Manchester Crane Survey 2024

Rising to the Challenge

Key findings

Market summary

Manchester and Salford have witnessed a remarkable period of growth over the past decade, with a significant focus on strategic regeneration areas and underutilised sites away from the City Core. Many parts of our Crane Survey area are unrecognisable from even 10 years ago, such has been the pace of change. New neighbourhoods have emerged which offer a variety of exciting and distinctive new destinations that continue to support the popularity of the city as a place to live, work, visit, and spend leisure time.

Against this backdrop, and notwithstanding frequently reported macroeconomic and geopolitical challenges, this year’s Crane Survey results illustrate a continuing healthy performance in the number of schemes being completed and under construction. Whilst there has been a slight reduction in the number of new starts across all sectors, from 24 to 21, this figure remains broadly consistent with the average for the previous five years (22 per annum).

Manchester and Salford continue to thrive despite UK developers reporting on the negative effects on development feasibility of rising interest rates, which have led to higher costs of debt. Indeed, Glenigan’s Index of Construction from October 2023 revealed that the total number of UK residential construction starts had decreased by 23% from the preceding three months and were 30% down against 2022 figures. However, the Index also shows that activity levels in Manchester and Salford continue to hold up. This is explained in part by a proactive planning process across the two cities as well as by the fundamental draw of the city region. In large measure, these results must also be a positive testament to the resilience and ingenuity of the talent pool within Manchester’s construction sector, across both the public and private sectors.

Consistent with Crane Survey trends in recent years, the pace and volume of activity is most noticeable within the residential sector, with ten schemes completing and seven commencing in 2023. Whilst 2023 has not been a stellar year for completions in the office sector, with the effects of the pandemic seemingly catching up on the market, the pipeline for 2024 is much stronger with a notable increase in the number of highly sustainable, well-designed and amenity rich new build Grade A offices. These features are driven largely by occupier requirements and are found within new schemes across both the new build and refurbished market segments. The leisure and hospitality sectors remain resilient with good long-term prospects for growth. Finally, 2023 has been the year where pent-up demand for Purpose-Built Student Accommodation (PBSA) in Manchester has led to a record number of new starts. We expect this record to be broken again during the next few years as the higher education institutions and private sector respond to formally identified needs within this sector.

Offices, research and innovation

A resilient office market - a post-pandemic return to office?

Completions have been slow in 2023 but levels are set to recover in 2024 and 2025, based on current levels of construction. Three schemes completed construction in 2023, delivering 381,000 sq. ft. of new office floorspace to the market. This represents a reduction of about 315,000 sq. ft. compared to the previous year; however, it is encouraging to note that 1.5 million sq. ft. of floorspace is due to complete in 2024, with 38% of that figure already pre-let. 616,680 sq. ft. is in the pipeline for completion in 2025, and a further 75,000 sq. ft. is scheduled to complete at St Michael’s in 2027.

For example, Pinsent Masons and Hill Dickinson have signed ten-year leases for a combined 45,000 sq. ft. of floorspace within the first phase of St Michael’s. Both firms are reported to be paying around £43 per sq. ft. for their space, the highest rents in the city. Four New Bailey has been entirely pre-let to British Telecommunications. Accountancy and business advisory firm BDO will take 23,000 sq. ft. of floorspace over three floors at Five New Bailey (Eden), and law firm TLT has agreed a 15-year lease to take 20,000 sq. ft. on the top two floors. Plot 9a on First Street has been fully let to the Government Property Agency, employing 2,500 civil servants.

Beyond 2025, there is a risk that office completions will again fall away given the current cautious investment market in this sector; however, we do expect some further new starts in 2024 which will boost the longer-term pipeline.

In terms of geographical distribution, office schemes under construction in 2023 are concentrated largely in the City Core and the Southern Arc, including the First Street and Circle Square regeneration areas.

‘Flight to quality’ and the environmental, social, and governance (ESG) agenda

New headline rents at St Michael’s are also indicative of limited supply, which is being felt more acutely given shifts in occupier demand since the pandemic for highly sustainable, well-designed and amenity rich Grade A office floorspace (‘the flight to quality’). This is aligned to key drivers of demand, which include a desire to occupy space that will attract and retain the best talent, support post-pandemic workplace models, and demonstrate commitment to meeting organisational ESG targets. In our view and based on our current projections beyond 2025, those brave enough to take forward their schemes in this market are likely to be rewarded, as the market is expected to remain quite thin.

A positive increase in the number of refurbishments amidst a risk of ‘stranded assets’

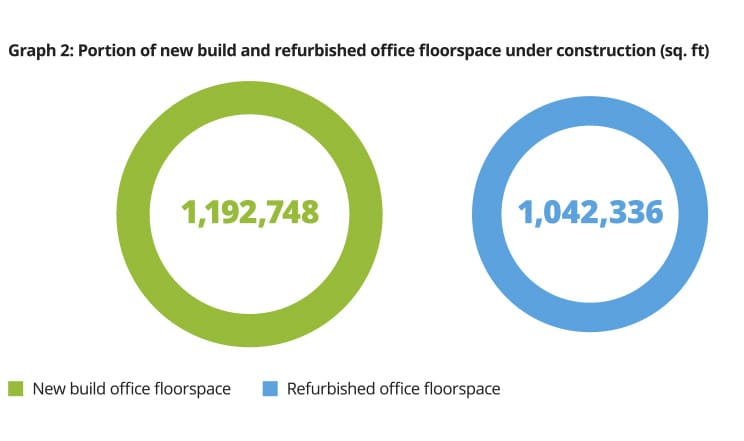

The amount of refurbished and extended office space, at around 1.2 million sq. ft. completed in 2023 or currently under construction, continues to grow. As a percentage of the total office floorspace under construction, the increase in refurbishments has been significant, from 21% in 2022 to 53% in 2023. This increase can be viewed as particularly positive given reported cooling-off within some segments of the investor market, fuelled by post-pandemic office trends, higher levels of office vacancies across the UK, and increasing concerns about obsolescent offices, often referred to as ‘stranded assets.’

Concerns about stranded assets are a 'push’ factor influencing this uptick in refurbished space. Asset managers are aware that businesses continue to want Grade A workspaces and are looking to vacate older office stock that struggles to meet the ESG expectations of eco-conscious occupiers. This is happening as businesses look to vacate older office stock that is struggling to meet the strong ESG credentials that are expected from eco-conscious businesses. The result is a widening gap in yields and capital value between lower-end and higher-end office space.

Another ‘push’ factor is the expected tightening of the Minimum Energy Efficiency Standard (MEES) Regulations, which will see developers and landlords under pressure to ensure that their buildings achieve a minimum Energy Performance Certificate (EPC) rating of B by 2030.

Conversely, there are also ‘pull’ factors making refurbished space more attractive, namely the sustainability benefits of reducing embodied carbon, and the potentially reduced build programme compared to new build offices. One such scheme is Bruntwood’s ‘Bond’ – the refurbishment of 38 - 42 Mosley Street and 57 Spring Gardens in Manchester City Centre. In addition to the benefits of reducing embodied carbon, the scheme also utilises the latest technologies to support a more sustainable future for the building, with secondary glazing, a new heat recovery air pump system, LED pendant lighting and a 100% electricity heating system to achieve an EPC A rating. Bond is reportedly 63% occupied despite only completing construction in October 2023.

Elsewhere across the city, the Rylands building is aiming for a BREEAM Excellent rating and a 5-star NABERS building performance and energy efficiency rating; and 70 Great Bridgewater Street (Havelock) is also coming to market in early 2024 as a BREEAM Outstanding, 5-star NABERS (Design Reviewed), and EPC A rated refurbishment and extension of an existing office building. This solution includes the retention of the structural frame of the building, and analysis prepared on behalf of the developer suggests that retention of the frame alone is saving an estimated 2,000 tonnes of CO2e.

Looking forward, the potential for refurbishing stranded office assets in Manchester will continue but will require all the creativity and ingenuity of the property sector to overcome the challenges. Manchester currently has an Article 4 Direction in place which removes permitted development rights from existing offices. Ultimately however some flexibility around land use may be required where all reasonable options for refreshed or renewed office space have been exhausted.

A good year for listed building office refurbishments

In the context of Manchester’s much valued cultural heritage, a positive feature of 2023 is that refurbishments of listed buildings total 31% of office floorspace in the pipeline. Out of the seven new office schemes starting on-site in 2023, listed buildings also dominated with four new refurbishment schemes, all located within the City Core. These include the refurbishment of 79 Mosley Street, the Rylands building, Pall Mall Court, and Sunlight House. As a reflection of occupier demand, these schemes are also pursuing similar environmental accolades to their new build counterparts; despite the latest government guidance not requiring listed building retrofits to meet the same environmental standards as new builds.

New builds

Of the office schemes completed in 2023, two were new-build office schemes: 4 Angel Square, NOMA; and Eden at New Bailey. Both are representative of major occupiers’ ‘flight to quality’.

Eden became the first new-build in the UK to achieve a record-breaking 5.5-star NABERS ‘Design Reviewed’ Target Rating and features Europe’s largest living wall.

At 240,000 sq. ft., 4 Angel Square is the largest office scheme delivered in the Crane Survey area during 2023. It has been designed with strong sustainability credentials – achieving a 5 NABERS ‘Design Reviewed’ Target Rating with smart technology playing a key role in ensuring energy performance, climate control and air quality. Planning Permission was also obtained in 2023 for a further 395,000 sq. ft. at 2 and 3 Angel Square, which will further establish NOMA as a key commercial destination alongside the significant levels of commercial floorspace within the listed estate.

At First Street, Plot 9B is coming forward as a NABERS 5.5-star rating, and the same rating is being achieved at Plot 10a which secured planning permission in 2023.

References to NABERS as a measure are a new feature in our Crane Survey. This in itself is an interesting change this year, with this method of assessment not stopping at construction but seeking to bridge the gap between construction and operation. Moving forward this will result in a shift in occupier responsibilities and working practices, and has consequences for the developer, landlord and occupier relationships and for leasing arrangements.

More generally, the UK government is set to move ahead with plans to regulate agencies that evaluate ESG performance of companies, due to the increasing influence that ESG has over investment and development. The aim of ESG regulation is to reduce instances of ‘greenwashing’ and ensure that the country remains on target to hit its 2050 net zero greenhouse gas emissions target, so that investors and consumers can make more informed decisions.

The importance of research and innovation

The UK government’s vision is to make the UK a global hub for innovation by 2035, and encouraging innovation is at the heart of its levelling up agenda. Innovation Greater Manchester seeks to leverage the success of Greater Manchester’s existing research and development (R&D) hubs to help level up the city region’s communities, generate the solutions needed to achieve net zero, and create the conditions for more businesses in more places to benefit from global exporting and inward investment.

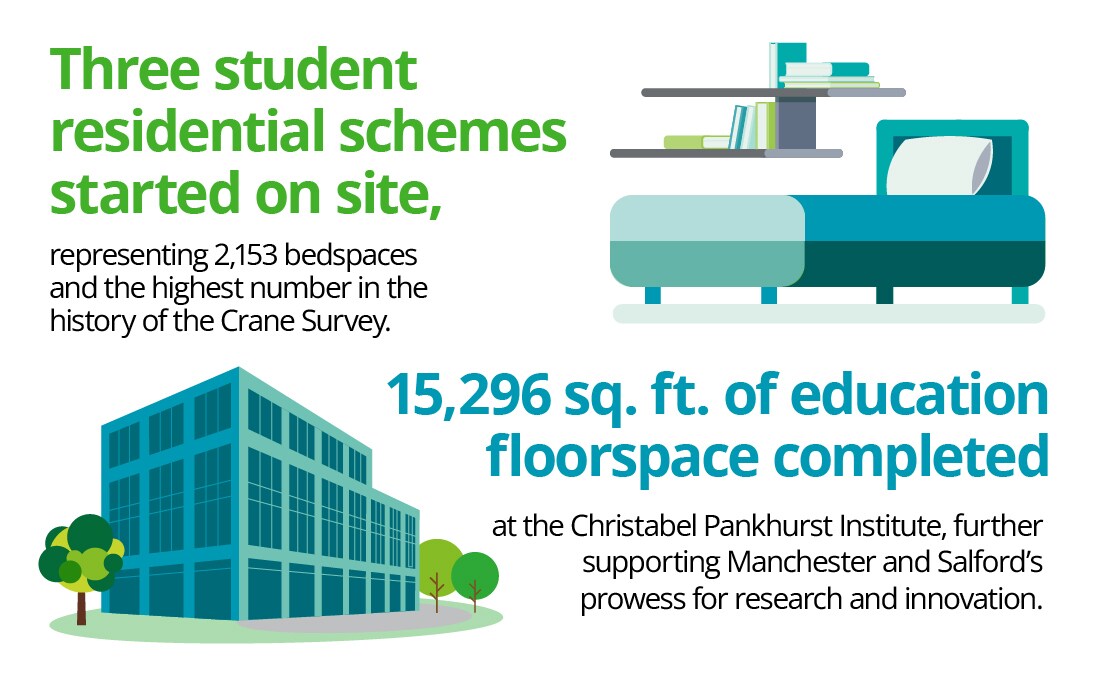

This focus on research and innovation is driving significant development activity to the study area. The University of Manchester’s Christabel Pankhurst Institute completed in 2023, creating over 15,000 sq. ft. of floorspace to promote needs-led health technology research and innovation. Comprising the refurbishment of a former bank on Oxford Road, the scheme provides some insight into how the education sector can also support the re-use of obsolete space in the City Centre. Planning permission was also granted for a new purpose-built facility to house UK Biobank within Manchester Science Park, moving from its existing Stockport location, with construction expected to commence in 2024.

Manchester City Council approved the ID Manchester Strategic Regeneration Framework in October 2023. Occupying the former University of Manchester North Campus site, ID Manchester provides a unique opportunity to deliver a comprehensive regeneration of this nine-hectare site. The vision is to establish a world-class innovation district in the heart of the city, commercialising the research specialisms of the University of Manchester, including health innovation, digital technology, and advanced materials. The ID Manchester illustrative masterplan totals over 4 million sq. ft., including offices and innovation space, homes, retail, leisure and local amenities.

Innovation-led development is also a feature outside the Oxford Road Corridor. English City Fund’s Crescent Innovation North seeks to create a distinctive, nationally competitive innovation district, delivering 1.4 million sq. ft. of commercial floorspace, nearly 1,000 new homes, a mobility hub, and 71,000 sq. ft. of learning facilities. Salford Rise, a 90m long ‘green podium’ providing pedestrian and cycle access over Frederick Road, will improve pedestrian mobility in this part of Salford to unlock further development opportunities.

In November 2023 the Chancellor announced the formation of the Greater Manchester Investment Zone, focusing on the advanced materials and manufacturing sectors, and committing £160m of public sector investment to the city region over the next ten years. The Investment Zone status will be an important step in realising the ambitions of innovation Greater Manchester. We anticipate that in 2024 the money will act as a catalyst for development activity in the Corridor and Innovation North, together with Atom Valley, to establish a world-class innovation ecosystem across the city region.

Housing

A move to steady state housing delivery?

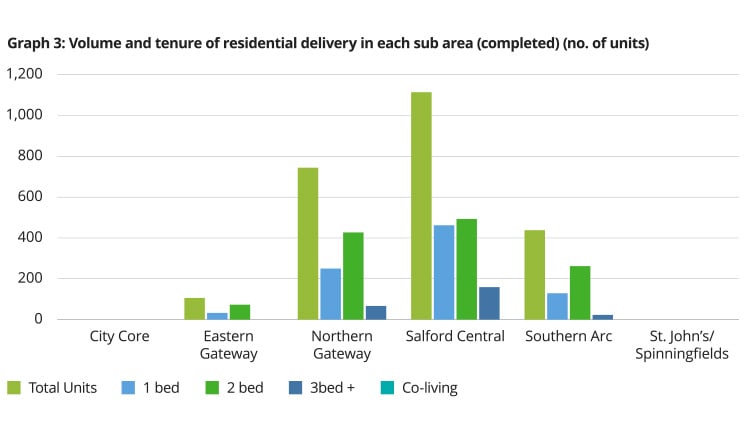

Housing delivery continues to hold up with a total of 2,402 new homes across ten schemes completed during 2023. This figure is largely consistent with the number of homes delivered in 2022 albeit under half the peak number of 5,549 homes delivered in 2021, which was the culmination of a delivery ‘boom’ period for housing in the Crane Survey area between 2019 and 2021.

The pipeline remains strong with 17 new starts in 2022 and seven new starts in 2023; however, there is no sign yet of a further boom period and the consistent delivery levels over the past two years may now be representative of a steadier and more sustainable trajectory of housing delivery, at least until economic conditions improve. However the total of 11,765 units under construction is well above the average of 6,349 units since our Crane Survey records began in 2007.

The City Core saw the highest volume of new homes starting construction, at 827 units across three schemes, with other new starts distributed across the Crane Survey area. Manchester City Council’s housing development company (This City) commenced construction at Rodney Street in the Eastern Gateway alongside Salboy’s Waterhouse Gardens in the Northern Gateway, Eutopia Homes’s Berkeley Square at Salford Central, and Renaker’s Phase 1 of Contour in the Southern Arc.

Salford Central as a delivery ‘hot spot’

The Salford Central area dominated residential delivery figures in 2023, with 1,114 completions across four schemes. These include Renaker’s Cortland at Colliers Yard, X1’s Manchester Waters Phase 2 Block C, Sourced Development Group’s Regent Plaza Tower B, and For Living’s Dock 5 scheme.

Most of the remaining completions are distributed within Manchester’s areas of strategic regeneration, notably Muse’s New Victoria scheme within the Northern Gateway.

Salford Central has now witnessed successive years of rapid housing delivery, with 15,996 new homes completed between 2014 and 2023. Additionally, there are 3,074 new homes currently under construction in this area.

Phase 1 of Berkeley Square was the sole new start in 2023. This could signal a slowing of activity in future years; however, the pipeline continues to be bolstered by new permissions. A further 1,190 new homes are planned at Middlewood Locks and there are major emerging proposals including Regents Retail Park, which was consulted on in early 2023. The Regents Retail Park proposals include five acres of public open space, up to 3,200 new homes in a series of tall buildings (akin to Deansgate Square in Manchester), and almost 107,000 sq. ft. of community and commercial space for shops, services and amenities. Major new sites also continue to come to market such as the Renault dealership on Trinity Way. Appetite regarding the expansion of activity towards and within Salford Quays remains strong.

Manchester’s evolving skyline

In Manchester, Great Jackson Street has been transformed from surface car parks to an iconic high-rise and high-quality residential-led destination, and new development continues apace. In 2023, the completion of 414 new homes at the Blade, together with the expected completion of a further 441 homes at Three60 in 2024 will add a further 1,800 residents to Great Jackson Street. During 2023, work began on Renaker’s new phase of development, known as Contour, which is scheduled to deliver a further 494 new homes to this area by the end of 2027. Alongside the residential development, significant emphasis has been given to placemaking and the provision of amenities and social infrastructure. The completion of the Crown Street Primary School in 2023 will help support the retention of families within the city centre. Indeed, there is already evidence of families taking up space within the Great Jackson Street area.

The seven completed residential towers at Great Jackson Street are now a significant feature of Manchester’s skyline, providing a backdrop to the City Core and, alongside the two further towers under construction, will provide 3,523 new homes over a period of eight years.

A focus on Build to Rent

The majority of new homes, both completed and under construction, are apartments, and a large number of these fall within the Build to Rent asset class.

This type of tenure has also not been without development viability challenges and additional problems thrown up by the Building Safety Act (including the need to introduce second staircases into consented schemes via planning amendments), but Build to Rent schemes in planning, under construction or completed continue to perform strongly.

Manchester’s dominance among regional cities as a primary market for Build to Rent, has been accompanied by a period of exceptional population growth. According to Manchester’s Economic Strategy published in 2023, the city’s population is estimated to have increased from 503,000 (2011 Census) to 607,000 in 2023 (Manchester City Council estimate), a rise of just over 20% and substantially ahead of the national average of 6.5%.[1] Given the rate of new housing delivery, much of this growth has been accommodated within the Crane Survey area.

In view of the substantial housing delivery in Manchester over recent years, it is somewhat surprising that Manchester’s Housing Strategy 2022 – 2032 identifies an estimated undersupply of 500 homes per annum and that overall delivery of new housing across the city has been unable to keep pace with demand. Indeed, we have had reports of some prospective tenants ending up in bidding wars, similar to what has been seen in the London rental market.

Due to the economics of supply and demand, Manchester has also experienced the highest rental growth among the top six UK cities outside London: Birmingham, Bristol, Edinburgh, Glasgow, Leeds and Manchester.[2] According to research by Urban Bubble, rents in Manchester, Salford and Trafford have increased by an average of 20% over the past year. This is undoubtedly another factor in the continued popularity of Manchester’s Build to Rent market with investors, albeit in the context of a somewhat more cautious approach in 2023 compared to previous years. With wages unable to also keep pace with rising rents, the affordability of rental products has been reduced.

An important component of demand for Manchester’s Build to Rent market is graduates from its universities, and indeed from further afield, choosing to begin their careers in the city. Manchester is ranked as the number one place to live in the UK as a graduate outside of London.[3] This is supported by strong graduate retention rates (just over half, according to pre-pandemic figures).[4] This trend is happening alongside a number of other reasons to stay in the city, including its improving transport infrastructure and connectivity, investment in green spaces such as Mayfield Park, the city’s growing cultural and leisure offerings, a thriving hospitality sector, and the establishment of attractive new neighbourhoods where people choose to live.

Notwithstanding the propensity of young people to choose Build to Rent, reports from many developers indicate that there is also a much older and more varied demographic within Build to Rent than had perhaps been expected.

The next ten years: Policy makers’ response

The current dynamics in the market have led Manchester and Salford’s policy makers to emphasise the need to support a broader range of new housing that meets the overall needs of its diverse and growing population whilst also addressing the rising levels of social inequalities that have been exacerbated by the effects of COVID-19 and the post-pandemic pressures on the cost of living.

For example, Manchester has committed to building 36,000 new homes in the city in the period 2022 to 2032, 10,000 of which will be affordable including a target of 3,000 new homes in the city centre. Within the Crane Survey area, 598 affordable homes were either completed during 2023 or are currently under construction, spread across nine schemes. A further five schemes in the Crane Survey area have planning permission and include the provision of affordable units including MCR Property Group’s The Gas Works, Clarion Housing Group’s Store Street and Great Ducie Street schemes, and Far East Consortium’s Dantzic Street and Red Bank schemes, delivering about 1,180 additional affordable units to the city.

Over recent years, there have been limitations to the amount of affordable housing delivered within market schemes, due to challenges around development viability demonstrated and checked through rigorous processes of independent peer review and scrutiny. The role that innovative public sector-led delivery models such as This City in Manchester, together with the use of Homes England grant funding where available, is likely to be crucial in relation to Manchester and Salford’s ability to meet its affordable housing needs.

Moreover, significant opportunities exist around the City Centre to meet housing needs in an inclusive and equitable manner within future areas of place-based regeneration focus, including the Northern Gateway, as well as Holt Town and Strangeways, both of which are to be the subject of refreshed strategies over the next 12 months.

The introduction of co-living

As an extension of Build to Rent, there are now also 2,656 co-living units, totalling 3,570 bedspaces across Downing’s Square Gardens at First Street and Vita’s Union T1 and T2 at St John’s. This is a significant addition to Manchester’s offering and it will be interesting to see how they perform in practice, and the value they add. The British Property Federation’s October 2023 Co-Living Report highlighted its potential role in meeting housing needs across UK cities,[5] but Manchester City Council has adopted a cautious approach. This has resulted in no further planning permissions for co-living schemes currently. Indeed, this cautious approach may continue to be the case until the value of current schemes under construction is assessed as they move into their operational phase over the next 24 months.

PBSA and education

The success of Manchester’s education institutions has been a feature over the past decade and a key pillar in its sustained economic growth. The major university campuses have been transformed and concentrated within the City Core; and the demand from both domestic and international students grows year on year, creating a talent pool that attracts businesses. The combined effects of business and institutions operating cheek by jowl are illustrated by the success of the Oxford Road Corridor. This trend continued in 2023, with the city’s education and research institutions continuing to drive development activity, and a further uptick in activity is predicted for 2024 and beyond.

A step-change in PBSA delivery

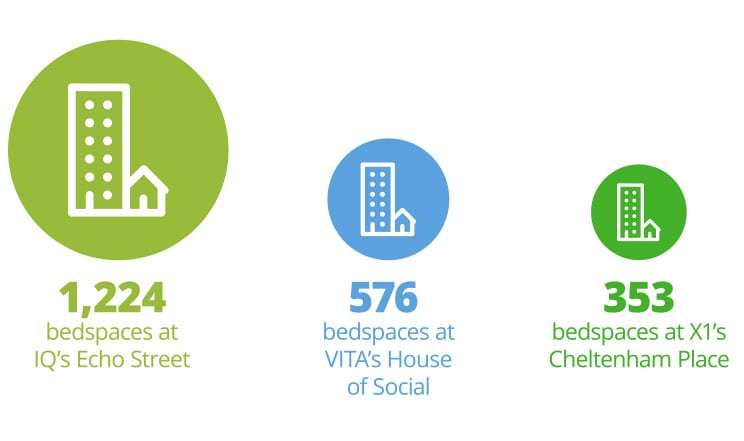

A key headline for this year’s Crane Survey relates to the step-change in the numbers of PBSA schemes coming forward in Manchester. The 2,153 additional bedspaces commenced in 2023, across the three schemes shown on the image below, is the highest number under construction on record (the previous peak being 1,794 bedspaces in 2018). This is in stark contrast to 2022 when no new schemes were reported. Additionally, a substantial number of schemes were coming through the planning system in 2023, with a total of 4,813 PBSA bedspaces granted permission within the Crane Survey area.

There are several reasons for this trend:

Historical undersupply exacerbated by closures. Since 2018, only 2,868 new student bedspaces were delivered, while full-time student numbers increased by 8,100 in the same period. There were also some closures, including Owens Park in 2019.

A shift in the level of support for new private sector-led PBSA accommodation in Manchester from the higher education institutions. This is reflected in Manchester City Council’s Economy and Scrutiny Committee Report of May 2023 which estimates that there is a need for an additional 5,440 to 11,320 bedspaces up to 2030. The actual levels of demand will need to be monitored carefully, and may well rise, given that the number of applicants in the UK each year for higher education is expected to increase from 750,000 currently to one million by 2030.[6]

The effect of Manchester’s undersupply has been a rising cost of PBSA. Manchester now has amongst the highest average student accommodation rental levels across the UK. Recent schemes that have secured planning permission have therefore offered up a percentage of affordable bedspaces through a nomination agreement with a university. This is being done on a voluntary basis, since Manchester City Council does not currently have a development plan policy covering affordable PBSA. However, existing planning policy does favour schemes where support has been secured from one of the higher education institutions. Examples include IQ’s Echo Street and VITA’s House of Social. As Manchester’s Local Plan Review comes forward, we might expect an affordability requirement to form part of a new student housing policy.

Demand in the Crane Survey area has resulted from a growing propensity for students to seek accommodation within the city centre. This trend partly reflects the growing numbers of international students. There are over 10,000 international students at the University of Manchester from 160 different countries, and over 4,000 reported at Manchester Metropolitan University from 100 different countries. Where this demand has not been met to date by student accommodation in the city centre, students have occupied mainstream residential accommodation. There is clear evidence to support this finding, with Manchester City Council able to track numbers of council tax exemptions.

Due to the difficulties described in this report with residential and office development and the current value of the PBSA market, several developers have sought to pivot towards PBSA during 2023. Our own evidence, from enquiries received, points to the level of interest in PBSA schemes at this time being at an all-time high.

All PBSA schemes in Manchester coming forward within the Crane Survey area fall within Manchester’s Oxford Road Corridor, in line with Manchester’s Core Strategy Policy H12. Manchester City Council’s May 2023 Economy and Scrutiny Committee Report also identifies that there is a pipeline of sites within this area capable of meeting Manchester’s identified need for PBSA.

Whilst significant progress has been made in 2023 towards addressing PBSA needs, construction levels are not yet where they need to be. However with a pipeline of permissions and schemes coming through the process, this situation is likely to be improved by the end of the decade.

Continued investment in world-class education facilities

In 2023, Manchester Metropolitan University demonstrated its commitment to enhancing education space to provide facilities that address the standards required by university applicants in an increasingly competitive higher education market. The University’s new Science and Engineering Campus will open on Cambridge Street in 2024 and a planning application for a new All Saints Library was submitted in November 2023. Phase 1 of the All Saints Park refurbishment works also started construction in 2023, to provide a high-quality, pedestrian focused, public realm and setting for Manchester Metropolitan University. Phase 2 of the Manchester College Strangeways Campus also commenced construction in 2023. Together with residential developments by Latimer and Salboy, this will comprehensively redevelop the former Boddingtons Brewery site, which will in turn act as a catalyst for development in the wider Strangeways area.

Tourism and hospitality

A city of culture

A key headline in 2023 was the completion of Factory International’s Aviva Studios, providing an international venue for arts and music that will add to Manchester’s role as a cultural destination and sees Manchester making a considerable investment in its future as a cultural capital.

Manchester remains firmly on the world stage as one of the top places to visit according to Lonely Planet’s Best in Travel 2023 list. Exciting new events, and new openings planned for 2024 are testament to this. In December 2023, Chanel chose to host the Métiers d’Art fashion show in the Northern Quarter, with Chanel’s Creative Director citing the gritty backdrop and music and arts culture as key to its attraction. Initial estimates are that this event generated a direct economic benefit of around £8 million and additionally over £100 million in value from positive national and international media coverage for the city.[7]

Also set to open in 2024 is Co-op Live, a best-in-class flexible use arena, which will operate alongside Manchester’s existing arena. Whilst just beyond the edge of the Crane Survey area, this venue will provide a major boost to the events and hospitality industry in central Manchester and Salford, encouraging further investment. Alongside the new arena, Manchester City’s North Stand development will be a further significant step towards creating a best-in-class fan experience and year-round leisure and entertainment destination at the Etihad Campus. The proposals, which aim to start on site in early 2024, will not only expand the Etihad Stadium capacity, but will deliver a mix of commercial, retail and leisure space, as well as new hotel beds, creating a destination with activity all year round. Together these projects will act as a further catalyst to the expansion of the city centre outwards into the Eastern Gateway area of our Crane Survey.

An insatiable appetite for F&B

Investment in the city's economic growth and its rising population continue to underpin its growing leisure and hospitality sectors. In the Crane Survey area, the strength of the F&B and leisure economy is unrecognisable from what it was even a few years ago, and this is partly a result of the critical mass of city centre residents who are enlivening and activating the area throughout the week.

In 2023, a total of 245,652 sq. ft. of new hospitality and leisure floorspace was brought to market, far exceeding any figures previously recorded in the Crane Survey. For example, Diecast combines F&B offerings with entertainment and a wider creative neighbourhood, within a former industrial setting. Other notable additions include New Century, Canvas and Yes. An additional 285,837 sq. ft. of retail and leisure floorspace is also under construction, being delivered largely as part of wider mixed-use developments.

As an accolade for the city’s thriving culinary culture, the Midland Hotel was chosen as the venue for the Michelin Guides Great Britain and Ireland Awards in February 2024. New independent entrants for 2024 also seek to capitalise on this rich culture providing a vibrant range of amenity offerings, including Maya on Chorlton Street, and Skof, a new restaurant by acclaimed chef Tom Barnes, which is set to be the newest amenity occupier to NOMA. Fairfield Social Club will also provide further activity and interest in the Redbank and Northern Gateway area. SOHO House is also set to open in 2024 and will further enliven the St John’s area, and will be the brand’s first opening in England outside London and the south of England.

Hotels and the introduction of branded residences

Following a peak of 1,504 rooms completed in 2022, no further hotel completions occurred during 2023. However, hotel occupancy rates remain resilient in Manchester. A rate of 68.5% was reported for January 2023 − higher than the city’s pre-pandemic level, and slightly stronger than London’s occupancy rates.[8]

Given the pipeline of projects, including the developments in the live entertainment sector, hotel developers are evidently responding with new and diverse offerings to further support the visitor economy. This is evident in seven schemes now on site, totalling 1,210 beds and including two hotel schemes totalling 519 beds which started construction in 2023. Most of the beds under construction are due to complete in 2024 delivering 691 new units to the market, including 216 beds at the Treehouse Hotel at Deansgate, the first venture of the brand in the UK outside London and comprising a major refurbishment of the former Renaissance Hotel.

New starts in 2023 include the 162-bed W Hotel, representing the luxury brand’s third UK location after London and Edinburgh. W Hotel will enhance the appeal of Manchester and Salford as a destination for visitors, adding a 5-star hotel offering that will add to Manchester’s growing range of similarly graded accommodation at hotels, such as The Edwardian and Hotel Gotham. Forming part of the second phase of the St Michael’s development, the hotel will be in a new 40-storey tower sitting alongside 213 new apartments, including W Residences which will be a first for Manchester in the branded residences space.

Aparthotels also continue to form part of the pipeline with a further 357 aparthotel rooms under construction at 325 Deansgate. These types of facility across the city can meet demand for ‘home from home’ amenities and help to alleviate the negative effects that a proliferation of Airbnb accommodation can have on community cohesion within residential developments.

The continuing positive outlook in the hotel sector provides further evidence of the city ‘bucking the trend’ meeting successfully the challenges of inflation, a stagnant economy, rising costs, and an inability to raise prices due to consumer pressures. However, challenges relating to climate change are perceived as a key risk for the hospitality industry in the future, alongside labour shortages which are expected to continue beyond 2025.

The results from this year’s Crane Survey underline the fact that Manchester and Salford remain well established as a key city destination, with new developments further supporting the city’s visitor economy. Manchester City Council established the first UK Tourist Tax in April 2023: the City Visitor Charge is expected to raise an additional three million pounds a year, but with a minimal impact on tourists at a charge of £1 a night. This tax which follows similar initiatives by other top European city destinations such as Paris and Barcelona, is testament to the city’s confidence in the visitor economy. No data has been released to date on the revenue receipts or the projects funded; however the outcomes of the scheme will be of interest to many in the industry and watched closely by other cities considering similar funding options.

Outlook

Offices, research and innovation

There is a significant pipeline of office floorspace with a total of 2.2 million sq. ft. under construction, and 1.5 million sq. ft. due to complete in 2024. A significant number of schemes comprise refurbishments and our Crane Survey suggests that this shift is likely to continue and will help to support Manchester’s journey to net zero, including embodied carbon savings. It is also proving positive news for listed buildings in the city, with several now undergoing refurbishment.

In a challenging debt market with high interest rates, a number of new schemes with planning permission appear to have stalled, meaning that there is some risk of an acute shortage in supply of accommodation that will meet occupier demand beyond the middle of the decade. There is also a risk of stranded assets becoming more prevalent, particularly among more ‘difficult’ assets – a challenge that will test the real estate sector’s levels of creativity and innovation.

Research and innovation continues to be a major driver of new employment space. Moving forward, this should continue to accelerate with proposals to create a world-class innovation district in the heart of the city at ID Manchester, as well as Salford’s Crescent Innovation North. More broadly, there is an opportunity to capitalise on a new Investment Zone for Greater Manchester, announced in November 2023. This will focus on advanced materials and manufacturing sectors, with £160m public sector investment committed to the City Region and an anticipated £1.1 bn of private sector investment.

Housing

Although figures remained strong, 2022 marked an end to the boom housing delivery period between 2018 to 2021 which has resulted in circa 22,000 homes being delivered to market over the past six years. The picture in 2023 is broadly consistent with 2022, suggesting a move to steady state housing delivery over the next few years. Moving forward, the city is now well established as a primary residential market and there are many good reasons to want to live in Manchester, as demonstrated through the diversity of activity in this report. For this reason, and with the expectation of improving market conditions, we expect housing delivery rates to increase as we move into the second half of the decade. This will also help to satisfy policy makers recognition that there still remains an undersupply of housing in Manchester.

Perhaps more challenging will be addressing the identified need to further diversify the types of housing delivery across the Crane Survey area, including Manchester’s desire for 3,000 affordable homes across the city centre in the period to 2031. This is likely to require public sector intervention through grant funding and new models of housing delivery. There is certainly much to be done, as development extends beyond historic city centre boundaries into areas identified as priorities for place-based regeneration including Strangeways and Holt Town.

PBSA and Education

A key headline in 2023 has been the step-change in PBSA delivery, with record levels of bedspaces under construction and in the pipeline. Whilst significant progress has been made in 2023 towards addressing PBSA needs, construction levels are not yet where they need to be. However with a pipeline of permissions and schemes coming through the process, this situation is likely to be improved by the end of the decade. With rising PBSA rents, moving forward we also expect more emphasis on the delivery of affordable PBSA and that Manchester City Council will introduce a policy in that regard as part of its forthcoming Local Plan Review.

In the coming years it is expected that the higher education institutions will continue to seek to commercialise and expand their main campuses to drive agglomeration, increase direct socio-economic benefits; and attract talent (students and staff). This will likely include tangible and intangible barriers being removed to improve better connections and harmony with the places in which they operate and introduce their students to the economic markets they are about to enter.

Leisure, retail and hotels

The city’s appetite for new hospitality and leisure space remains strong. In 2024, we anticipate the opening of Co-op Live, a best-in-class flexible use arena capable of hosting a wide range of premier events, with audiences of up to 23,500 people to further boost this sector and the visitor economy. The seven hotel schemes on site will provide a further boost to the supply of accommodation in the city against the backdrop of strong hotel occupancy rates reported in January 2023, which have returned to, if not exceeded, the levels immediately preceding the pandemic.

Data in detail

A summary of all data across all development sectors can be accessed using the interactive Development map, Development activity and New start charts below, allowing you to explore all development projects, their location and what this means in terms of overall development activity.

The Report

Why?

A report that measures the developments taking place across Manchester and Salford city centres and their impact. Property types include residential, office, hotel, retail and leisure, student accommodation, education and research facilities, and healthcare.

Where?

Our Crane Survey research area covers Manchester City Centre and Central Salford.

What?

Developers building new schemes or undertaking significant refurbishments exceeding any of the following sizes: office – 10,000 sq. ft.; retail and leisure 10,000 sq. ft.; residential property – 25 units; education, healthcare and research – 10,000 sq. ft.; hotel – 35 rooms.

When?

Data for the Crane Survey was recorded between 3 January 2023 and 3 January 2024.

How?

The local Deloitte Real Assets Advisory team has monitored construction activity and planning permissions granted, supplemented by rigorous field research. This research has been verified by industry contacts and in-house research teams.

Contacts

Simon Bedford

Partner, Real Assets Advisory - Development

Zoe Davidson

Partner, Real Assets Advisory – Development

John Cooper

Partner, Real Assets Advisory – Planning