India Modi 2.0 begins amid economic headwinds: What to expect next?

8 minute read

02 August 2019

Political stability has come at a time when growth is slowing. The new government's budget has set the tone for its policy response, with the focus on investment, jobs, and infrastructure.

The month that was: May 2019

May 2019 turned out to be a power-packed month for India, with the much-awaited—and unexpected—general elections 2019 results and rather disappointing Q4 GDP and unemployment data being announced back to back.

The Bharatiya Janata Party (BJP), led by the current Prime Minister Narendra Modi, emerged the single-largest party and got a majority in Lok Sabha (the lower house) for the second consecutive term. Interestingly, the electoral mandate this time is even bigger than in 2014 (figure 1), with BJP and allies winning 353 seats of the 542 seats contested; 272 seats are needed to form a government. BJP alone won 302 seats, 21 seats more than in 2014—a performance that none of the surveys or market participants had predicted. The results are a resounding endorsement of Modi's popularity, his government's achievements in the past five years, and his campaign that centered on national security, nationalism, and development.

What is remarkable about this election is that this is the first time since 1971 that an incumbent prime minister has secured an absolute majority for their party for a second successive term by winning even more seats than before. Not just the election outcome this year, but the general election too broke several electoral records. Voter turnout was 67.11 percent, the highest ever for any general election in India. It surpassed the 66.4 percent voter turnout in the 2014 elections, which will now be the second highest. For the first time, the voter turnout of men and women was almost equal, with the gap narrowing down significantly from 9 percent to only 0.4 percent over the past decade.1 This election saw not only the largest number of women candidates, but also the largest number of women who won. The proportion of women candidates to total, however, remained less than 10 percent.

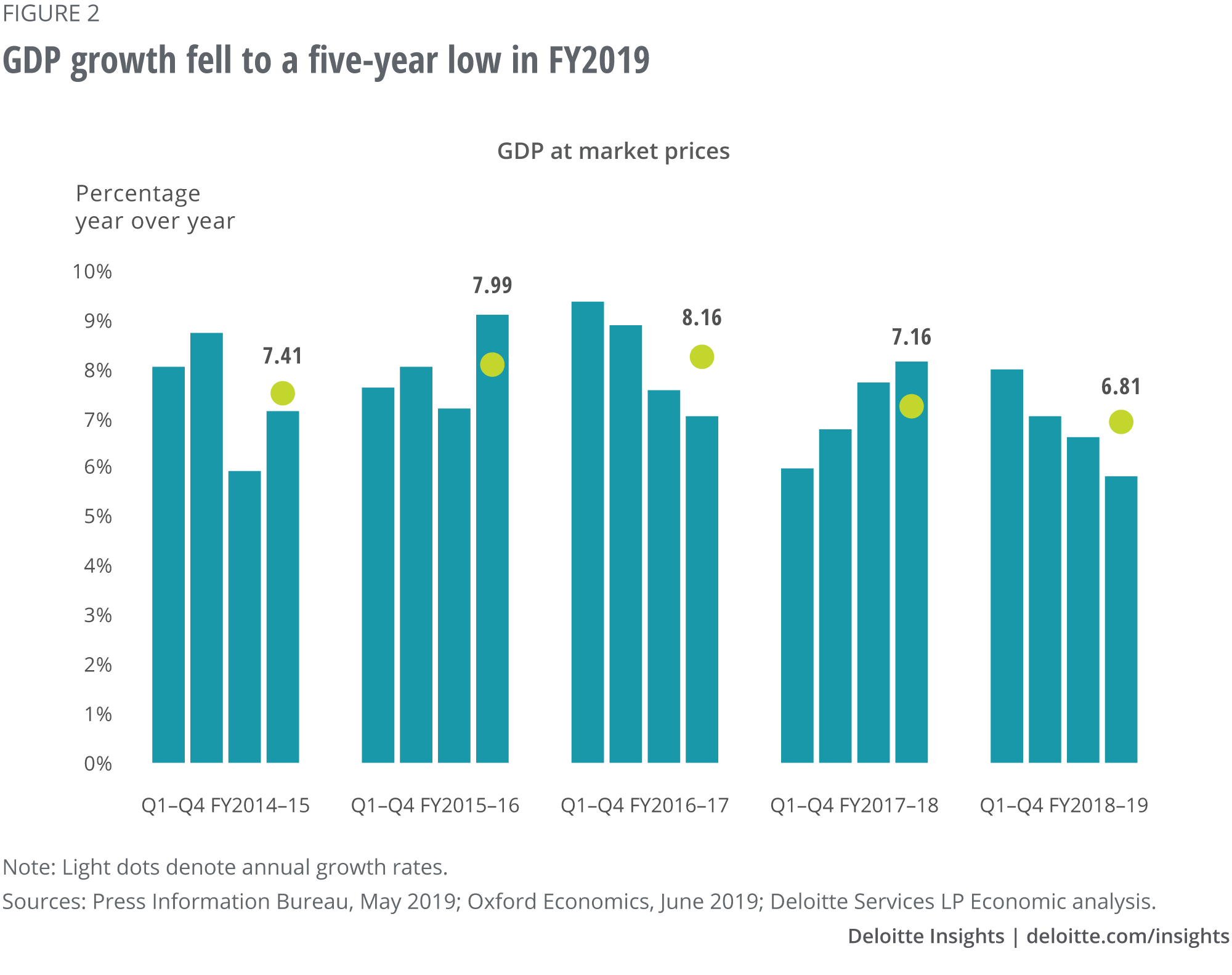

The other major events of the month were the data release of GDP for Q4 FY2019 and the unemployment rate for the July 2017–June 2018 period on the last day of the month. GDP data came in lower than expected, printing a five-year low of 5.8 percent year over year in Q4 FY2019 (figure 2). Annual growth for FY2019 was 6.8 percent year over year compared to 7.2 percent year over year in FY2018. Private domestic demand performed even poorly at 6.4 percent year over year, indicating government spending helped boost growth last year.

Private final consumption expenditure, which has been the sole engine of growth, declined. One of the primary reasons for the drop was rural distress and tightening lending conditions, which were, in turn, a result of ailing health of the financial institutions, specifically the nonbank financial companies. At the same time, growth in gross fixed capital formation dipped to 3.6 percent in Q4 FY2019 because of political uncertainty.

On the industry side, construction and manufacturing registered better growth than in FY2018, but growth in agriculture and allied activities as well as in mining declined significantly, resulting in poor rural income. Services, the biggest contributor to GDP, grew by 7.5 percent, half a percentage point slower than last year.

According to the data released by the Ministry of Labour and Employment, the unemployment rate was 6.1 percent in 2017–18, with the youth unemployment rates in urban and rural India being 7.8 percent and 5.3 percent, respectively.2 While it is being claimed as the highest joblessness rate in 45 years, it is worth noting that there has been a change in the measurement design and matrix this year. Therefore, an apples-to-apples comparison with previous years is difficult.3 There were more males unemployed than females, and urban unemployment was higher than rural unemployment. However, one has to be cautious in drawing conclusions from this data as unemployment in rural areas and among women is often underreported due to several factors, such as the existence of disguised unemployment among farmers, women’s role in households and families, and their inability to declare themselves as working because of societal norms.

Policy prudence is the way forward

While the single-party majority mandate has set the foundation for a stable central government for another five years, significant headwinds potentially lie ahead. Domestic risks (such as slowing demand and poor health of the banking sector), together with external risks (from uncertainties around global trade), will likely impact business investment and credit growth, and thereby, growth.

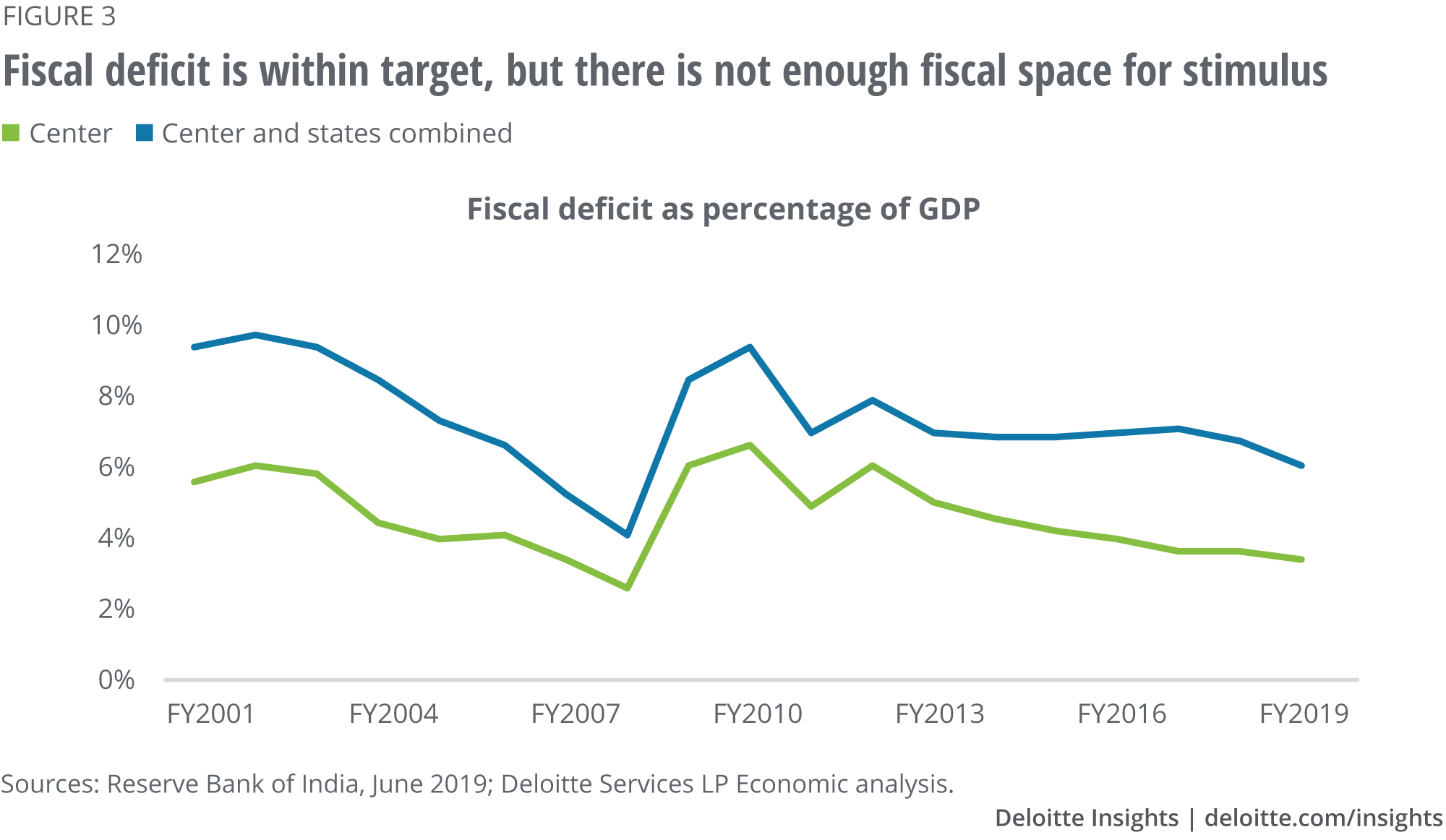

However, the government does not have many weapons to manage decelerating growth. Room to maneuver the fiscal policy is limited. India’s general deficit, or the combined fiscal deficit of the center and states, was 5.9 percent in FY2018 and is likely to increase in FY2019 due to higher spending by the states ahead of elections (figure 3). For the center, the government has pegged its FY2019 fiscal deficit target at 3.4 percent. Nonetheless, public sector borrowing requirements remain high, and any further rise may crowd out private investments and stress the financial sector further. Besides, a higher deficit will likely impact the efficacy of the monetary policy, which is the other policy instrument that the market expects the government to use to counter slow growth.

The government is tasked with achieving fiscal consolidation and propelling growth by a counter-cyclical fiscal policy—clearly, this is a tough balancing act.

So, what is the policy response?

In its June meeting, the monetary policy committee (MPC) of the Reserve Bank of India (RBI) cut policy rates for the third straight time by 25 bps and changed its stance from “neutral” to “accommodative.” With the headline inflation trajectory remaining below MPC’s target, there is a scope to pencil in further monetary policy easing in the future to “accommodate growth concerns by supporting efforts to boost aggregate demand, and in particular, reinvigorate private investment activity, while remaining consistent with its flexible inflation-targeting mandate.”4

That said, in the coming months, monsoon will play a crucial role in calibrating monetary policy. This year’s monsoon is predicted to be lower than average, which will likely have implications for both inflation and growth. Besides, if global uncertainties (such as the global trade crisis) intensify, there could be pressure on the currency and trade balance. The RBI will closely monitor economic conditions and likely undertake corrections and adjustments accordingly. However, it will be a tightrope walk. When viewed dispassionately, in the current economic scenario, India likely needs more than just monetary policy to correct its course. Future policy actions have to be more strategic. The government will have to manage the fiscal account and yet address structural deficiencies with full accountability and transparency as monetary policy cannot alone turn the tide.

Fiscal policy and budget: All eyes are now on the Modi 2.0 era

The government has acknowledged the challenges and already started taking actions. Within a week of swearing-in, the Prime Minister’s Office directed all the government departments to submit by mid-June their action plans for the first 100 days and for the full five years with clearly defined measurable outcomes.5 The Goods and Services Tax (GST) Council met in June to decide on crucial matters on taxation, such as ease registrations and return filings, to simplify GST and improve compliance.6 All these measures indicate that the emphasis is now on delivering on promises and building an accountable system in the administration. In addition, the government wants to tackle the challenge of economic growth and jobs sooner than later—it set up the two new cabinet committees on investment and employment just days after the GDP data release.7

More importantly, all eyes were on the mid-term budget presented on July 5—the first budget of the Modi government’s second term—by India’s first woman full-time finance minister, Nirmala Sitharaman. It was a tightrope walk balancing the need to boost growth, create jobs, and offer tax breaks without straining expenditure. In the backdrop of the finance minister’s mantra of reform, perform, and transform, the budget packed competing goals and a strong commitment to fiscal prudence. The finance minister announced a forward-looking budget that addressed all the pressing issues, be it reviving private and foreign investments and jobs, building infrastructure, fixing farm policies, or promoting ease of living and doing business (see sidebar, “The union budget for FY2020: Is the devil in the detail?”). All this while setting a fiscal deficit target of 3.3 percent for FY2020, 0.1 percentage point lower than what was targeted in the budget presented in February.8

Over the past five years, the government took myriad steps and implemented several groundbreaking reforms, such as implementing the landmark tax reform, allowing foreign investment in restricted sectors, and reforming the bankruptcy law. By presenting a visionary budget with mid- to long-term benefits, the finance minister committed to continuity of previous policies. However, the budget lacked details on implementation, and all eyes will now be on the specific steps the government takes to execute its proposals.

The union budget for FY2020: Is the devil in the detail?

The budget focused on reviving investments and the rural economy as well as improving the financial structure to spur credit and spending growth.9

- To boost investment, the finance minister proposed reducing the corporate tax rate to 25 percent for companies with an annual turnover up to INR 400 crore (or INR 4 billion; accounting for 99.3 percent of total companies). Earlier, companies with annual turnover up to INR 250 crore were entitled to a lower rate of 25 percent; for the others, it was a higher variable rate. Some of the measures to attract foreign capital into the domestic market include increasing the foreign direct investment (FDI) limit in insurance intermediaries to 100 percent; easing local sourcing norms for FDI in the single-brand retail sector; increasing statutory investment limits for foreign portfolio investment; and providing nonresident Indians a seamless access to Indian equities. Thrust to affordable housing and concessions to boost production of electric vehicles were the other moves to help investment in the housing sector and green technology.

- In a bid to strengthen the rural economy and jobs, the budget proposed several measures. These include expanding financial support to and a new pension scheme for farmers, providing relief for small taxpayers (tax rate cut from 10 percent to 5 percent for individuals with an annual income of INR 250,000 to 500,000), developing skills in agro-rural industries, and expanding solid waste management efforts.

- To revamp the financial and banking sector, the budget proposed INR 70,000 crore (INR 700 billion) for bank recapitalization. It also recommended greater regulatory authority to the RBI over the housing financial sector and nonbank financial companies (NBFCs), which are the biggest sources for credit creation in rural India. In addition to the government giving partial credit guarantees to public sector banks, the budget offers certain measures specifically for the NBFCs to ensure they get funding from banks and mutual funds.

Sitharaman addressed concerns related to job creation by giving small and medium enterprises (SMEs)—the biggest source of employment generation and grappling with a lack of access to funds and thereby growth—access to social security, quick loans, and an efficient payment platform to avoid payment delays. Taking up labor reform, the finance minister announced the government’s plan to streamline multiple labor laws into a set of four labor codes, which are expected to boost investment in and job creation by SMEs.

To promote self-employment and skills, the finance minister emphasized women’s participation in the economy and offered concessions to startups to encourage entrepreneurship. For job creation on a sustainable basis, she stressed on improving education (through introducing a new education policy, transforming higher education, and creating funds to promote research), skills among the youth (through encouraging the youth to undertake programs on artificial intelligence, big data, robotics, etc.), and popularizing sports.

In the making of New India, infrastructure development was given top priority. The finance minister announced an investment of INR 100 lakh crore (INR 100 trillion) over the next five years, with the focus on improving the railway, building local infrastructure for water sustainability, and bridging critical infrastructure gaps in the agriculture sector, among others. At the same time, Sitharaman committed to restricting the fiscal deficit through improved revenue generation. Although it sounds ambitious, the finance minister announced a higher disinvestment target to finance spending. No changes were proposed in personal income tax rates, but additional surcharges were levied on the superrich.

Focus was also on improving the “ease of living” for the middle class, through announcements such as cheaper digital payments, ATM-like One Nation One Card for pan-India travel, new model rental laws, deductions on interest payments for purchase of affordable houses and electric vehicles, and pensions for workers in the informal sector.

However, the market seemed apprehensive about the proposal to increase minimum public shareholding to 35 percent from 25 percent. Investors fear that, if implemented, it might reduce liquidity from the stock market due to increased private capital outflow and lead multinational corporations with high promoter stakes to consider delisting. Consequently, the stock market reacted negatively.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Learn more

Get in touch

- Dr. Rumki Majumdar

- Executive manager, Deloitte Research

- Deloitte Service LP

- rmajumdar@deloitte.com

- + 1 470 434 4090

Related

More in Economics

-

Global Weekly Economic Update Article4 days ago

Global Weekly Economic Update Article4 days ago -

United States Economic Forecast Q1 2024 Article1 month ago

United States Economic Forecast Q1 2024 Article1 month ago -

Economics: Asia Pacific Collection

Economics: Asia Pacific Collection -

Economics: Americas Collection

Economics: Americas Collection -

-

Japan economic outlook, April 2024 Article2 days ago

Japan economic outlook, April 2024 Article2 days ago