Contentious matters in the Energy and Resources sector: A subjective price has been saved

Article

Contentious matters in the Energy and Resources sector: A subjective price

When considering their asset portfolio, energy and mining companies may be rethinking their approach to coal and questioning whether to invest or disinvest. Lacklustre global demand for the commodity amid a continuing volatile global economy may mean a sustained decline in future coal prices. The economic impact on prices and the period over which this will be felt is a question for debate.

The authoritative statement on demand scenarios

A global decline in the usage of coal is expected by the IEA, (the International Energy Agency, an autonomous and authoritative source of data and analysis). While the anticipated rebound in coal demand in 2021, as a result of economic recovery from the coronavirus pandemic, is not predicted to be sustainable, it is unlikely that coal demand will decline in the immediate future. A flat or declining outlook is forecast thereafter. Demand from developing Asia is set to hold or grow in the near term. However, it is yet to be determined if any increase in demand from Asian countries is enough to offset declining demand elsewhere.

Beyond 2021, growth in coal prices is thought to be slow or declining. However, most parties have predicted alternative scenarios. For example, the IMF has put forward a situation where prices could increase to more favourable levels in 2021 and follow a slow-growth trajectory from 2021 into 2023. The future of coal remains the subject of debate.

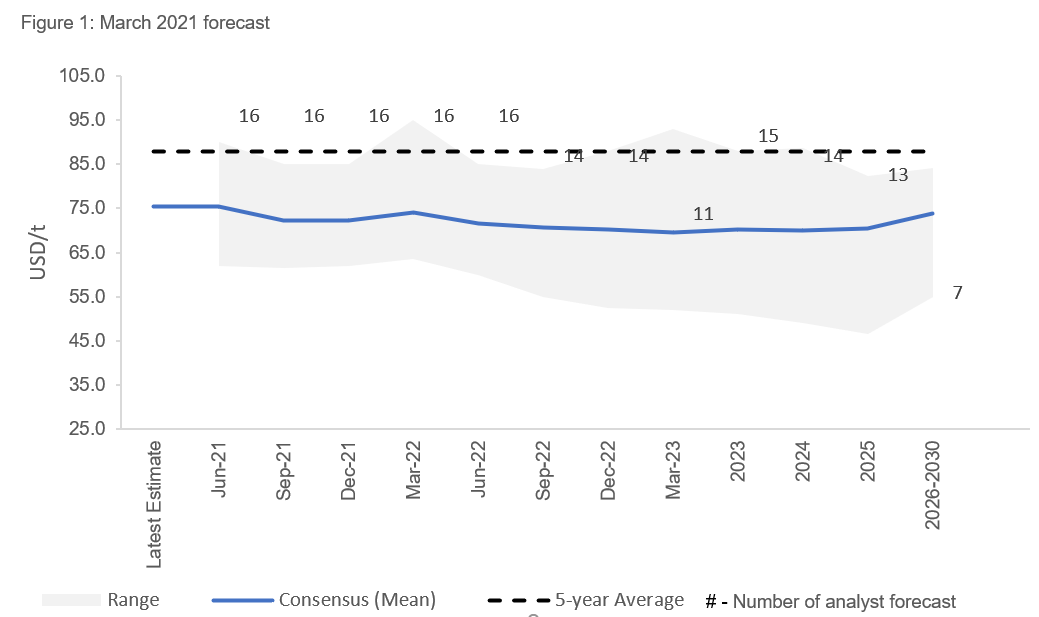

Consensus Forecasts

Analysts’ expectations of the coal price outlook diverge greatly and a lack of transparency in forecasting methodologies adds to the cloud of uncertainty hanging over the market. Benchmark prices, used to guide estimates for alternate thermal coal products, should be compared with scepticism as the price difference expected between traded products has historically exhibited volatility.

In monthly Energy and Metals Consensus Forecasts’ surveys conducted by Consensus Economics1, it can generally be observed that far fewer participants provide long term forecasts, suggesting a reluctance to provide extended forecasts. In addition, certain analysts are prepared to suggest a more optimistic outlook, whereas others maintain a conservative viewpoint, with a declining outlook. It is difficult to determine any trend or success in forecasting, with outliers among brokers. Forecasts put forward by the banking and analyst community for thermal coal suggest a delayed recovery scenario or wide-ranging recovery in thermal coal price indices from 2020 in the near term. Despite a continuation in the diverse range in estimates put forward by a cohort of 15 groups, broker consensus is that the medium-term price outlook (2022-2025) is declining. This continues into the long-term forecasts, but with a wide range.

Consensus forecasts suggest some medium-term stability among analysts for thermal coal prices (~USD 75/t), however, prices are thought to remain lower than a historical 5-year average price (USD 87.81/t).

Even with the current recovery of the thermal coal price, due to the anticipated recovery of the global economy, broker forecasts present a generally muted view of the coal market, with varied divergence from the consensus or mean values in the medium and long term. This uncertain outlook is likely driven by global pressures to switch to cleaner sources of energy, among other factors. A shift, from a flat to a declining outlook, has been observed between the March and June forecasts (See Figure 1 and 2 respectively). This shift could be attributed to the growing amount of uncertainty around coal consumption, exacerbated by the rapid decline in consumption in the United States and Europe.

Source: Consensus Economics, Energy & Metals Forecasts, Survey Date: March 15, 2021

Source: Consensus Economics, Energy & Metals Forecasts, Survey Date: June 21, 2021

Moves by the mining community

It is considered that the coal trade is complex and regional supplies are often diverted for undefined periods for geopolitical reasons, to meet growing demand. This is evidenced by China’s imports of non-Australian thermal coal and the resultant positive impact on prices in the last quarter of 2020. However, the impact on price was relatively short-lived.

With a gradual decline in available assets and productivity cuts, coal prices may still increase. The gradual decline in demand will likely be matched by slowing output, due to limited capital available to fund mine extensions or develop exploration assets to sustain output. This could potentially result in a ‘lower demand: lower supply’ market balance where prices have more support.

The wide range of forecasts and variety of scenarios in coal demand and pricing adds an increasing volatility, uncertainty and subjectivity to the coal market. It also adds a level of risk to new market participants bargaining on the remaining life of assets, potentially placing greater reliance on decisions made by the major miners. Maintaining a close eye on price estimates and drivers, such as economic recovery and future energy demand, is critical to not only ensuring a fair product price in the market, but a fair valuation of its remaining assets.

1 Consensus Economics, established since 1989, is the world’s leading macroeconomic survey firm, polling over 700 economists each month for their forecasts and views. Visit https://www.consensuseconomics.com/what-are-consensus-forecasts/ to find out how Consensus Forecasts are calculated.

Key contacts

Julia Peacocke

Senior techno-economic consultant

Strategy & Business Design

Deloitte Consulting South Africa

Neil Mckenna

Managing Director: Deloitte Technical Mining Advisory – Global Markets