South Africa Charting a difficult road to recovery

8 minute read

18 November 2020

With coordinated and proactive programmes, South Africa can script a recovery and revive the economy.

Over the past few years, South Africa’s ongoing struggle with weak growth, rising unemployment, negative GDP per capita growth, and mounting public debt has been no secret. Before the COVID-19 pandemic struck, real GDP growth forecasts to 2022 were near 1%, due to, inter alia, persisting structural challenges and ongoing electricity supply woes.1 Recessionary pressures were acute. In fact, in March 2020, Statistics South Africa (Stats SA) lowered the annual GDP growth rate estimate to only 0.2% for 2019, sending the economy in a technical recession, given two consecutive quarters of negative growth during the end of that year.2

Learn More

Explore the Economics collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

COVID-19 pushes South Africa deeper into recession

COVID-19 has changed the already-challenging economic outlook for the worse, while further exposing deep structural divides in the economy. South Africa has had some of the world’s strictest lockdown restrictions in place since the end of March 2020, as the country prioritised its response to the health crisis by aiming to save as many lives as possible.

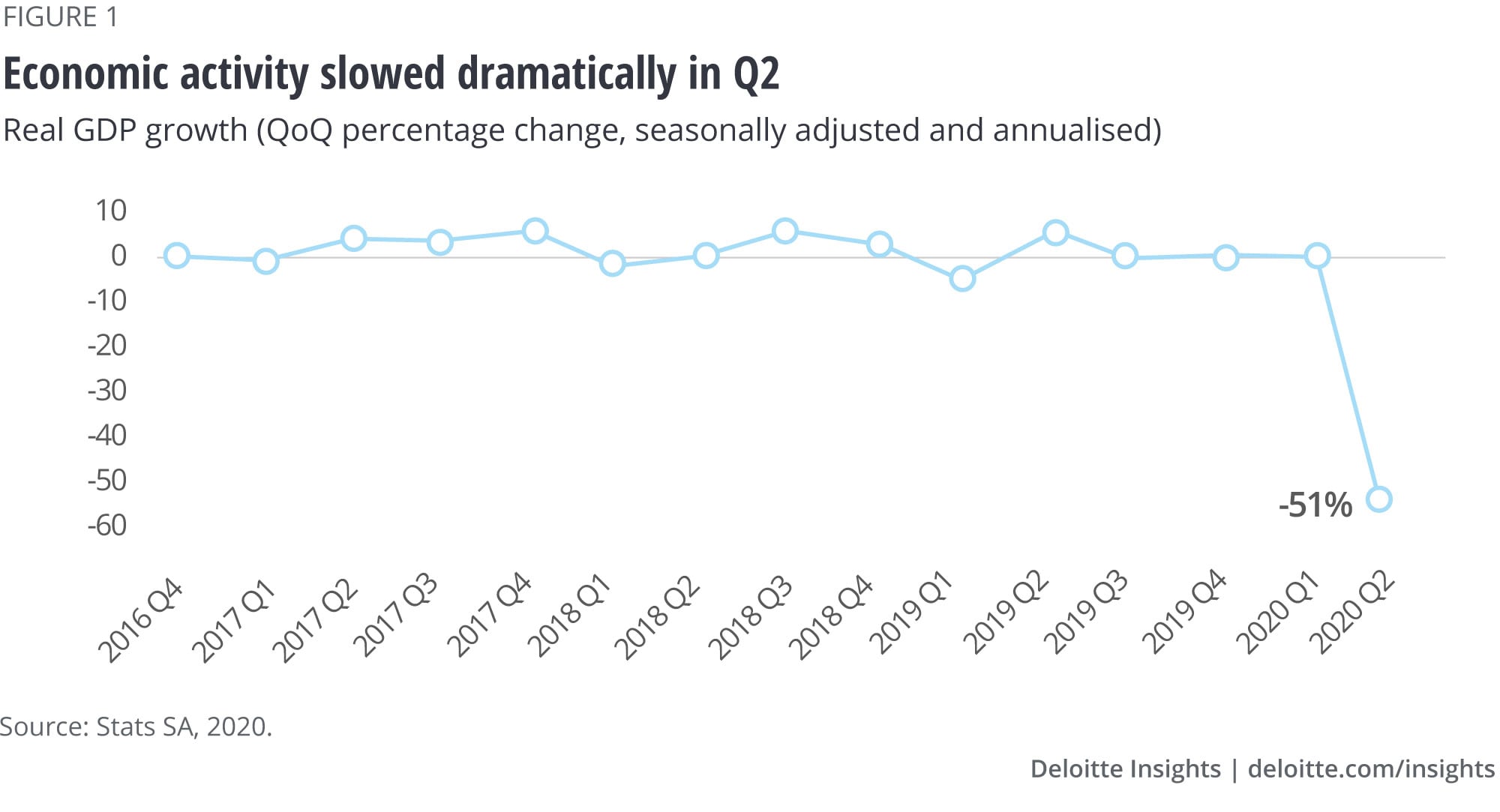

This prioritisation saw South Africa face an almost unique situation in its history—economic activity faced a systemwide shock from both supply and demand sides. Economic activity came to a complete halt for a number of weeks in the second quarter across many sectors, playing out dramatically in the economic data: Real GDP dropped by 51% quarter-on-quarter (seasonally adjusted and annualised) in Q2 of 2020 (or –17.2% in nonannualised year-on-year terms), after a 1.8% quarter-on-quarter (seasonally adjusted and annualised) contraction in Q1 (figure 1).3

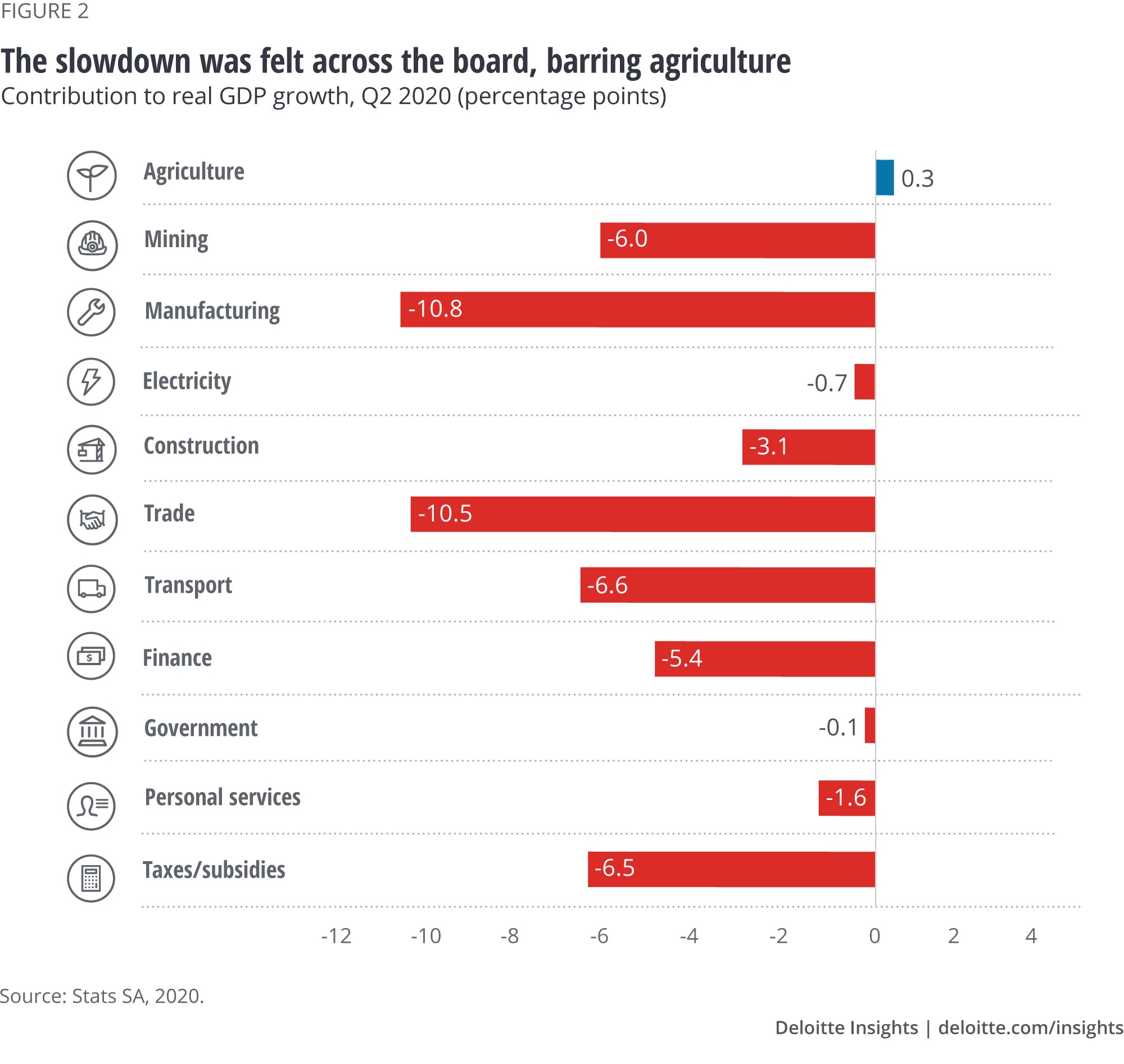

The economywide slowdown was most felt in the manufacturing sector—it contracted 74.9% quarter-on-quarter (seasonally adjusted and annualised) and had the largest contribution (-10.8 percentage points) to the overall slowdown. The second-largest contribution stemmed from the trade and accommodation sector, which contracted by 67.6% quarter-on-quarter (seasonally adjusted and annualised). In the third place was the transport sector that contracted by 67.9% quarter-on-quarter (seasonally adjusted and annualised) (figure 2).

The agricultural sector was the only one that posted growth, albeit marginal.4

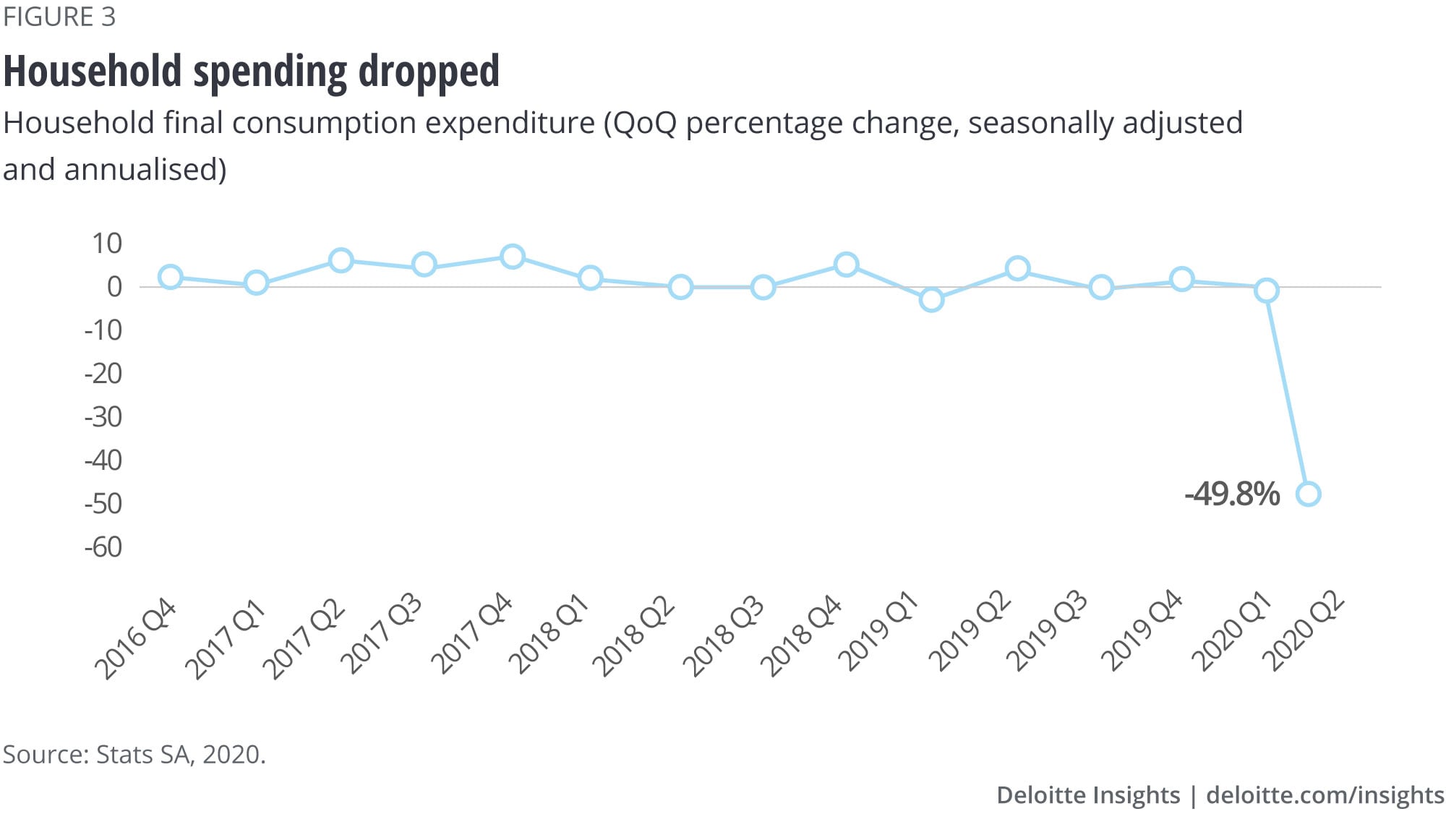

Household spending saw a similar slump given curfews and limitations on movement; lockdown restrictions on retail, leisure, and travel sectors; and resultant worker layoffs (figure 3). The biggest spending knocks were seen in semidurable and durable goods. Work-from-home policies (in sectors where working from home was viable) saw households increasing expenditure on utilities and communication services.5

Job losses accelerated sharply

The pandemic and the subsequent economic lockdown have had a devastating effect on employment. South Africa’s unemployment rate (narrow definition) increased to a record high of 30.8% in Q3 2020, after a record total 2.2 million jobs lost between April and June 2020. The largest job losses recorded in a single quarter before this was in Q3 2009 (527,000 job losses), in the wake of the global financial crisis.6

While consumers regained some confidence in Q3 2020 as parts of the economy opened up for business, consumer confidence remained in negative territory, moving from –33 points in Q2 to –23 points in Q3.7

This still-weak confidence also reflected in the October 2020 survey of the Deloitte State of the Consumer Tracker, indicating that South African consumers still have a number of financial concerns—38% are concerned about making upcoming payments, 51% are delaying large purchases, and 53% are worried about losing their job.8

A recovery in consumer confidence and household incomes to levels seen prior to the COVID-19 pandemic is likely to take some time, possibly extending to a number of years.9

Some green shoots are emerging

Nonetheless, there are a number of green shoots sprouting across the bleak economic landscape. The latest data from Stats SA shows that mining production increased by 40.6% (quarter-on-quarter, seasonally adjusted) in Q3 2020,10 while manufacturing production climbed by 32.9% (quarter-on-quarter, seasonally adjusted).11

Encouragingly, seasonally adjusted retail trade sales increased by 4% in August 2020 compared with July 2020, while the latest Purchasing Managers’ Index data from the Bureau of Economic Research increased to 60.9 index points in October, compared to a revised 58.5 index points in the preceding month.12

Another indicator showcasing a rebound is an uptick in vehicle sales, with seasonally adjusted motor trade sales increasing by 6.4% in August 2020 compared with July 2020.13 These increases are encouraging signs going into the tail end of the year, following the record contraction a few months earlier.

Medium-term growth outlook

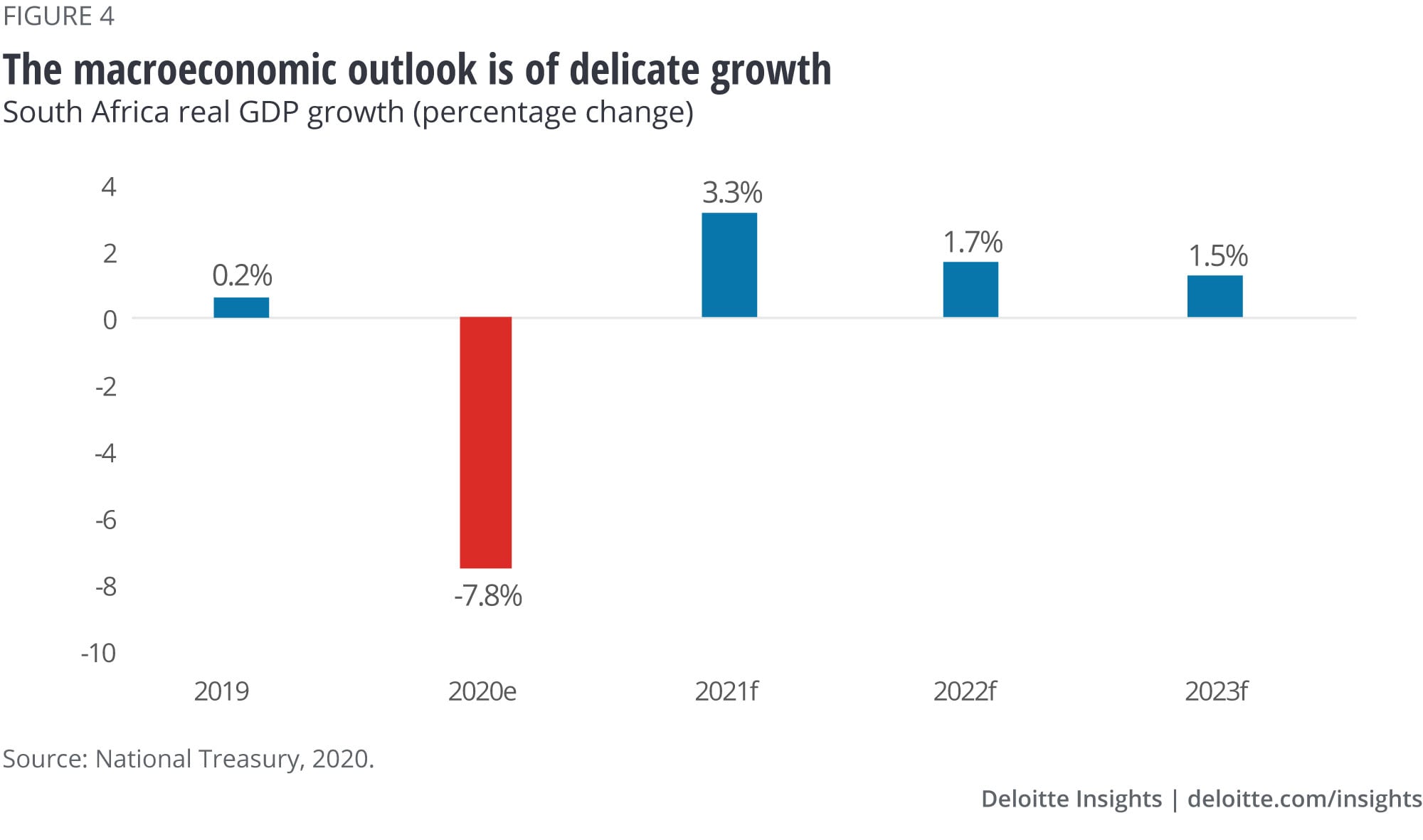

Despite this, there are various estimates of the economic fallout for 2020, ranging from real GDP growth of –7.8% (National Treasury),14 and –8.2% (South African Reserve Bank)15 to –11.5% (OECD).16

Given the magnitude of the expected contraction in an already-weak economy, the need for concerted action to transition onto a path of economic recovery has become even more urgent. Policy tools, such as the emergency fiscal stimulus and an easier monetary policy stance, are likely to only cushion some of the worst impacts.

In response to the rising number of unemployed and discouraged workers, the COVID-19–driven economic contraction, limited fiscal space, and South Africa’s rising debt service bill, the National Treasury proposed in its medium-term budget policy statement (MTBPS) a number of options to stimulate GDP expansion and return the country to a path of growth over the next few years. Part of the plan includes:17

- A five-year fiscal consolidation path that promotes growth and reigns in debt (expected to peak at 94.6% as a share of GDP in the 2025–26 fiscal year)

- Reforming the electricity sector by allowing for the procurement of independent power sources, unbundling of power utility Eskom into separate business units, and allowing municipalities to buy electricity from different sources

- Supporting investment in infrastructure that will stimulate a shift to investment-led growth, while making it easier for pension funds to invest in infrastructure projects

- Easing regulations and improving the overall ease of doing business

As such, macroeconomic projections to 2023 forecast a rebound in 2021 from the sharp contraction in 2020, with growth moderating thereafter, rather than a recovery (figure 4).18

But with limited fiscal space …

With a fast-expanding debt-to-GDP ratio, the government has limited fiscal space because of which it is unable to take the country out of its economic predicament via spending. As such, the biggest priority outlined in the National Treasury’s MTBPS is the urgent need to maintain fiscal consolidation, while enacting immediate pro-growth reforms. Funding is expected to come from a rising borrowing component, as well as the reprioritisation of spending from other departments.

Despite the reduction in expenditure, the focus is on moving from consumption-led growth (a feature of the economy following the impact of the global financial crisis) toward investment-led, and particularly private investment-led, growth. The cornerstone of this initiative is the infrastructure fund that is designed to crowd in private-sector finance. Investment by the government and public corporations has shown negative real growth for three of the past four years.19

While this supports the government’s mid-October 2020-released economic reconstruction and recovery plan20—which focuses on job creation primarily through infrastructure investment, reindustrialisation of the economy, speeding up economic reforms to unlock investment and growth, combating crime and corruption, and creating a capable state—it is likely to face a number of challenges.

The biggest challenge remains the government’s rising debt. As finance minister Tito Mboweni noted in his MTBPS, South Africa spends ZAR2.1 billion per day on borrowing costs—the fastest-growing expenditure item in the medium term.21 The ability to reign in debt has been further hindered by an expected sharp contraction in tax revenue as a result of the COVID-19 pandemic. Furthermore, it has been flagged for a number of years that South Africa has limited to no room to raise taxes to bring in additional tax revenue, given that the country is likely to have already reached the top of the Laffer Curve.22

The risk South Africa thus finds itself in is that if spending is not disciplined enough, it is inevitable that the country will be forced into a debt trap and will need to turn to international financial institutions for aid. In this scenario, austerity-enforced GDP growth is likely to remain under pressure in the next five years.

Furthermore, the proposed budget adjustments require a drastic slowdown in public-sector wage growth. This could have several ramifications down the road. First, this is likely to be met with strong opposition from the public sector and may result in resistance from unions. Second, the slowing in wage growth is likely to depress household consumption and demand from the public sector, further adding to already-depressed private-sector consumption over the next three years (which could be substantial, given that the public-sector accounts for around 30% of earnings across industries).23

Finally, the reduction in spending across departments may adversely affect economic growth and welfare of the population over time. Indeed, COVID-19 has thrown South Africa’s decades-long struggle with poverty and inequality into even sharper spotlight, with poorer households arguably the most severely affected by the consequences of the pandemic.

… all eyes are on urgent reforms

The need for economic reforms is now more urgent than ever before. While it has been difficult to do until now, this might be the opportunity for South Africa to strictly focus on pro-growth reforms that will unlock a new growth path over the medium term, one that is inclusive and more sustainable, but also more competitive and resilient, and raises economic expansion above the meagre figures that the country has experienced in the years leading up to the pandemic.

Vital focus areas, which will require consolidated efforts from both government and the private sector, include increased spending on infrastructure investment, reducing wasteful expenditure and corruption, unlocking efficiencies and opportunities presented by the digital economy, as well as a focus on implementation.

In short, South Africa faces a difficult road to recovery. Scripting this recovery is likely to only be in the realm of possibility if all stakeholders come together to drive a coordinated and proactive programme to respond to the social, economic, and health impact of COVID-19 and jointly rebuild the economy.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network's industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte's top management and partners abreast of topical issues.

Get in touch

- Hannah Marais

- Associate director | Africa Insights

- Clients & Industries | Deloitte Africa

- hmarais@deloitte.co.za

- +27 11 304 5463

More from the Economics collection

-

State of the US Consumer: March 2024 Article3 weeks ago

State of the US Consumer: March 2024 Article3 weeks ago -

Brazil economic outlook, February 2024 Article1 month ago

Brazil economic outlook, February 2024 Article1 month ago -

-

-

G7 economies Article3 years ago

G7 economies Article3 years ago