The Paradox of Plenty has been saved

Perspectives

The Paradox of Plenty

Part 4: More Money, More Problems?

What challenges can prevent UK banking technology leaders from achieving impact with their investments?

In our previous articles, we called out evidence of rising budgets and a stronger commitment to transformation change spend by UK banking technology leaders. And yet, against a backdrop of more plentiful resources, a number of these key decision-makers also reported that the bulk of their deployments had been only 'partially successful', delivering just 50-75% of their intended impact. To understand why that may be, we look at the barriers to successful tech deployment.

Figure 1 below shows the factors identified by our survey respondents as the key barriers to delivery for their technology projects. These challenges can be divided into ‘internal’ and ‘external’ issues, which is important since, while a specific institution can do very little to change the trajectory of the macro economy around them, or impact regulation at large, internal issues should, in theory, be far more tractable.

Figure 1: A mix of internal and external factors influence the success of projects.

Within internal factors, we found half of respondents (50%) called out ‘complex internal processes’ as a key problem area, making this the leading internal challenge for banking and capital markets tech decision-makers. This also shares overall joint first place with ‘market conditions’ across the full list. This tracks broader trends in the market, including the growing size of buying committees at many institutions, which budget holders need to manage effectively to get their ideas off the drawing board and into production. In addition, while buying committee members may be IT savvy, they may not necessarily be IT-aligned – including board overseers as well as stakeholders in the lines of business – and so, for this and other reasons, getting things done has perhaps never been more complicated.

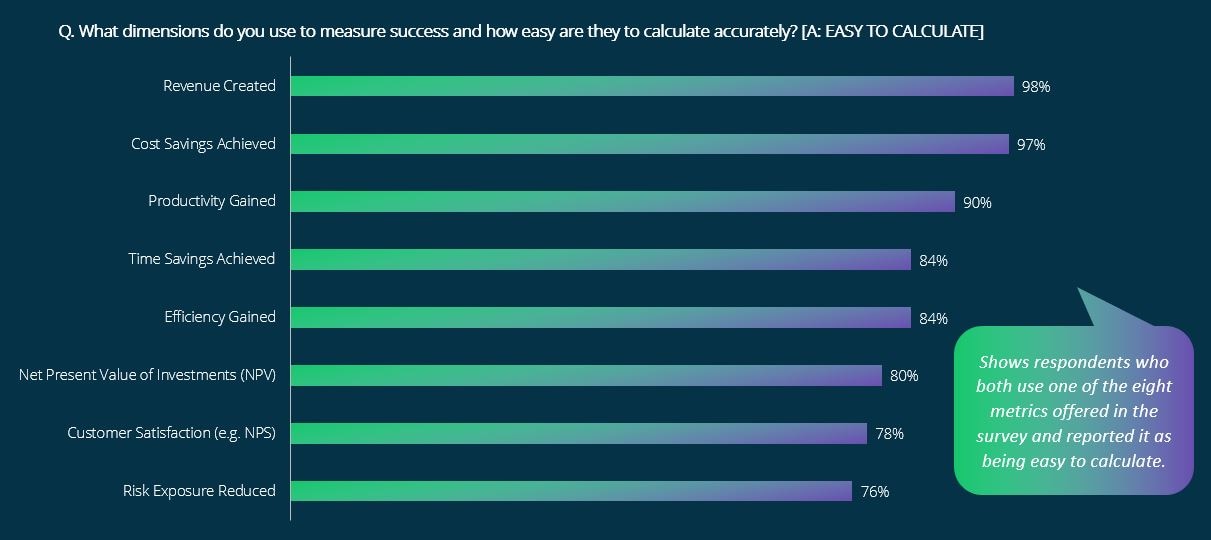

Beyond this, we also have the associated challenge of how decision makers evidence delivery. There are many key performance indicators (KPIs) that firms use to measure the success of their projects and, as Figure 2 below ably demonstrates, firms are making use of a wide variety of metrics. Specifically, here we can see the proportion of respondents who both used any of the eight measures suggested and described them as ‘easy to calculate’.

Figure 2: A wide variety of measures are used by BCM firms to gauge the success of tech projects.

Source: Deloitte UK Banking & Capital Markets Technology Study, 2023

What we see here is surprising since, on the face of it, most decision-makers seem to be finding it easy to measure success in most dimensions. However, this may simply come down to the ways in which certain metrics are designed upfront, with different triggers delivering different levels of anticipated revenue growth, cost reduction or time saved. Importantly though, disregarding the reported ease of calculation for a moment, what’s also striking here is that most respondents were using most of the KPIs offered to them. The variety of measurements being used here makes some sense, particularly given the wide range of value firms are trying to capture. Indeed, recent research conducted by our global Deloitte colleagues identified a taxonomy of 46 digital value KPIs across Financial, Customer, Process, Workforce and Purpose measures1.

Figure 3: A new framework for digital transformation value.

Source: Mapping Digital Transformation Value - Metrics that Matter (Deloitte Center for Integrated Research, 17 Nov 2023)

In the same study, financial services institutions were found to be more confident in their ability to measure success than those in other industries. Nevertheless, confidence does not equal accuracy, and three-quarters of the tech leaders in this study also cited the inability to define exact impacts or metrics as a leading challenge too, just ahead of the difficulty they had in collecting the data required to make their calculations.

As we saw in Figure 1, our own survey found that 46% of respondents cited the difficulty of measuring outcomes as a key internal barrier to delivering success. So, while confidence is a common thread here (i.e., “calculating a KPI is easy”) there may still be a gap between this and the utility of the KPIs used (i.e., “can I use what I’m measuring to actually make my case?”). Indeed, while many of the metrics currently being used by firms may be considered easy to calculate by those doing the calculations, their value in helping banking and capital markets technology decision-makers to communicate and evidence delivery across a wide range of complex projects may be lacking, particularly as those internal complexities continue to grow.

And this matters since, if technology leaders are unable to reach a holistic view of the digital value they create, crucial discussions with key stakeholders around investment ROI could wind up being guesswork. However, there are alternatives, and a structured holistic measurement framework can be helpful in attributing a larger share of firms’ enterprise value to digital transformation. Such measures, we think, could certainly help our respondents achieve better outcomes from their efforts.

So too would addressing their legacy technology issues, which for 44% of respondents were imposing significant constraints on their ability to implement technology change. These legacy issues include outdated and inflexible core banking systems, which hamper operational resilience and make it harder for IT teams to integrate newer systems. In addition, legacy technology can also drive higher maintenance costs. For example, code written in archaic programming languages like the Common Business Orientated Language (COBOL) will need to be translated into modern equivalents like Python owing to its complexity and the relative scarcity of developers fluent in this decades-old programming language. Python offers extensive development libraries and easy operability across a wide range of modern hardware platforms, however translating from one coding language to the other can be a painstaking and time-consuming issue for firms to solve. Similarly, these and other legacy technology issues can also present security vulnerabilities, particularly where older systems can no longer be patched and updated effectively. It should also be noted here that the latest Generative AI solutions running on up-to-date kit can be used to help firms handle their burden of legacy code, further underlining perhaps the value of addressing outdated systems.

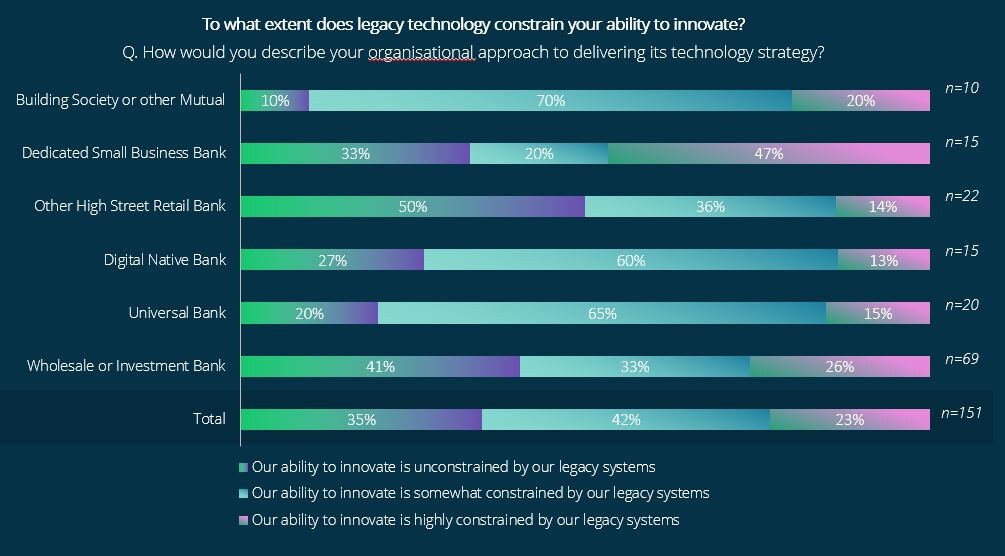

Importantly, legacy technology may not be properly integrated with other organisational systems, which can lead to data silos. This, in turn, can make it much harder for firms to fully utilise their analytics and unify their customer data in a single place, making it much harder to achieve the objective of delivering better customer experiences. And, as Figure 4 below shows, when asked the extent to which legacy technology curtailed their ability to innovate, two-thirds of respondents (65%) reported that it ‘somewhat’ or ‘highly’ constrained their efforts here too.

Figure 4: Two-thirds of respondents claimed legacy tech was constraining their ability to innovate.

Source: Deloitte UK Banking & Capital Markets Technology Study, 2023

As the exhibit shows, building societies (90%) and universal banks (80%) were the most exposed to the drag on innovation caused by outdated legacy technology. Intriguingly though, the third most impacted segment were the Digital Natives, where 73% of respondents called out legacy tech as a drag on innovation. While this may seem counter intuitive, there could be several factors at work behind the scenes driving this.

For a start, the physical technology infrastructure used by these institutions when they first started out may not be capable of scaling efficiently with them as they grow. The need, for example, to constantly update and maintain older infrastructure as new customers are acquired could certainly result in legacy technology issues down the line. This so-called ‘technical debt’ can also extend to the code base, with the accumulated consequences of compromises made in the quest for speed-to-market becoming similarly burdensome in future years. Added to this, digital banks will also need to interact with older systems in areas such as payments. Such integrations may themselves require the adoption of older protocols and systems to interoperate, creating further legacy issues. And so, thanks to a combination of some or all of these factors, digital natives now find themselves just as vulnerable as their more established competitors to the challenges of legacy technology.

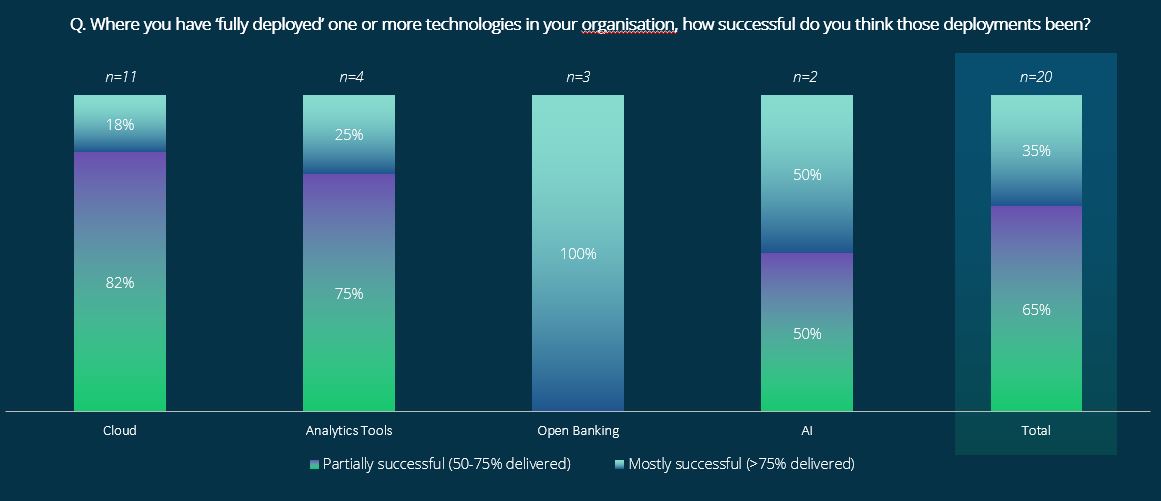

In the face of these operational, organisational and technological constraints, how did our respondents feel they were doing when it came to realising value from their efforts? As Figure 5 below shows, considerable value is being left on the table.

Figure 5: In most cases, BCM technology implementations fail to fully deliver on their objectives.

Source: Deloitte UK Banking & Capital Markets Technology Study, 2023

It should be noted that this exhibit draws on a statistically small number of responses, just 20 respondents out of the 151 surveyed who told us they had fully deployed projects in one or more of the foundational technology areas discussed earlier in this piece. Nevertheless, we believe the shared experience of these 20 technology leaders is consistent with our wider view that around 70% of digital transformations fail, providing a valuable lens on the success tech teams are achieving right now in the face of the barriers outlined above.

Indeed, in two-thirds of these cases – 13 out of the 20 reported full deployments in our study – respondents told us they only achieved 50-75% of the value they had originally targeted. Notwithstanding the challenges explored above concerning the ways in which firms measure success, and assuming this finding is scalable, this is clearly an area of concern. Larger budgets present bigger opportunities but also increase the pressure on tech leaders to deliver for their stakeholders. And here again we find ourselves facing the Paradox of Plenty.

In light of these results, the burning question facing tech leaders across banking and capital markets now is how to make the most of their investments – how best to deliver on outcomes targeted, how best to measure the success of their transformation projects and how to leave as little value on the table as possible in order to maximise the returns generated by their efforts.

We will explore these opportunities in the fifth and final instalment of this article series.

To read more on this please see our full five-part series linked below:

- The long and winding road… key challenges facing today’s BCM tech leaders after decades of banking transformation.

- Show me the money… what resources do UK BCM tech decision makers have to work with?

- Putting budgets to work… how are BCM tech leaders allocating their resources?

- Solving the paradox… how should high performing tech leaders in BCM respond to these challenges?

________________________________________________________________________________________________________________________________________________________________

1See “Mapping Digital Transformation Value – Metrics that Matter” (Deloitte Center for Integrated Research, 17 Nov 2023)

2Our survey was run in September 2023 with the assistance of an external B2B survey company called Coleman Parkes. The survey itself was anonymous, reaching 151 senior technology decision-makers at 68 separate BCM organisations across the UK satisfying a discrete set of criteria. Blog 1 in this series provides more detail on these criteria, showing the constituency we reached as well as the roles and responsibilities of the respondents who answered our survey – 80% of whom held CxO technology titles. Our respondents represent firms across UK retail, digital and SME banking as well as mutuals and wholesale and capital markets, the latter of which included the UK operations of various US and International investment banks. All were asked a series of questions concerning their technology investments, of which a cross-section of results is presented here.

Key contacts