{kind=link}

Measuring semiconductors’ economic impact in a smarter world has been saved

Cover image by: Viktor Koen

The rise of smart devices, cars, and pretty much everything else has been great for the semiconductor industry: In 2020, global sales rose 6.6% to US$440 billion1 even as global GDP shrank 3.5%.2 Chips are emerging in new places every day, and they’re getting only more ubiquitous.

And the size of the role that semiconductors play in products and operations—and in the global economy in general—is important to leaders across industries. While a chip shortage in 1990 would have affected strictly tech companies, a shortage today would keep a broad range of CEOs up at night. So it’s useful for executives to track how semiconductors are doing.

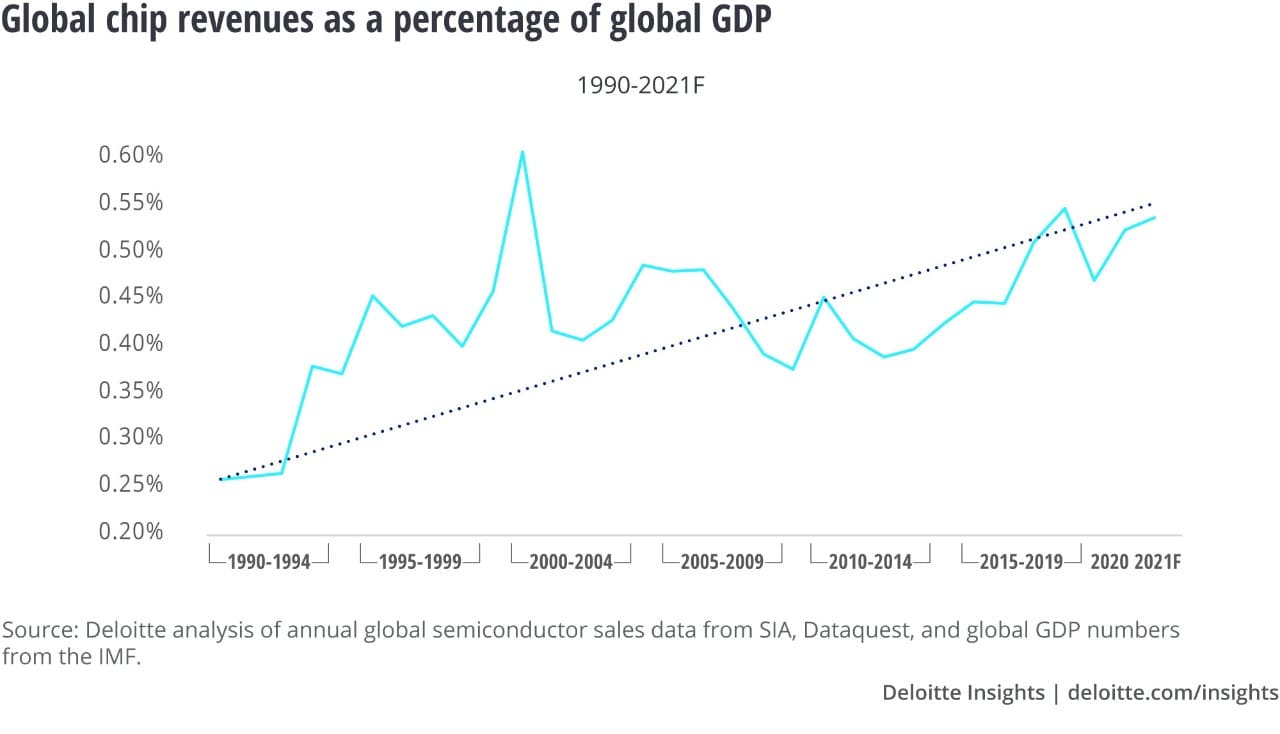

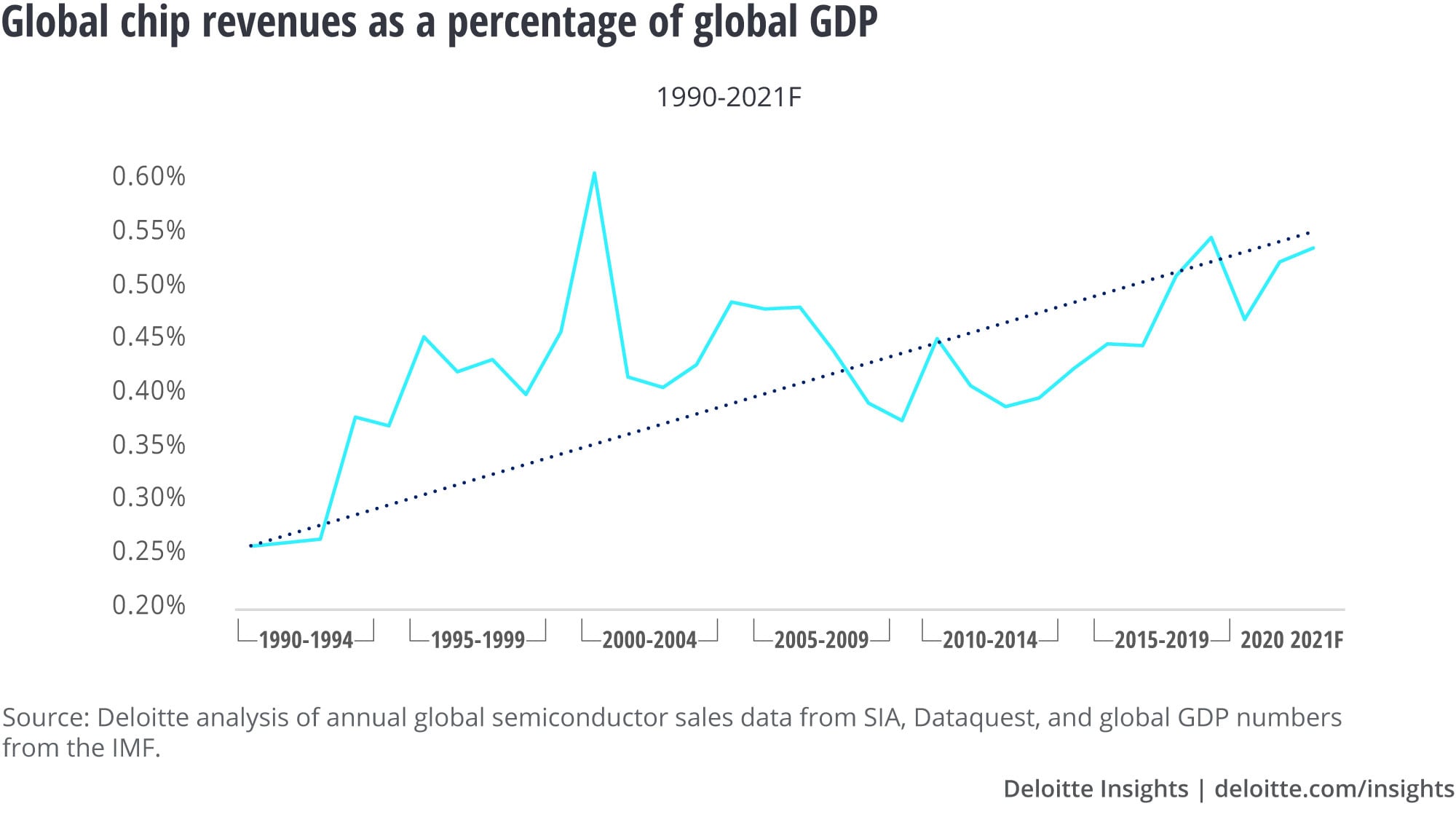

The thing is, trying to assess the industry’s importance at a single point in time is like trying to hang a picture on a boat during a storm: Since 1996, chips have seen annual growth spurts of 35–60% four different times—and 15–50% drops on five different occasions.3 A better gauge of semiconductors’ importance is measuring sales as a percentage of GDP over time, which factors in the effects of inflation, economic growth, and recessions.4

Using this approach, the figure shows global chip revenues doubling in importance over the last three decades, from 0.25% of global GDP to over 0.50% in both 2020 and 2021 forecasted. Although there is some volatility—especially around the 1999/2000 tech bubble—the trendline since 1990 suggests that the industry will continue to grow in importance for the foreseeable future.

Revenue totals don’t take into account the astonishing gains in value/capability per dollar. At the start of 1990, chip memory cost US$100 per megabyte, or about US$200 in 2020 dollars; today, a megabyte costs about $0.003.5 In other words, companies are now spending twice as much on chips as a percentage of global GDP—and getting 66,667 times more capability per dollar.6

No wonder, then, that today chips are essentially everywhere—and everywhere they are essential. Chips themselves may constitute a small percentage of global GDP, but they power trillions of dollars of goods and processes—manufacturers are putting semiconductors in far more than computers, smartphones, and IoT sensors. As of 2020, the average passenger vehicle contained US$475 worth of chips, even more than in a smartphone.7 And that means more reliance: Supply chain issues with semiconductors in early 2021 have shown that a lack of critical chips could lead to a US$61 billion shortfall in global automotive sales this year.8

Supply chain rethink. Though ongoing innovation means that chips get obsolete faster than most other kinds of inventory, leaders at both sellers and buyers of chips may want to rethink keeping just-in-time minimal inventories. Further, in light of recent disruptions—from the COVID-19 pandemic to the Ever Given blocking Suez Canal shipping9—supply chain executives may want to revisit their chip strategy to include sourcing essential chips from half a planet away, considering certain onshore manufacturing even if it means focusing less on cost.

Strategy, high-level. There’s no sign that the trends toward higher spending, more powerful chips, and greater economic multipliers will flatten anytime soon. For companies with products and/or operations dependent on access to chips: Does your firm have—well, perhaps not a chief semiconductor officer, but supply chain visibility with a specific focus on chip supply? At a minimum, leaders should look to incorporate chips and chip issues as part of short-, medium-, and long-term strategy.

Strategy, growth opportunity. Tech companies already consider chips vital, but what about health care, retail, mining, utilities, and manufacturing? Leaders in those industries should look at how greater use of semiconductors might grow their markets—after all, developers are finding fresh applications for chips every day.

Cover image by: Viktor Koen