United Kingdom: Pressing Play on a European powerhouse has been saved

Article

United Kingdom: Pressing Play on a European powerhouse

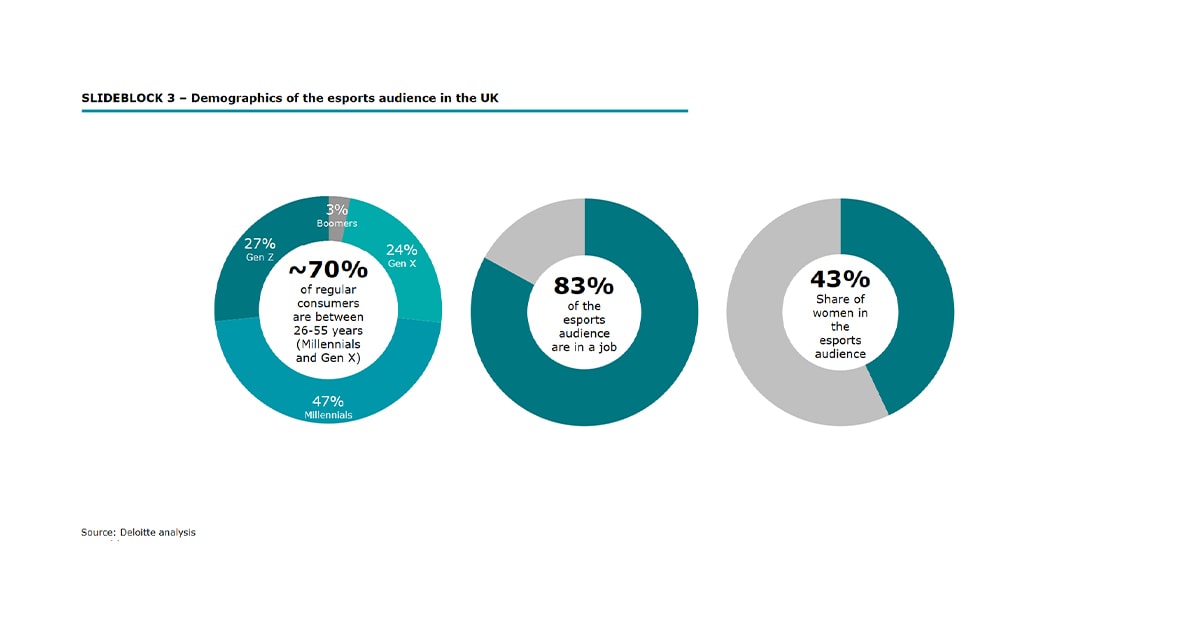

The UK is an important esports market and is therefore naturally home to a number of strong and eminent esports teams. This combined with an interesting audience profile (the majority (73%) of its regular consumers being over the age of 25 - only 27% being Gen Z), brings fan engagement and monetisation opportunities.

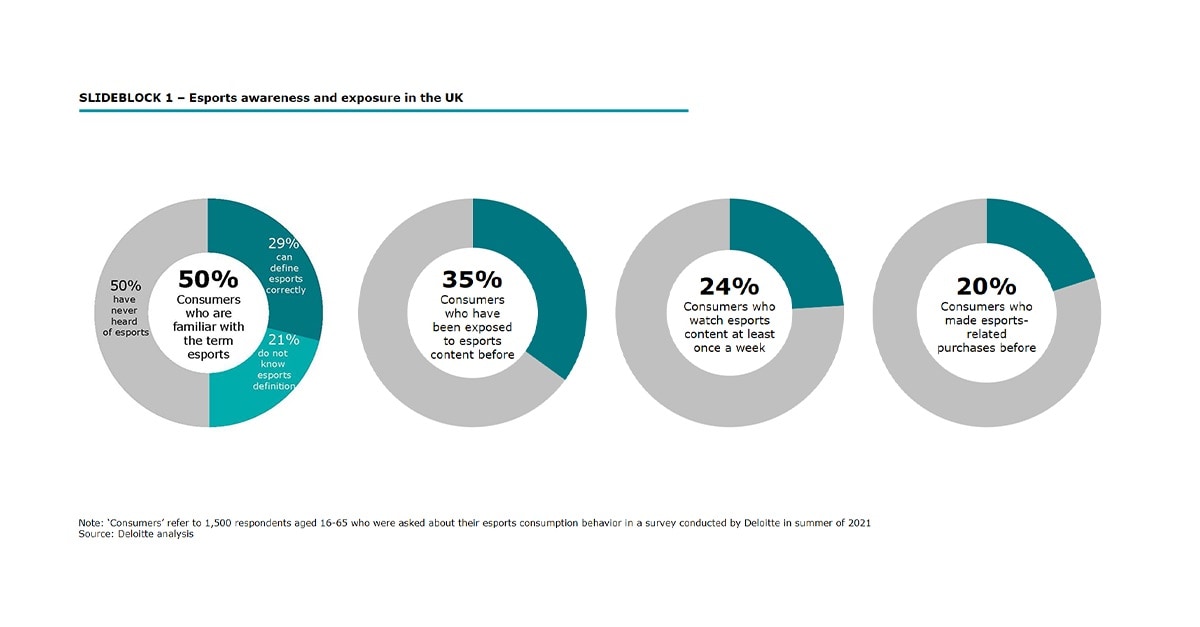

UK esports corporate and investor interest appears to be taking note following recent significant deals, signifying confidence in future growth across its ecosystem. However, the UK lags some of its European peers in respect of awareness levels (29% of respondents are aware of esports and able to correctly define it) and regularity of esports content consumption (24%).

Leading teams attracting corporate and investor interest

While the UK is among the leaders in Europe for traditional sports, its esports ecosystem is still developing, especially at grassroots level. Popular titles include Counter-Strike: Global Offensive (CS:GO),DOTA 2, FIFA, League of Legends and Rocket League.

Fnatic, Team Dignitas and Gfinity are the eminent esports teams in the UK, however investor interest has seen the establishment of challengers, such as the London Stock Exchange (LSE) listed Guild-esports, backed by David Beckham. Further investor interest can be seen via successful fundraising efforts by Fnatic (both institutional and crowd-funded), excel esports (€20m raised) and corporate interest via Fnatic again following its recent sponsorship deal with crypto.com.

There appears to be an international focus among some UK teams, with the recent efforts of Wolverhampton Wanderers FC, an English Premier League football team, who have looked to expand internationally via the acquisition of Chinese esports team QGhappy by its esports division, Wolves esports. Gfinity has taken the innovative approach of creating its own Digital Media Group to engage with its fans globally.

The success of these teams on the international stage may prove to be the catalyst of growth domestically and lead to a more competitive and widespread esports landscape to the benefit of all its stakeholders.

The interaction between traditional sports and esports in the UK is intriguing, with the esports FIFA 20 Premier League tournament between professional football players for their respective teams gaining significant traction, with the BBC, a free-to-air TV platform in the UK, subsequently agreeing to broadcast the FIFA 21 Global Series via its OTT platform, aiding visibility in the UK to attract new and existing fans.

The pipeline of talent into the sector will also be key, with some universities and colleges in the UK now offering esports-related degrees to support the creation of careers in the industry, these courses vary from esports production, coaching & performance, events management and business management.

This, combined with the efforts by not-for-profit national bodies such as the British esports Association and esports teams such as Gfinity through its Challenger and Elite Series, are enabling the grassroots development of esports.

A relatively more mature audience presents monetisation opportunities

The UK esports sector has opportunities to improve upon the current proportion (20%) of its audience that have purchased esports-related products and services, with 83% of 16 to 65 year olds (including students and those who are retired) employed with a relatively high net average monthly salary of 2,846€.

An interesting demographic profile has developed within UK esports, with strong interest from Millennial and Gen X consumers (70%), as well as an above-average female audience (43%) which underpins the diverse economic opportunities available.

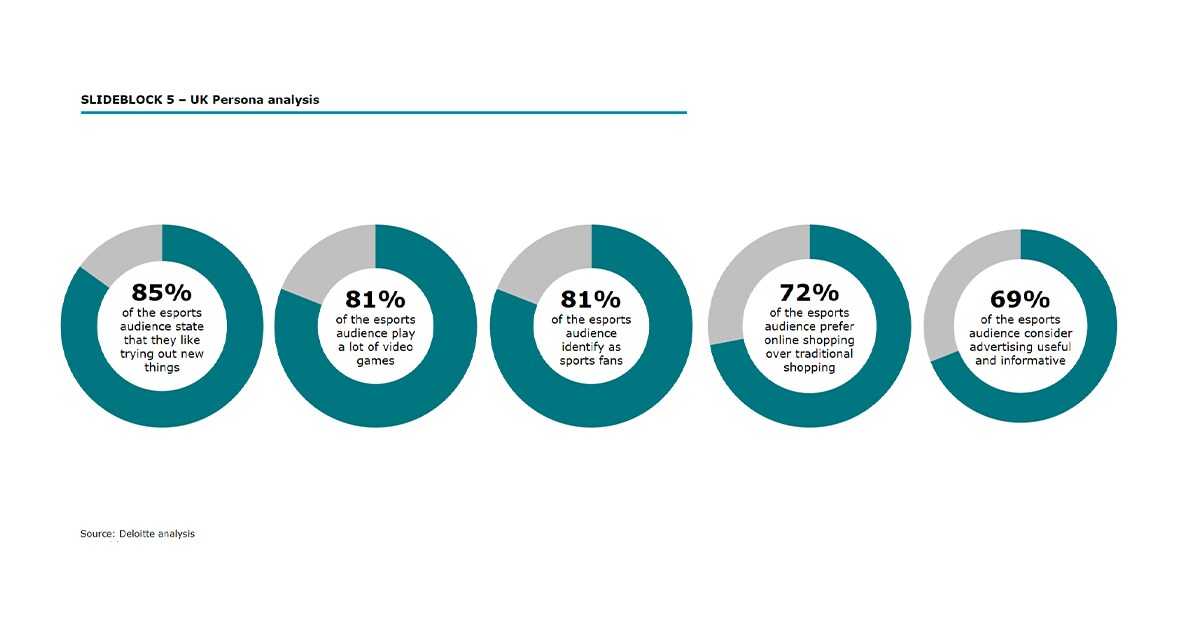

Commercially (as seen with the recent Crypto.com and Fnatic partnership), there are also considerable commercial opportunities for brands and teams to engage with each other and the esports community – the majority of fans enjoy shopping (83%) and trying new things (85%), while 69% find advertisements informative, providing further rationale for brand collaborations.

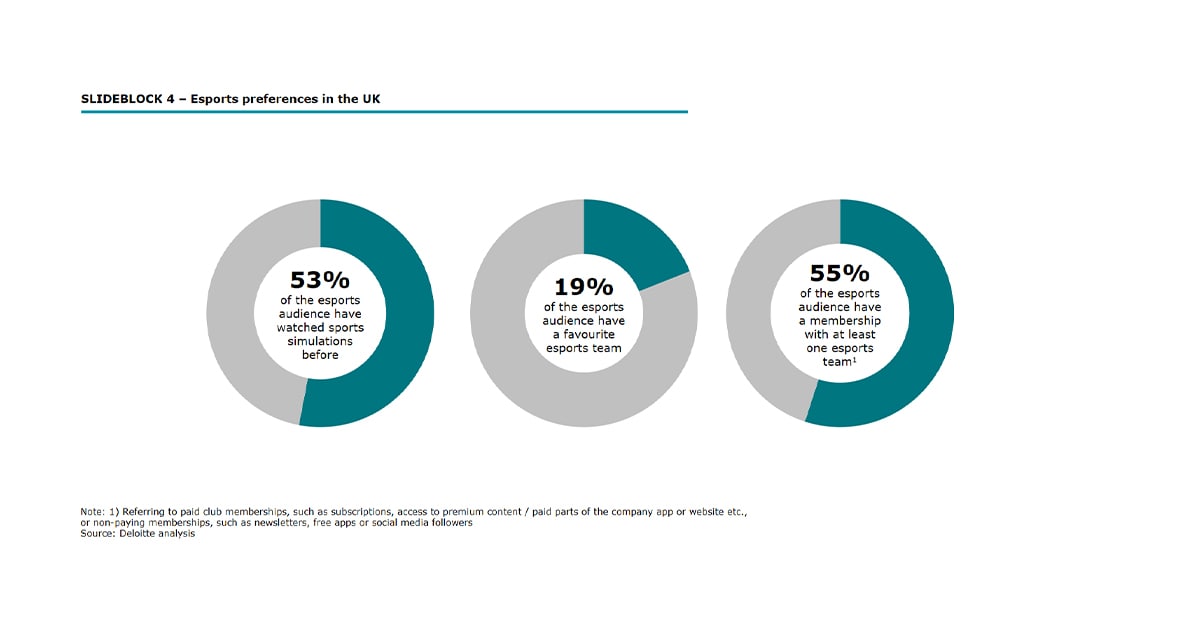

The interaction with traditional sports deserves attention, with four-fifths (81%) of esports fans identifying as sports fans, while sports simulations have the greatest reach among the esports audience (53%) and spend 36% of their passive esports consumption time on games in this category.

The UK reboot following COVID-19 is gathering momentum

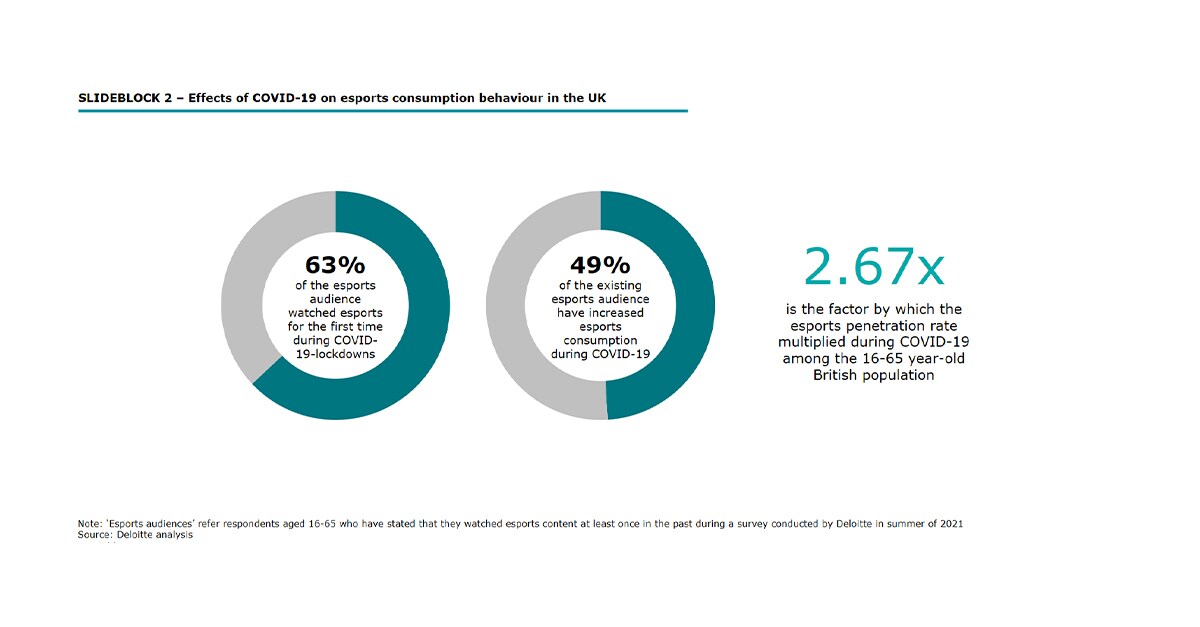

COVID-19 has significantly impacted UK esports, and while damaging in many respects, has created new opportunities. The inability to host in-person events has constrained growth, however on a more positive note, there has been growth in esports awareness and consumption in 2020. 63% of consumers consumed esports content for the first time during COVID-19 and 49% of existing consumers increased esports consumption in 2020.

Nevertheless, this growth has not directly led to revenue growth in 2020 - Gfinity recorded a 43% revenue reduction in 2020 for example. Continuing with Gfinity, esports teams have been responsive to changing market conditions, with Gfinity significantly cutting costs (by c.50%) to reduce losses from its 2019 levels, with new innovations (such as its digital media arm) helping forge a path to targeted profitability in the future.

The growing audience, professionalisation and innovation among esports teams has helped increase corporate and investor confidence and interest in the UK (as seen by the previous examples on this page), with many appearing optimistic about the future growth potential of the UK esports sector.

Let's Play! 2021

The European esports market

The European esports market

The 6th edition of the Deloitte study 'Let's Play! - The European esports market' focuses on the economically sustainable development of the European esports sector. The study was based on extensive consumer research and numerous expert opinions. In addition, there are 13 country profiles that outline the current state of the esports sector in different European markets.

Please find the full report here. For the individual country profiles, navigate via the map of Europe.

Deloitte offering and country contacts

The Sports Business Group at Deloitte is the Go-to-partner for stakeholders of the esports industry and organisations seeking to join the ecosystem at every stage of their esports ventures – from building market knowledge to advising on complex matters with a particular focus on commercial, financial and investment topics.

With over 25 years of experience in the national and international sports, fitness and esports industry, our work draws on Deloitte’s global network. It combines expertise in auditing, tax and legal, financial and risk advisory, and consulting with the industry expertise of the Sports Business Group. This multidisciplinary approach combined with digital competence in all areas enables us to tailor our work specifically to the needs of our clients.

Recommendations

Thriving in a privacy-centric ad sales ecosystem

Lessons from conversations with leading European publishers and broadcasters

News in a digital age

Modern times, an ancient problem...