Economic factors affecting lease accounting & reporting has been saved

Perspectives

Economic factors affecting lease accounting & reporting

On the Radar: A roadmap for ASC 842

Several economic factors have affected the lease accounting for many commercial real estate entities, including owners, operators, and developers. Explore hot topics, common pitfalls, and more information related to why entities that have adopted ASC 842 should continually monitor, evaluate, and update their lease-related accounting and reporting.

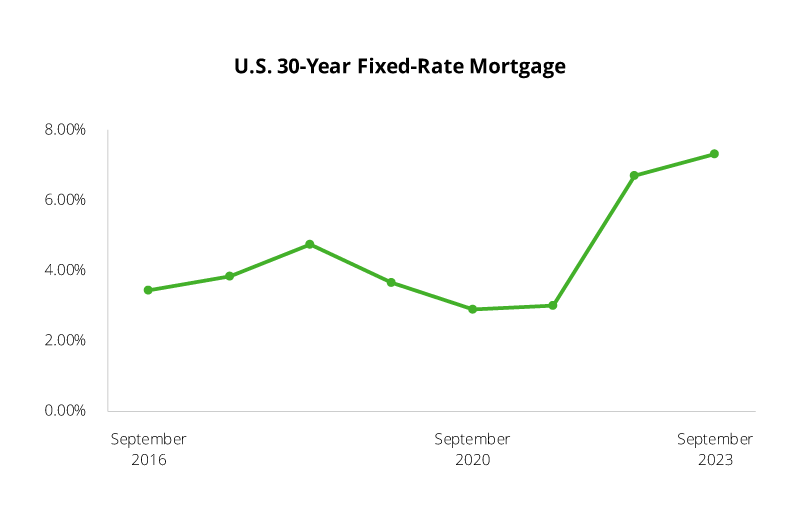

The current macroeconomic environment has created ongoing challenges and uncertainty in various areas ofaccounting, including the accounting for leases. For example, the U.S. 30-year fixed mortgage rate has nearlydoubled since 2016, the year in which ASC 842 was issued.

Source for graphic: Mortgage Rates — Freddie Mac.

Many commercial real estate entities have encountered increased costs of capital and tightening lending standards while also dealing with higher levels of maturing debt; reductions in the volume of real estate transactions; and evolving real estate demands and preferences related to the way people work, live, and shop. The actual impact of the current macroeconomic environment on commercial real estate assets will differ on the basis of various factors, including geographic location, tenant-specific operations, and in-place lease terms. Commercial real estate entities, including real estate owners, operators, and developers, should continually monitor, evaluate, and update their lease-related accounting and reporting.

On the Radar: Leases

Lease accounting hot topics for entities that have adopted ASC 842

Ongoing accounting standard-setting activities

Since the issuance of ASU 2016-02 several years ago, the FASB has released various ASUs to provide additional transition relief and make certain technical corrections and improvements to the standard.

Most recently, in March 2023, the FASB issued ASU 2023-01, which amends certain provisions of ASC 842 that apply to arrangements between related parties under common control. ASU 2023-01 allows non-PBEs, as well as not-for-profit entities that are not conduit bond obligors, to make an accounting policy election of using the written terms and conditions of a common-control arrangement when determining whether a lease exists, as well as the accounting for the lease (including lease classification), on an arrangement-by-arrangement basis. Accordingly, a non-PBE, as well as a not-for-profit entity that is not a conduit bond obligor, that makes this election may not be required to consider the legal enforceability of such written terms and conditions, as described above.

ASU 2023-01 also amends the accounting for leasehold improvements in common-control arrangements for all entities.

The FASB continues to evaluate stakeholder feedback on the adoption of ASC 842. Stay tuned for future refinements in accounting standard setting as a result of these initiatives.

Learn more about lease accounting

ASC 842 offers practical expedients that can be elected by certain entities or in certain arrangements. For a comprehensive discussion of the lease accounting guidance in ASC 842, see Deloitte's Roadmap Leases.

Lease Accounting focus areas—watch the videos

Let's talk!

Learn more about this topic

Get in touch for service offerings

Recommendations

Operationalizing the new lease standard

Lease accounting

New lease standard implementation workshop

Understanding and implementing FASB ASC 842