Article

What’s beyond the peak?

CEE loan markets still offer new opportunities

In the 7th edition of our annual report reviewing recent trends of non-performing loan portfolio markets in the CEE region, we provide an overview on the main developments of the CEE NPL market, analysing the evolution of key NPL metrics as well as the dynamics of loan portfolio transactions. As a novelty, this year’s report is covering Albania as well, increasing the number of analysed countries to fifteen.

Explore Content

- Key findings

- Improvement of asset and credit portfolio quality

- Consolidation of banking sector

- CEE NPL markets are still benefiting from solid deleveraging activity

- Get in touch

Key findings

Deleveraging via disposals remained an important option to address non-performing loans among financial institutions in the CEE region. Although, CEE loan sales markets recorded a subdued activity in 2017 and 2018 H1 compared to record deal-making in 2016 as banks have been gradually decreasing their NPL portfolios to a sustainable level. As a result of continuously diminishing NPL portfolios, competition remained strong on the demand side mainly among investors who have already built their servicing capacity in the region. However, the tools of credit portfolio management also included significant write-offs of bad debts as well as restructuring agreements instead of traditional in-court and collateral enforcement proceedings.

Improvement of asset and credit portfolio quality

The improvement of asset quality is evidenced in the NPL ratios gradually trending back to single-digit figures or even converging the pre-crisis level in some countries. This was also stimulated by the recovery of lending activity driven by the continued positive trends in the macroeconomic environment. The economic upturn also contributed to a better financial position of both corporates and households, which gave a stimulus to the repayment of legacy non-performing loans.

The improvement of the credit portfolio quality is also evidenced in the declining default rates that are indicative of the inflow of new NPLs. Nevertheless, time since the rebound of lending is relatively short to draw robust conclusions in terms of the NPL formation in the coming years. The expected rise in interest rates from the historical lows may also put pressure on the debtors’ repayment capacity.

Consolidation of banking sector

The outlook of the CEE loan sales markets envisages a miscellaneous picture. Activity on markets that have already tackled most of their NPLs are likely to gradually subside in the coming years and the trade of other non-core assets – among others performing leasing and loan portfolios, subsidiaries of financial institutions as well as servicing platforms – will gain momentum. This trend will be driven by the consolidation of the banking sector as well as banks’ efforts to reshape their portfolios and divest assets considered as strategically non-core. On the other hand, we still anticipate some larger transactions on markets considered to enter the final phase of the deleveraging process as newcomers are assessing the option of selling their non-performing loan books in order to accelerate the balance sheet clean-up.

CEE NPL markets are still benefiting from solid deleveraging activity

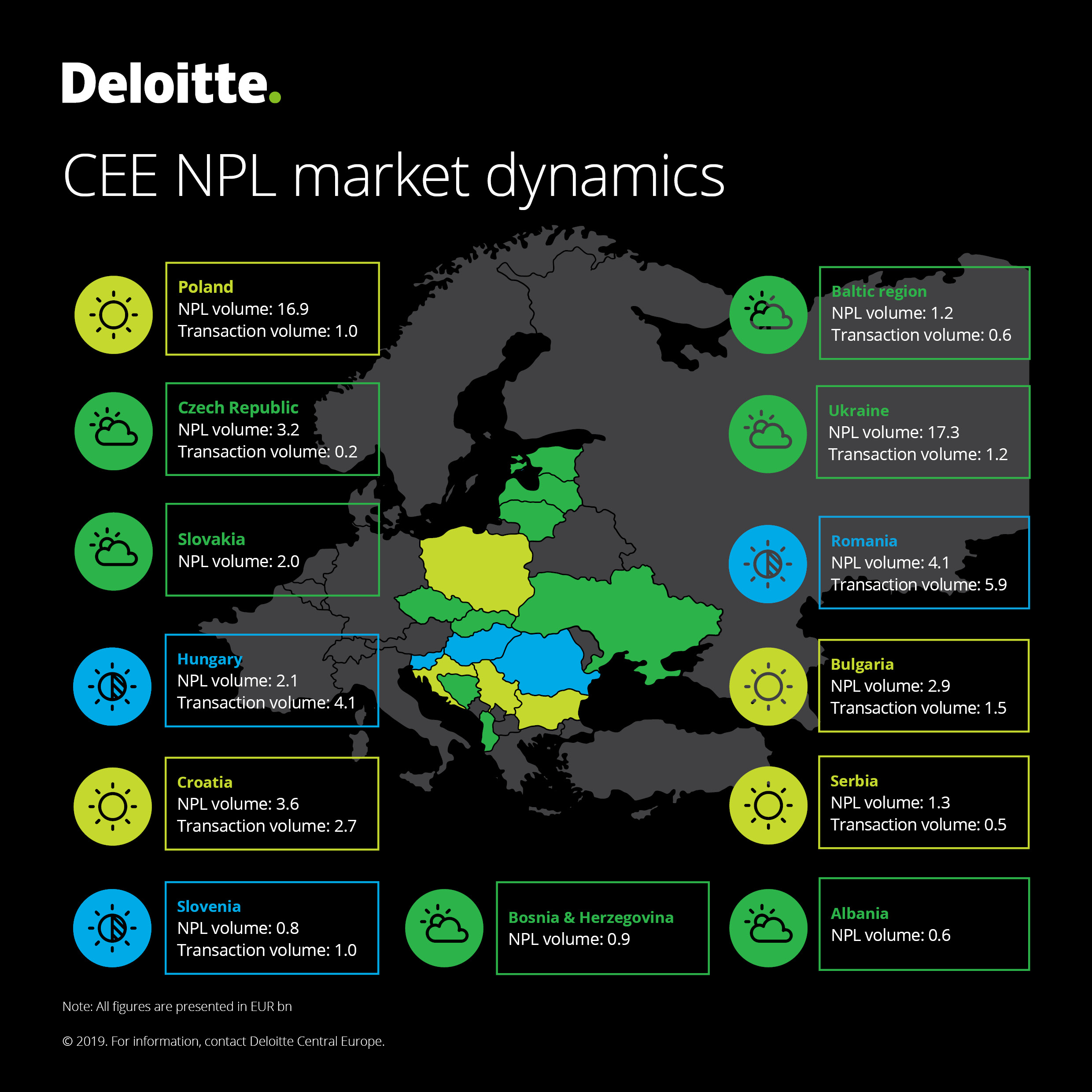

Romania, Hungary and Croatia have experienced a strong transaction track record between 2015 and 2017 with just over EUR 9.5bn worth of deals concluded. In addition, we observed continued interest from international and domestic investors on these loan sale markets based on the volume of transactions completed in 2018 H1 as well as the number of reported ongoing transactions.

Relatively untapped markets with potential future deal flow are Ukraine with its sizeable NPL market, and also Bosnia and Herzegovina and Albania where no major loan sales activity has been reported so far. International and domestic NPL investors keep an eye on the Ukrainian market mainly due to the material supply of non-performing corporate loans, however the desired stimulus to the legal and insolvency framework as well as the infrastructure of distressed debt market is still awaited. Robust provisioning of NPLs potentially contributes to a reduced pricing gap between the investors and sellers, which could also promote the number of deal-makings.

Download previous editions

- NPL Study 2018 (PDF, 4.8 MB)

- NPL Study 2017 (PDF, 4.8 MB)

- NPL Study 2016 (PDF, 1.5 MB)

- NPL Study 2015 (PDF, 1.5 MB)

- NPL Study 2013 (PDF, 15 MB)

- NPL Study 2012 (PDF, 6 MB)