2020 Global Health Care Outlook has been saved

Analysis

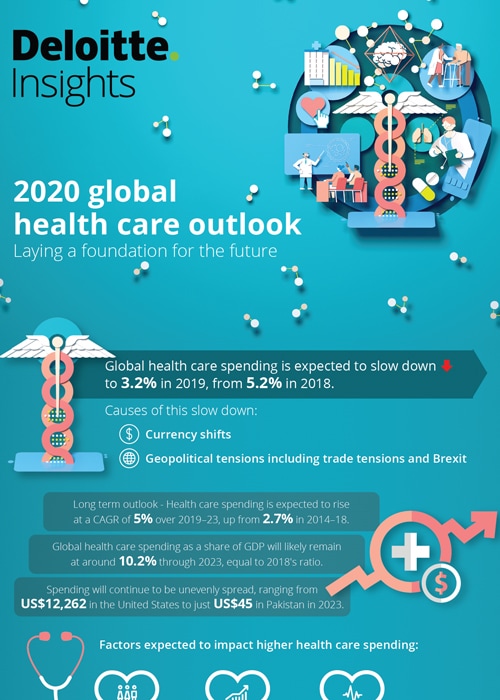

2020 Global Health Care Outlook

Laying a foundation for the future

Rising health care costs. Changing patient demographics. Evolving consumer expectations. New market entrants. Complex health and technology ecosystems. Health care stakeholders need to invest in value-based care, innovative care delivery models, advanced digital technologies, data interoperability, and alternative employment models to prepare for these uncertainties and build a smart health ecosystem.

Explore Content

- Overview

- Global health care sector issues in 2020

- Care model innovation

- Digital transformation and interoperability

- Future of work

Looking for the latest Life Sciences insight on COVID-19?

Read our weekly blog

Overview

With global health care spending expected to rise at a CAGR of 5 percent in 2019-23, it will likely present many opportunities for the sector. While there will be uncertainties, stakeholders can navigate them by factoring in historic and current drivers of change when strategizing for 2020 and beyond. Among these drivers are a growing and aging population, rising prevalence of chronic diseases, infrastructure investments, technological advancements, evolving care models, higher labor costs amidst workforce shortages, and the expansion of health care systems in developing markets. Health care systems need to work toward a future in which the collective focus shifts away from treatment, to prevention and early intervention. But, are stakeholders ready to respond to these trends and brace the smart health care delivery of the future? Deloitte's 2020 Global health care outlook takes a detailed look at the factors driving change in the sector and outlines suggestions that stakeholders can consider as they lay a solid foundation for the future.

Global health care sector issues in 2020

Financial operations and performance improvement

For years, financial challenges have shadowed the world’s public and private health systems to varying degrees, and we expect the situation to persist in 2020. This will make “value” a watchword in health care payment reform. The entry of non-traditional players in the health care sector have the potential to both support and suppress incumbents’ efforts to grow revenue. Digital giants and digital-first health solution disruptors are demonstrating that there could be an easier and more user-friendly way to conduct health care transactions.

Key Takeaways

- Health care stakeholders are implementing payment reforms such as value-based payment models that help providers, payers, and patients achieve the best outcomes at the lowest cost.

- Technology-enabled patient engagement strategies are enabling increased financial independence for patients in their health care decisions, in addition to improving interactions with their health care systems.

- Governments are also moving the needle by adopting universal health coverage and introducing pricing controls on pharmaceuticals and medical technology devices.

- Population health management (PHM) is being used to identify people’s health care needs and offer services accordingly.

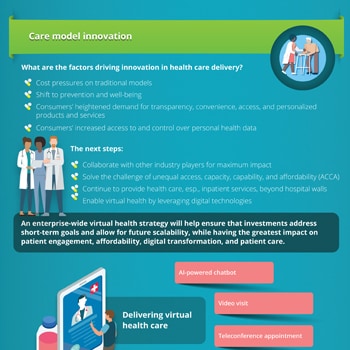

Care model innovation

Patients are no longer passive participants in their health care, they are demanding transparency, convenience, access, and personalized products and services. Which elements of consumers’ experiences with today’s health care ecosystem matter the most to them?

Care model innovation is expected to manifest itself in numerous ways during 2020. Future-focused care models will likely leverage people, process, and technology to address evolving individual and group health needs.

Key Takeaways

- Improving the health of a population requires new care models and technologies that address the drivers of health, enable early diagnosis, and monitor response to treatment.

- Hospital leaders might invest more in virtual care technologies or existing facilities rather than expanding their physical footprint.

- Health care systems can also link digital offerings to a strategically segmented customer experience and invest in core analytics to create a 360-degree view of the consumer, thus eliminating any operational barriers.

Digital transformation and interoperability

Despite numerous challenges, there has been considerable progress in digital transformation of health care, which we expect will continue in 2020 and beyond. With digital finding traction, the health care systems will witness a shift in data management from storing data sets to extracting insights that can be monetized and support opportunity areas including population health management and value-based care. Amidst this growth, there are challenges to digitization in health care—posed by outdated legacy platforms, cost and complexity of new technologies, and constantly evolving business needs and scenarios—and cybersecurity will continue to remain a prime concern.

Key takeaways

- Technologies such as cloud computing, 5G, Artificial Intelligence (AI), Natural Language Processing (NLP), and Internet of Medical Things (IoMT) can help streamline health care delivery and align it with changing consumer preferences.

- Increased use of Data-as-a-Platform (DaaP) to extract insights from patient data, will be area of interest for most health care players

- As virtual health care increases in capability and popularity, organizations will likely need to continue investing in security tools and services to identify risks and keep them at bay.

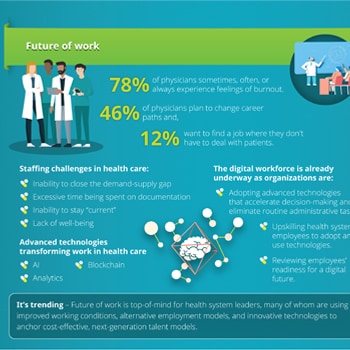

Future of work

A widening demand-supply gap of skilled professionals is creating immediate challenges for public and private health systems, which may also have long-term, detrimental consequences in 2020 and beyond. The situation appears to be particularly acute within two pivotal medical professions—physicians and nurses. Will health care systems consider new methods to source, hire, train, and retain skilled workers to achieve their overall objective?

Key takeaway

Holistic approaches to investments in people, processes, and technology will be key to regulatory compliance. A thorough assessment by health care businesses to understand how recent and upcoming policy changes will impact organisational priorities is an imperative. Care providers also need to explore strategies to build second-line defenses to reduce their administrative, financial, and reputational exposure.

Read our 2019 Life Sciences Outlook to learn more about the trends and issues impacting the life sciences sector.

Access previous versions

Review or download previous health care sector outlooks.

2018 global health care sector outlook

2017 global health care sector outlook

2016 global health care sector outlook