{kind=link}

{kind=link}

{kind=link}

The curious case of the labor market recovery has been saved

Cover image by: Jaime Austin

The reaction of labor markets to the economic recession and recovery brought on by COVID-19 has been nothing short of odd.

Prior to the pandemic, the United States had never experienced such a swift onset of a recession, with a precipitous drop in GDP and employment. Some 22 million jobs were lost between February and April 2020. While it’s expected for employment to fall during recessions,1 during the two-month COVID-19 recession, even as the number of unemployed swelled from 6 million to 23 million, an additional 8 million people left the labor force. We do not usually experience such a large decline in the labor force during recessions. However, given the nature of the COVID-19–led recession and the health, safety, and caregiving challenges it presented, it is not surprising that many did drop out.

Another notable difference compared to prior downturns is the speed of the economic turnaround. It took three years for GDP to regain its prerecession level following the global financial crisis of 2008–09, while the post–COVID-19 recovery regained its prepandemic level of GDP in just a year and a half. Even more remarkable was how fast the demand for labor returned. Job growth started almost immediately after the recession trough (April 2020). This recovery is the opposite of the “jobless recoveries” that have been the norm in the last few business cycles. Even so, employment seems to be growing relatively slowly—but job openings are at an all-time high. The big question is how willing and able are those currently unemployed or out of the labor force to return to work. We look to some detailed industry data for possible explanations.

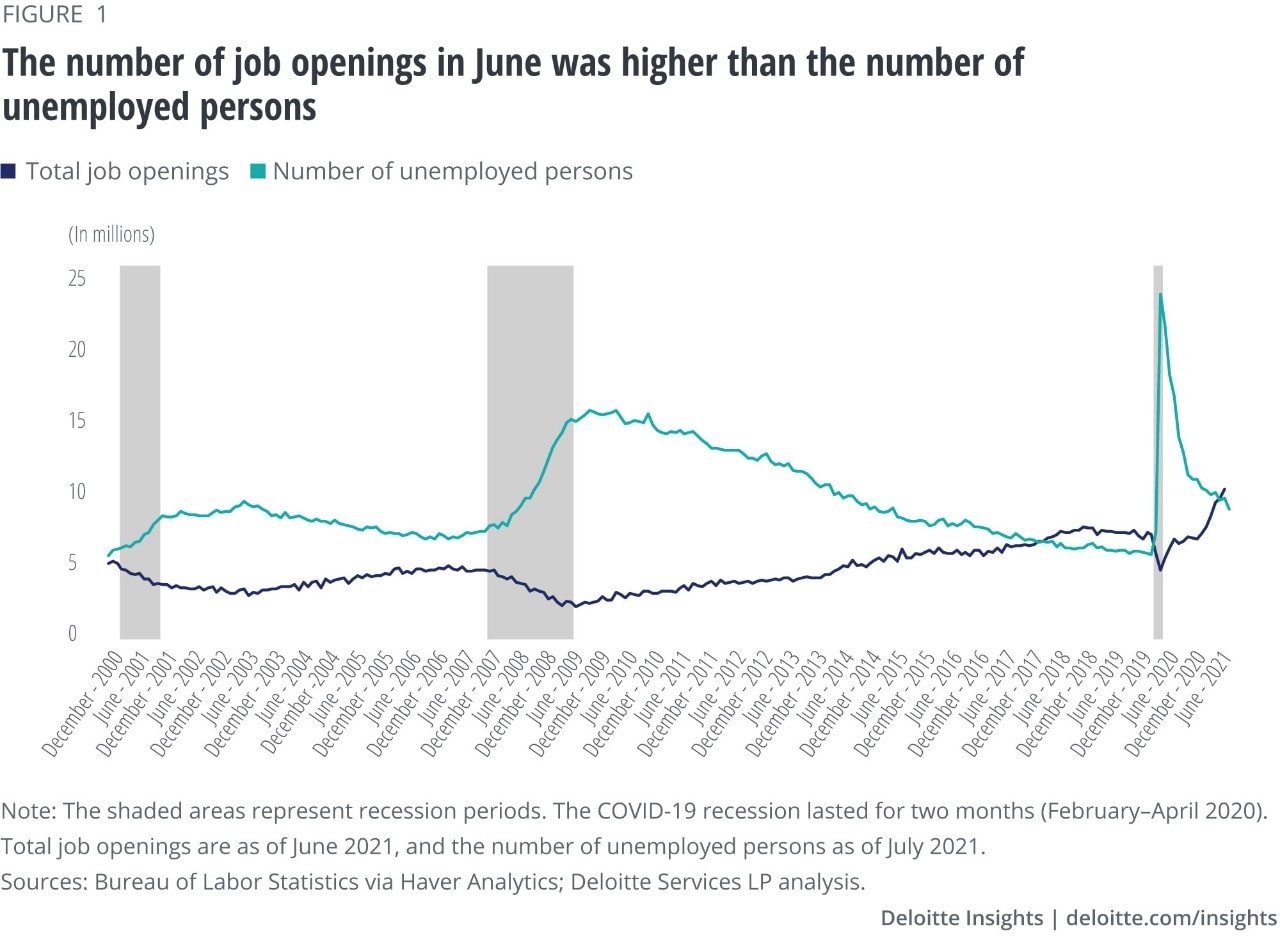

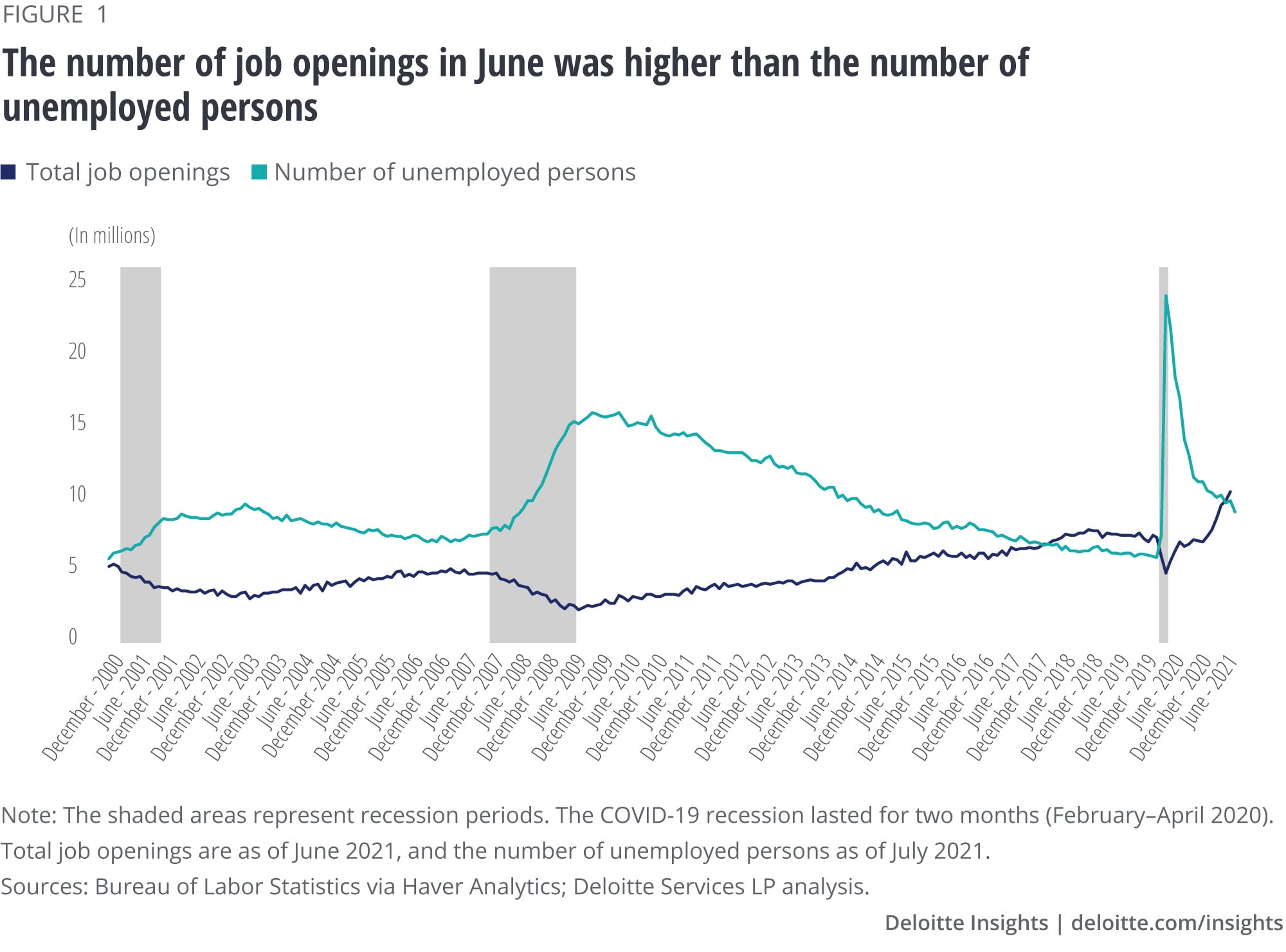

The unique nature of labor market dynamics during the COVID-19 recession and recovery is shown in figure 1. In the two prior recessions (recessions are denoted by gray bars), the number of unemployed people continued to rise even after the recessions officially ended, and job openings were slow to pick up. In the two years prior to the pandemic, the labor market was particularly tight, with less than one unemployed person per job opening. Somewhat surprisingly, the May Job Openings and Labor Turnover Survey (JOLTS) report from the Bureau of Labor Statistics (BLS) found that the ratio of unemployed persons to job openings was almost back to the prepandemic level, with job openings and the number of unemployed about equal. However, this does not mean that the labor market has recovered, as the record number of job openings in June (10 million) was higher than the number of unemployed. Yet, before the pandemic, the unemployment rate was 3.5%; it is currently 5.4%—a substantial improvement over the 14.8% recorded in April 2020, but still high.

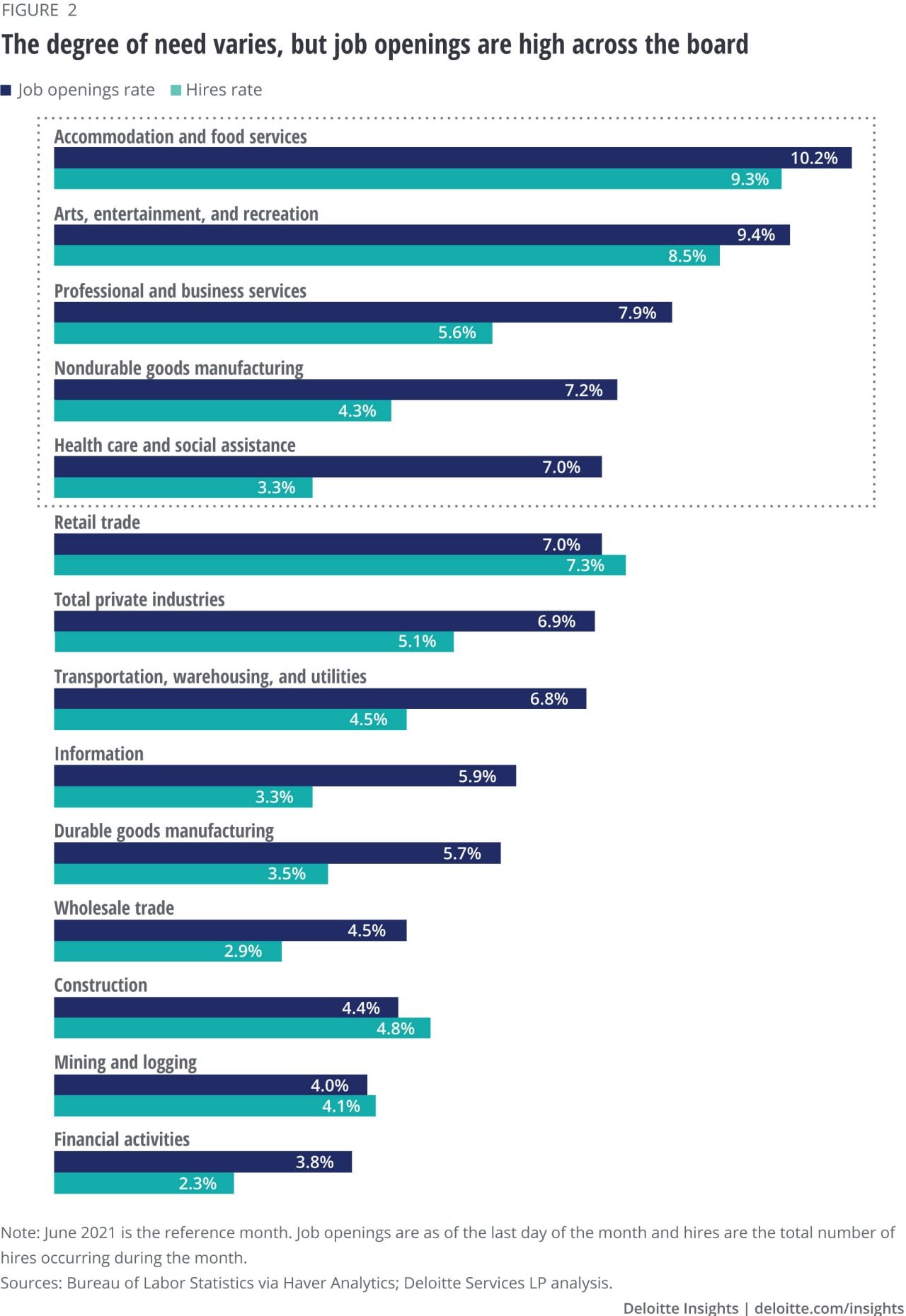

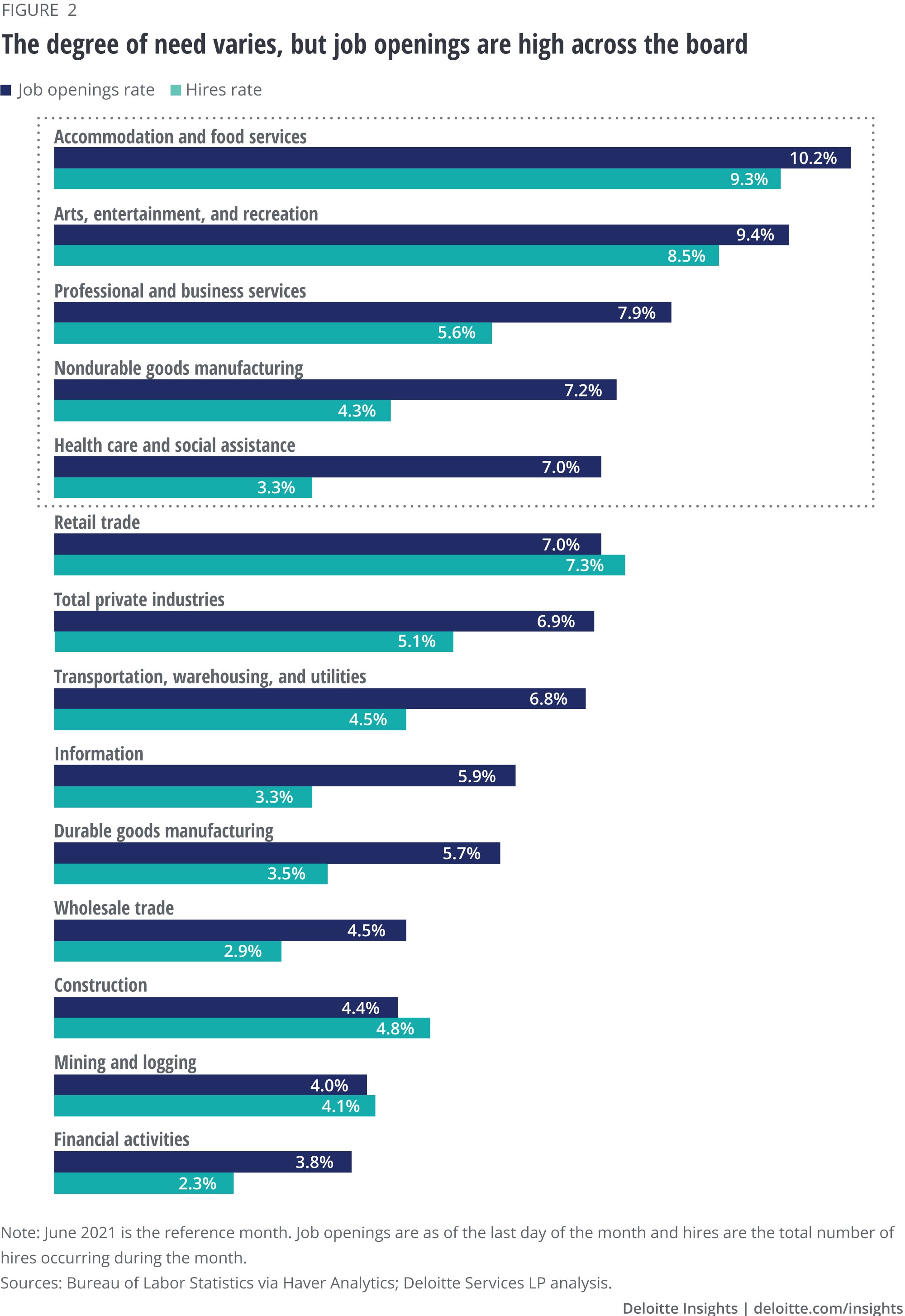

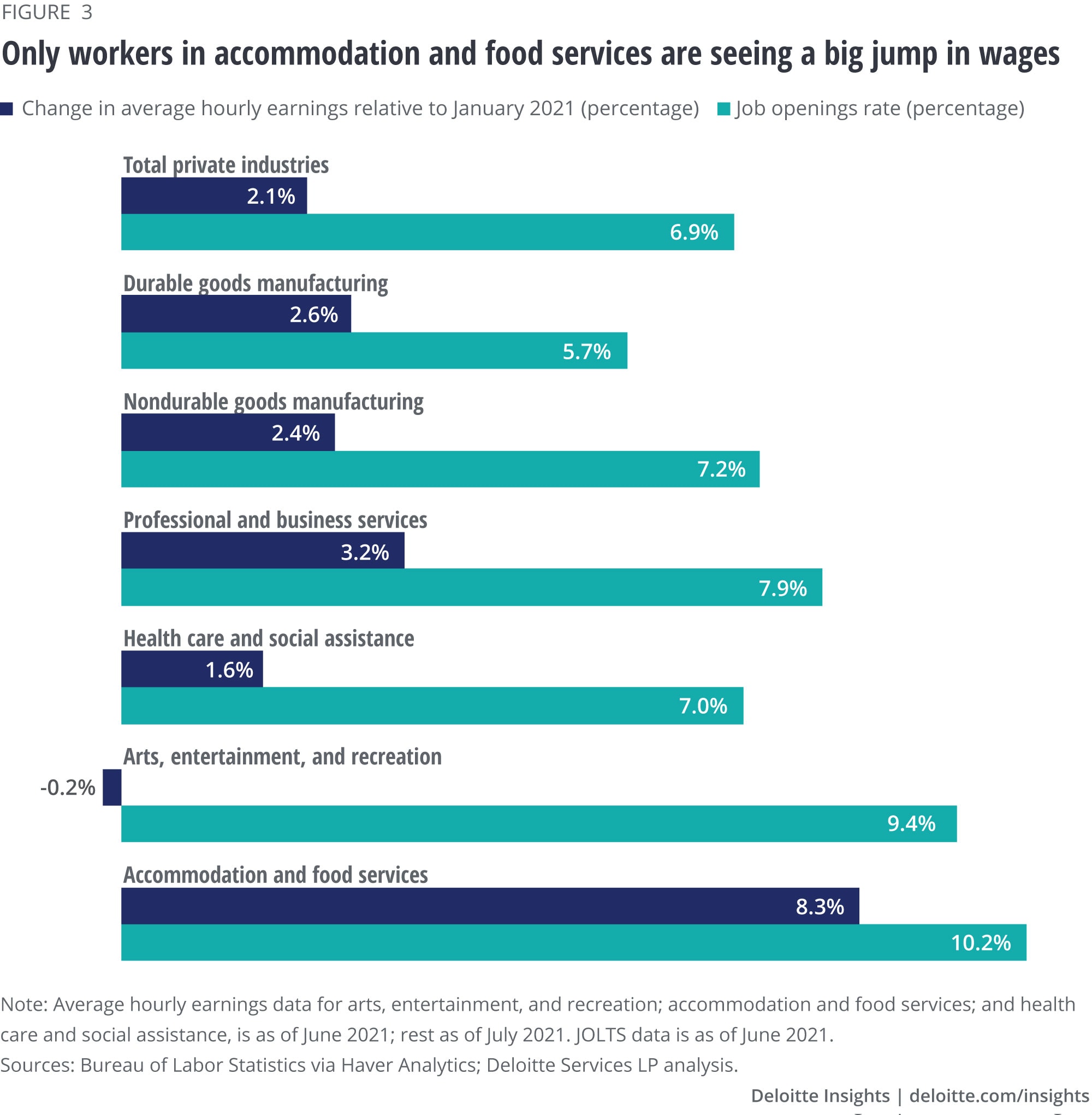

The large spike in the job openings rate (share of jobs available and unfilled) has not been uniform across industries. For example, job openings in mining and logging, construction, information, financial activities, and educational services are at rates similar to those prior to the pandemic. And in industries such as retail and transportation, warehousing, and utilities, the job opening rates—while currently high—are not in record territory. However, in the remaining industries (those boxed in figure 2), the current job openings rates are substantially above their prior norm. Accommodation and food services and arts, entertainment, and recreation not only have the highest job opening rates, but their hire rates (the number of hires as a share of total employment) are even higher. This is not surprising given how fast these industries shed jobs early in the pandemic and how quickly business leaders in those industries wish to return to “normal” levels.

Given the high rate of job openings, are employers trying to lure new employees with higher wages? Despite lots of stories in the press, the answer is oddly—not particularly. While many of the industries with a higher-than-average job openings rate have seen above-average increases in wages since January, only accommodation and food service employers are paying, on average, significantly higher wages than before the pandemic. Therefore, even though we are hearing anecdotal reports of large signing bonuses and wage increases for employees in certain specialties, these specific wage hikes have not translated into large rises in the aggregate.

Wages are not the only factor that may be affecting potential employees’ willingness to take those open jobs. Many employees and potential employees are emerging from the pandemic with a different set of priorities. Two key areas that may be having an impact on the labor market are:

What does all this mean to employers? To meet their employment needs, firms will need to search outside of their usual recruiting pools to include diversity of all types in the candidates—race, gender, sexual orientation, age—and modify their interview strategies so that candidates are not excluded early in the process by background factors, such as extended absence from the workforce. Assuming that prepandemic employment processes will serve in the postpandemic world is a recipe for continuing recruiting problems. And according to our earlier research,5 about half of the decline in the labor force is due to workers aged 55+ years retiring. This group, in particular, might be persuaded to rejoin the workforce—but employers can’t assume it will happen automatically. More accommodations and benefits tailored to these older workers may be required to entice them back to the job market.

It’s true that the upcoming expiration of enhanced unemployment benefits might be sufficient to cause some workers on the sidelines to return to some jobs. But employers might not want to count on this, given the lack of evidence from the 26 states that have withdrawn from federal unemployment programs.

Cover image by: Jaime Austin