Governance frameworks: has been saved

Insights

Governance frameworks:

ME PoV Summer 2022 issue

The challenges facing governments nowadays are not easy. Such challenges include, but are not limited to, geopolitical tensions, macroeconomic factors (inflation, recession, cost of living crisis, etc.), climate change, robotics, and disruptive technology. Alongside these challenges comes increased scrutiny of performance, and a need to enhance governance practices that help government organizations navigate these complexities and uncertainties. To add to this, citizens and taxpayers are becoming more skeptical; they want to know how public money is being spent, about the quality of services provided, and about the overall value derived vis-à-vis the taxes being paid.

There is no doubt that good governance in the public sector will result in enhanced management, performance, and stewardship of public funds. Whilst publicly listed companies are following a very strict and rigid corporate governance framework in most of the financial markets globally, there have been several failures (such as the Enron scandal), in addition to increasing and evolving codes, which have also led to more emphasis on governance for the public sector. However, policy makers are facing challenges in deciding which governance framework to adopt to ensure a balance between public interest, central government requirements, and regulators’ requirements, and at the same time, achieving sufficient resilience in running the affairs of the public entity.

There is no “one size fits all” for public governance

There are fundamental differences between governance in public and private sectors. As a starting point, the type and nature of government “bodies” vary – departments, councils, authorities, and both commercial and non-commercial entities. Furthermore, the ecosystem within which they operate is multifaceted and complex. The governance requirements for such bodies are not the same as those for privately owned entities. In the public sector context, good governance is central to the effective operation of those bodies and importantly plays a key role in supporting them to discharge their obligations as set out under law and driven by wider government policy. As such, it can be concluded that there is no “one size fits all” for government and public sector entities.

Conformance and performance dimensions

Principles of governance can be indicated in two dimensions: conformance and performance. The government policy makers often focus on the conformance aspect by emphasizing on meeting the expectations of external scrutiny through compliance with various laws and following acceptable and defensible governance standards. On the other hand, the performance aspect is often overlooked and little focus is exercised on the strategic activities and maximizing the benefits flowing to stakeholders. While the former focuses on accountability and responsibility to demonstrate due diligence under the law, the latter has a leadership role linked to the execution of business activities and, therefore, has more of a business orientation.

Governance frameworks

What types of standards and codes are relevant?

Several countries and bodies have developed guidance documents to support good governance in the public sector, such as the following codes:

Corporate Governance Code forCentral Government Departments 2017 |

|

Protocol on Corporate Governance in the Public Sector |

|

|

Code of Practice for the Governance of State Bodies 2016 |

|

Building Better Governance |

Globally, there are three types of guidance issued to support good governance in the public sector:

- Department standards – these are governance principles issued to drive good governance within the government departments

- Behavioral/conduct codes – these are standards of ethics that those working in public office (including senior leadership and board members) are required to follow.

- Governance codes – key requirements for state bodies, often covering both commercial and non-commercial entities.

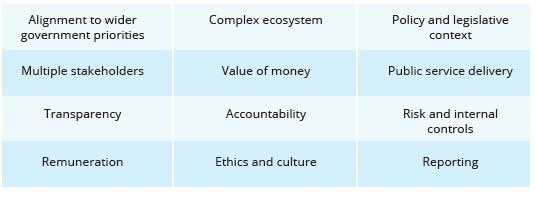

Yet, and regardless of the types of guidance issued, they all have common themes to be addressed which are depicted below:

Practical steps for policy makers

With the several codes of governance and the differences in each government entity’s mandate, environment, and regulations, government policy makers are recommended to implement the following steps:

- Select the standard/code that is relevant to them: Government entities should agree on the code/standard that best fits the organization; that’s in addition to the agreement on the main government principles that will be applied, which are relevant to the strategy, mission, vision, and values of the organization.

- Undertake a current state assessment: The current state assessment would identify gaps that prevent the government entity from reaching the level of maturity expected from the different stakeholders.

- Address the gaps: Government entities shall develop a road map of implementable initiatives to transform the governance status from “as-is” to “to-be.”

- Ensure clarity on the mandate: The mandate and expectations of the government entity should be known, aligned, and agreed with the different stakeholders and/or central governments.

- Consider agreeing on service-level agreements (SLAs) with other government entities: Government entities should consider agreeing on SLAs with other government entities when there are intersections in operations. SLAs could include a responsibility assignment matrix (RACI matrix), communication plan, escalation procedure, etc.

- Ensure clarity of roles and responsibilities internally: Roles and responsibilities between the different departments/units within the government entity shall be clear, agreed, and communicated to all concerned parties. Some of the main enablers that would support such clarity include: an internal Delegation of Authority (DOA), RACI matrix, committees’ charters, etc.

- Internal controls framework: Government entities shall focus on implementing a robust internal controls framework that is fit-for-purpose. The internal control framework could include the following: control environment, risk assessment, control activities, information & communication, and monitoring.

- Keep the governance under regular review: The regulations, risks, and operations are dynamic, and therefore there is a need for a regular check and assessment of the governance framework that is implemented in the government entities to ensure that the right selection of codes/principles are still valid, and there are no major gaps in the implementation of the framework that could prevent the organization from reaching its targets.

In the end, policy administrators could adapt the governance framework that they best see fit for the type and mandate of their organization. However, it is recommended that the adapted governance framework, that could enable and enhance the trust in government, reduces uncertainties to stakeholders and citizens, and achieves sustainability.

By Wael M. Kaafarani, Director, Risk Advisory, Deloitte Middle East and Melissa Scully, Director, Corporate Governance, Deloitte Ireland

Endnotes

- Utami, M., & Silvia Sutejo, B. (2018). The importance of corporate governance. January 2012. https://doi.org/10.2991/insyma-18.2018.24

- OECD Guidelines on Corporate Governance of State-Owned Enterprises, 2015. Access here: OECD Guidelines on Corporate Governance of State-Owned Enterprises 2015 (oecd-ilibrary.org)