pace and boosting domestic inflation, thereby putting an upward pressure on interest rates. Foreign reserves and capital inflows have essentially been used as a medium to plug rising deficit levels and manage currency fluctuations. India’s reserves are currently sufficient, but they have declined from US$420 billion in April 2018 to US$400 billion at end-August 2018. Some of the decline has been because of the central bank’s intervention in the currency market (figure 4). The Reserve Bank of India sold close to US$8.25 billion in US Treasury bonds in the domestic spot market during April and May 2018, reflecting its intervention to cushion the fall in the rupee.6

Policy response

Recognizing the concerns regarding the current account deficit, the Indian government announced some measures to boost capital flows and reduce “nonessential” imports. Primary among them are:

- Elimination of withholding tax on the rupee-denominated bonds sold in the overseas market (commonly known as Masala bonds)

- Relaxation on FPIs, which involves removal of the FPI exposure limit of 20 percent in the corporate bond portfolio to a single corporate group and 50 percent of any issue of corporate bond

- Enabling manufacturing units to access external commercial borrowings up to US$50 million for a minimum maturity of one year

The government hopes to encourage capital flows, albeit mostly in the debt market, through these steps. Apart from this, the government has also raised import tariffs on 19 items to curb widening CAD. These include, washing machines, refrigerators, radial tyres, and aviation turbine fuel (ATF) among others.

These measures are the first policy response to the widening deficit, and their efficacy will be assessed in time. However, the more important initiatives will be toward reforms that can stimulate exports and promote efficient utilization of capital, thereby generating better returns for foreign investors. Some of these measures could be speeding up project implementation, enabling the ease of doing business, providing more support to small enterprises, especially export units, etc.

It needs to be recognized that India’s domestic fundamentals remain stable, and the widening current account deficit and currency depreciation are a product of global factors. Therefore, it is advisable to maintain a conservative stance on fiscal consolidation and continue to use currency depreciation as a tool to enhance price competitiveness of Indian exports. In the long term, all net energy importers, especially large consumers like India, will have to adopt widescale use of renewable energy. Currently, the Indian government can do only so much to contain imports. Overall, the Indian economy will gain much more if the Indian government focuses more on efficacious implementation of existing projects and normalizing domestic investment growth.

Deloitte's Global Economist Network

Learn more

Get in touch

- Richa Gupta

- Senior director and senior economist

- Deloitte Haskins & Sells LLP

- rIchagupta@deloitte.com

- +91 9811119548