{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Mexico has been saved

Cover image by: Jaime Austin

The Mexican economy ended 2020 with the largest drop in GDP since the Great Depression, contracting 8.3% in real terms from the previous year. The partial recovery that the country experienced during the third quarter of 2020 was nullified by a second wave of infections that resulted in additional lockdowns and suspension of economic activity.1 Additionally, in the first months of 2021, two events had a significant impact on industrial activity. First, a worldwide semiconductor dearth caused numerous auto plants to stop operations,2 and second, the country suffered natural gas shortages and power outages.3 Due to these factors, we were anticipating GDP to contract in the first quarter of 2021. Instead, the economy grew 0.8% quarter-on-quarter, buoyed by the solid recovery in the US economy and a milder-than-anticipated impact of the lockdowns (figure 1).

The vaccination efforts and restrictions on the movement of people helped curb the spread of COVID-19. As of May 2021, there were no states under the maximum alert levels of the epidemiological traffic-light monitoring system, the official tool to track the spread of the disease.4 And as of June 2, the total number of vaccines administered was more than 30 million (24% of the population), of which 12.6 million (9.8% of the population) were completely vaccinated (two doses).

The resultant increase in mobility and consumption has also contributed to the expansion of the services sector, which accounts for nearly two-thirds of economic activity. During the first quarter, it jumped 0.9% quarter-to-quarter in seasonally adjusted terms. Secondary activities (industry) rose 0.5% quarterly, with manufacturing activities contracting 0.2%, considering output disruptions due to chip shortages and power outages.5

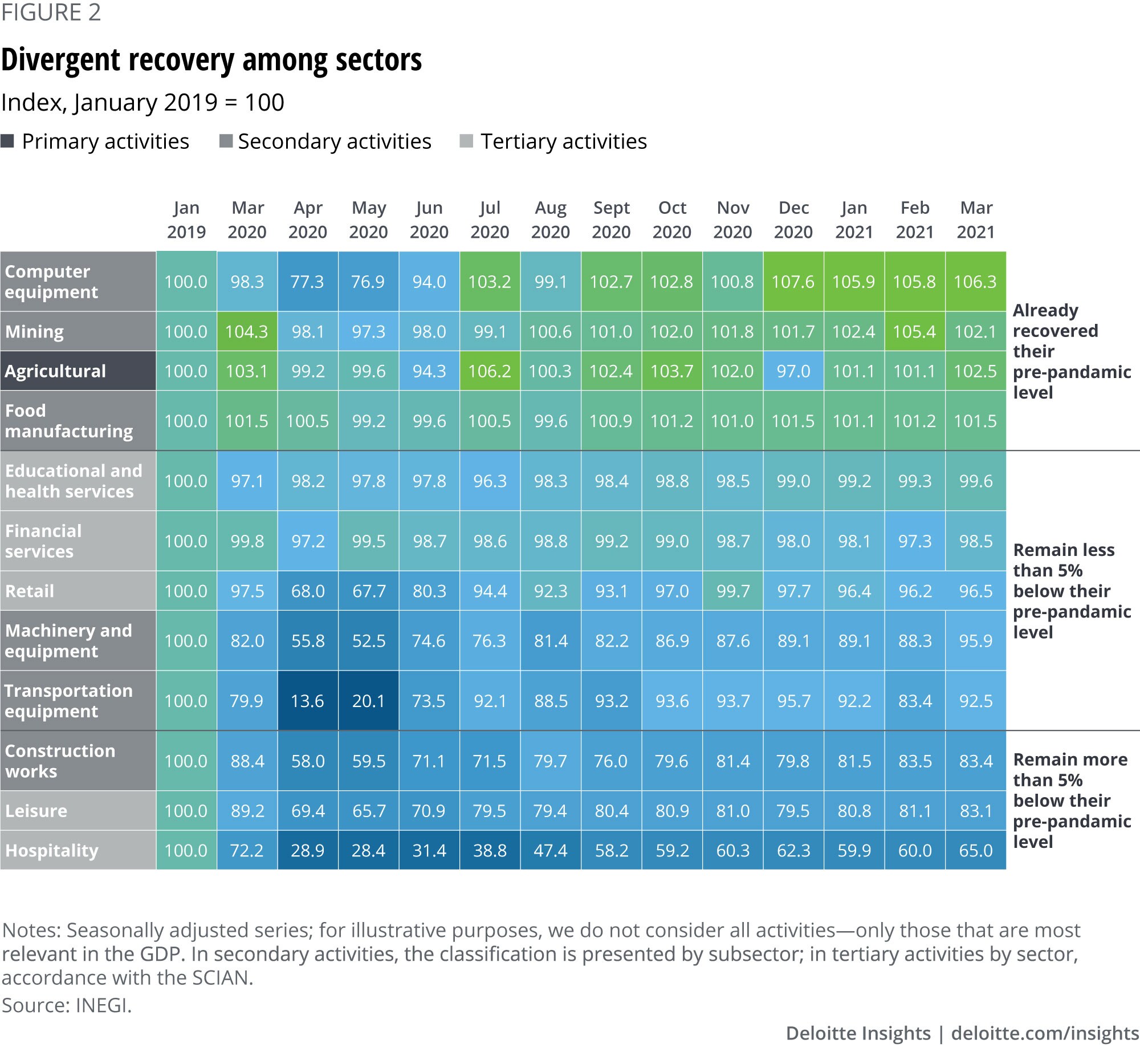

As figure 2 shows, the recovery has been divergent by industries. Export-related sectors, such as manufacturing and agriculture, have performed better, and many of them have already exceeded their prepandemic levels. Some activities related to the domestic market are also making progress, although at a more moderate rate. While the positive trend of export-oriented and consumer industries is a move in the right direction, the steep decline in other industries, such as leisure and hospitality, will remain a challenge. Tourism, an important source of revenue for multiple states, is well below prepandemic levels, and the recent decision of the Federal Aviation Administration (FAA) to downgrade Mexico’s aviation safety rating will put additional pressure on an ailing industry.6

The bold recovery of the American economy is bolstering Mexican exports to its northern neighbor. The trade balance saw a surplus of US$26.6 billion, or 2.4% of GDP, in 2020, the highest level recorded since data became available in 1993 (figure 3). In March 2021, exports grew 31% year over year to reach US$43 billion, the largest expansion in almost a decade. This growth was driven by machinery and metal manufacturing, which expanded 6.6%; electronics and professional equipment also registered expansions of 21.3% and 14.5%, respectively. Despite this strong performance, exports of automobiles and other transportation equipment contracted 5.2%. The automotive industry, one of Mexico’s most important industries, has also been impacted by the disruptions in the global supply chain of semiconductors.

The contraction in imports during 2020 explains the trade surplus. However, the recovery of the Mexican economy is also powering a rebound in imports. In March 2021, imports grew 31.4% annually, the highest increase in the last 15 months.7 Imports of consumer goods expanded 16.2% and intermediate ones rose 33.8%, while capital goods expanded 31.1%.

Remittances are also helping boost the economy: They rose 13%, from US$9.4 billion in Q1 2020 to US$10.6 billion in Q1 2021, the highest-ever level for a quarter since records began in 1995.8 It is very likely that this trend will continue throughout the year, setting records and surpassing 2020 data at US$40.6 billion, equivalent to 3.8% of GDP. This would help improve expectations and sustain private consumption.

The strong performance of the external sector has helped in mitigating the weakness of the domestic market. Although household consumption is gaining steam, it remains substantially below prepandemic levels. Until February 2021, private consumption was 6.5% below February 2020 and 7.2% below February 2019. In April, some variables indicated a more positive outlook. Retail sales rose 38.4% in real annual terms, and car sales jumped 16% month over month in March, although they contracted 12.5% monthly in April. While those figures are distorted due to the low base of comparison, since April and May were the months most affected by the pandemic, they indicate a more dynamic market. Additionally, the consumer confidence index rose to 42.4 points, its highest level in 12 months.

However, there is another factor associated with the domestic market that remains sluggish: private investment (figure 4). A series of domestic policy decisions have caused some concerns about the investment climate in the country.9 The government has already approved a new electricity industry law10 and a constitutional initiative to reform the energy law, which strengthens the position of the state oil company Pemex.11 While the new electricity law has been barred by the judiciary, its approval did not fare well among potential investors and the private sector.12 Figure 4 highlights several factors associated with the long-term decrease in the investment performance, such as the cancellation of the new airport construction, oil bid rounds, and special economic zones, as well as the resignation of the former Treasury head.

Mexico responded to the pandemic with a smaller set of countercyclical incentives, compared to other emerging economies.13 While there was criticism for not supporting those most impacted by the pandemic, it had a positive effect on public finances, which allowed the country to close 2020 with better numbers than expected. This situation resulted in a stronger fiscal position compared to its regional and even global peers (figure 5).

However, this has a two-sided impact, as the absence of a debt-financed fiscal response factors into the depth of Mexico’s downturn, particularly affecting private investment, consumer consumption, and the labor market. Unemployment was near 4.7% in April, but if we consider the population that remains outside the labor force and would accept a job if proposed, the unemployment rate jumps to 16.0%.14 This remains consistent with our earlier findings that the close down of firms has likely led to a persistent downshift in employment.15

Additionally, this situation has increased poverty and exacerbated inequality among workers. The percentage of people who had an income lower than the value of the basic food basket grew from 37.3% in 2019 to 40.7% at the end of 2020 (figure 6). Meanwhile, 80% of people saw a decrease in their income.16

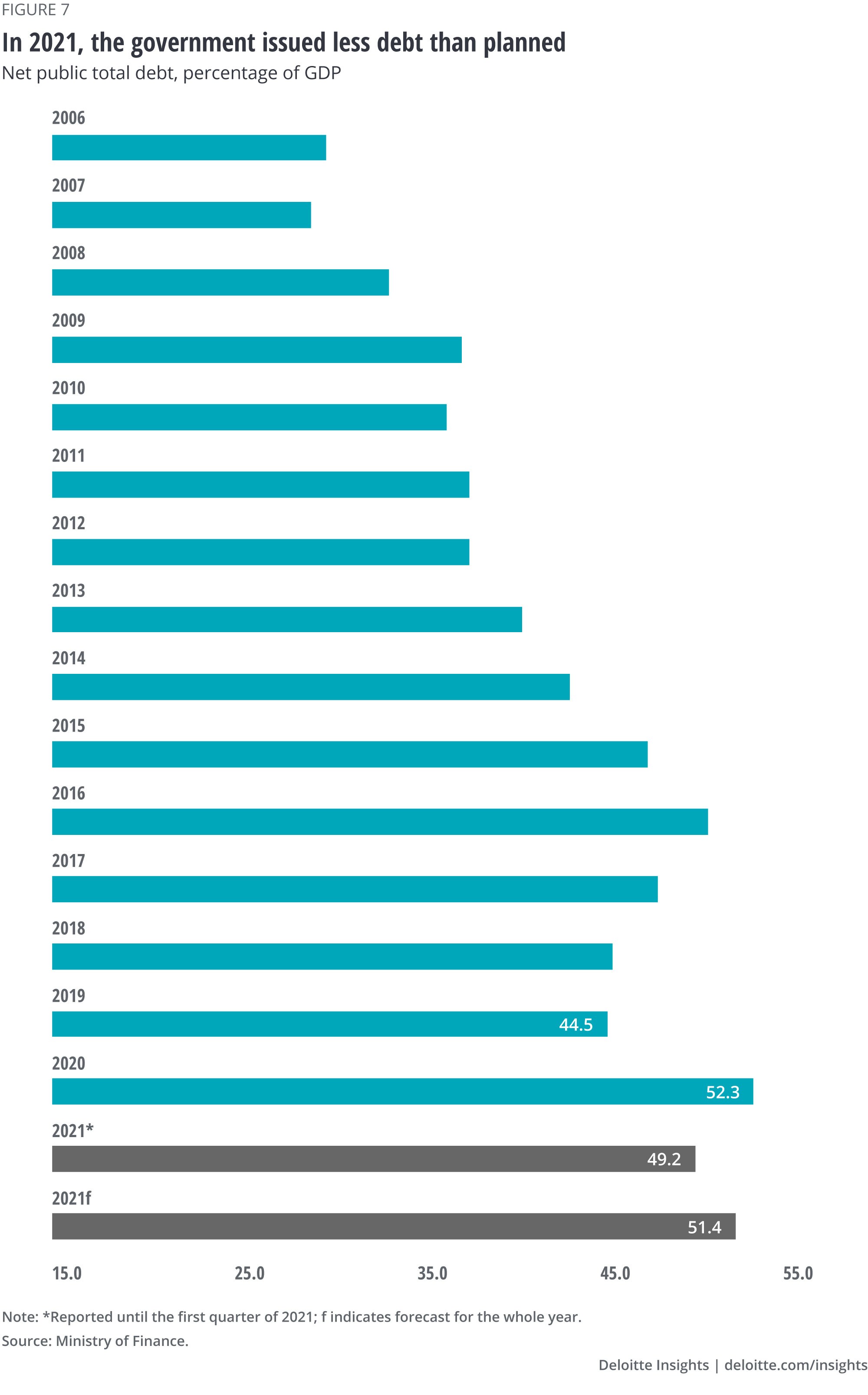

In the first quarter of this year, the government continued to spend less than planned, while obtaining higher revenues, mainly due to larger oil earnings and the use of some nonrecurring sources earmarked for emergencies. Thanks to this, the main fiscal metrics are quite positive: The fiscal deficit is shrinking and debt over GDP has once again fallen below 50% (figure 7).

Although these numbers have led rating agencies to maintain their outlook,17 the sluggish recovery will strain the security of revenue sources. Moreover, Pemex will continue to need the injection of federal resources to stay afloat and, as the year ends, the money from nonrecurring sources will cease.18 Currently, the balance of the Budgetary Income Stabilization Fund is US$0.77 billion (15.8 billion pesos), 90% less than what it was at the beginning of 2020. Because of this, Mexico’s government is studying the need for a tax reform,19 which is likely to be proposed later this year or in the first half of 2022.

As Mexico emerges from lockdowns—and the rate of vaccination speeds up20—the economy seems to be gathering steam, particularly in terms of domestic demand, which has thus far lagged behind its external counterpart. One important thing to note is that even if lockdowns are re-established, they will likely have a more moderate impact on economic activity than we anticipated. This is the reason we are upgrading our growth forecast for this year to 5.1%, from 4.5%.

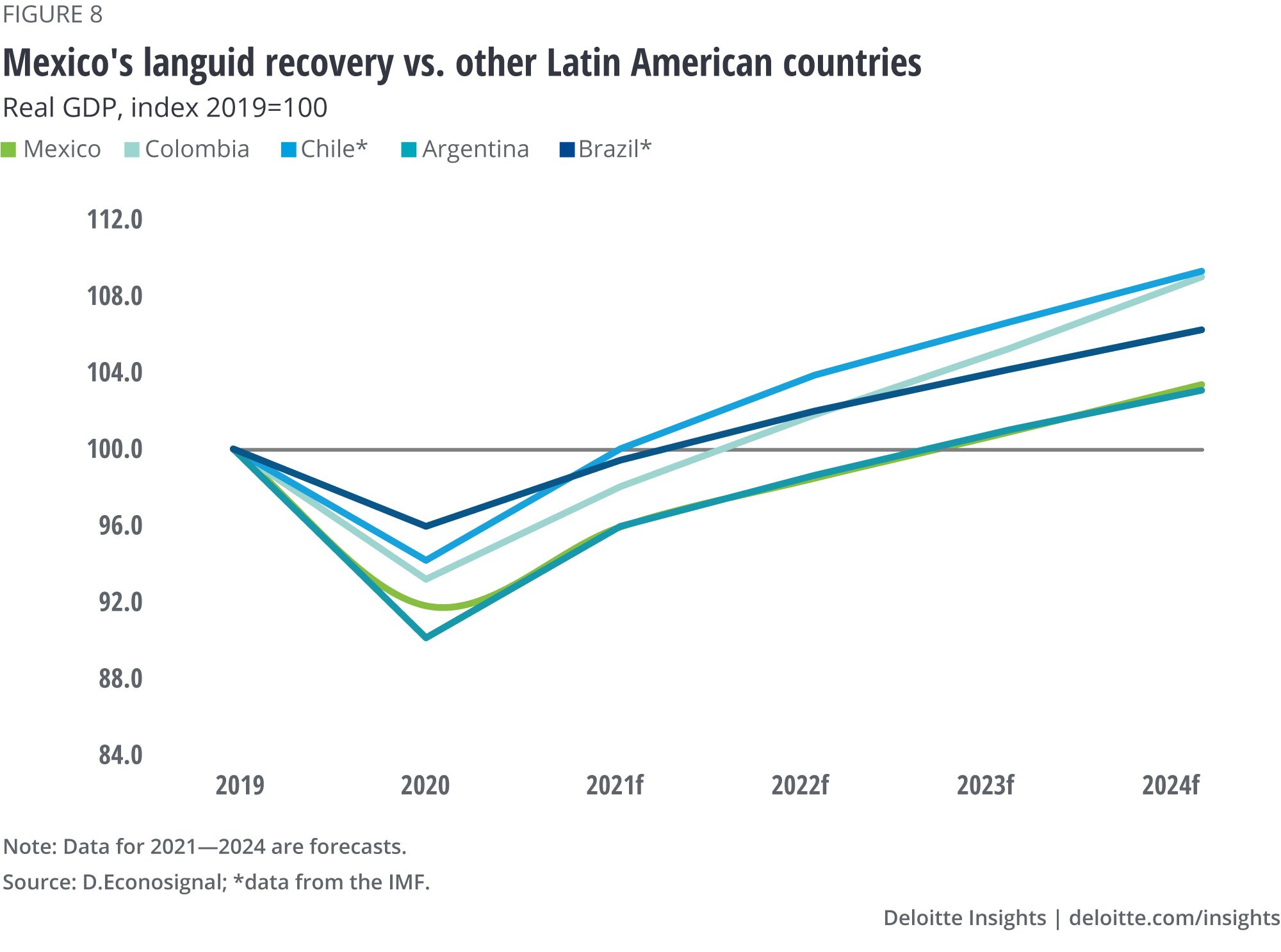

Despite the rebound, the economy will not be able to reach the prepandemic levels for a while. Apart from the factors mentioned above, such as insufficient economic stimulus and the lack of policies that promote and generate investment in a long-term perspective, the Mexican economy has exhibited a languid behavior since 2019, when GDP contracted 0.2%. Because of this, we expect the country to not achieve its prepandemic levels until 2023 (figure 8), being one of the largest countries in Latin America that will take the longest to recover.

In conclusion, we expect growth to be driven by exports, mainly industries focused on the consumption of durable goods, such as household appliances, electronics and furniture, propelled by strong economic stimulus in the United States. This will help alleviate the sluggish domestic market—it’s mostly private investment that will remain depressed as economic policy is not likely to generate enough confidence among investors.

Cover image by: Jaime Austin