The hotel industry prepares for a prolonged recovery | Deloitte UK has been saved

As the hospitality industry across Europe and the UK continues to face headwinds posed by the pandemic, we reinstated our Hotel Sentiment Survey to explore the expectations and priorities of leaders in the sector. The survey indicated varying points of view, while we saw an improvement in sentiment on the length of disruption, expectations on the pace of recovery have shifted further out.

Sentiment on disruption has shifted towards the longer term with 71% of respondents expecting it to last beyond 2021 compared to the results seen in the October survey (59%). On a positive note, the majority (28%) now believe that disruption will last up to the first half of 2022, compared to the previous survey where the majority (24%) expected disruption to last until the second half of 2022. Though the results also show that nearly a quarter (24%) believe it will last until at least 2023.

When we consider the pace of recovery, respondent sentiment has deteriorated as 90% now believe that performance will not return to pre COVID-19 levels until at least 2023, compared to 71% in the October survey. While more than half (52%) expect 2023 to be the year of recovery, 38% expect recovery only in 2024 and beyond.

When asked what the key priorities over the next four weeks were, the majority stated that cash management remains the top consideration. Transactions and expansion moved up the ranks as the second priority, climbing 10 percentage points, at the expense of financial considerations which fell by 20 percentage points. The significance of remote working capabilities has also decreased. The two new priorities added in this survey, strategic growth initiatives and preparing for the withdrawal of government support ranked fifth and eighth, respectively.

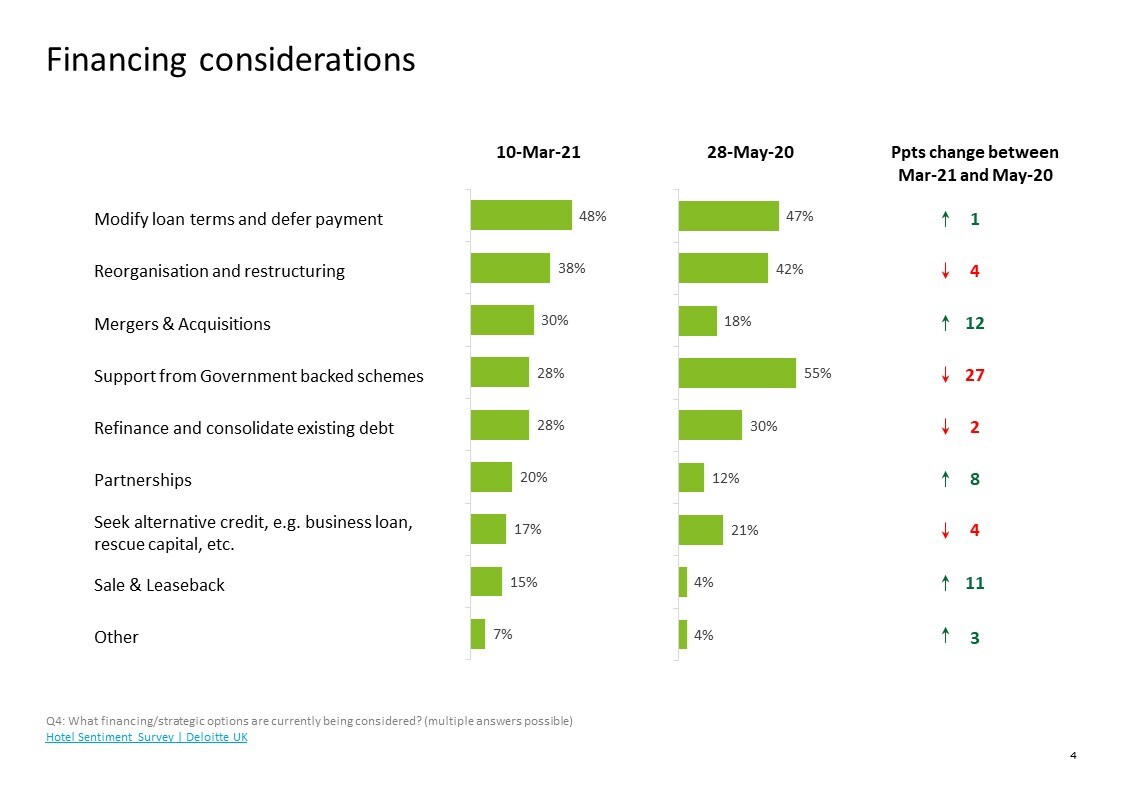

Turning next to financing and strategic options being considered, our survey revealed that nearly half are modifying their loan terms and deferring payments, and more than a third are considering reorganisation and restructuring. Compared with the results from the survey conducted in May 2020, mergers and acquisitions as well as sales and leaseback options have seen a significant rise in consideration, while support from government-backed schemes have halved.

Tax relief was the main support business leaders expected from the government at 68% climbing 18 percentage points from the survey conducted in the same period in last year. While wage support and financial aid dropped by 13 percentage points and 12 percentage points, respectively, the new category of traveller support saw 44% wanting government intervention.

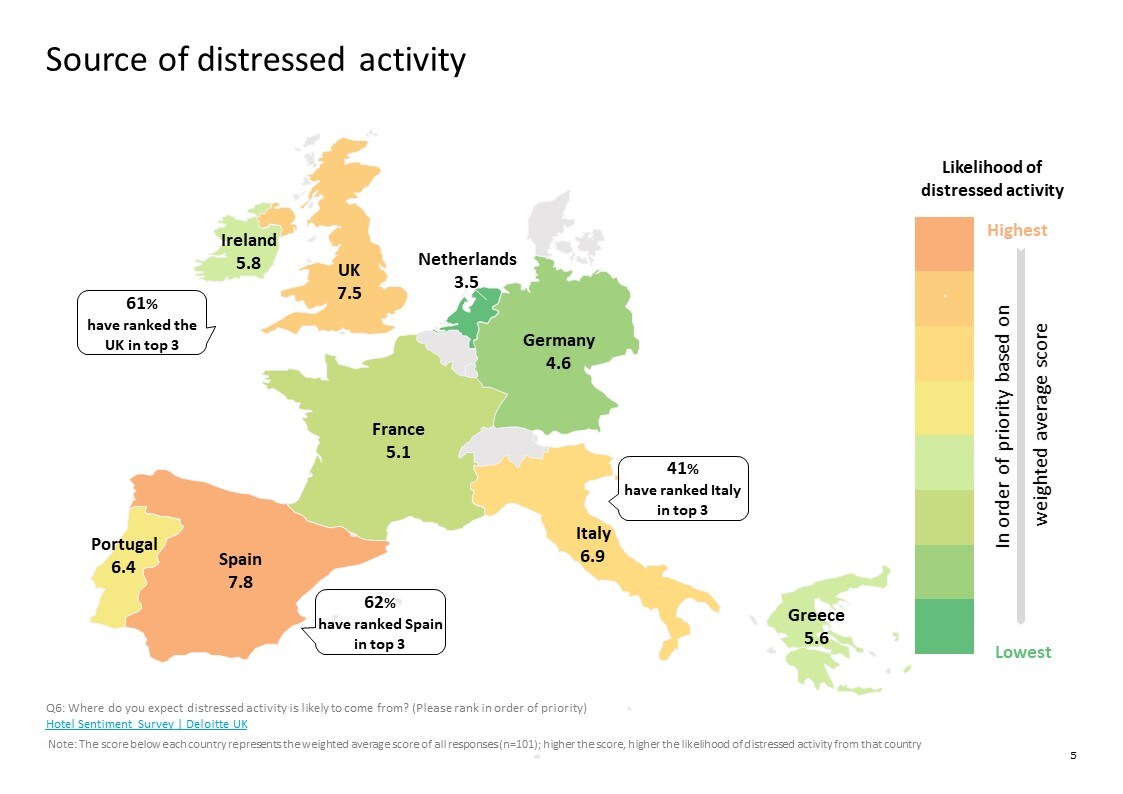

And finally, when asked where distressed activity is likely to come from, Spain emerged as the most likely source of distressed activity, closely followed by the UK and Italy. In order of priority based on a weighted average score, Spain ranked the mostly likely with 7.8 average score, followed by the UK. If we clubbed the top three countries where distressed activity is likely to come from, 62% ranked Spain in the top three, while 61% ranked the UK followed by Italy with 41%.

With new variants of the virus taking hold in some countries, uneven vaccine rollout across the UK and Europe and more countries looking at pre-travel testing and post-travel quarantine requirements and digital health passes, the hospitality sector is gearing up for a prolonged recovery.

For more details on the Hotel Sentiment Survey results and insights, you can access our EHIC hub.

Key contact

Simon Oaten

CFO Advisory Lead Partner

Simon is the lead Partner in the Deloitte UK CFO Advisory Practice and specialises in the Travel Hospitality and Leisure sector where he brings over twenty years’ experience. Simon has worked with some of the leading players in the industry in the UK, Europe and globally, in both the private and public sector.