United States Economic Forecast has been saved

United States Economic Forecast 1st Quarter 2017

13 March 2017

With a new US administration discussing shifts on trade, taxes, and regulations, it’s almost certain that economic conditions for businesses will change in the upcoming months. But it’s hard for CEOs to make key decisions until new policies begin to take shape.

Introduction: When will new policies emerge?

It seemed like far more than 10 weeks between the November election and the new administration taking office, and even more for the country’s policymaking process to lurch into action. Plus, the US policymaking system is hardly designed for fast results: Unlike in parliamentary systems, winning an election in the United States signals only the beginning of the work of a new administration.

President Trump enters the fray with an advantage and a disadvantage. The advantage is that much of politics concerns doing deals—and the president is a self-proclaimed expert at dealmaking. His efforts to translate that expertise from business to politics means that the United States could see significant policy changes. The disadvantage is that Republicans, with control over the legislative and budgetary agenda, are not unified on the specifics of the policies they’ve long pledged to enact. Energetic debates within the GOP over many issues (such as how to replace the Affordable Care Act) need to be resolved before Congress can take action. The Democratic opposition, seeing little outreach toward them and historically low presidential approval polls,1 is doing what it can to slow down everything.

All this adds up to more waiting until the outlines of what the new administration intends to do—and what it will be able to do—become apparent. Over the next few months, at least some of the policy debates should begin to approach consensus. That will give businesses a clearer view of what Washington will and won’t deliver. Until then, we continue to recommend (as we always do) that CEOs pay attention to all the scenarios in the forecast. That’s how to avoid being unhappily surprised.

Economic policy could advance (or not) on the following fronts:

Health care: Campaign promises notwithstanding, changing the health care system without dropping a significant share of the privately insured from the system is proving more difficult than many assumed.2 The Deloitte forecast assumes that there will be no major macroeconomic impacts of changing (or not changing) the health care system.

Tax policy: Debate is swirling around the possibility of adopting the Republican House tax plan for reforming the corporate income tax, with the feature of “border adjustment.”3 This would provide for a tax rebate for exports and for taxing imports. However, some Republicans (and possibly the White House, and definitely many retailers4) are unhappy with this approach. The Deloitte forecast assumes undefined cuts in both personal and corporate tax rates, although smaller than in our last forecast. This reflects the difficulties evident in passing larger tax cuts.

Regulation: Businesses will likely face lower regulatory hurdles, but the overall impact may be more modest than some expect—especially in the short run. Eliminating regulations can be difficult and time-consuming, requiring careful action to avoid running into legal problems. The Deloitte forecast assumes that the changed regulatory environment will lower business costs.

Trade: As of this writing (early March), the administration has not taken concrete actions on trade. Swift and significant actions could pose problems for economic activity and growth. That is reflected in the Deloitte’s slow scenario. In the baseline scenario, the Deloitte forecast assumes that trade policy adds to business costs, just offsetting the reduction in costs from easier regulation.

Infrastructure spending: Although this was a key component of President’s Trump’s campaign platform, it appears to be fading a bit as a legislative priority. The Deloitte forecast assumes that there will be an infrastructure spending program worth about $125 billion, mainly spent in 2018 and 2019. About half of this is assumed to be traditional infrastructure spending, with the rest being private-sector spending. This is half the size of the program we assumed in our previous forecast.

Immigration: The Deloitte forecast assumes that immigration policy, despite a great deal of public discussion,5 will have little or no impact at the macroeconomic level. Specific industries such as technology and agriculture may feel significant effects.

We do not judge that the supply-side elements of the program, such as regulatory relief, will have a large impact in the five-year forecast horizon. This doesn’t mean that they might not be important for the economy’s long-run growth. But over the next few years, we expect, the impact on economic aggregates such as GDP, employment, and inflation will be dominated by the demand-side impacts of this policy mix.

With the economy now relatively close to full employment, the demand stimulus will likely create inflationary pressures. The Deloitte forecast assumes that the labor force participation rate rises substantially as strong growth attracts workers back into the labor force. That in turn would moderate inflation and the Fed’s response. The slow scenario assumes less slack in the economy, making inflationary pressures show up more quickly.6

Scenarios

Our scenarios are designed to demonstrate the different paths down which the new administration’s policies might take the American economy. Foreign risks have not dissipated, and we’ve incorporated them into the scenarios. But for now, we view the greatest uncertainty in the US economy to be that generated within the United States.

The baseline (55 percent probability): Uncertainty restrains business investment in early 2017, but tax cuts and infrastructure spending push up GDP in 2018 and 2019. With the economy at full employment, the faster GDP growth creates some inflationary pressures. A small increase in trade restrictions add to business costs, but this is offset by lower regulatory costs. Annual growth rises to 2.5 percent before falling off as the impact of the stimulus fades.

Recession (5 percent): Policy changes in the United States, including a large tariff on Chinese goods, trigger a global financial crisis. The crisis is exacerbated by a large rise in global supply chain cost structures from higher US trade barriers, as well as retaliation from China. The Fed and the European Central Bank act to ease financial conditions, and growth starts to pick up as businesses adapt to the new global costs and restructure their capital to reflect the new global cost structure. GDP falls in the last two quarters of 2017 and recovers after 2018.

Slower growth (30 percent): The infrastructure program and tax cuts stall in Congress even as the administration places significant restrictions on American imports, raising costs and disrupting supply chains. Businesses hold back on investments to restructure their supply chains because of uncertainty about future policy. GDP growth falls to 1 percent over the forecast period, and the unemployment rate rises.

Successful policy takeoff (10 percent): The administration takes only symbolic action on trade. With supply chain disruptions off the table, businesses focus on tax cuts that are designed to increase investment spending, and the opportunities available from the infrastructure plan. Growth remains above 2 percent for the next five years.

Sectors

Consumer spending

The household sector has been the bright spot of the American economy for the past year or two. Even while business investment was weak, exports faced substantial headwinds, and housing stalled, consumer spending has grown steadily. But that’s not surprising, since job growth has been quite strong for the past few years. Even with relatively low wage growth, those jobs have put money in consumers’ pockets. That has allowed households to spend while keeping savings at a high (for the United States) level.

Consumer confidence has remained strong, and even picked up after the election. This may have reflected that even many voters unhappy with the election results still expect business conditions to improve. And fundamentals such as job growth and inflation remain strong. Given recent economic data, there’s no reason to expect confidence to fall much, even if the news from Washington indicates confusion in policymaking.

American households still face some obstacles in their pursuit of the good life. They have (mostly) recovered from the over-borrowing of the 2000s, though many remain “underwater,” with houses worth less than what the household owes on the attached mortgage. And there is the problem of growing income and wealth inequality. The possibility of higher inflation would be welcome for reducing the number of underwater households, since their borrowing is in nominal dollars. But it’s unclear whether—much less how—the new administration intends to address the inequality problem.7

Many US consumers spent the 1990s and ’00s trying to maintain spending even as incomes stagnated. After all, excitable pundits kept assuring them that the technology transforming their lives would soon—any day now—make them all wealthy. But now they are wiser (and older, which is another problem, as many Baby Boomers face imminent retirement with inadequate savings8). As long as a large share of the gains from technology and other economic improvements flow to a relatively small number of households, overall US consumer spending is likely to remain relatively restrained.

CONSUMER NEWS

Real consumer expenditures grew at just 0.1 percentage point a month on average in the fourth quarter. Real consumer spending grew about twice as fast, so the savings rate fell to 5.4 percent in December.

Headline retail sales picked up in December. Sales less those at auto dealers grew a healthy 0.4 percent on average in October to December.

Consumer confidence picked up a bit, to very high levels in December. The main cause is continued strength in labor markets, but households—like stock market investors—may be optimistic that infrastructure spending and tax cuts will improve the economy further.

Housing

Every year, thousands of young Americans abandon the nest, happy to leave home and start their own households. But more than usual stayed put during the recession: The number of households didn’t grow nearly enough to account for all the newly minted young adults. We expect those young adults would prefer to live on their own and create new households; as the economy continues to recover, they will likely do exactly that—as previous generations have.

This means some positive fundamentals for housing construction in the short run. Since 2008, the United States has been building fewer new housing units than the population would normally require; in fact, housing construction was hit so hard that the oversupply turned into an undersupply. But the hole is shallower than you might think. Several factors offset each other: If household size returns to mid-2000s levels, we would need an additional 3.2 million units; on the other hand, household vacancy rates are much higher than normal. Vacancy returning to normal would make available an additional 2.5 million units—which would fill 78 percent of the pent-up demand for housing units.

But are the existing vacant houses in the right place or condition, or are they the right type, for that pent-up demand? The future of housing may look very different than in the past. Growth in new housing construction has been concentrated in multifamily units. If that persists, we may find it is related to young buyers’ growing reluctance to settle in existing single-family units.

While economic growth and job creation may point to strong house sales, higher interest rates may moderate any potential housing boom. Higher inflation and a strong Fed response may drive up mortgage rates more quickly than businesses in the housing sector would like.

HOUSING NEWS

Housing permits were barely (2.3 percent) above their year-ago level in December. A rise in single family permits over the year was offset by a decline in multifamily permits. At about 1.2 million, permits are still below the level required to make up for the many years of low housing growth.

Contract interest rates rose about 30 basis points through December, reflecting the upward movement in all long-term rates. Although long-term interest rates had begun rising even before the election, the movement accelerated afterward, likely reflecting higher inflation expectations. House prices continue to move up, and even accelerated a bit during the fall. In November, the Case-Shiller national index was 5.6 percent above the previous year’s level.

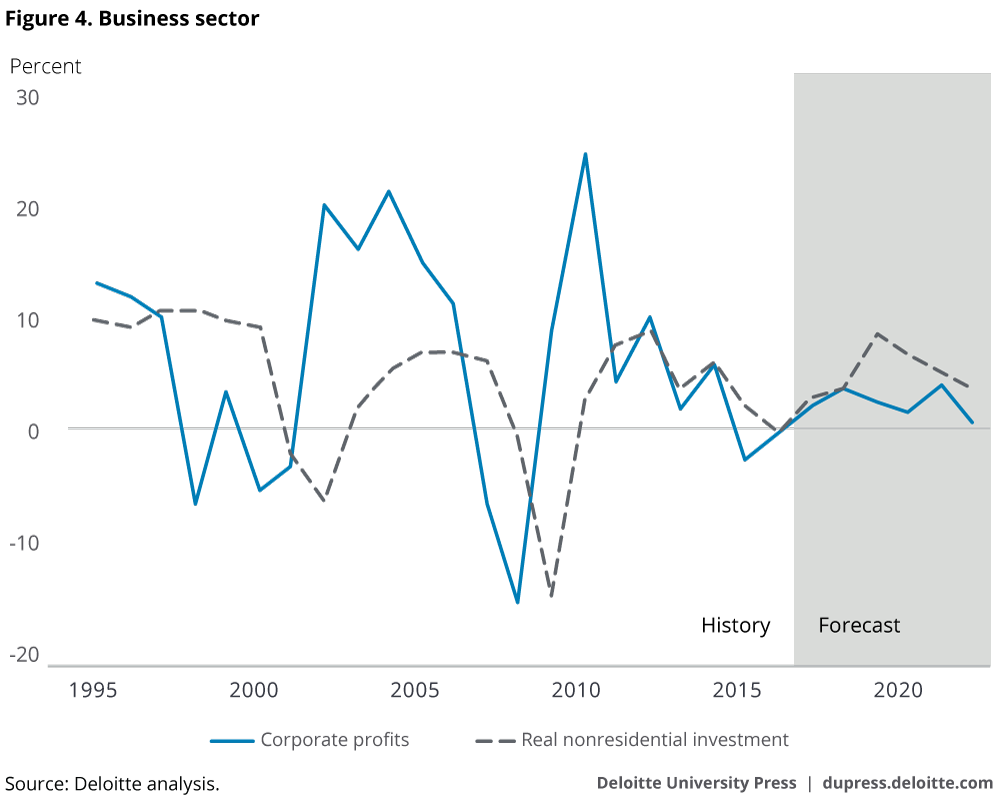

Business investment

Many may blame election-season uncertainty for lagging investment, but it’s easy to find more fundamental reasons for the weakness in this area over the two past years.

Oil and gas extraction accounted for 6 percent of all nonresidential fixed investment in 2013. That’s a hefty amount (considerably larger than the sector’s value-added share), so shutting down new US oil exploration in late 2014 had a larger-than-expected impact on investment. Indeed, the 2015 data on investment by type show that most of 2015’s decline was due to two specific categories: mining structures and mining and oilfield equipment. Other types of investment—ranging from commercial structures to transportation equipment to intellectual property—have held up much better. It’s likely the continuing low price of oil, not the low state of political debate, that has held down investment.

The weakness in investment spread to other areas in the first half of 2016. However, it’s not hard to find a key culprit in the fundamentals: The rising dollar is not only making American companies less competitive—it’s cutting overseas earnings valued in dollars and therefore reducing margins for US multinationals. And China’s slowing growth is exposing global excess capacity in many industries.

Our baseline scenario assumes that uncertainty plays a role in early 2017. Investment spending may slow somewhat as businesses wait to get direction about government policy. On the other hand, the strong economy is pushing businesses in the direction of growing capacity, less they lose the opportunity that the current hot economy presents.

The medium-term problem that businesses face is deciding whether they need to rebuild their supply chains. Industries such as automobile production have developed intricate networks across North America and reaching into Asia and Europe, based on the longstanding assumption that materials and parts can be moved across borders with little cost or disruption. These capital-intensive industries are likely to want to postpone easily delayed investments in these networks until the administration’s trade policy becomes clearer.

Beyond the immediate impact of this policy uncertainty, the truth is that demand is the key to business investment. Simply, if businesses see higher demand for their products, they will grow capacity. In the baseline forecast, there is a modest boom in private investment that is induced by higher infrastructure spending and demand from tax cuts.

BUSINESS INVESTMENT NEWS

Real business fixed investment rose 2.4 percent in the fourth quarter (according to the first GDP release). That’s the third quarter of slow growth, but it’s better than the 3.0 percent decline in Q4 2015 and Q1 2016. Structures investment fell 5.0 percent, while equipment investment registered the first positive quarter since Q3 2015. Intellectual-property investment continues to rise at healthy rates.

Nondefense capital-goods shipments—an effective high-frequency measure of equipment spending— bounced back in December after falling in October and November. Less aircraft, capital goods shipments looked much better, rising 0.7 percent in November and 1.0 percent in December. This suggests strong momentum in equipment investment going into the first quarter.

Private nonresidential construction was flat in the quarter, but the weakness was entirely in manufacturing construction. Office construction posted a strong gain in December after two months of little growth, while commercial construction has grown for three months to December at an average monthly rate of almost 2.0 percent.

Yields on corporate bonds started to creep up even before the election. In November and December, they jumped almost half a percentage point but have stayed flat since then. Stock indexes made headlines by reaching new highs, as traders anticipated the impact of tax cuts, higher infrastructure spending, and (especially for financial companies) reduced regulation.9 Corporate profits rose 29 percent at an annual rate in the third quarter. Profits remain at close to a record share of national income.

Foreign trade

Over the past few decades, business—especially manufacturing—has taken advantage of open borders and cheap transportation to cut costs and improve global efficiency. The result is a complex matrix of production that makes the traditional measures of imports and exports misleading in some senses. For example, in 2007, 37 percent of Mexico’s exports to the United States consisted of intermediate inputs purchased from the United States.10

Recent events appear to be placing this global manufacturing system at risk. Brexit, which may affect the United Kingdom’s position in the European manufacturing ecosystem, along with the suggestion that the United States would cancel or renegotiate its position in NAFTA, may slow the growth of this system or even cause it to unwind. The impact would be felt in several ways:

• In the short run, uncertainty about border crossing costs may reduce investment spending. Businesses may be reluctant to put capital in place when faced with the possibility of a sudden shift in costs. The Deloitte forecast includes a very modest decline in US investment spending for the first two quarters of 2017 to reflect the fact that the full direction of American trade policy is still not evident.

• A significant change in border-crossing costs—as would occur if the United States withdrew from NAFTA—would likely reduce the value of capital investment put in place to take advantage of global goods flows. Essentially, the global capital stock would depreciate more quickly than our normal measures would suggest. In practical terms, some plants and equipment in the United States would go idle without the ability to access foreign intermediate products.

• With this loss of productive capacity would come the need to replace it with plants and equipment that would be profitable at the higher border cost. We might expect gross investment to increase.

The baseline forecast assumes some retaliatory measures that reduce US exports—but not an all-out trade war.

The current account is determined by global investment flows, not trade costs. Any potential reduction in the current account deficit is likely to be largely offset by a reduction in American competitiveness through higher costs in the United States, lower costs abroad, and a higher dollar. The forecast assumes that the current account deficit therefore remains unaffected by trade flows.

FOREIGN TRADE NEWS

US goods exports grew 3.2 percent in December after falling in the previous two months. Imports grew for all three months of the fourth quarter at about 1.5 percent per month. As a result, the trade deficit gradually grew. In December, it was at a monthly rate of $65 billion.

The dollar appreciated at about 1.5 to 2.0 percent per month in the last three months of 2016. The Canadian dollar appreciated slightly, while the euro moved to $1.05 by December, and the Mexican peso dropped from 18.9 in October to 20.5 in December. The dollar depreciated in January against most major currencies, although the Mexican peso continued to lose ground.

The Chinese economy is recording satisfactory growth, though many observers remain concerned about the country’s financial system and continuing infrastructure investment. Some analysts focus on signs of strength in China’s consumer and service sectors, suggesting a long-awaited adjustment to becoming a consumer-driven economy. Others point to indications that official Chinese figures may be implausibly high.11 The country’s future remains a large risk for the global economy.

Europe has shown some signs of growth. European GDP grew 0.5 percent in the fourth quarter, with relatively fast growth in Spain, the Netherlands, Portugal, and the United Kingdom. German and French GDP grew 0.4 percent. However, negotiations over the continuation of aid to Greece remain potential source of uncertainty for the Eurozone.

Government

Recently, we started to see a modest contribution of federal spending to GDP. That’s the result of the last federal budget agreement, which raised caps on both defense and nondefense purchases. The new administration, however, may change this if it decides to follow through on the infrastructure spending program on which President Trump campaigned, along with relieving the budget sequester that has hamstrung spending since 2013. The forecast assumes a more state and local investment spending, as about half the total $125 billion program we’ve put into the forecast is assumed to be private-sector spending. This is an important driver of the relatively fast growth expected in the baseline in 2018 and ’19. It also drives a decline in growth in reflecting the end of the program and a consequent decline in state and local spending.

The rise in spending occurs alongside a significant tax cut. The forecast assumes that the president and Congress will decide that these initiatives are sufficiently important to permit a significant rise in the federal deficit. If the deficit becomes an important debating point, passing either or both of these policy packages will become more difficult.

After years of belt-tightening, most state and local governments are no longer actively cutting spending. A portion of the infrastructure program is likely to take the form of transfers to state and local governments (most infrastructure investment in the United States takes place at the state and local level).

GOVERNMENT NEWS

The federal deficit ended the first four months of the fiscal year at $159 billion, the same level as last year. Outlays and receipts were each up less than 1 percent over the previous year’s level.

Federal employment grew slightly over the quarter, while state and local employment fell, mainly because of a decline in employment in education.

Labor markets

If the American economy is to produce more goods and services, it will likely need more workers. However, many potential workers remain out of the labor force: They left in 2009, when the labor market was terrible. The stability of the participation rate in 2016, even as the labor force is aging, is an encouraging sign. Accelerating production will likely carry with it an eventual acceleration in demand for labor, along with a welcome mild rise in wages. That should help to bring people back into the labor force.

But a great many people have been out of work for a long time—long enough that their basic work skills may be eroding. When the labor market tightens, will those people be employable? Deloitte’s forecast team remains optimistic that improvements in the labor market will eventually prove attractive to potential workers, with labor force participation picking up accordingly.

Significant immigration restrictions and/or deportation might have a marginal impact on the labor force. According to the Pew Research Center, undocumented immigrants make up about 5 percent of the total American labor force.12 Removal of all such workers would clearly have a significant impact—but that is unlikely to happen. A more realistic assumption might be the return of about half a million undocumented workers annually. That would create labor shortages in certain industries (such as agriculture, in which 17 percent of workers are unauthorized, and construction, in which 13 percent of workers are unauthorized)13 but would likely have little significant impact at the aggregate level.

LABOR MARKET NEWS

Initial claims for unemployment insurance have fallen from the 260,000 monthly range last summer to the 250,000 range (and below) in January. That’s very low, especially considering that the labor force and total employment continue to grow over time. Job openings have been flat, in the 5.5 million range. However, this is just under the highest level recorded (since 2002). Quits (voluntary separations) have also been stable at around 3.0 million—also a high number. The large number of voluntary quits suggests that labor demand remains strong.

Payroll employment rose at an average rate of 168,000 per month in October-January. That’s almost twice as much as would be required by the growth of the labor force, although slower than the rate recorded in 2014–15.

Financial markets

Interest rates are among the most difficult economic variables to forecast because movements depend on news—and if we knew it ahead of time, it wouldn’t be news. The Deloitte interest-rate forecast is designed to show a path for interest rates consistent with the forecast for the real economy. But the potential risk for different interest-rate movements is higher here than in other parts of our forecast.

Global financial markets are now in a highly unusual state. About $10 trillion in sovereign debt is now trading at negative interest rates (meaning borrowers are paying for the privilege of loaning money to these countries). The existence of negative interest rates is unprecedented, and the fact that even large countries (such as Germany) are borrowing on these terms indicates that global financial markets have not fully recovered from the problems of the previous decade.

Despite this, the forecast sees both long- and short-term interest rates headed up—maybe not this week, or this month, but sometime in the future. The combination of tax cuts and infrastructure spending assumed in the baseline is very simulative. The Fed currently is assuming that the economy is near full employment and would therefore likely react strongly to a pickup in growth such as assumed here. For that reason, the current baseline assumes an aggressive Fed reaction, with the Fed raising rates every other FOMC meeting for the next few years. However, we have lowered our baseline long-term view of the stable Fed funds rate to be consistent with our assumption of a smaller demand-side policy impact. Long-term interest rates move up as the economy returns to full employment and some inflationary pressures appear.

FINANCIAL MARKET NEWS

Speculation about the future of the Fed will continue to grow over the next year. The new administration has an immediate chance to make an impression on the central bank by filling two open slots on the Board of Governors and appointing a new chairman in February 2018.

Long-term bonds rose in the last two months of 2016, then fell a bit in January. AAA corporate bonds maintained a spread of 90 to 100 basis points over Treasuries, while the junk-bond spread fell in December by about 30 basis points and remained lower in January. Traders continue to anticipate that the new administration will promote economic stimulus that will lead to more government borrowing and ultimately higher inflation.

Stock prices rose through January and February and are at record levels. Indeed, there is considerable debate about whether stocks are overpriced, since P/E ratios are high and investors are evidently optimistic about future federal government fiscal policy.

Prices

It’s been a long time since inflation has posed a problem for American policymakers. The US economy has functioned below potential since 2008, and even before then there were few signs of significant inflation. With so much slack, neither workers nor businesses had the ability to raise prices.

Many observers believe that the economy is approaching full employment (although the Deloitte forecast projects some additional contribution from workers returning to the labor force as the economy continues to improve). Thus, the fiscal stimulus of tax cuts combined with infrastructure spending—if they occur as forecast—might create some shortages in both labor and product markets, and, as a result, some inflation. A return to 1970s-style inflation is unlikely, but it would not be surprising in those circumstances to see the core CPI running at percent to 3.0 percent—or perhaps even a little higher. The forecast expects timely Fed action to prevent inflation from rising too much, but the price (of course) is higher interest rates.

PRICE NEWS

The overall CPI accelerated in January, mainly due to higher energy prices. However, the core CPI is beginning to accelerate as well. It is now consistently above 2 percent over the previous year’s level, which policymakers will tolerate (indeed, by reducing the possibility that deflation might set in, the higher inflation is welcome). Inflationary pressures in the pipeline remain mild.

Final demand PPI was up just 1.7 percent in the year ending in January. That is higher than a few months ago but still well within the acceptable range.

The hourly wage grew just 2.4 percent in the year to January, lower than the average growth recorded in the previous recovery. Some measures of pay, such as the employment cost index, are beginning to show signs of acceleration. If that continues, it will indicate that the economy is reaching full employment, and that policymakers need to begin to lean against economic growth.

Appendix