Hospitality sector focused on ramping up operations and planning for growth has been saved

Analysis

Hospitality sector focused on ramping up operations and planning for growth

Ahead of the UK reducing its pandemic related restrictions on 19th July, we asked European hospitality leaders about their expectations and priorities for the preceding weeks and months. The Hotel Sentiment Survey shows that while hospitality businesses expect the pandemic to continue to cause disruption, they are gradually shifting away from ‘downturn market behaviours’ and focused on ramping up operations and planning for future growth.

As COVID-19 cases continue to rise in many European countries, 56% of hospitality leaders expect pandemic related disruption to last at least until 2022 and a further 38% to 2023 and beyond.

Length of the disruption to the hospitality sector

Recovery is also expected to take some time. Most leaders (62%) now believe that performance will not return to pre COVID-19 levels until 2023, up from 52% in March 2021, and a further 36% expect that it will happen sometime in 2024 or later.

When asked about the near future, most hospitality leaders (46%) in our survey still cite cash flow management as the top priority going into August. However, hiring and re-staffing has emerged as the second most important area to focus on with 42% of respondents citing this. They expect they can best attract skilled staff into the sector by raising pay and offering flexible contracts. However, how well this can be balanced with the continued focus on cash flow management remains to be seen.

Strategic growth initiatives are now the third highest priority, with the share of respondents stating this up by 7 percentage points from March 2021. Similarly, more respondents (up by 5 points) are now focused on resolving challenges around their supply chain while fewer look to prioritise managing stakeholder relationships (down 11 points) and streamlining operations (down 14 points).

Key priorities for the next four weeks

The hospitality sector expects demand in the short term to come largely from leisure travel. As consumers finally have more options for holidays, independent leisure travellers and staycations are expected to be fuelling demand in the coming weeks.

Financing and transactions

In terms of financing, hospitality businesses are increasingly planning to move away from options that are more typical in a downturn. Now only 24% are considering reorganisation or restructuring, down 14 points from March 2021, while the share of those saying they are planning to modify loan terms or defer payments is down 9 points compared with three months ago. Instead, more organisations are looking at refinancing and consolidating existing debts (up by 7 points) and partnerships (up by 1 point).

Financing options considered

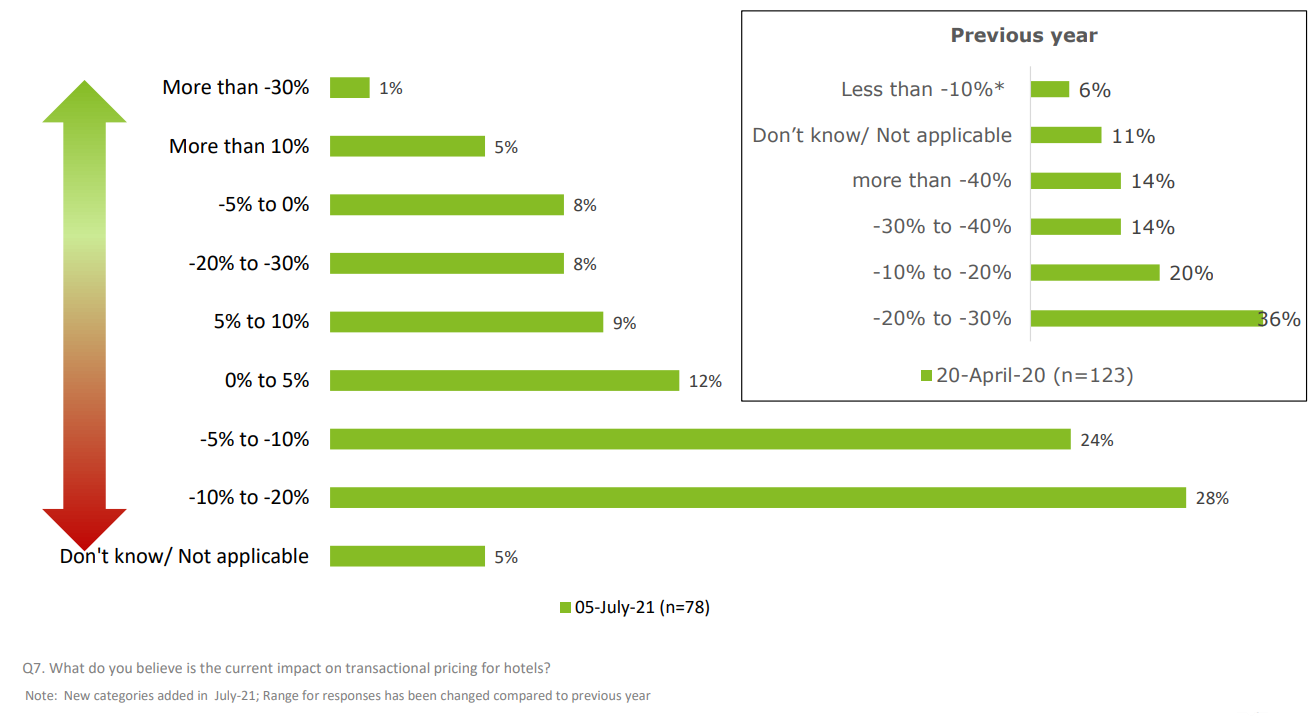

The respondents expect distress activity to continue to originate mainly from the UK, Spain and Italy, echoing the findings of our March 2021 survey. When asked about transaction prices, the views on the impact the pandemic are somewhat diverging. Over a quarter (26%) of our survey respondents believe pricing is up while 28% believe that current hotel values are down by 10-20% as a result of the pandemic.

Impact of the pandemic on transaction pricing

The coming months will be still a challenging time for the hospitality sector across Europe but it certainly seems that the leaders in our survey are committed to serving its customers again and look forward to a more promising future.

For more details on the Hotel Sentiment Survey results and insights, you can access our Hospitality pages.