{kind=link}

{kind=link}

Is the world really going through some great rethink? has been saved

The authors would like to thank Marcello Gasdia for his contribution to this article.

Cover image by: Sylvia Yoon Chang

Record numbers of people are quitting their jobs.1 Big cities are losing residents.2 Few are jumping at the idea of returning to the office full-time.3 Recent headlines continue to highlight large swathes of people collectively making some big life choices. It’s difficult to imagine the collective experience of the last year and a half not having something to do with it.

While some temporary lifestyle shifts were a necessary part of navigating the pandemic, we wanted to better understand how people are changing in more meaningful ways that may stick in the long term. As part of a longitudinal consumer study, we surveyed more than 20,000 people across 23 countries about how they feel their priorities have shifted over the past year.4 Priorities focused on areas that help get behind some of current headlines we’re seeing today—exploring shifting sentiment around work, purpose, money, how and where we spend our time, and more.

For consumer businesses, understanding these priority shifts is important. Our findings suggest priorities are not only shifting, but in some cases, these shifts are influencing what and how we buy.

In this article, we explore findings for the United States. For a look at global insights across 23 countries, head to our State of the Consumer Tracker dashboard.

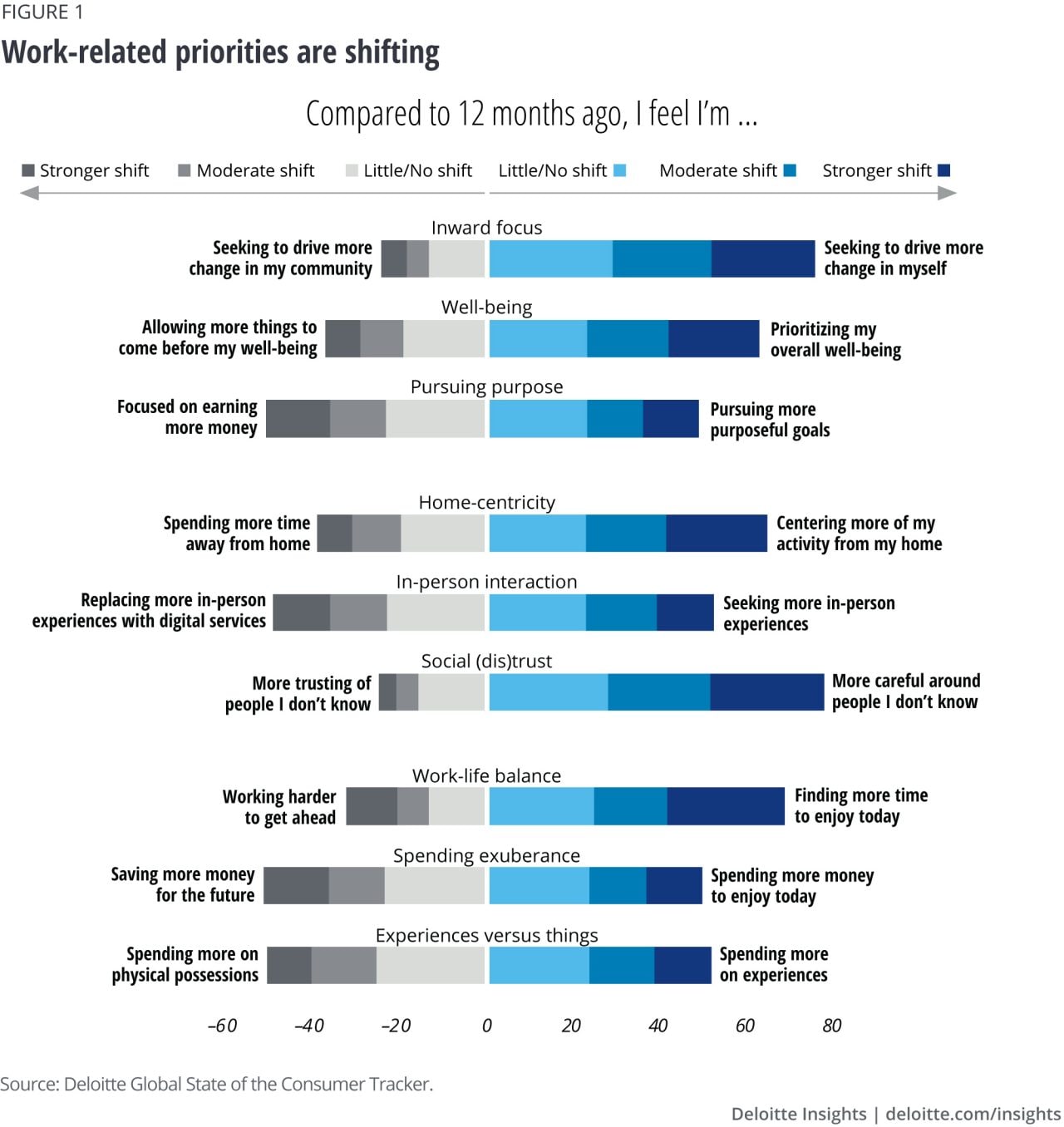

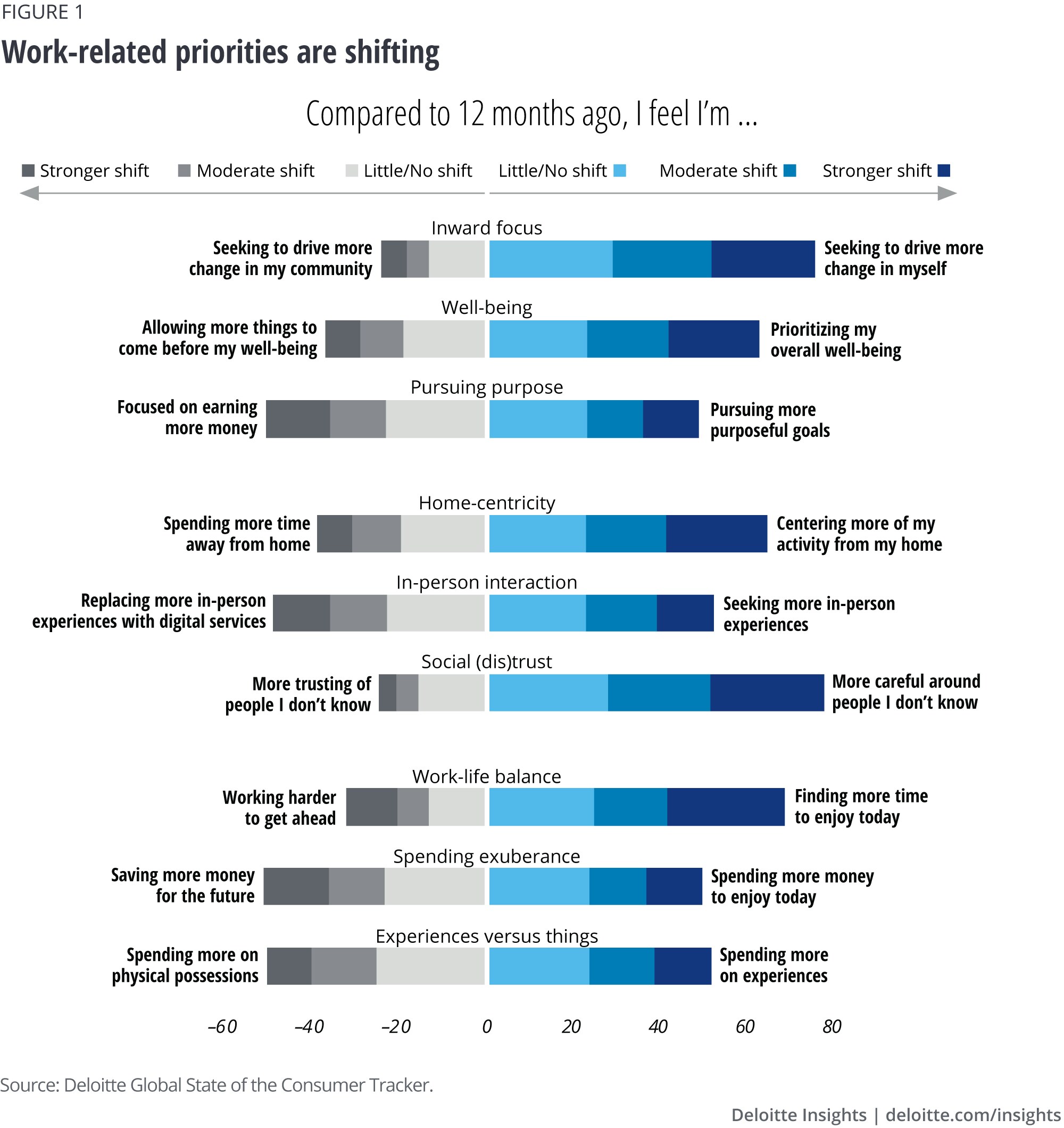

When asked to reflect on the past year, the overwhelming majority of Americans feel they’re more focused on personal change (figure 1). This introspective shift—a precursor to personal change—is among the strongest shifts we measured and gives us a peek into the general mindset of Americans. Data reveals that people more focused on change are likely to contemplate how life could improve … and they’re also more likely to act. People who measured high in seeking personal change were also more likely to cite a shift in other priorities—particularly around areas like work/life balance.

Some interesting dynamics are playing out around priorities related to work. Roughly one in four Americans feel they’re pursuing more purposeful goals rather than focusing on earning more (figure 1).5 Nearly double that number (44%) cite finding more time to enjoy today rather than working harder to get ahead.

Overall, this is a healthy proportion of people choosing meaning and time over work and money—particularly considering the financial challenges many faced throughout the pandemic, sunsetting stimulus programs, and rising prices for everyday purchases.

But perhaps more interesting is not how many people are rethinking things like work and earning more—but who these people are. Income plays a big role. Higher earners are significantly more likely to deprioritize earning more and working harder (figure 2). In parallel with headlines around the “Great Resignation,” these priority shifts continue to lend some credence to the notion that the pandemic induced a bit of an existential rethink around work. But while these shifts were measured across all income bands, they were much more likely to occur among those who can afford it, i.e., the higher-income group.

More importantly, even when controlling for age, income, and employment status, those 44% of Americans prioritizing free time over working harder plan to spend money differently. Over the next month, they intend to spend roughly 1.7 times more on recreation and entertainment, 1.6 times more on restaurants, and 1.2 times more on leisure travel compared to those prioritizing working harder.

Even with more people beginning to put the pandemic days behind them, 40% of Americans still feel they’re centering more of their daily life around the home compared to one year ago (figure 1). In comparison, only 19% feel they’re spending more time away from home.

Work from home naturally plays a big role here—particularly in the United States. Deloitte’s State of the Consumer Survey data reveals that at an average of 3.5 days per week, Americans are working from home significantly more than other countries. And if Americans have their way, the trend likely won’t be short lived. Americans able to do their jobs from home would prefer to stay at home most of the week (4.1 days)—but only if their employer allowed it. Additionally, strong work-from-home preferences are not being driven by more temporary safety concerns6—clearly suggesting a more permanent shift.

The strength of the shift toward home-centricity—in both the number of people experiencing it and the likely permanence of the trend—brings several implications for the consumer industry. Spending more time at home influences spending behavior in more ways than one. From a category perspective, home-centricity significantly impacts two of the 15 categories we tested—housing and restaurants. Over the next four weeks, those spending more time at home plan to spend 1.2 times more on housing—including rent and mortgage, as well as on buckets like maintenance, renovations, and utilities—and 2.6 times less on restaurants—compared to those spending more time away from home.

More time at home also means more online shopping instead of going to the store. When controlling for factors, such as age and income that typically influence digital behaviors, those spending more time at home plan to purchase a significantly larger share of their groceries, clothing, and electronics online. Similar to home-centricity, those who feel they’re living a more virtual life have a higher propensity to buy online.

While Americans might feel their daily lives have become more home-centric—the inherently social side of people is still shining through the data. Compared to 12 months ago, approximately one in four (29%) feel they are seeking more in-person interaction—almost equaling those who feel they’re replacing more in-person interaction with digital services (26%). The emergence of two distinct groups—one seeking in-person interaction and the other replacing it—is an interesting finding in itself. Watching which way the trend leans in the coming months can provide insight into the pandemic’s long-term impact on digital behavior. Overall, perception of pandemic safety is still among the strongest predictors of what side of the divide people fall.

On the back of a pandemic that created unprecedented financial challenges for many, the United States is virtually split down the middle in terms of the number of people prioritizing saving for the future (28%) versus those prioritizing spending for today (26%, figure 1).

As most would expect, income plays a role (figure 2). But, surprisingly, safety perceptions are an even more powerful predictor. The less people are concerned about pandemic safety, the more likely they are to prioritize spending over saving.

The collective experience of the past year and a half has clearly activated a moment of reflection for many. We’re seeing clear preference for more home-centric daily lives, which is potentially shifting some more spending toward the home and online for some major categories, including grocery, clothing, and electronics. At the same time, more people feel they’re living more to enjoy today rather than working harder to get ahead—a sentiment with clear correlations to higher spending intentions in areas such as recreation and entertainment, leisure travel, and restaurants.

As more people reevaluate what a better life might mean, consumer businesses will increasingly serve customers whose lifestyles and buying behaviors are realigning to their evolving priorities or values. Consumer businesses should proactively consider how their organizations can be more purpose-driven in ways that meet customers and employees alike on where their values and priorities are.

The authors would like to thank Marcello Gasdia for his contribution to this article.

Cover image by: Sylvia Yoon Chang