Streamline: Operational TP has been saved

Solutions

Streamline: Operational TP

Automate your transfer pricing documentation through a pragmatic approach to transfer pricing technology

One of the biggest challenges in transfer pricing is ensuring that your business model and transfer pricing policy translates into a simple intercompany agreement that is accurately reflected in your financial statements and statutory returns. Often, the data you need for transfer pricing is not "tax sensitised" and is scattered across disparate IT systems and databases. We'll turn these challenges into an opportunity to create a pragmatic, user-friendly solution. We'll work with you to design and streamline your processes - and then automate them using an appropriate technology solution that fits your long term IT vision. As a result, you'll transform your tax department, and go from simply being compliant to being in control.

Explore Content

- Thought leadership paper: Operational Transfer Pricing

- Form: Operational Transfer Pricing

- Infographic: A best practice blueprint for integrated global transfer pricing operations

- Video: Robotic Process Automation for Tax

Thought leadership paper: Operational Transfer Pricing

Transforming the process and managing change

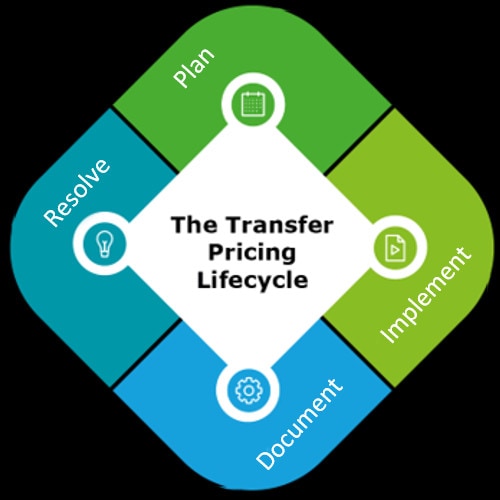

The OECD's BEPS Action13 initiative and other tax measures have brought about significant operational transfer pricing policy implications for tax executives of multinational companies. While many companies maintain a firm focus on the "plan," "manage," and "resolve" phases, less emphasis is often placed on the "streamline" phase of the lifecycle, commonly referred to as Operational Transfer Pricing (OTP). Incorrectly recorded outcomes are increasingly a target of tax authorities and the main cause of adjustments in most tax audits. Aligning all elements of the Transfer Pricing lifecycle—policy, documentation, and tax authority interaction—with OTP is essential.

Three key drivers of this development are:

- Validity of Transfer Pricing policy. The spotlight has intensified on individual businesses with added scrutiny and reporting requirements.

- Tightening tax authority requirements. Some jurisdictions are increasingly reluctant to accept post year-end margin/costing adjustments.

- E-audit requirements. New measures are mandating that financial data be available in (or close to) real time and new data requirements for adjustments.

These implications create an imperative for businesses to implement efficient, automated technology-enabled approaches to operational transfer pricing.

Infographic: A best practice blueprint for integrated global transfer pricing operations

There are a wide spectrum of technology solutions available in the marketplace that can fulfill your current business needs―but there is no one "perfect solution". To help you to identify the best fit for your organisation, Deloitte has a unique approach and process to help you:

- Improve your existing transfer pricing processes

- Identify data and people gaps

- Leverage your existing IT infrastructure and future IT vision

By implementing a suitable technology solution and updated processes, you will enjoy the following benefits:

- An acccurate reflection of TP policies in your financial statements;

- A near real time access to data necessary to monitor your transfer pricing

- A timely identification of any TP adjustments necessary;

- An efficient and quick book close process; and

- Readily available data segmentation that makes it possible to fulfill TP documentation and compliance requirements.

Operational Transfer Pricing (“OTP”) provides confidence that the agreed-upon transfer pricing policies are actually happening on the ground, all around the world. This not only enables the business to implement these policies, but also to confirm that they are consistent in all the company’s records.

This area is under increasing scrutiny due to the BEPS project and tax authorities around the world testing, in detail, the actual outcomes of TP policies. Without a robust OTP system in place, organisations might not be able to implement TP policies consistently nor respond appropriately to TP audits.

For many companies, transfer pricing represents the largest tax risk if the company and tax authority cannot agree on the appropriate arm’s length price. This can result in large penalties from the tax authorities, which has implications not only on finances, but also on reputation in the market.

Key contact

Recommendations

The Global Transfer Pricing Readiness Center

Your global transfer pricing checklist