{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

European consumers after the pandemic has been saved

The authors would like to thank Julius Elting and Anna Seidel of Deloitte Germany, and Tom Simmons of Deloitte UK for their contributions to this article.

Cover image by: Victoria Lee.

Germany

United Kingdom

United Kingdom

Germany

The European economy suffered a lot in 2020: two waves of COVID-19 infections, a high death toll and two lockdowns in most countries. The consequent economic recession was the deepest on record. While most of Europe is currently in the second lockdown, vaccination programmes are making progress, providing much-needed hope. The question of what will follow the recession is becoming crucial for companies. What is clear is that consumer expenditure – the largest component of gross domestic product and its main growth driver in recent years – will determine to a large degree how Europe emerges from the recession and what sort of recovery we get.

The calculation is difficult because this is a special recession. What makes it unique is that it was driven by the closure of whole sectors, ranging from international airlines to the local hairdresser. Consumer-facing service industries were worst affected by the effort to combat the virus.

The consequence for executives in the consumer goods and retail industries is that they should not expect the recovery to follow the ‘normal’ post-recession pattern. The range of possible developments is much wider than usual and hinges on completely different factors, such as the speed of vaccination campaigns and the potential unleashing of pent-up demand.

To understand how European consumers might emerge from the crisis, it is crucial to understand how the recession differs from previous ones, how policymakers’ choices are affecting consumers and what scenarios are possible going forward.

During recessions consumers tend to keep their wallets tightly closed, which results in an increase in savings. However, the slowdown in spending does not affect all consumption categories equally. Durable items, such as cars, consumer electronics, jewellery, lawn and garden equipment, sporting goods and washing machines tended to be the most volatile in terms of demand in previous recessions. Spending on these items is likely to be postponed until after the economy recovers. During the global financial crisis, for example, the revenue generated in the automotive sector fell by more than 20 per cent. Demand for non-durable (short-lived) consumer goods and services, on the other hand, is usually more stable as these categories include spending on food and housing.

But the level of consumer expenditure is not easy to predict and does not follow simple patterns. Of course the financial position of households plays a critical role, but it is not the only factor. The future expectations of consumers are equally important, although much harder to measure. An actual severe loss of income or an anticipated one will certainly influence spending, but in economic terms, what matters most are the prospects of consumers once the economy turns up.

The development of consumer expenditure in Germany in previous recessions illustrates this point. The recession experienced after the global financial crisis was by far the deepest in the post-war period. Gross domestic product fell by almost six per cent. Previously, it had never fallen by more than one per cent.1 Nevertheless, consumption attained pre-recession levels after only six quarters. After a much milder downturn in 1981, consumption took almost as long to recover.2

The longest slump in consumer spending in Germany occurred in the global slowdown that followed the bursting of the so-called dot-com bubble in US stock markets in 2000 and the 9/11 terrorist attack. Although the German economy did not fall into recession technically and still grew weakly during the subsequent global economic slump, it took more than three years for consumption to return to previous levels. The main factor was the persistently poor labour market. Consumers needed to recoup income lost during the tough economic period before they regained the confidence to spend more freely. It is not the severity of the recession that shapes spending patterns; it is how consumers assess their financial future, with the labour market they anticipate playing an important role.

In recent years, private consumption has driven growth in the Eurozone. True, the Eurozone is an export-driven economy, and the share of exports in its GDP is much higher than in the United States or in China. But world trade largely stagnated after the financial crisis and corporate investment grew very sluggishly, while labour markets performed well, driving consumer expenditure. Between 2014 and 2019, private consumption showed pretty solid growth rates (figure 1).

This of course immediately changed when the COVID-19 crisis struck. Private consumption contracted by 8.6 per cent in 2020. A contraction on this scale is unprecedented. In 2009, at the peak of the recession caused by the global financial crisis, the contraction amounted to a comparatively tiny 1.4 per cent.

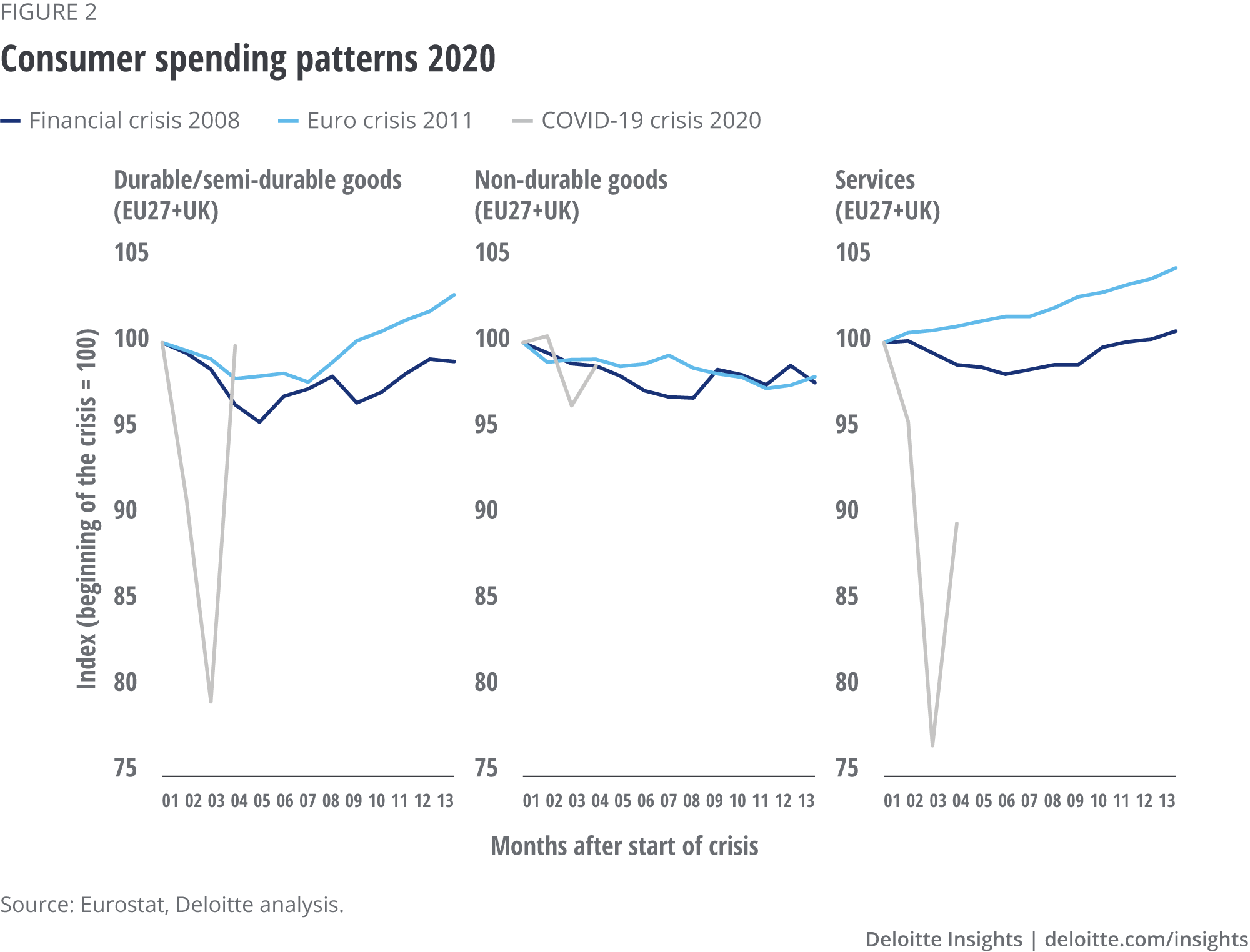

Looking below the headline figures shows that the patterns we have seen in previous recessions are not of much help when trying to understand the current one. Consumer behaviour during the COVID-19 crisis does not match these templates (figure 2). In fact, consumers behaved in the opposite way. After the initial wave of lockdowns in Europe, spending on consumer durables recovered extremely quickly, yet based on past recessions it would be expected that durable goods would experience the harshest effects and would rebound only after the recession was over.

By comparison, in the COVID-19 recession, non-durable goods contracted, though not dramatically, and began to recover very quickly. For services, the picture looks completely different. They fell further than durable goods in the first phase of the recession and could not recoup their losses. The reason is pretty clear. Government interventions required large parts of the Eurozone’s services sector to close completely. The unusual, swift recovery in durable goods also reflects government interventions through a set of policies that have insulated consumers from the most extreme effects.

The extent to which the COVID-19 crisis affected consumption across countries, therefore, stems from the difference in consumption structures. While in the UK, for example, 21 per cent of consumer spending is spent on so-called socially consumed services, such as meals out, leisure activities and holidays – the areas most affected by lockdown measures – in Germany, this share represents only around 16 per cent. The fall in UK consumption was consequently more severe compared to Germany.

Disposable income in the European Union and United Kingdom fell substantially during the initial outbreak of the COVID-19 crisis in the first quarter of 2020 but recovered in the following quarters. This was thanks to unprecedented fiscal, monetary and labour market measures implemented by governments to limit the impact of the novel coronavirus on the economy.

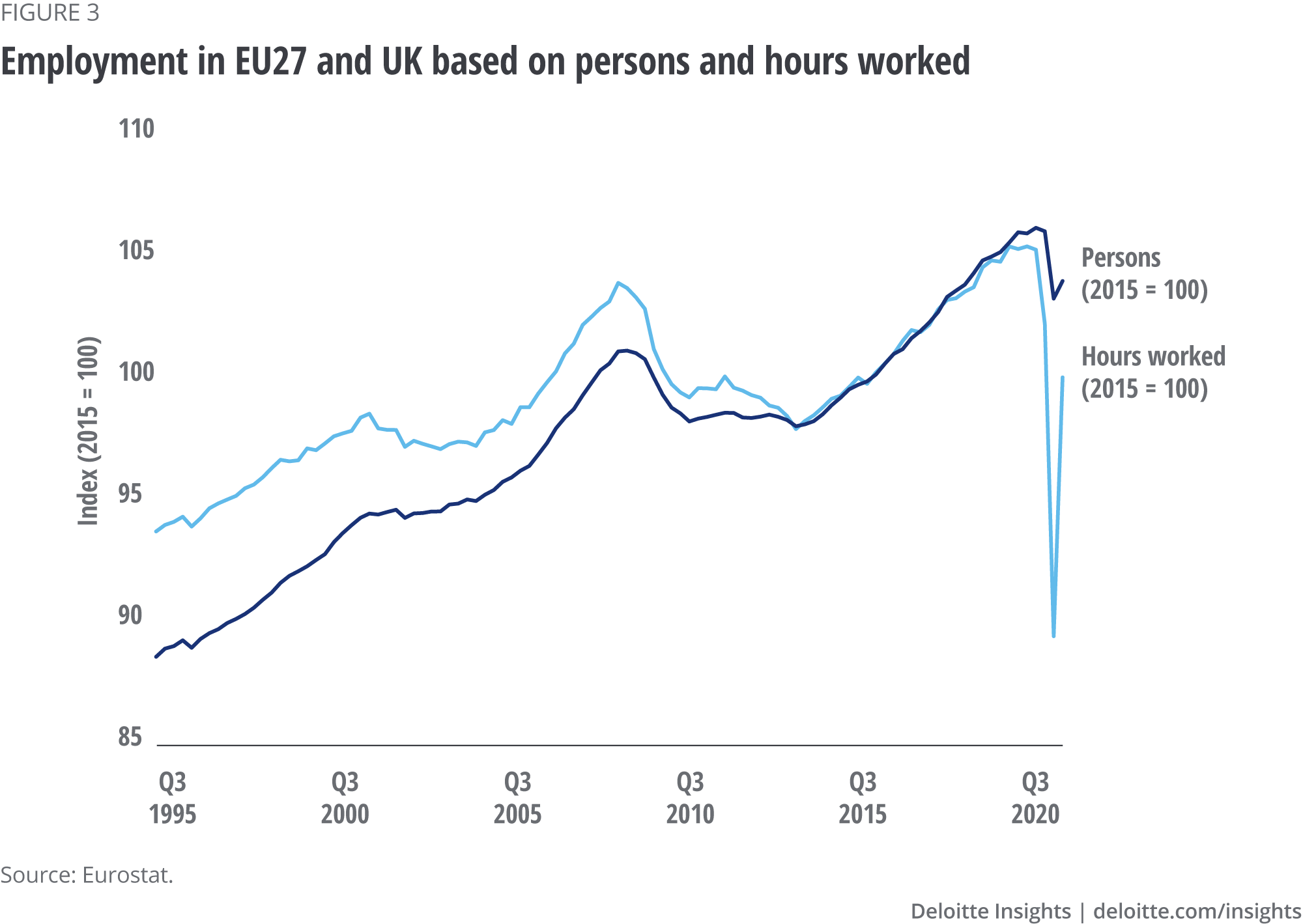

One of the key measures used to stabilise European labour markets was the introduction of short-term work or furlough schemes. These schemes were intended to protect the labour market, covering the cost of workers with government money so that employers dealing with the downturn did not have to sack them. In this way, employees could be compensated for lost income by government transfers and keep their jobs, which might otherwise have been lost, and recovery once economies reopened could be seamless. According to the European Central Bank, the five largest European countries (France, Germany, Italy, Spain and the UK) used these schemes in a big way. In France and Italy, 40 per cent of employees were in furlough schemes last summer. In Germany and Spain, the share was smaller, though still substantial at 20 per cent; while in the UK, 30 per cent of employees were in furlough schemes at the peak of the crisis.3

Employment data reveals how these schemes affected the labour market. While European employment based on hours worked declined by 15 per cent in the second quarter of 2020 compared to the fourth quarter of 2019, employment based on persons working decreased by only 3 per cent (figure 3). This means employees remained in work but worked substantially fewer hours. There was only a slight uptick in unemployment.

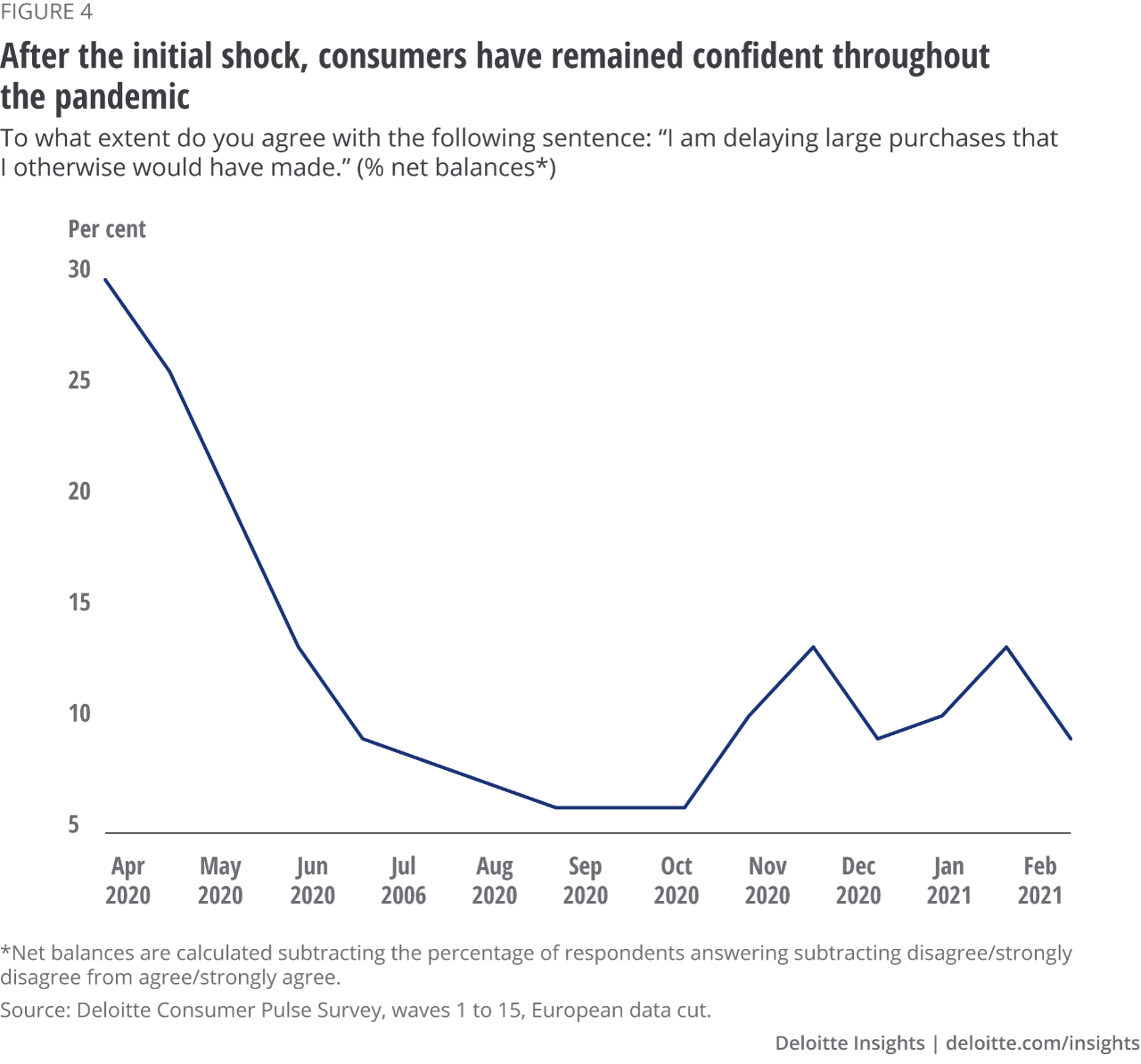

Government interventions designed to protect jobs and businesses also are having an impact on consumption as consumers across Europe remain surprisingly optimistic with regards to their personal finances. Consumers’ propensity to make large purchases is a good indicator of consumer sentiment. At the start of the pandemic, consumers delaying large purchases outweighed those who continued to make them, resulting in a positive net balance of 29 per cent. However, the net balance fell quickly during summer 2020 and into the autumn, following the evolution of the epidemiological curve. The second wave and subsequent lockdowns affected confidence but not to the same extent as the first wave – with the net balance in November 2020 less than half that recorded in April 2020 when uncertainty with regards to the pandemic and its economic impact made consumers more cautious (figure 4).

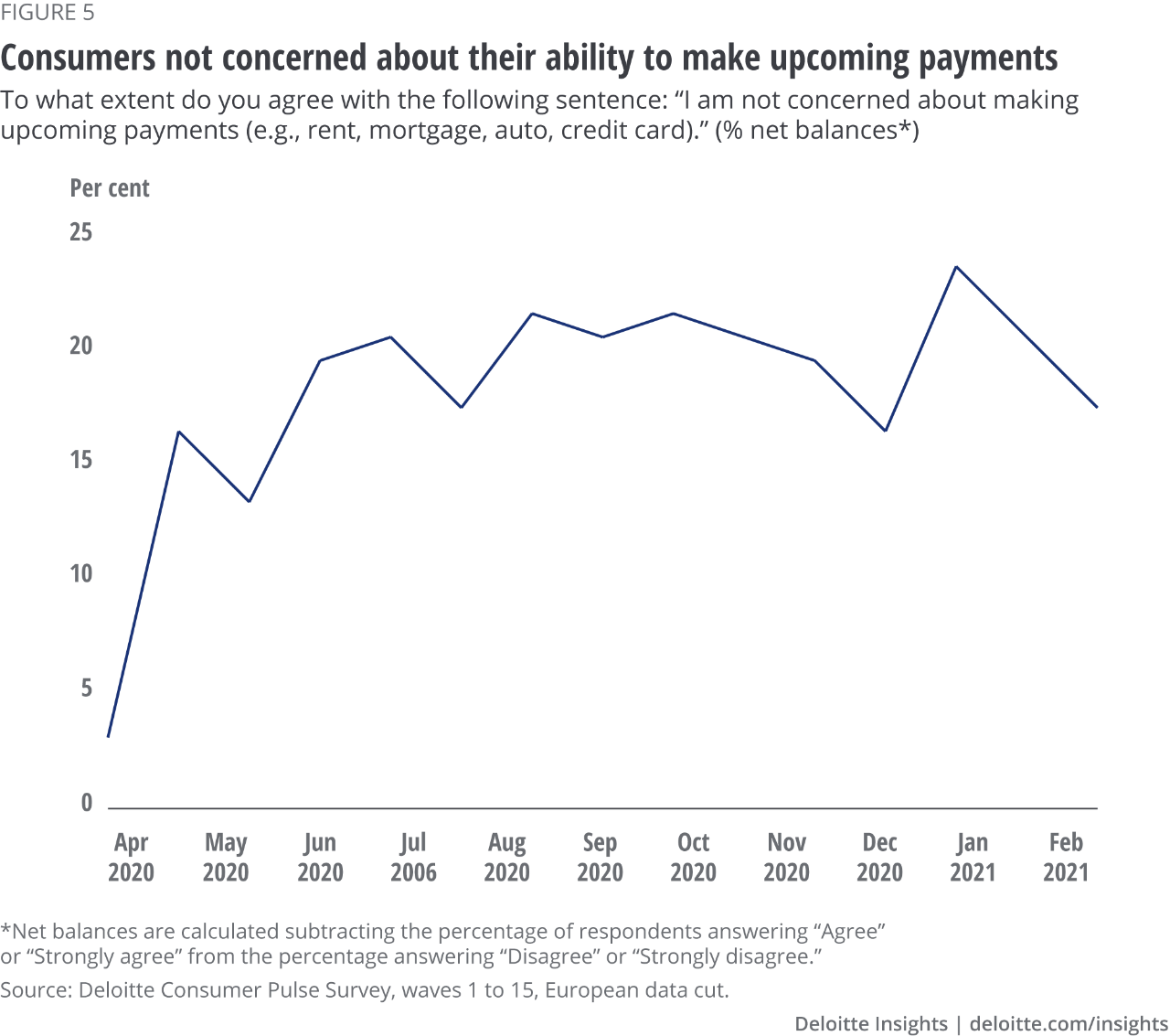

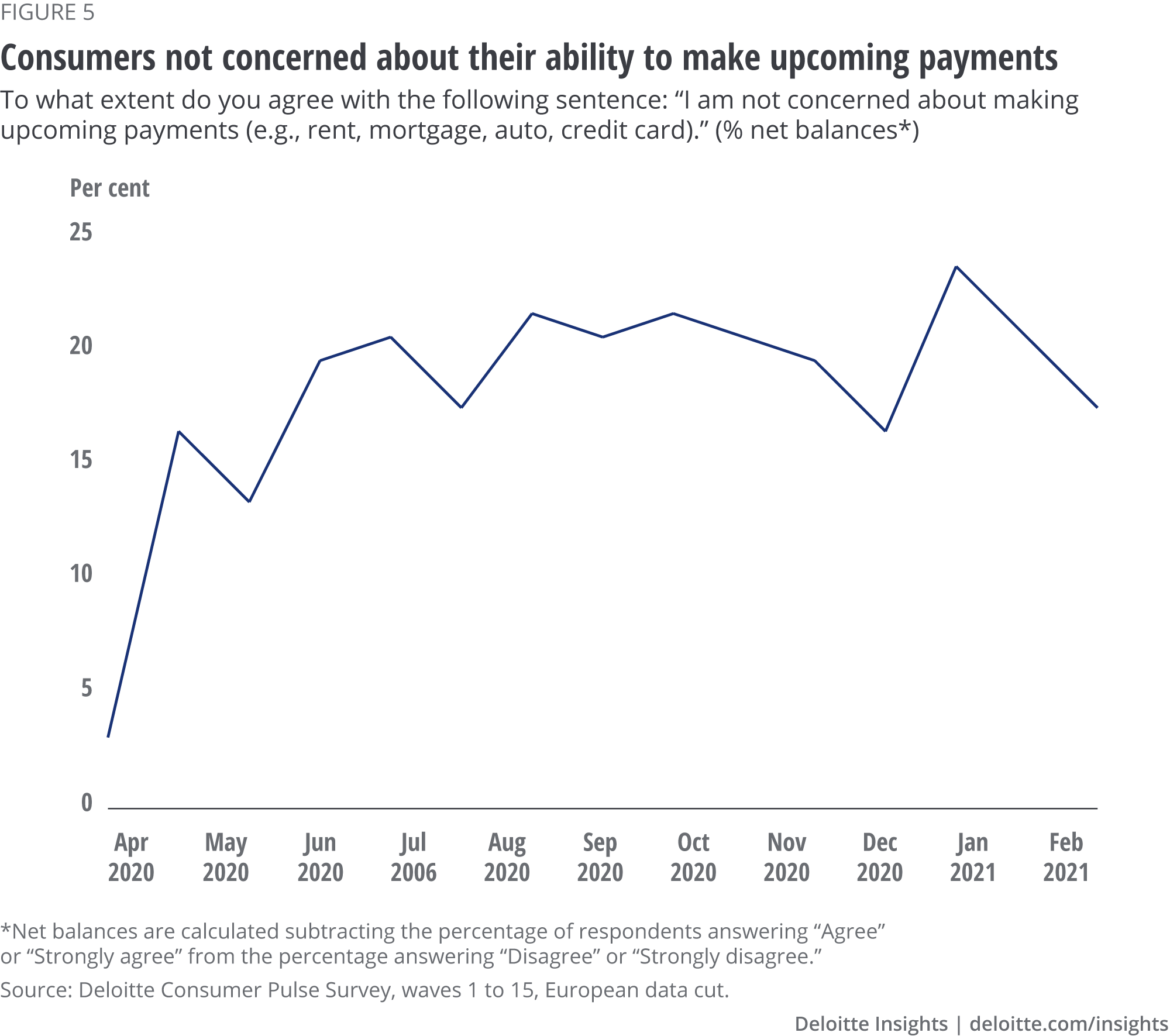

The extent to which government support programmes are helping maintain the status quo in the consumer sector is further highlighted by consumers’ confidence in their disposable income. The share of people who are unconcerned about being able to make upcoming payments exceeds the share of people who are concerned – the net balance is, therefore, negative and has been since April 2020 (figure 5). The COVID-19 global pandemic has proved to be a dual-front crisis, with health concerns consistently outweighing financial concerns. In fact, consumer finances have held up remarkably well, with fewer than one out of five respondents reporting that their total household spending exceeds their current income.

The second and very welcome effect of the major government policy response has been the stabilisation of disposable income. For the Eurozone and the UK, as a whole, disposable income fell by around 3 per cent in the second quarter – much less than the GDP contraction of more than 13 per cent – and it recovered pretty quickly afterwards.

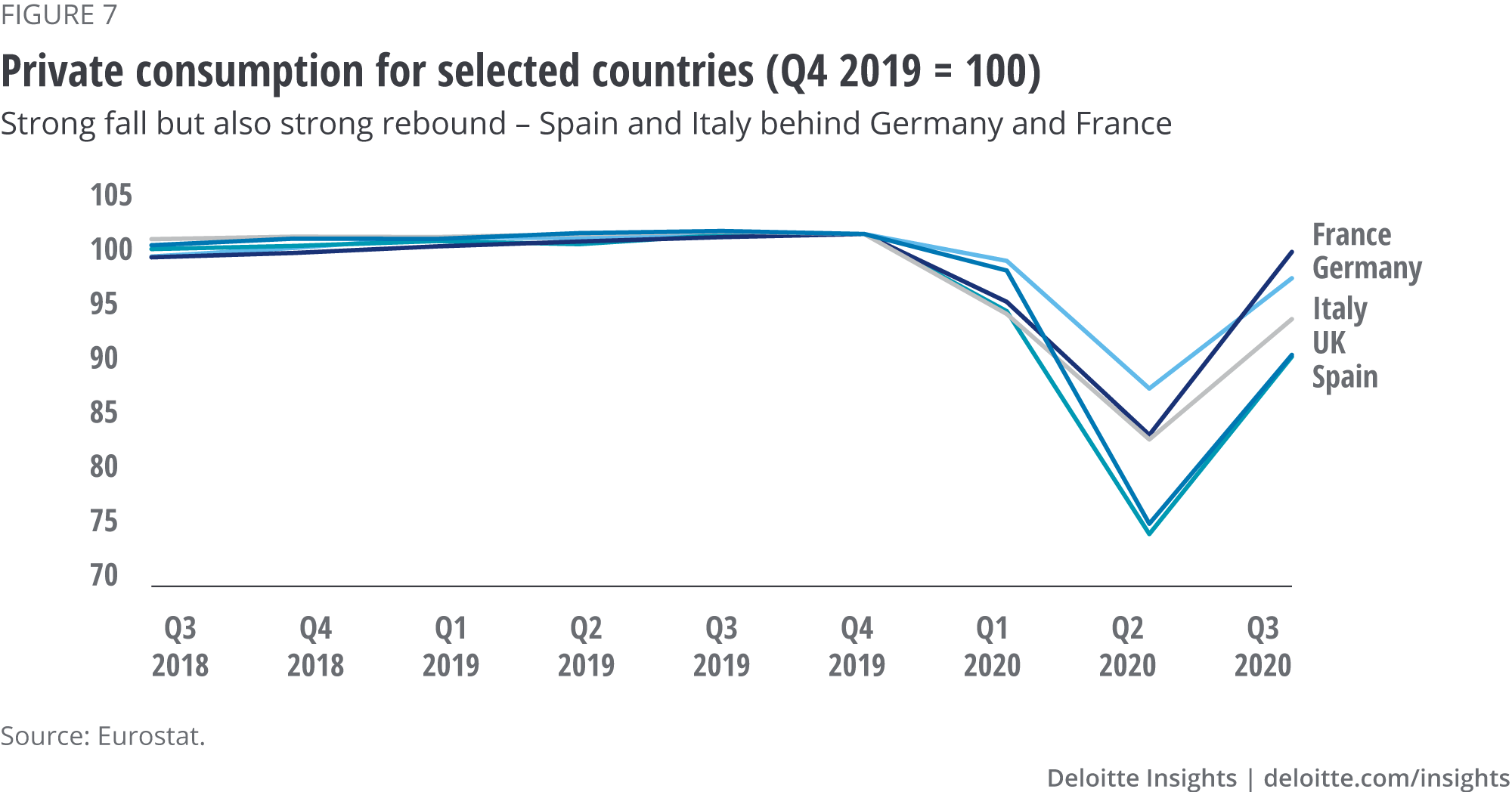

Of course, there are differences between European economies depending on the depth of the national crisis in terms of both the pandemic and the economy. Italy, Spain and the United Kingdom were heavily affected, while France and Germany saw rapid recoveries in consumption. But nonetheless, as a whole, the European recovery set in quickly.

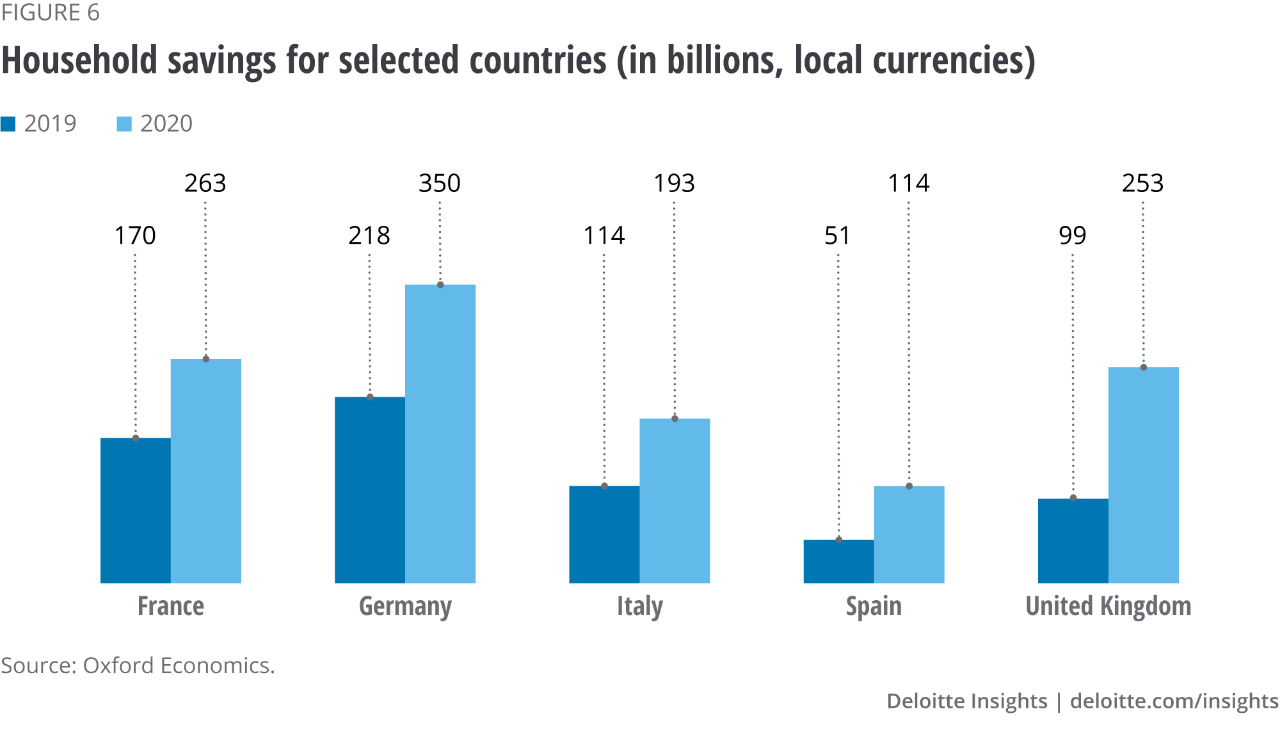

An important side effect emerges from these trends. Lockdowns coupled with stable income meant that consumers could not spend as they normally would due to limited opportunities – except online. Therefore, the savings rate exploded. It doubled to 25 per cent of disposable income in Q2 2020 compared to Q4 2019 (figure 6). Precautionary motives certainly play a role in this unprecedented increase, but it can be safely assumed that a good part of it reflects involuntary saving.

This assumption is backed by empirical evidence. A survey conducted by the German Central Bank in August after the first lockdown suggests that the two most important reasons for reduced consumer expenditure were that many goods and services were not available and that some spending, such as on commuting to work, was no longer necessary. Reduced income or the fear of reduced income in the future was much less important.4

In other words, European consumers are sitting on a mountain of spare cash that they would have spent if they had the opportunity to do so. The amount is impressive. If we make a reasonable assumption of a savings rate of 19 per cent for the whole of 2020, Eurozone consumers would have saved around 450 billion Euros more in 2020 than in 2019 – the equivalent of around 7 per cent of total consumer spending in 2019. On a country level, excess savings per capita compared to 2019 range from 1,300 Euro in Spain to more than 2,000 Pounds in the United Kingdom. These savings could play an important role in the recovery. The use of only parts of them could provide a substantial boost to consumer spending in 2021 and in following years. Therefore, how, when and how fast this money is spent will be crucial factors for the recovery.

It cannot be predicted with certainty how consumers will behave after the immediate health crisis is over and the normal pattern of consumer spending is possible. The crucial factors will be the successful and rapid roll-out of vaccinations and consumers’ financial position and feeling about their finances, which will influence their spending of disposable income.

The economic factors will depend on the ramifications of the crisis – in economics jargon, the so-called scarring. If many people have lost their jobs and companies have gone out of business, household finances and consumer sentiment will be depressed. However, the experience after the first wave of infections and lockdowns provides some hope in this respect. Consumption rebounded very quickly in Q3 2020, indicating that consumers were happy to open their wallets again (figure 7). Scarring after the first wave did not emerge to a noticeable degree, even if some consumption, such as restaurant visits, clearly could not be recovered. In China, which largely succeeded in preventing a second wave of infections, demand – especially for services – picked up quickly after containment measures had been lifted, bringing consumer spending to pre-crisis levels already at the end of last year.

History, too, provides some hopeful signs for the recovery. After the SARS epidemic in Hong Kong the economy rebounded sharply. The economy had dipped markedly in Q2 2003 and recovered strongly in Q3 2003 as tourists and visitors from the Chinese mainland flooded back. Consumer fears evaporated once the virus was under control, and their spending recovered quickly.5 Although SARS was much less severe than COVID-19 and did not create a supply shock, its example shows that consumer confidence can rapidly rebound after an epidemic.

There are historians who see a more general pattern. Niall Ferguson, the Milbank Family Senior Fellow at the Hoover Institution at Stanford University, believes COVID-19 could be history by the end of 2021 and forgotten soon after, as pandemics tend to disappear quickly from public awareness.6 He argues that the 1957–58 pandemic, known as the Asian flu, is broadly comparable to the COVID-19 crisis and is barely remembered today. Other academics, such as Nouriel Roubini, Professor of Economics and International Business at New York University Stern School of Business, however, fear that the COVID-19 crisis could trigger a storm of financial, political, socioeconomic, and environmental risks, provoking a depression in the current decade.

Deloitte’s Global Consumer Tracker survey results reveal clear differences between younger and older consumers. Throughout the pandemic, younger demographics (not only those aged 18 to 34, but also those aged 35 to 54) have been more likely to delay large purchases. They have been much more concerned than older (55+) respondents about their ability to make upcoming payments and about losing their jobs (figure 8). Younger consumers are more likely to work in the industries most affected by COVID-19, such as retail and hospitality, often in low-paid roles. They also are more likely to have lower levels of savings and fewer assets and are therefore more exposed to the financial impacts of the pandemic. The 35-to-54 age group faces a different set of challenges, with many having mortgages to pay and families to provide for, and so while they may earn higher salaries they often also have higher levels of expenditure.

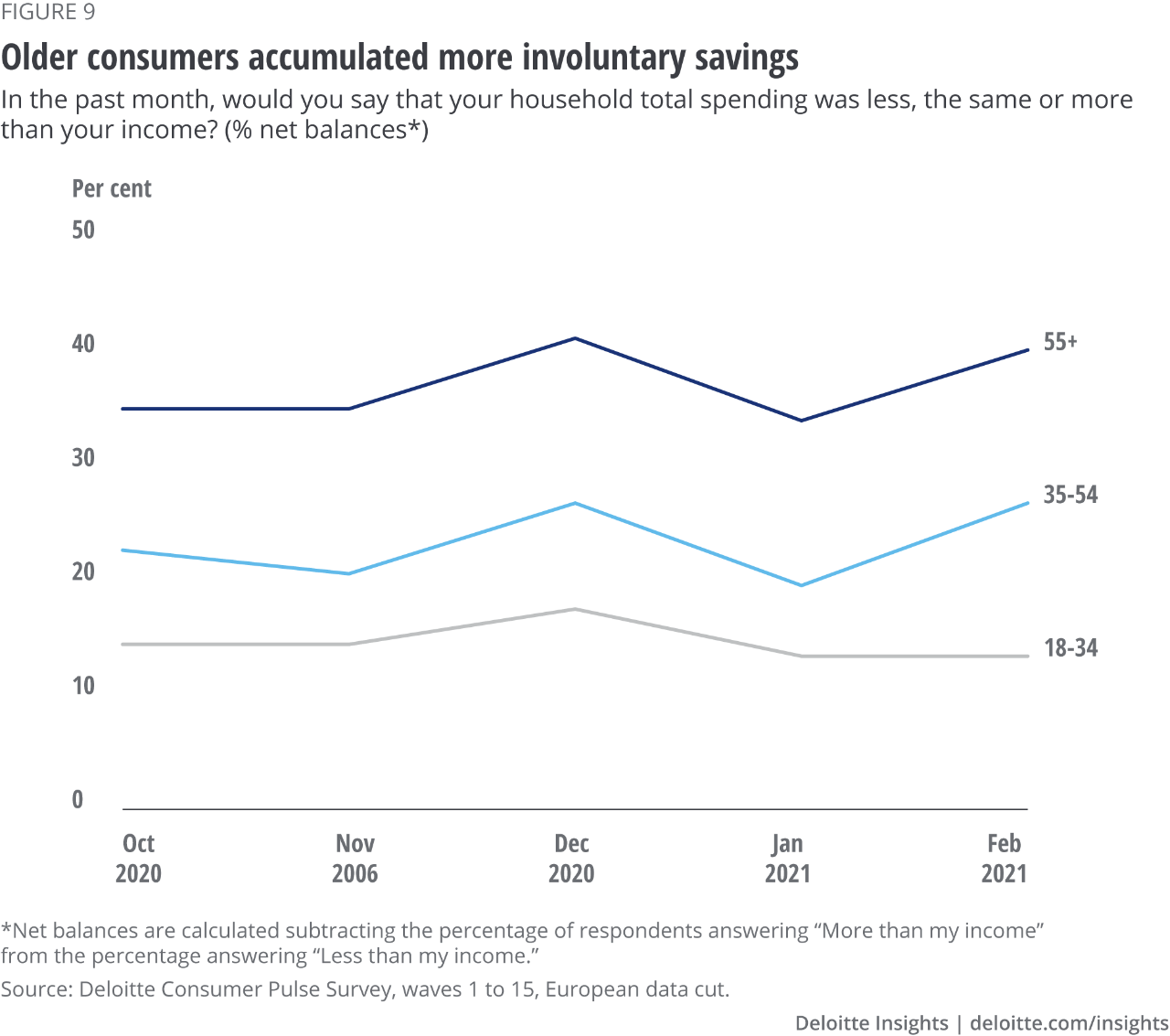

An implication of this squeeze on younger consumers is that they have been less likely to accumulate “involuntary” savings. In the latest wave of the survey, the net balance of respondents reporting to be spending less than their income is 39 per cent among those aged 55+, but only 13 per cent among respondents aged 18 to 34 (figure 9).

The pandemic seems then to be having a deeper impact on the finances and confidence of younger consumers – who would normally be among the first to resume travelling, eating out and socialising. Labour market conditions across the EU also may have negative implications for the ability of younger consumers to spend in the medium and long term. Given the effects on their confidence and the challenging outlook, any recovery in consumer spending is likely to be unevenly distributed, and therefore, businesses catering to returning younger consumers will need to consider what they can do to help them.

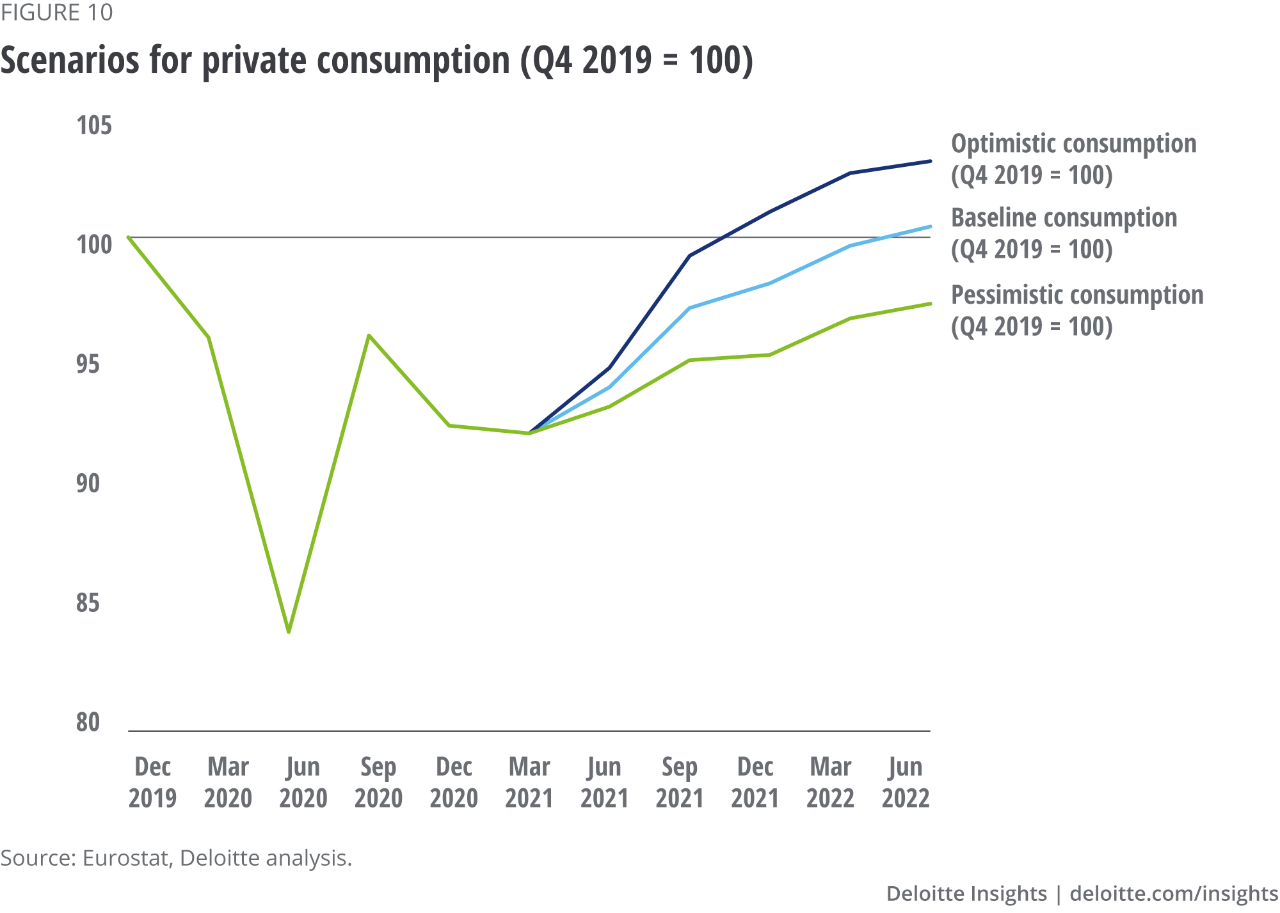

Limiting the time horizon to the more immediate future, three scenarios for consumer expenditure in the Eurozone are conceivable (figure 10). They hinge on the success and speed of vaccination campaigns as well as on the post-pandemic condition of consumers in Europe.

Baseline: The good – a return to pre-crisis levels of consumption by Q2 2022

Consensus forecasts expect economic uncertainty to linger and COVID-19 restrictions to be extended well into the first quarter of 2021, stalling recovery in the Eurozone. An easing of lockdown restrictions in the spring and summer will support a rebound in consumption, particularly for services. This rebound will be partly offset by rising unemployment as policies supporting the labour market are wound down. Deloitte Research expects that the pre-crisis level of GDP will not be reached until the second quarter of 2022. While consumer sentiment and spending may recover in this scenario, they may do so cautiously and in spurts as people wait to see what happens in the labour market, as well as the economic policy reactions and COVID-19 crisis management. Moreover, the rapid recovery in durable goods suggests that some of the demand in this category was front-loaded and its role as a driver of demand will possibly be muted compared to previous recoveries. However, the more confident consumers become that the crisis is over, the faster consumption may rebound. On the basis of the current parameters, a moderate recovery in consumption seems plausible in the second quarter of 2021, accelerating in the third quarter.

The ugly – a return to pre-crisis levels of consumption by Q2 2023

In the case that vaccines do not prove particularly effective and COVID-19 outbreaks continue to flare, then disruptive stop-and-go lockdowns may remain a feature of society for the future. This would be an extremely negative scenario, especially when coupled with the eventual withdrawal of the expensive furlough subsidies. Any surge in unemployment may deal a severe blow to families’ finances, forcing them to save whenever possible and therefore dampening demand. Economic recovery towards pre-crisis GDP levels would then be a long and arduous process given the harm done to both the labour market and household income. This recovery would look more look like an L or a W than a U or a V.

The very good – a return to pre-crisis levels of consumption by Q4 2021

Some countries have proven that a quick vaccination roll-out is possible. At the time of this writing, nearly one-third of the UK population has been vaccinated. If vaccines begin to be distributed more quickly in other European countries and labour markets continue to come through the crisis relatively unscathed, then governments could end lockdown restrictions earlier than planned and wind back the various job protection schemes without too much disruption. This could encourage consumers to spend the large amount of money saved during the crisis. A release of pent-up demand could lead to a virtuous circle in which increasing demand continues to improve the business climate to the point that corporate investments are again stimulated. A sharp rebound in consumer demand may, however, lead to a temporary spike in inflation. In the most extreme form of this positive scenario, we could experience another Roaring Twenties, a decade of economic growth and prosperity that followed the end of the First World War and the receding of the Spanish flu.

Which scenario is more likely, and how can retail and consumer goods executives prepare? All three scenarios are plausible, but the baseline scenario seems the most likely at the time of this writing. Given the many uncertainties and risks, the more extreme scenarios should be included in strategic planning. Consumer-facing businesses should thoroughly analyse how dependent their business is on the business cycle. There are huge differences in the position of, for example, groceries, tourism and e-commerce in the current crisis. This exercise should be done also on a country level, as it is likely that the speed and depth of the recovery will differ substantially between European countries. Finally, it can be helpful to look at the more extreme scenarios to generate strategic options. How to cope with a continued recession is the most daunting possibility. More enjoyable is to consider how to meet explosive demand should European consumers unload their excess savings quickly.

The authors would like to thank Julius Elting and Anna Seidel of Deloitte Germany, and Tom Simmons of Deloitte UK for their contributions to this article.

Cover image by: Victoria Lee.