Consumer Duty Benchmarking results – General Insurance Market has been saved

The Financial Conduct Authority’s (FCA) Consumer Duty (Duty) regime is now live. Given the Duty is a topic that requires significant judgement, we carried out a benchmarking survey on the General Insurance (GI) market to understand its progress and priorities.

40 firms participated, including company insurers, Lloyd’s managing agents, brokers and MGAs. We thank these firms for their participation!

The topics included in the survey were:

In this blog, we look at four of these benchmarking topics and use them to summarise what we think the results say about the GI market’s progress and priorities. Please get in contact if you’d like to discuss the full results.

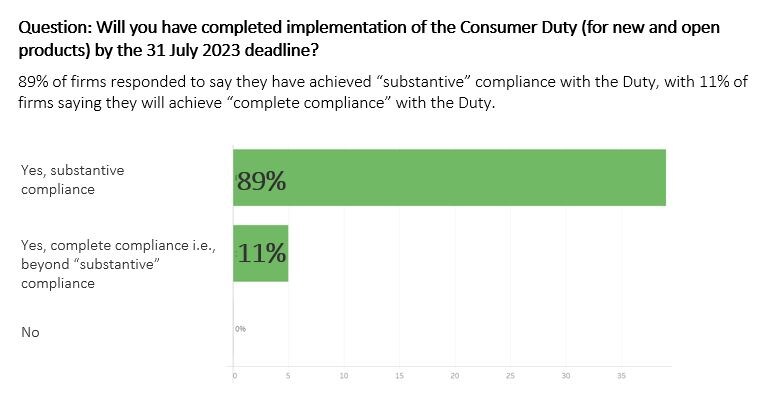

1. Has the market completed implementation by the deadline? 100% say they have achieved compliance, with 89% saying this is “substantive compliance”.

The first question we asked firms was, “Will you have completed implementation of the Consumer Duty by the 31st of July?” 100% of firms said they have achieved compliance, and we know the significant amount of work undertaken by many GI firms to address the Duty requirements.

We found it interesting that the concept of “substantive compliance” has been acted on by such an extent of the GI market, with 89% of firms saying they will be in “substantive compliance” vs 11% of firms saying they will have “complete compliance”.

We then asked firms how they had interpreted “substantive compliance” and we provided three high-level options based on how much of the Duty has been addressed and across how much of the firm’s business. There was a pretty even split of responses across these three options.

So, what does this mean? Substantive compliance is open to interpretation, and there is likely to be different interpretations and progress across firms. Companies will need to be able to respond to questions about how they have evidenced this compliance. They will then need to progress beyond “substantive compliance” as part of “Day 2” activity, in addition to focusing on enhancing and embedding the framework.

It's also crucial for firms to remember that this regulation focuses on customer outcomes, so evidence of customer outcomes and how foreseeable harm is being addressed is fundamental.

2. Has there been an improvement in the customer-centric culture and governance challenge linked to your work on the Duty? Most firms say yes, which is positive.

We wanted to understand whether firms had already experienced improvements in their culture and governance because of their work on the Duty. The results were positive, with 78% of firms improving their customer-centric culture and 85% experiencing increased governance around customer outcomes.

The Duty is bringing more information to the fore on products, pricing, distribution and value, all of which have commercial considerations. The specific decisions firms make concerning products, distribution, and value are key indicators of culture. Our benchmarking results provided insights on the extent of product and distribution change by the GI market to enhance customer outcomes due to the Duty requirements.

Examples where we see challenges from Boards and Committees, include: challenging and acting on specific Management Information (MI) relating to customer outcomes and harms; accuracy, completeness and automation of MI; effectiveness of working with other firms in the distribution chain; sustainability and efficiency of the framework; operating models of the relevant teams operating in the 1st Line of Defence (LOD); and prioritisation of the “Day 2” activity and evidence of compliance.

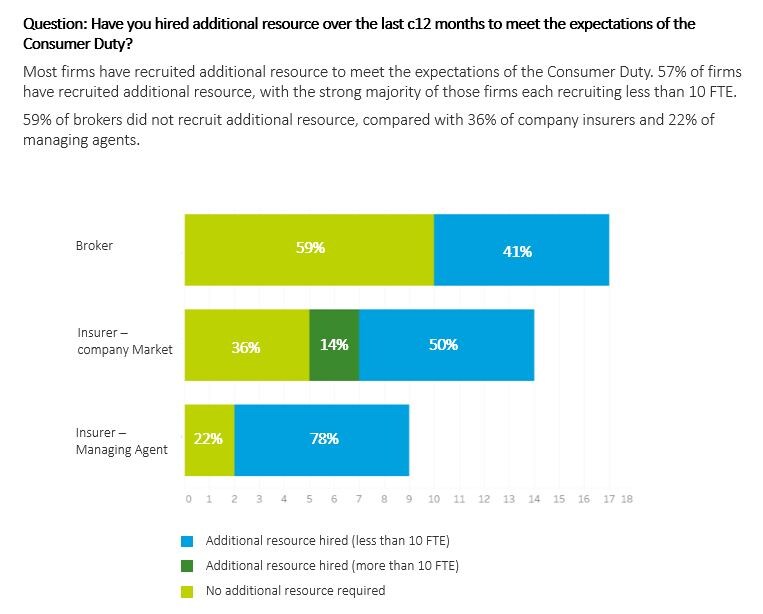

3. Have you hired additional resource to meet the expectations of the Duty? The majority of firms have recruited additional resource, which we see is leading to revisiting 1st LOD operating models and indicative of a largely manual process.

We wanted to understand the extent of recruitment in the market driven by the Duty. 57% of firms have recruited additional resource to meet the expectations of the Duty, with recruitment undertaken by 78% of managing agents, 64% of company insurers and 41% of brokers.

In our experience, recruitment has primarily been into the 1st LOD, including conduct and product teams, teams overseeing distribution and teams undertaking customer outcomes testing/assurance. This increase in headcount, a trend we’ve seen over the last few years with related regulatory topics, is leading firms to revisit their 1st LOD operating models and team structures so that they work effectively and align well with the Risk and Compliance functions in the 2nd LOD.

This benchmarking result also supports our view that these new and enhanced frameworks to address the Duty are largely manual and currently require hard work by people to implement and embed. Our next benchmarking result supports this view.

4. What do you need to do next? The top “Day 2” priorities for firms are Management Information and Technology/Automation.

There is a significant “Day 2” focus for firms, with ongoing enhancement and embedding required. Some firms are delivering this through ongoing project management support, while others are transitioning this into the business.

With 75% of firms focussing on their Management Information, there is a clear need for the Duty frameworks to produce more actionable insight. A measure of success for firms will be identifying areas within their business that require action to enhance customer outcomes and address foreseeable harm. This could relate to products, distribution, communications or support and could be regarding specific customer cohorts or vulnerabilities. Useful, accurate, well-structured and timely MI brings the right information to the fore, so that action can be taken.

The second priority is Technology and Automation, with 48% of firms focussing on this as part of “Day 2”. This supports our previous point that we believe frameworks are predominantly manual and the right technology can strengthen the Duty control environment; increase the effectiveness, accuracy and efficiency of process; produce instant MI and increase accountability.

With 30% of firms saying the fair value assessment process is more challenging this year compared with last year, it suggests automation will be critical. One example of how firms are using technology to automate their Duty approach is Deloitte’s OneView: Product Governance solution, which automates the product governance, fair value assessment and distributor data/oversight process.

Other focus areas for “Day 2” include how other new and important regulatory topics are considered within the Duty framework. Three examples are:

- The consideration of “greenwashing risk” within the framework. Only 5% of firms in our benchmarking have considered this within their Duty approach so far;

- The FCA’s new concept of “policy stakeholders” and the impact of this on different GI products and customers. See our blog, which originates from the FCA’s focus on multi-occupancy buildings insurance; and

- The upcoming introduction of heightened expectations for fraud control frameworks. You can read our blog on this topic here.

We hope these benchmarking insights are helpful. It’s clear that the Duty is a priority for the GI market, and the market has been working hard to address these requirements. Now that we are on “Day 2”, firms will need to re-focus their activities and concentrate on embedding frameworks, enhancing MI to produce actionable insights and using technology to strengthen the Duty control environment.

Key Contacts

Christopher Jamieson

Partner

Chris focuses on strategic regulatory and operational change across financial services, helping clients evolve through practical and risk-based advice to major regulatory topics, as well as through the use of RegTech solutions.

Adam Knight

Partner, Insurance Risk and Regulation

Leading Deloitte’s General Insurance Regulatory and Strategy team. This work includes internal audit, due diligence, section 166 reviews, control framework reviews (including risk, compliance, internal audit and governance) and other bespoke regulatory work, for example conflicts of interest reviews.

David Clements

Partner

David has 25 years’ experience in the financial services industry and has significant experience across Retail Banking, Wealth Management and Insurance markets. David leads our National Retail Conduct and Governance team. David specialises in advising on compliance and conduct risk issues, ranging from SMCR, the design and development of conduct risk strategy and frameworks, leading our conduct assurance activity, including skilled person review and leading many of our large scale complex regulatory transformation projects.