Canada After a shake, rattle, and stall the economy is poised for modest growth

7 minute read

09 May 2019

While the Canadian economy stalled at the end of 2018, economic growth should continue at a modest pace in 2019.

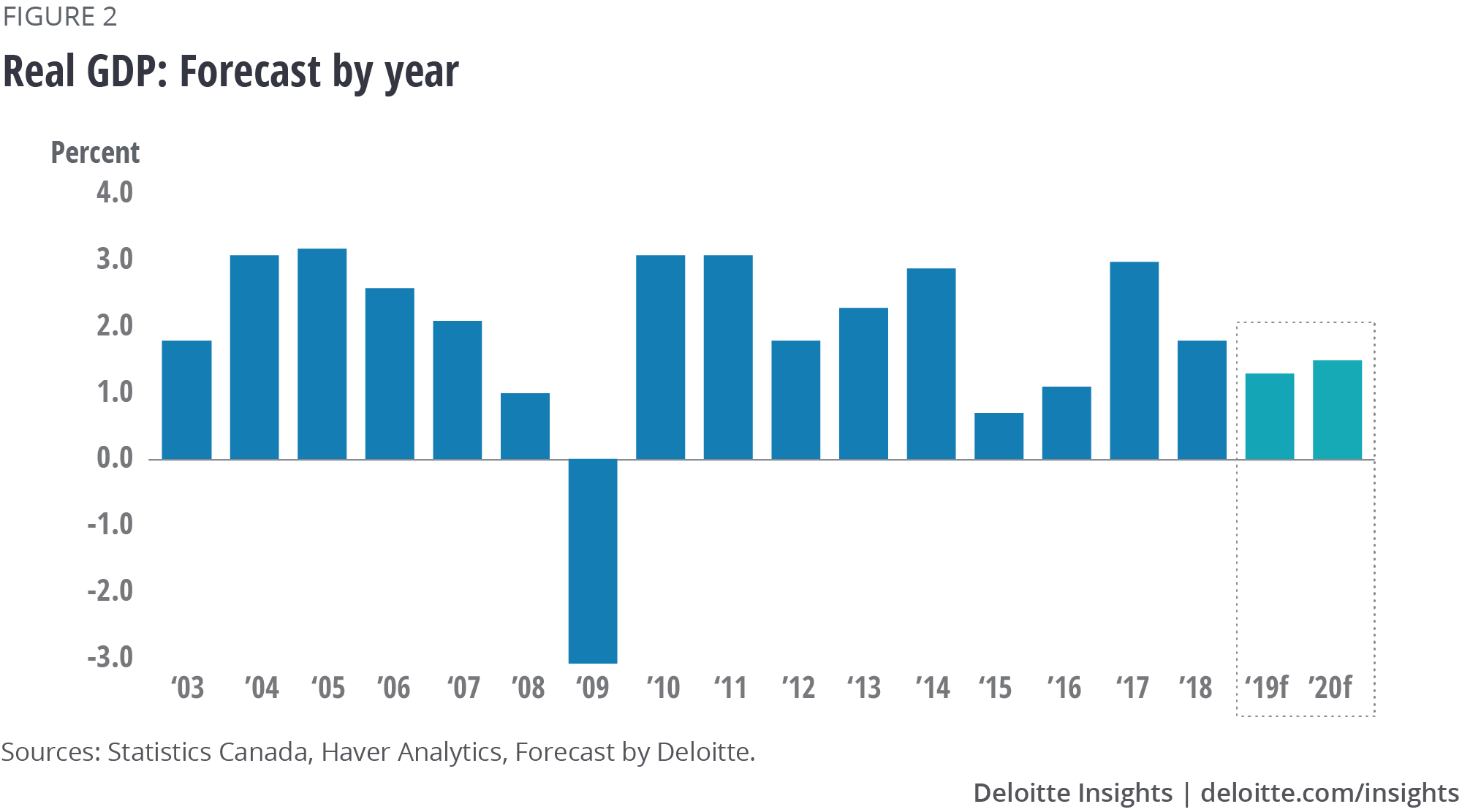

Economic growth in Canada slowed from 3.0 percent in 2017 to just 1.8 percent last year, and had little momentum heading into 2019. Growth is unlikely to bounce back substantially in early 2019 as inventories are reduced and household spending remains modest. Business investment should pick up, but the weak global backdrop and decelerating US economy will likely keep the gains muted and temper export growth. Accordingly, the Canadian economy is now projected to grow by a weak 1.3 percent this year and fare only slightly better in 2020, with 1.5 percent growth. With the pace of expansion below its long-run potential pace, inflation should remain in abeyance, leading the Bank of Canada to keep interest rates unchanged and contributing to a sustained weak Canadian dollar.

Learn more

Read the latest quarterly economic forecast for Canada

View past outlooks for Canada

Explore the Economics: Americas collection

Subscribe to receive related content

Canada’s economy stalled in Q4, but did not derail

The Canadian economy stalled in the last quarter of 2018, with real GDP increasing by a mere 0.4 percent (annualized) in the final three months of the year. Were it not for a buildup in inventories, the economy would have contracted 1.1 percent (annualized). The weakness was broadly based across sectors during the quarter. Moreover, real GDP declined 0.1 percent in December, creating a weak handoff into 2019 (figure 1).

Investment was a key source of disappointment in the fourth quarter. Residential investment plunged an annualized 14.7 percent, following a 5.5 percent decline in the prior quarter. Overall, residential construction activity declined in all but one quarter last year and was down 7.5 percent from a year ago. Real estate activity was down sharply in existing home markets last year due to tighter mortgage qualification regulations, higher mortgage rates, and increasing household debt service costs, with the softness spilling over to new housing.

Nonresidential investment was another source of weakness, with a 15.0 percent (annualized) drop in structures and a 4.8 percent decline in machinery and equipment investment. After contracting in the third quarter, some reprieve was expected in the final three months of the year. Alas, this was not the case. While the drop in oil prices in late 2018 was a blow to investment in the energy patch, the decline in business investment was much broader, as it was apparent in many industries.

Unlike in the first half of 2018, household spending did not help the economy much. With a mere 0.7 percent (annualized) increase in the fourth quarter, it was the weakest showing since the recession. This is consistent with our prior view that heavily indebted consumers would temper their spending, particularly on categories sensitive to interest rates, such as autos and big-ticket housing-related items. Outlays on durable goods fell 2.0 percent in the fourth quarter, marking a third consecutive contraction. Spending on services was more resilient, continuing to advance at a 2.0 percent pace.

Net exports contributed slightly to economic growth, though not in a favorable manner. The volume of exports edged down 0.3 percent, and imports fell 1.1 percent, echoing the weakness in domestic spending. Removing exports from the picture, final domestic demand has declined for two quarters in a row—the first time since early 2015.

The C$13.2 billion increase in inventory investment kept the economy afloat in the fourth quarter. However, it appears the accumulation was likely not desired by businesses. Inventories were already at high levels relative to sales, suggesting that destocking is in store in the coming quarters. This will hinder future economic growth.

Outlook: Weak Q1, then better growth

Where does the economy go from here? The contraction in residential and business investment may spill over into early 2019, but it is unlikely to be sustained. Moreover, the fundamentals for consumer spending—highlighted by low unemployment and rising income—should support higher outlays. The recent economic slowdown is also likely to keep the Bank of Canada from raising interest rates further. This will arrest the increase in household debt service costs, support real estate, and keep a lid on the Canadian dollar. In other words, economic growth should improve but a sharp rebound is unlikely.

While consumption expenditures and nonresidential investment are expected to improve in early 2019, further declines in residential investment and inventory destocking will likely offset the gains. As such, growth in the first quarter will accelerate but the pace will remain subpar, at close to 1.0 percent. As drag from residential investment diminishes and inventory stockpiles are reduced, the pace of economic expansion is projected to then strengthen to around a 2.0 percent pace later in the year.

While this marks an improvement, the pace is well shy of a typical rebound as heavily indebted consumers continue to moderate their spending and home-buying activity. Nonresidential investment should also pick up, but the weakness in the global economy and continued risks related to the United-States–Mexico–Canada Agreement ratification, US protectionism, and global retaliation may weigh on business confidence. A weak Canadian dollar will support Canadian export competitiveness, but slowing global trade and world demand growth will limit the gains. The cooling in US economic growth is also likely to restrain the gains in Canadian exports.

All told, the Canadian economy is expected to grow at a subpar 1.3 percent in 2019 and 1.5 percent in 2020 (figure 2). This is below the economy’s long-run sustainable pace of expansion, which is estimated at around 1.7 percent given the prospects for labor force growth and labor productivity. However, the resulting economic slack should keep inflation under wraps. Importantly, the modest pace of economic growth will leave the Canadian economy more vulnerable to unexpected negative shocks.

Outlook by region

The provincial picture varies over the 2019–2020 period. British Columbia will likely remain at the top of the provincial leaderboard with economic growth of a bit below 2.0 percent, but this is a slower pace than its robust expansion of recent years. Ontario and Quebec are expected to be in the second and third positions, with growth close to or slightly above the national average. Saskatchewan and Prince Edward Island will likely be only slightly below the national average.

Alberta and Newfoundland and Labrador will struggle with the fallout from last year’s decline in oil prices, which have recovered but are not back to prior levels. The pace of growth in these two provinces will be a bit above 1.0 percent, but this is disappointing given the painful economic times in 2015–2016 caused by a prior oil shock. Manitoba’s economy is low on the provincial ranking, reflecting mine closures and the completion of major construction projects.

Meanwhile, demographic pressures from aging baby boomers are particularly acute in all Atlantic provinces. Indeed, the forecasted growth rates of 0.9 percent in New Brunswick and 1.2 percent in Nova Scotia are favorable when one makes allowances for demographic pressures.

Prepare to mine the silver lining

The base case outlook remains for continued modest growth, but talks about recession risks are unlikely to disappear. The odds of a Canadian economic contraction without a US recession or a hard landing in the global economy are very low. The Canadian economy is integrated into a North American production chain and is tied to global commodity markets. An economic downturn caused by a drop solely in domestic demand is likely to be mild. However, a significant downturn could materialize should weakening domestic conditions coincide with a significant external shock.

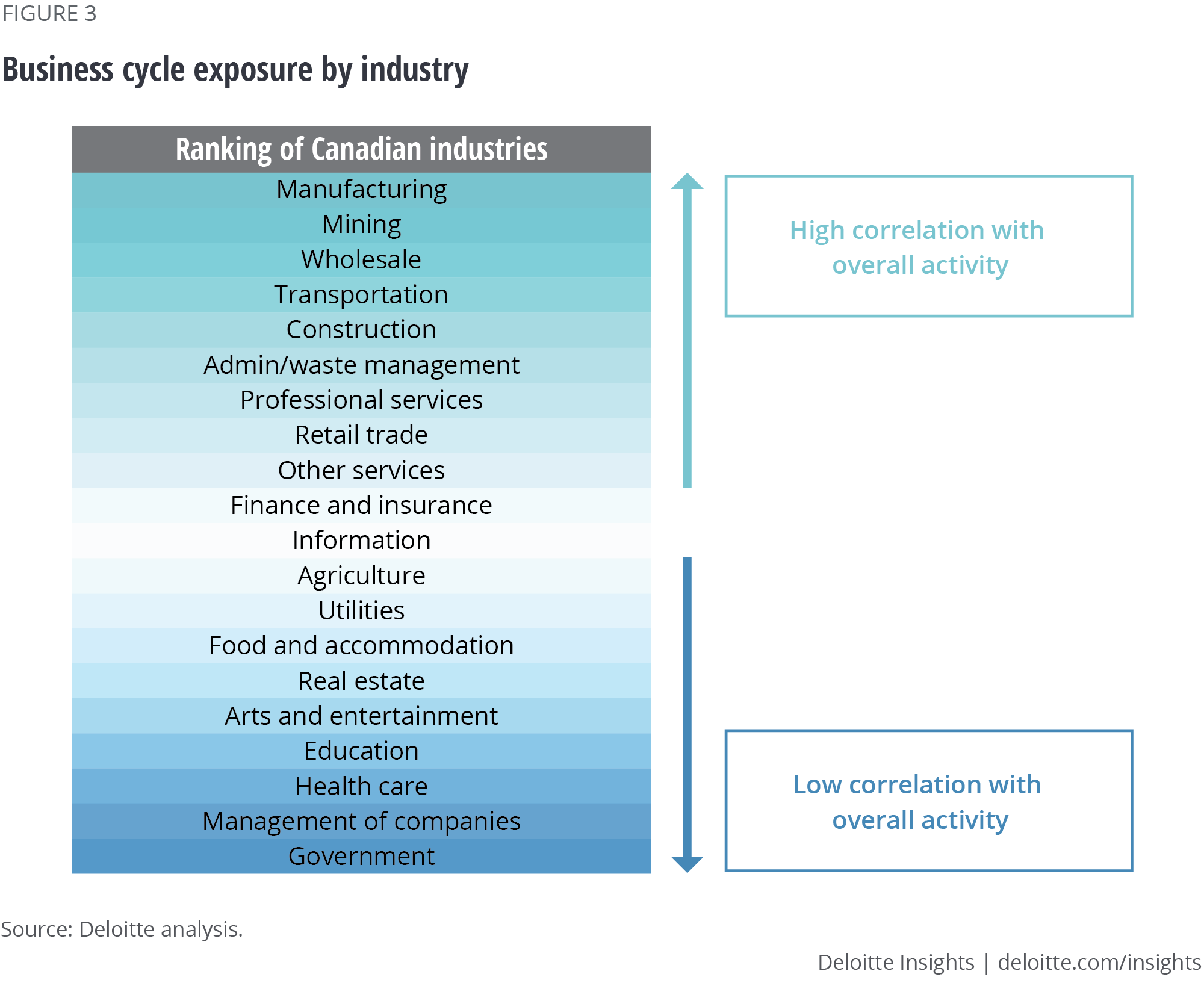

All Canadian companies and governments will be affected by such macroeconomic conditions. The industries most affected by cyclical changes in the economy include manufacturing, mining, wholesale trade, transportation, and construction (figure 3). Other industries such as retail, finance, utilities, and real estate also follow the cycle closely. Industries that are least affected include public administration, health care, and education—but being less vulnerable is not the same as being immune.

This means that each business in every industry needs a good appreciation of how sensitive it is to shifting demand. If an organization is particularly vulnerable, making a plan now about how to deal with the evolution of the economy is advised: Being prepared for a challenge is better than being forced to respond in the midst of one. Businesses that are more resilient or better positioned than their competitors to deal with changing economic times can take advantage of business opportunities. Additionally, economic and financial volatility has varied effects—some organizations will benefit from a weaker Canadian dollar, while for others it poses a challenge.

Concluding remarks

The last few months have been a bit of rollercoaster ride, with the global economy shaken by some dramatic financial swings and evidence of a broad-based slowdown; Canada’s own economic growth sputtered with expectation of an anemic year ahead. Businesses and governments cannot immunize themselves from economic and financial cycles. The key to remaining healthy is to understand the risks and their implications.

Since the Great Depression, the Canadian economy has experienced 12 economic cycles. Its governments and businesses have weathered them all and thrived, with the economy expanding and supporting a rising standard of living. The current economic outlook may look more challenging and business downcycle risks do exist, but it is important not to develop a recession mindset. Instead economic challenges can be a good motivator for innovation and change.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Learn more

Get in touch

- Craig Alexander

- Chief economist

- Partner, Deloitte Canada

- craigalexander@deloitte.ca

- +1 647 354 0348

Explore the Economics: Americas collection

-

How the financial crisis reshaped the world’s workforce Article5 years ago

How the financial crisis reshaped the world’s workforce Article5 years ago -

-

Brazil economic outlook, February 2024 Article1 month ago

Brazil economic outlook, February 2024 Article1 month ago -

Volatility in emerging economies: Is contagion too harsh a word? Article5 years ago

Volatility in emerging economies: Is contagion too harsh a word? Article5 years ago -

United States Economic Forecast Q1 2024 Article1 month ago

United States Economic Forecast Q1 2024 Article1 month ago -

Issues by the Numbers, July 2018 Article5 years ago

Issues by the Numbers, July 2018 Article5 years ago