India economic outlook, October 2023

India is making headlines—in both space science and economy—but to soar to its aspired heights, it must drive domestic demand through its MSMEs amidst global uncertainties.

As if the moon was not enough, India is now aiming for the stars. After the successful launch of Chandraayan-3 on August 23, 2023, India has now set its sights on the sun by launching Aditya-L1, a spacecraft designed to study the solar atmosphere. Only a handful of countries have achieved this historic feat.

And it is not just in science where India is taking big leaps. The Indian economy, according to IMF estimates, will emerge as the world’s third largest economy by 2027, hopping over Japan and Germany, as its GDP crosses US$5 trillion dollars. By 2047, India aspires to be a developed economy.

According to our estimates, India will need at least 6.5% growth to reach its first milestone in 2027 and about 8%–9% growth to reach the second in 2047. The buoyancy in the economy instills confidence that the country, at least in the short run, will likely achieve these numbers. The pace in the first few years will be critical for a sustained, fast-growth trajectory in the long run.

In light of the Q1 GDP growth, we have revised our growth estimate for this year to reflect it. We expect GDP to grow in the range of 6.5% to 6.8% primarily due to festive spending in the coming months followed by higher government spending before the upcoming national elections mid-next year. We believe GDP growth will be over 6.5% next year as geopolitical uncertainties subside, and the global economy bounces back on a stronger growth path.

Navigating geopolitical uncertainties and the slowdown in the global economy, undoubtedly, will not be easy. India will have to rely on its own domestic demand to firepower its growth, specifically, private consumption and investment spending. What works in India’s favor on the private consumption front is the size of its consumer base, the rising income, and the aspirations of its young population, which is the largest in the world. As for investments, with the size and scale of operations it has to offer to global companies, the availability of skill and talent, and technology and innovation capabilities, India continues to be an attractive investment destination.

The spotlight, in this outlook, is on India’s micro, small, or medium enterprises (MSMEs). These, we believe, will be key in generating income, capabilities, capacities, and ecosystems needed for sustained growth in consumption and investment that is broad-based and comes from all sections of the economy. The MSME sector will also drive innovation and new opportunities in a cost-effective manner. It will drive job creation and entrepreneurship, especially for women in rural India. In short, the sector will help India reap the potential benefits of its demographic dividend and the expansion of the middle-income class.

The good news is that the past two quarters have seen an uptick in the MSME sector. Out of the shadow of the pandemic, the steady revival of this sector will likely help India achieve broad-based growth at the grassroots levels, which is needed to ensure sustained economic activity.

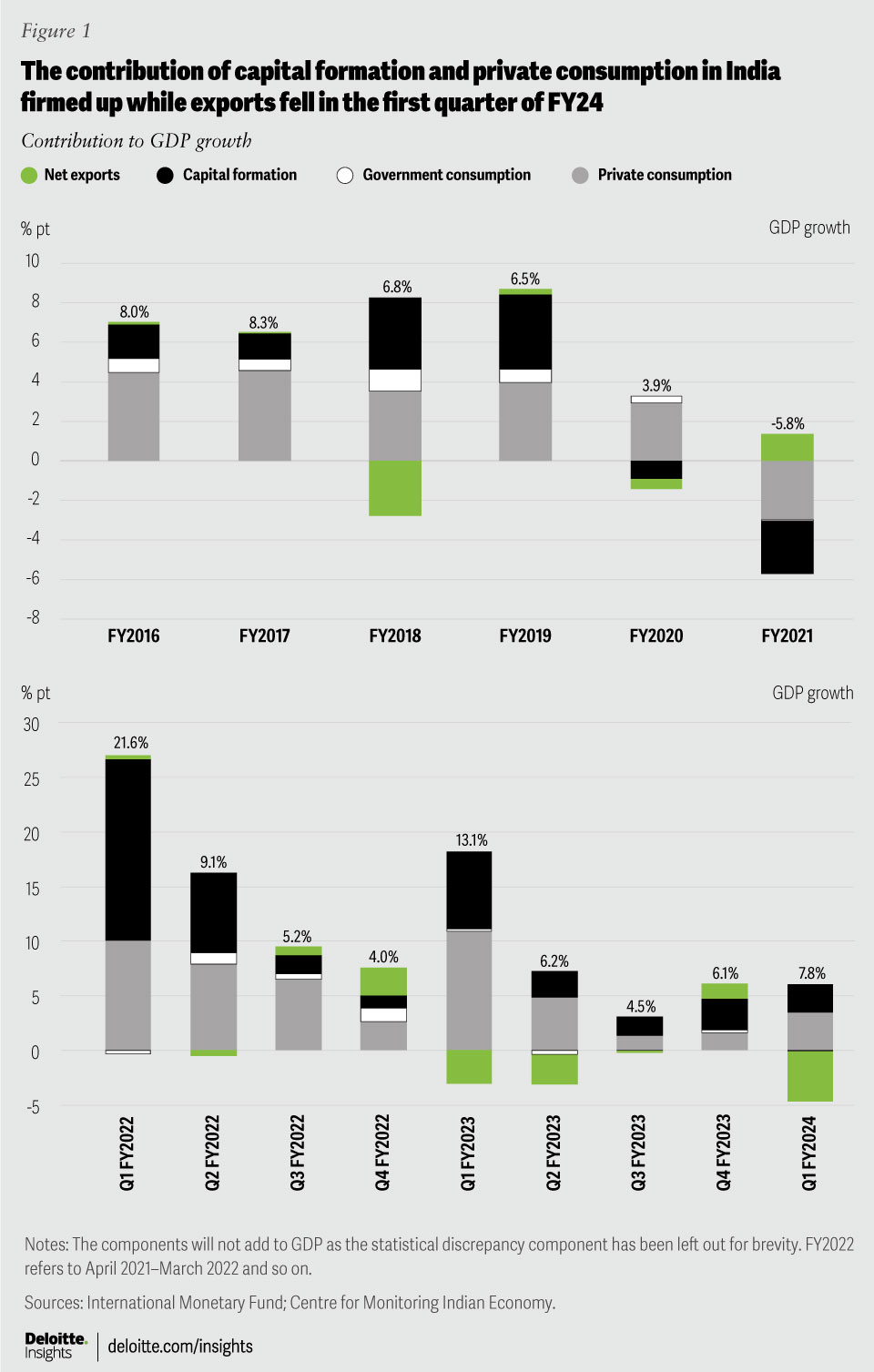

Decoding growth in Q1 FY24

India grew 7.8% in the first quarter, which is close to the Reserve Bank of India’s (RBI’s) estimate of 8.1%. A large part of this growth came from strong domestic demand even during the time the global economic slowdown weighed on exports, which contracted by 7.7% after growing in double digits for eight consecutive quarters. While the contraction was broad-based due to moderating demand, the exports in electronics goods remained strong—its share in total exports has gone up from 3.4% to 7.2% in two years. What aided this growth was the accelerated digitization around the globe and India’s determination to accelerate efforts towards self-sufficiency in the electronics space.

Private sector investment grew 7.8% YoY, thus maintaining the steady momentum of the past five quarters, aided by the crowding-in effect of higher capital expenditure by the government. The highlight was probably the strong revival in private consumption by 6 % after its lackluster growth for two quarters. Modest consumer spending, to some extent, has kept private investment on a leash. The strong consumption growth this first quarter bodes well for investors, who are waiting for sustained cues in consumer demand to invest. The completion of investment projects, as per the Center for Monitoring Indian Economy’s (CMIE’s) capital expenditure database, showed a strong jump in the first quarter. Moreover, the pipeline of upcoming projects appears quite strong.1

{kind=link}

The manufacturing and construction sectors—buoyed by pick-up in capital expenditure by the government, the rise in demand for new residential properties, and falling input prices (as indicated by wholesale and fuel prices)—witnessed robust growth of 4.7% YoY and 7.9% YoY, respectively. But the biggest boost in growth came from the services sector, which grew 10.3% YoY in the first quarter, up from 6.9% in the previous quarter. This boost can be attributed to strong growth in the financial, real estate, and business services sector. It also corroborates the consistent rise in the export of professional services. An uptick in credit growth following the improvement of the bank balance sheets, rising deposits, and innovation in the fintech space played a vital role as well. The trade, transport, and communication sector also did well (9.2% YoY).

Growth in the agriculture sector, in contrast, slowed down marginally to 3.5% year over year. The delay in the arrival of the monsoons and spatial rains across the country impacted agriculture output in June. So far, cumulative rains have been below normal, which will likely temper agriculture growth in the first half of FY2023-24. A slowing agriculture output could exacerbate food inflation further, and therefore, weigh on consumer spending and investment.

What lies ahead

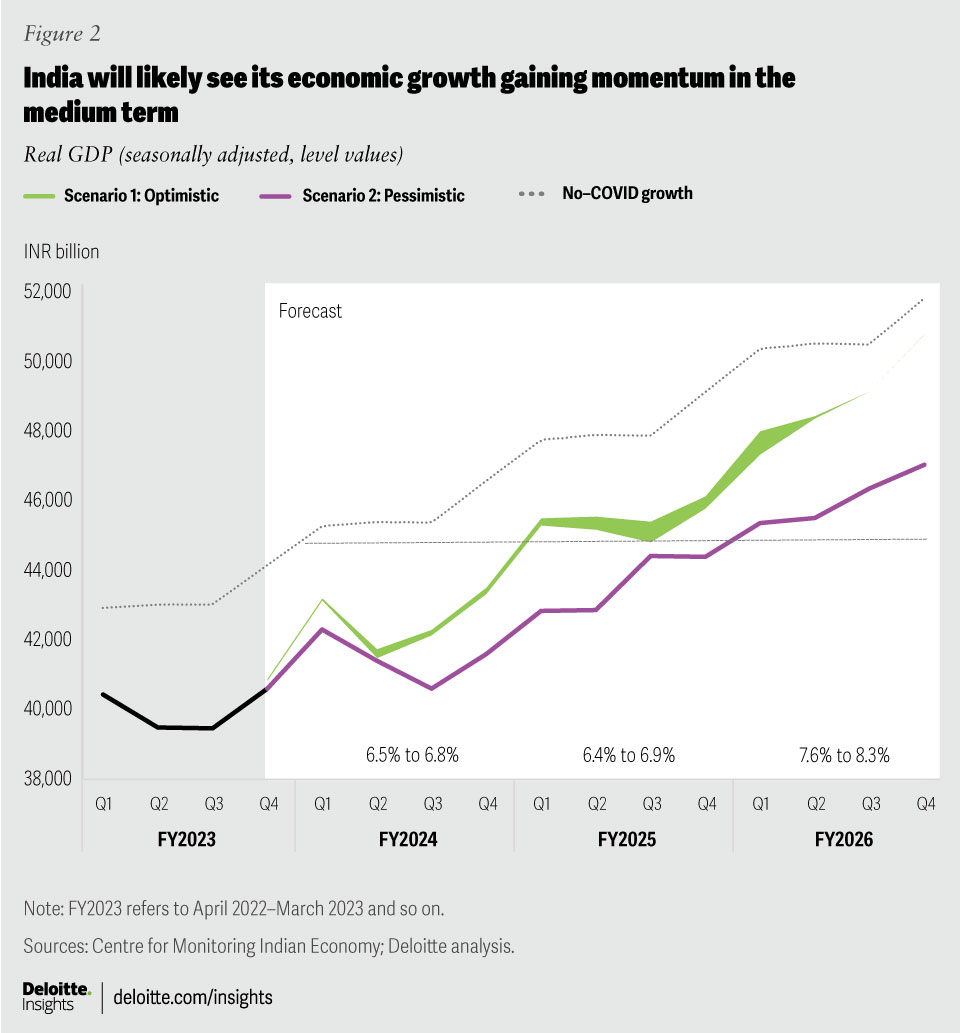

We continue to remain optimistic about the economy this year and expect India to grow between 6.5% and 6.8% between FY23 and FY24 in our baseline scenario, followed by an average of 6.65% and 7.95% over the next two years as the global economy turns buoyant (figure 2). (For more on our baseline and pessimistic scenarios, see Key assumptions.)

{kind=link}

Key assumptions

Optimistic scenario: The Russia-Ukraine conflict does not escalate but is prolonged for a long period. The bank crises remain contained with no meaningful global impact. Growth in the United States and the EU slows down over a tighter monetary policy this year but rebounds in 2024. There is political stability after the elections in India and the United States.

- The US Federal Reserve pauses policy-rate hikes until later this year, as inflation seems to be slowing.

- Crude oil prices remain high, between US$85 and US$95 per barrel, thus adding pressure on global inflation. Yet, a slowdown in China keeps a tab on price rises.

- The RBI balances growth, inflation, and depreciating currency against the US dollar and capital flight by maintaining a tighter policy stance. It goes for one more hike before it halts further hikes.

- The government’s efforts toward consolidation of expenses continue, supported by buoyant revenues, even though expenses go up due to upcoming elections.

- The state and the Centre election results do not bring any political uncertainties or instabilities.

- Inflation remains vulnerable to rising food and fuel prices for at least the next year.

- Investors factor in uncertainties and focus on growth potential. Consequently, investments pick up robustly over the next two years.

Pessimistic scenario: The Russia-Ukraine conflict continues for a prolonged period. Tensions escalate with several nations getting directly involved in the war. The United States and Europe enter a recession. The crisis in the banking system raises significant tail risks for economic activity.

- Prolonged crises lead to second-order implications for financial stability and supply chain disruptions.

- Crude oil prices breach US$110 per barrel.

- Political instability after national and state elections impacts market sentiments.

- Inflation spirals up globally, impeding growth in investments.

- The RBI goes with further hikes but later retracts them as growth tumbles.

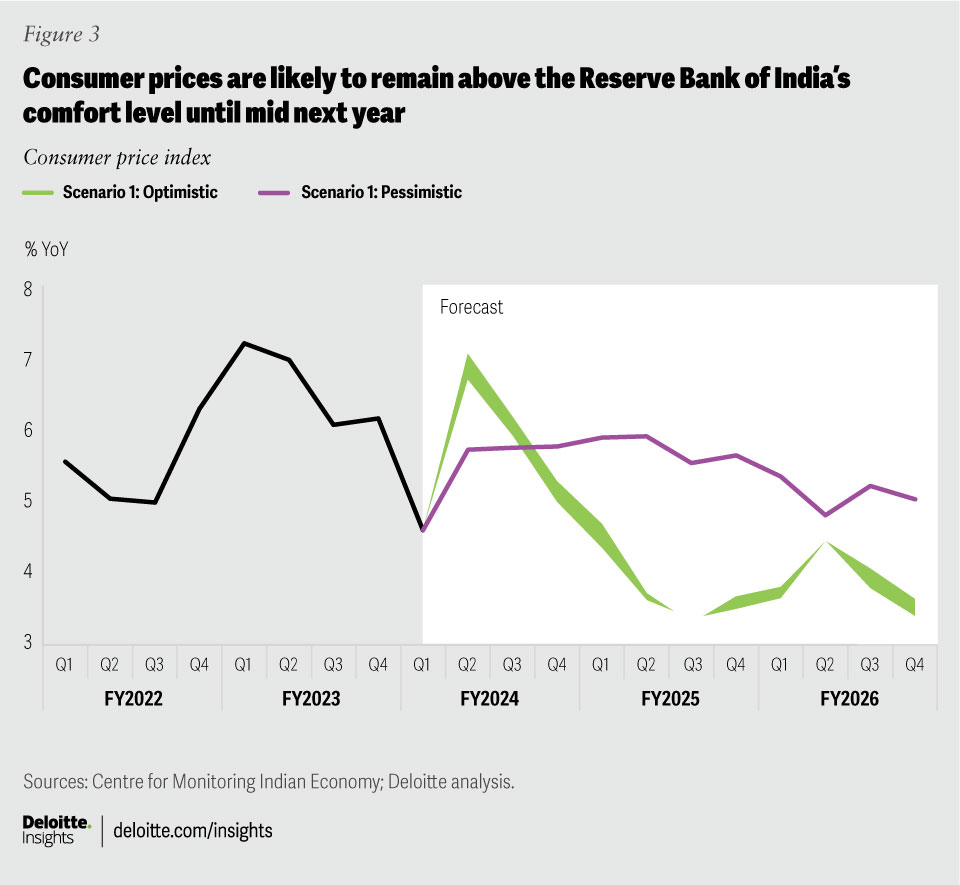

Our worries about inflation persist. High food prices, especially the double-digit growth in pulses and cereals, which have a significant share in the CPI food basket, are concerning. Besides, oil prices are trending up quickly. Food and fuel prices are likely to keep inflation high. The spillover effect on core prices, which have been stable so far but in the upper bracket of the RBI’s desired range, could lead to inflation getting out of control. We expect higher prices over the next 1.5 years. We expect inflation to remain in the upper range of the RBI’s inflation target band over the entire forecast period (figure 3).

{kind=link}

Spotlight on MSMEs

By the end of FY2023 (end of last fiscal year), India is estimated to have 75 million MSMEs. The sector has been responsible for contributing approximately 30% to the country’s GDP, 43.6% of merchandise exports, and close to 123 million jobs to employment. With a predominance of the microsegment and a strong presence in rural areas, the MSME sector is well placed to cater to rural demand and low-income consumers. Hence, it is the foremost source of reducing regional imbalance and assuring equitable income distribution. Furthermore, India needs income generation at the grassroots and a transition of labor from agriculture to manufacturing and services—the MSME sector can be of significant help on both fronts. Besides, a large proportion of MSMEs work in the services sector, which accounts for 57% of GDP. Needless to say, growth in this sector will pave the way for sustainable growth in income and output.

Despite its importance, the sector is also mired in challenges. Some are structural in nature, such as limited access to formal credit, skill and technology gaps, insufficient infrastructure, and complex tax structure. These structural impediments have often weighed on their operational efficiencies and prevented units from scaling up. These impediments have also inhibited MSMEs’ ability to compete globally. The sector has also been vulnerable to fluctuating commodity prices, global trade and dumping from China, and changing regulations and standards, among others. Recently, the pandemic played havoc on this sector due to the sudden drying up of liquidity, labor migration, fall in demand for goods, cancellation of contracts, and disruptions in logistics and supply chains.

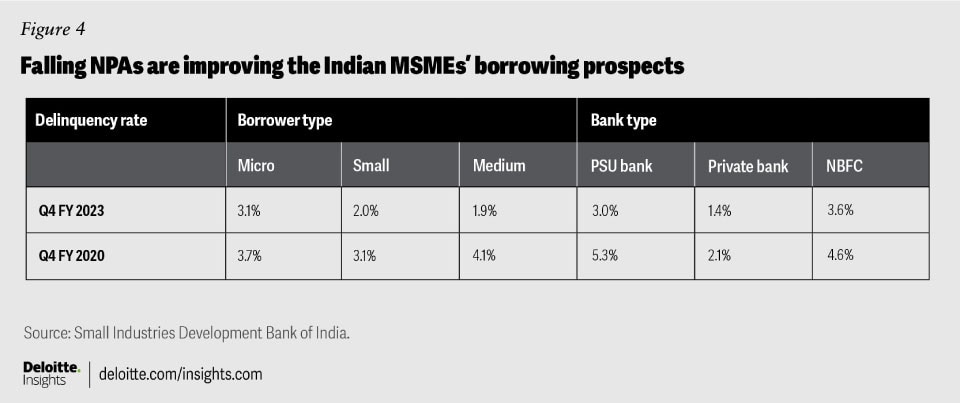

Thankfully, the sector is now emerging out of the crisis and several parameters point to steady growth. The demand for loans, for example, in the sector has gone up 33% in the first quarter of FY2023-24, while the delinquencies are declining as nonperforming assets have improved across all types of lenders lending to MSMEs and across all MSME borrowers (figure 4).

{kind=link}

Technology changing the MSME landscape

Technology is helping the MSME sector in important ways to overcome several of the sector’s challenges. During the pandemic, many enterprises were compelled to register themselves (so that they could avail the government’s support to deal with the financial stress) and adopt digital services to sustain themselves. Moreover, MSMEs are rapidly adopting digital payments over cash: During the pandemic, 72% of payments were done through digital mode, while just 28% of transactions used cash between 2020 and 2021.2 Technologies, such as the cloud, are helping MSMEs with better forecasting abilities, while automation and robotics are aiding in speeding up and streamlining operational processes, reducing costs, and improving sustainability. Furthermore, embedded finance startups and account aggregators are helping these MSMEs to access faster credit, which has been one of the biggest challenges facing MSMEs in India.

Some of the policy initiatives have also aided recovery in this sector, such as the emergency credit line guarantee (ECLG) scheme during the pandemic and production-linked incentive (PLI) schemes. According to State Bank of India research, 12% of the outstanding MSME credit was saved from slipping into nonperforming assets and 16.5 million job losses were avoided because of the ECLG scheme.3 Close to 176 MSMEs are likely to be indirect beneficiaries of the PLI scheme in sectors such as bulk drugs, telecom, textiles, medical devices, white goods, drones, and food processing. The rise of the sunrise sectors, such as green energy, e-mobility, semiconductors, food processing, defense, and space, is also opening up new opportunities for the sector.

The sector has seen steady performance improvement over the years. Not only are MSME units growing, but many are also turning into midsized corporates thanks to greater integration with larger value chains.

MSMEs will need the right impetus to go global

Recognizing the paramount role the MSME sector plays in the economy, the Indian government will have to ensure that the sector rebounds strongly by promptly addressing the structural and institutional challenges the sector is facing with the right policies and recommendations. Measures around formalization, addressing infrastructural bottlenecks, encouraging exports, and promoting digitization will go a long way toward improving the contribution of the sector to employment, income, and exports. Doing this will require a sector-specific approach (separate policies for manufacturing and services) during policy formulation as a generic approach may not address the shortcomings.

Efforts must be focused on elevating quality standards and preventing brand dilution from low-quality products. This may require the government to grant a level of exclusivity to the MSMEs and encourage them to protect their intellectual property, inventions (with the help of patents), and designs (by legally registering the design). To encourage innovation and adoption of technology, the government must make its digital public infrastructure accessible and affordable for MSMEs to scale up businesses and customer base. This will also help boost entrepreneurship and create job opportunities, especially among women, where the potential remains untapped.

It is often said that the whole is greater than the sum of its parts—in India, MSMEs will need a strong revival in the coming years. That revival will have a systemic impact on the entire economy leading to stronger and more resilient growth giving India the desired impetus it needs to achieve its ambition of reaching stars.