{kind=link}

{kind=link}

{kind=link}

Brazil economic outlook, February 2023 has been saved

Cover image by: Jaime Austin

Brazil successfully cut inflation by more than half between June and December of last year, thanks to hawkish monetary policy. High commodity prices, ample external demand, and fiscal expansion flattered growth last year. As the global economy slows dramatically this year, Brazil will likely follow suit. Relatively tight monetary policy and uncertainty around fiscal policy will add to economic headwinds. As of January 13, markets expected real GDP growth to slip from about 3% in 2022 to below 1% in 2023.1 However, external demand for Brazil’s goods has held up better than it has for its peers. China’s reopening and a strong soybean crop should likely help to prevent Brazil from falling into a recession this year.

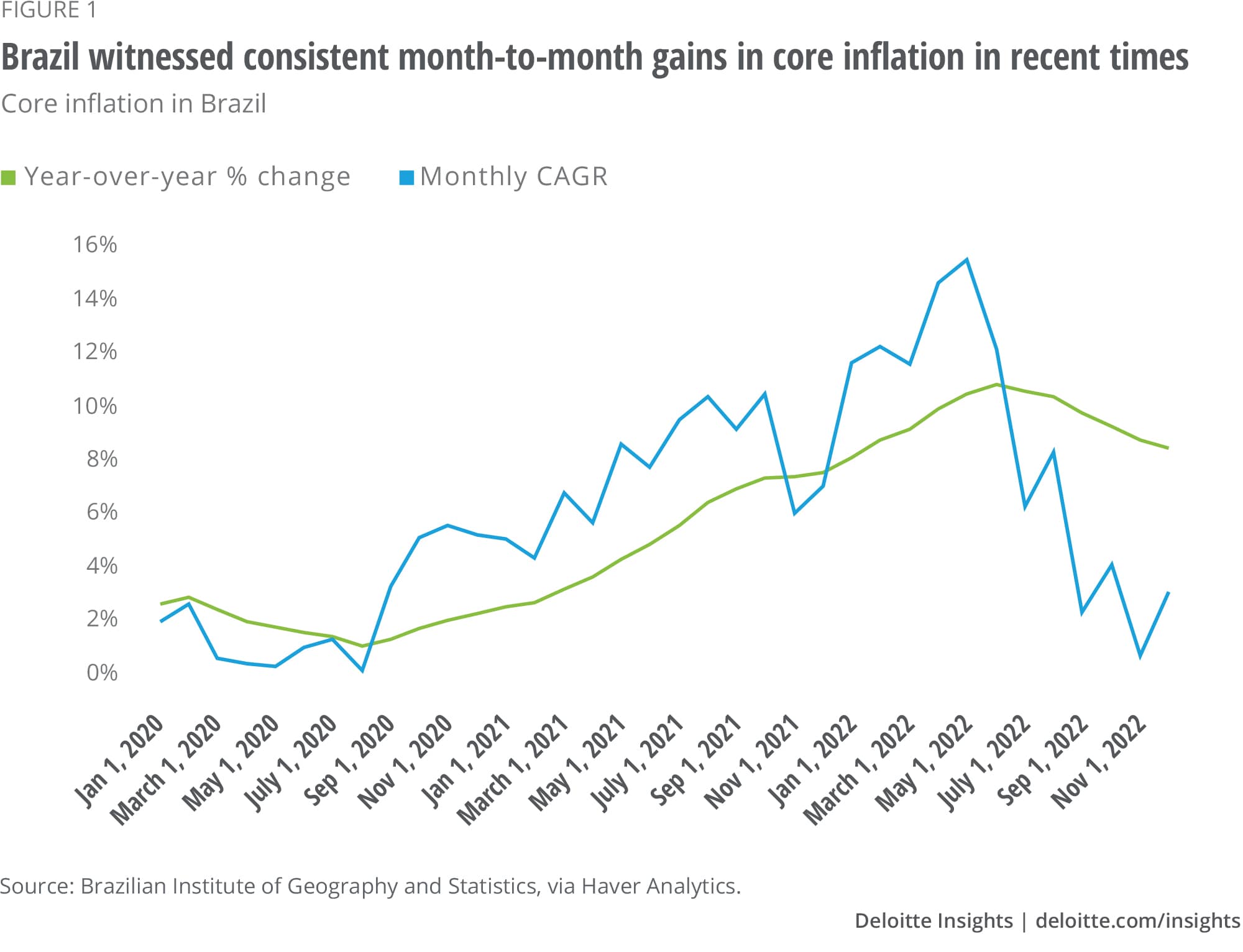

Headline inflation in Brazil was just 5.8% year over year in December, down from 12.2% the previous April.2 Falling energy prices have provided substantial support to pushing inflation lower. Fuels and energy prices were down 12.9% year over year, while residential electricity prices dropped 19% over the same period. Despite the fall in overall inflation, some goods are still seeing rapid price gains. Food and beverage prices, for example, were up 11.6% year over year, while the cost of personal care products and clothing was growing by double digits. Core inflation, which excludes volatile food and energy components, was still up a lofty 8.4% year over year in December. Fortunately, the last four month-to-month gains in core inflation were consistent with just 2.5% annual growth (figure 1), suggesting that the year-ago growth rate should come down soon.3

The Banco Central do Brasil (BCB) responded relatively early and aggressively to quell inflation, raising interest rates from 2% in February 2021 to 13.75% by August 2022.4 With inflationary pressures waning, the BCB should be able to lower interest rates from here. Doing so would alleviate some of the pressures refinancing costs are contributing to the government deficit. However, there are several risks lurking that could fan the inflationary flames, including fiscal policy, China’s reopening, and strong wage growth. Indeed, the BCB noted at its December meeting that it would not hesitate to raise rates to combat higher inflation, warning the incoming government administration over loose fiscal policy.5 The BCB is understandably concerned about elevated inflation expectations considering consumers expect inflation to average 8.8% over the next 12 months.6

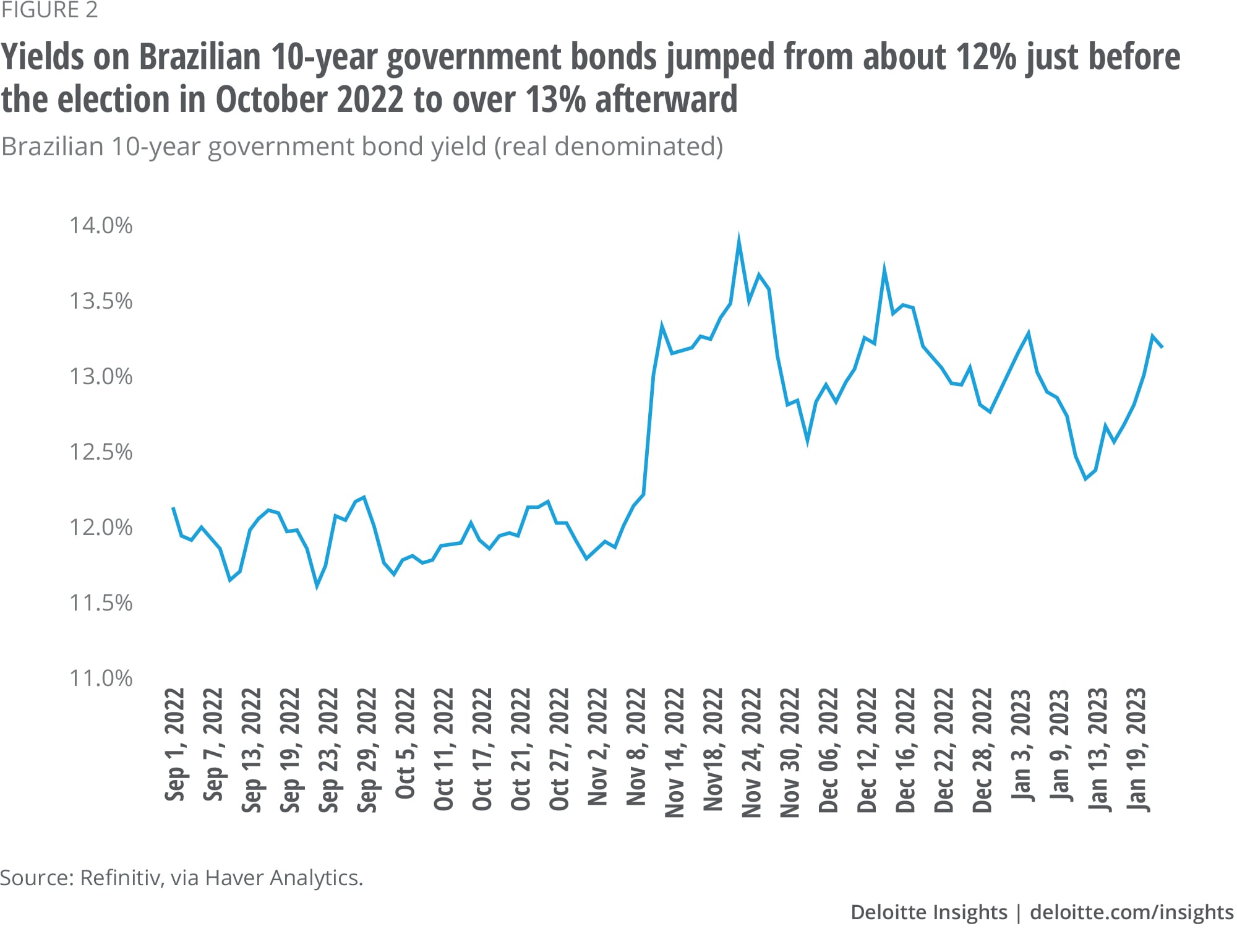

Perhaps the biggest risk to inflation is fiscal spending. Pandemic-related spending plus stimulus ahead of last year’s elections weakened Brazil’s fiscal position. More recently, Congress approved 168 billion reais in additional spending this year, which is expected to widen the primary deficit (i.e., the balance excluding interest payments) to nearly 2% of GDP.7 The newly appointed finance minister has promised to replace the fiscal cap with a new fiscal anchor by April to keep spending from getting out of hand.8 However, financial markets have their doubts and are concerned that the incoming administration’s plans will balloon government spending relative to the size of the economy. For example, yields on 10-year government bonds jumped from about 12% just before the election to over 13% afterward. As of January 24, yields remained above 13% (figure 2).9

Recent government stimulus included fuel tax relief, which has helped to bring headline inflation down. However, that relief is set to expire by March,10 which will force fuel prices higher, making inflation look considerably worse than it does now. This puts the government in an uncomfortable position. Removing the fuel-tax subsidies would help shore up beleaguered government finances, but it will also raise energy costs, which risks raising input costs and driving inflation expectations higher. Plus, this comes as poverty and food insecurity in Brazil have been trending higher.11 Even if government support doesn’t expire, fuel prices may rise again anyway. The International Energy Agency expects oil demand to outstrip supply this year, which would push prices higher.12 China’s reopening is expected to support excess demand, while sanctions on Russia should limit the supply of oil available to get to market.

Labor-market tightness and the strong wage growth that has come with it could also fuel more inflation. Nominal wage growth was up 14% year over year in November, while inflation-adjusted wage growth was up 7.2%.13 Such strong growth in labor costs is inconsistent with inflation coming down to the central bank’s target of 3%. Productivity growth could help alleviate some of these higher wage costs, but unfortunately, numerous structural issues have caused productivity to decline,14 which pushes unit labor costs ever higher. 15

On the positive side, there may be some relief to wage growth in the near term. Although the unemployment rate hit its lowest level since 2015, employment growth has clearly slowed.16 Total employment was virtually unchanged in November relative to October 2022.

The global economic slowdown has weighed on the export outlook across most countries. Supply chain issues have mostly been resolved, companies have restored their inventories, and the United States and much of Europe could be headed for recession this year. All of this points to reduced demand for goods globally. Across most emerging market economies, goods exports slowed rapidly at the end of 2022.

In Brazil, the export slowdown has been less pronounced. For example, goods export growth accelerated by 5.5 percentage points in Q4 relative to Q3.17 Even so, export growth has likely peaked (figure 3). In December, exports were the weakest they had been since the previous January. Durable consumption goods and intermediate goods exports were lower in December relative to a year earlier. Agricultural exports were up 23.8% from a year earlier in December, but that is less than a third of the growth rate seen just two months prior. On the positive side, exports of mining products and transportation equipment posted sharper increases at the end of last year.18

Although the global economic outlook for this year clouds the export picture, there are a few reasons to be somewhat optimistic about Brazil’s exporting prospects. First, Brazil’s soybean harvest is expected to be a record one this year.19 As the world’s largest soybean producer, Brazil could see a substantial upside to exports as a result. Some of this bumper crop may ultimately be used by domestic producers to make oils, which have experienced a jump in price due to the lack of available alternatives such as sunflower oil out of Ukraine. However, soybean oils are likely to be exported as well.

China’s reopening should also have a positive effect on Brazil’s export position as demand in China rebounds this year. China is Brazil’s largest export market and the largest buyer of Brazil’s soybeans. Plus, China has reduced the volume of soybeans it imports from the United States, diverting demand to Brazil’s producers. China’s reopening has also supported global commodity prices. For example, soybean prices have rallied nearly 10% between the beginning of October and January 20.20

While agricultural and some metals exports could hold up reasonably well this year, the manufacturing sector otherwise looks less bright. Purchasing managers’ index for Brazil sunk to 44.2 in December, well below a reading of 50—a reading above 50 indicates an expanding sector.21 Manufacturing production managed to eke out a 1.3% year-ago gain in November, but capacity utilization has been sliding since early 2021.22 Domestic demand has also clearly shifted lower. Inflation-adjusted retail sales were just 1.5% higher than a year ago, less than half the rate of growth seen as recently as September.23 Rapidly rising food prices and the prospect of higher fuel costs will weigh further on consumer spending, especially as wage growth comes down.

There’s little doubt that Brazil’s economy is slowing. Tight monetary policy and a rapidly rising cost of living are restraining domestic demand. Policymakers’ desire to provide support to those who are struggling needs to be balanced with enough restraint to keep inflation from worsening. That balance will largely dictate Brazil’s economic trajectory over this year and the next. At the same time, weakening global demand is expected to hold back export growth, though China’s reopening and a strong soybean yield will likely offset some of that weakness.

Central Bank of Brazil, Focus–market readout, accessed February 7, 2023.

View in ArticleBrazilian Institute of Geography and Statistics, via Haver Analytics.

View in ArticleIbid.

View in ArticleCentral Bank of Brazil, Haver Analytics.

View in ArticleMaria Eloisa Capurro, “Brazil holds key rate at 13.75% as Lula’s spending plan adds to inflation risk,” Bloomberg, December 8, 2022.

View in ArticleGetulio Vargas Foundation, via Haver Analytics.

View in ArticleWalter Brandimarte, “President Lula’s Brazil budget math doesn’t add up for investors,” Bloomberg, January 13, 2023.

View in ArticleIbid.

View in ArticleRefinitiv, via Haver Analytics.

View in ArticleReuters, “Lula decrees extension for tax exemption on fuels in Brazil,” January 2, 2023.

View in ArticleGisella Vieira, “Going hungry in Brazil,” Wilson Center, August 5, 2022.

View in ArticleInternational Energy Agency, Oil market report—January 2023, January 2023.

View in ArticleBrazilian Institute of Geography and Statistics, via Haver Analytics.

View in ArticleThe World Bank, “The World Bank in Brazil,” October 7, 2022.

View in Articleibid.

View in ArticleIbid.

View in ArticleMinistry of Development, Industry, Commerce and Services Brazil, via Haver Analytics.

View in ArticleIbid.

View in ArticleJohn Reidy, “Brazil on track for record soybean crop,” WorldGrain, January 12, 2023.

View in ArticleRefinitiv, via Haver Analytics.

View in ArticleS&P Global, via Haver Analytics.

View in ArticleBrazilian Institute of Geography and Statistics and National Confederation of Industry Brazil, via Haver Analytics.

View in ArticleBrazilian Institute of Geography and Statistics, via Haver Analytics.

View in ArticleCover image by: Jaime Austin