Tax Transparency

Achieving clarity in a complex world

Businesses are increasingly expected to go beyond existing legal requirements and volunteer more information about their approach to the management of tax and its outcomes (i.e. the taxes they pay and collect on behalf of others). Communicating effectively about a complex subject such as tax is important but can be difficult, particularly in the absence of common standards.

In addition to the content below, you can also download our practical summary on how groups are responding to a variety of tax transparency drivers, and read our detailed thought piece on how tax transparency initiatives are evolving and the trends we’re seeing in the market.

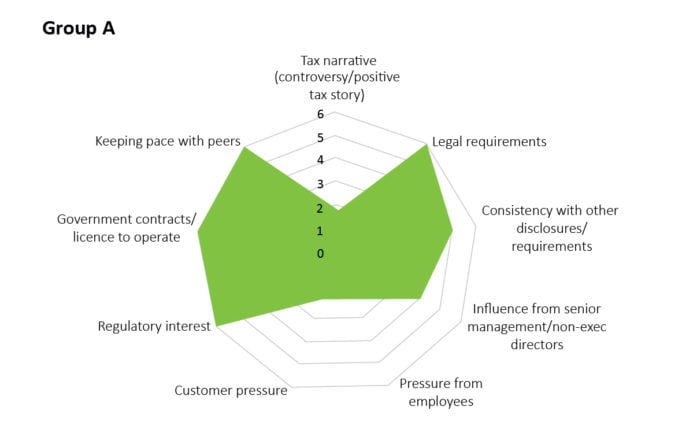

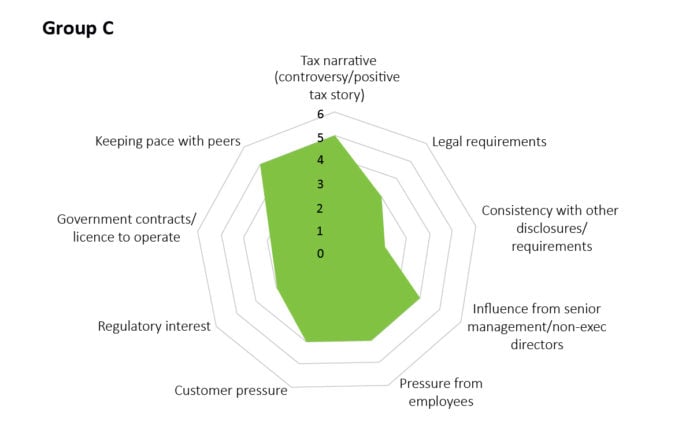

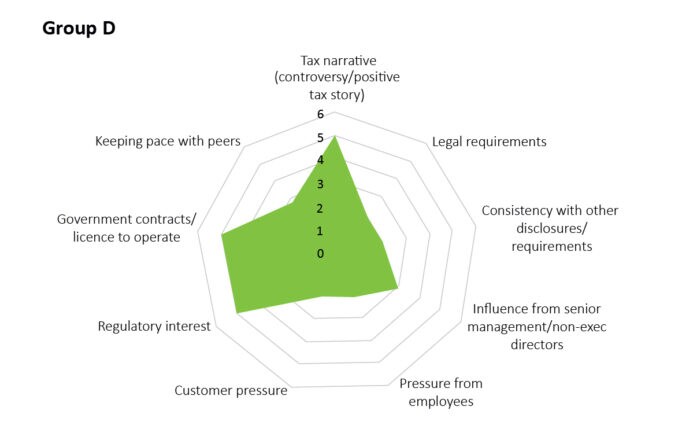

Experience and evidence show that there is no single ‘right’ way for all businesses to respond to these expectations. Instead, groups’ disclosures are influenced by a varying range of factors; from external stakeholder expectations (such as regulators, tax authorities, investors and customers) to internal expectations and considerations (such as pressure from employees and senior management, a need to be consistent with other Environmental, Social and Governance (ESG) disclosures, or a desire to keep up with peers).

Whilst for many groups with a UK presence, the UK’s Tax Strategy legislation has set the standard for their Tax Transparency disclosure, this is likely to change significantly in the coming years with the introduction of the EU’s public country-by-country (CBCR) requirement. The Directive will require multinationals with worldwide revenues of more than EUR 750 million to disclose publicly, on a country-by-country basis, corporate income tax information relating to their operations in each of the 27 member states, as well as information for certain third countries on the EU list of non-cooperative jurisdictions.

Member States have until June 2023 to transpose the Directive into national laws. These national laws will apply, at the latest, from the commencement date of a business's first financial year starting on or after 22 June 2024, but individual Member States have the option to implement the rules sooner. It is our expectation that this development will prompt affected businesses to think about their wider tax transparency strategy and many may feel that their story is better told if they provide more information than the minimum required.

In addition to mandatory disclosure requirements around tax transparency, there are a wide range of voluntary tax transparency regimes to which groups can sign up. As noted above, groups may look to obtain a tax transparency ‘badge’ (by way of signing up to a regime) in order to provide positive messaging about their tax affairs or counter previous controversy. Many groups are also now looking to demonstrate their ESG credentials in order to secure investment and funding, as well as attract customers and partners, and signing up to one or more of these tax transparency regimes may fulfil a key part of this complex ESG puzzle.

The chart below shows a range of voluntary tax transparency regimes which groups can sign up to. Some are specific to the UK and others are global. Some are specific to tax and others are broader (reflecting a range of ESG topics).

Typical themes of tax transparency disclosure

Although there are a lot of different drivers for groups, and a wide variety of external transparency regimes groups may be aligned with, groups typically make voluntary tax disclosures under the following themes: context, approach, key matters, data and assurance.

Low level of disclosure

High-level summary of scale and breadth of the organisation’s commercial activities. Setting the scene for the group’s tax profile.

High level of disclosure

In-depth explanation of key parts of the business and their value chains, and related taxes and other payments to governments. Deeper dives on selected key countries.

Low level of disclosure

Core elements of tax strategy: commitment to compliance, approach to planning, governance and risk management arrangements and interaction with tax authorities.

High level of disclosure

Global strategy statements which also expand on other areas of interest, including: value chain, use of advisors, engagement around tax policy and connection of tax to broader ESG agenda/purpose.

Low level of disclosure

No or limited commentary on specific tax matters.

High level of disclosure

Detailed commentary on specific aspects of the group’s tax profile e.g. presence in low tax jurisdictions, overview of intra-group transactions/transfer pricing, and policy towards tax incentives.

Low level of disclosure

Country-level information provided on taxes and other payments borne by the organisation.

High level of disclosure

Broader tax contribution data (including where taxes are collected but not borne). Some provide broader economic contribution/community investment data. Data may be presented at more granular levels (e.g. national/state). Some OECD-based CbC disclosures.

Low level of disclosure

No external assurance in relation to voluntary tax transparency reporting.

High level of disclosure

Limited/reasonable assurance opinions, typically in relation to approach taken to collect/report tax contribution data. Some included audit opinions.

Steps to communicating with confidence

Regardless of the scale and starting point, groups would do well to follow a proven four step process when developing and enhancing their tax transparency disclosure:

Understand the landscape

Set a tailored strategy

Mobilise efficiently

Communicate confidently

Tax Transparency – long read

Read our detailed thought piece on how tax transparency initiatives are evolving and the trends we are seeing in the market.

Tax Transparency – practical summary

Read our summary of the practical steps which groups are taking in response to a variety of tax transparency drivers.

You can view our latest Tax Transparency DBrief webinar here

Get in touch

In addition to supporting groups across all four of the steps above, Deloitte has extensive experience working with organisations across multiple industries to assist them in planning their responses to legislative change and new ESG governance and compliance requirements. To discuss your ESG requirements in more detail, please get in touch with our team through the contacts below, or speak to your regular Deloitte Tax contact.

Mark Kennedy

Partner, Tax Transparency

Chris Thomas

Associate Director, Tax Transparency