Japan economic outlook, January 2024

High inflation and weak wage growth present challenges to Japan’s economic recovery.

Japan’s recovery is struggling to gain momentum. Real GDP contracted in the third quarter as inflation eroded purchasing power. Real domestic consumer spending fell 0.3%—the second consecutive contraction.1 Although monetary policy remains highly accommodative, inflation is outpacing wage growth, causing real spending to fall. Until inflation comes down or wages move up, domestic demand is expected to remain subdued or even continue to decline. This dynamic will likely persist until the second quarter of 2024 when wage growth is expected to pick up as the Bank of Japan (BoJ) becomes more hawkish in its efforts to bring inflation down.

An earlier move from the BoJ seems unlikely, however, as wage growth will remain subdued until March or April 2024—a time when many annual wage negotiations are expected to occur. In the meantime, consumers will also likely get some help from the government, which unveiled a 17 trillion-yen (approximately US$117.7 billion) fiscal package to offset purchasing power lost to inflation, with temporary tax cuts and fuel subsidies.2 By the second half of the year, moderating inflation and accelerating wages should allow for a stronger recovery to take hold.

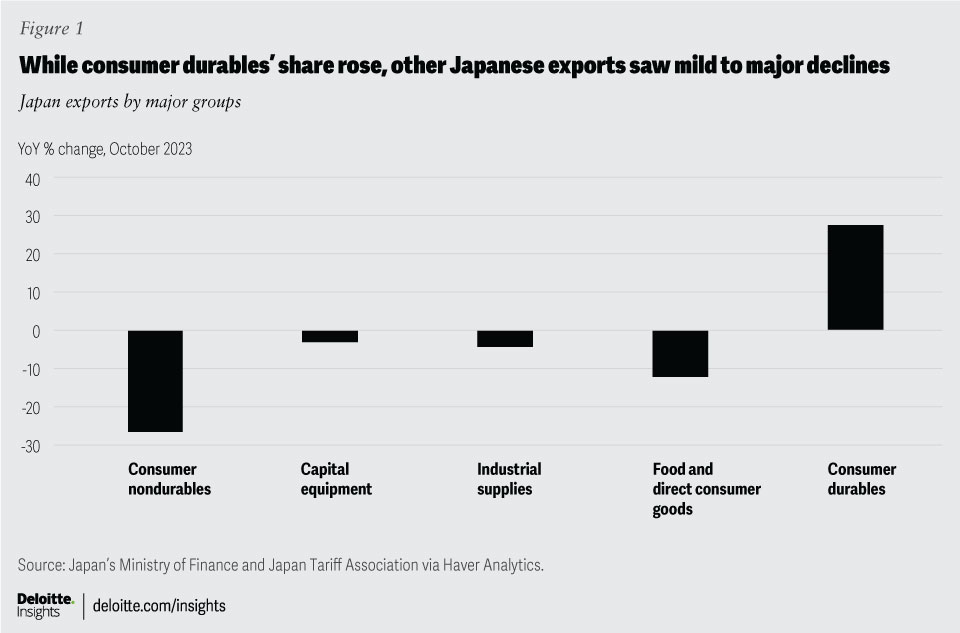

Export growth will also likely come down as global growth slows and pent-up foreign demand for Japanese goods eases. Japan’s goods exports were up just 1.6% from a year ago in October.3 A surge in motor vehicle exports is the main reason exports grew at all. Motor vehicle exports were up 35.4% from a year earlier4—with export growth to the United States, European Union, and China standing above 30%. The US autoworkers’ strike, higher operating costs in Europe, pent-up demand for automobiles following supply disruptions, and a weak yen all likely contributed to this robust performance. However, other major export categories were all lower on a year-ago basis, including food and direct consumer goods, industrial supplies, capital equipment, and consumer nondurable goods.5

{kind=link}

The strength seen in motor vehicle exports is unlikely to last. The US autoworker strike has ended and pent-up demand for autos seems to be waning as high interest rates make financing vehicles more expensive. At the same time, the yen is beginning to appreciate—thanks to expectations of a dovish Fed and hawkish BoJ. The value of the yen reached a new low of 151.74 to the dollar on November 13. By December 12, however, the yen had appreciated to 145.44.6

Inflation continues to climb

Inflation in Japan continues to run above the BoJ’s 2% target, with headline inflation at 3.3% in October on a year-ago basis.7 Although inflation has been persistent, its driving forces are changing. Goods inflation continues to run hot at 4.4% but has come down substantially since January 2023 when it was 7.3%.8 Much of the persistence in goods inflation is due to rising food prices—food and beverages costs were still up 8.6% in October. Although services inflation was just 2.1% in October, that is the highest reading since 1998.9 After excluding volatile food and energy components, the so-called western core was up 2.8%—the highest it has been since 1992.

Although inflation is clearly running above target, Japan’s bout of inflation has been more muted than what was seen in the United States and Europe. It seems that Japan’s inflation is following those countries but with a delay and a lower peak. The central banks in the United States and Eurozone raised rates substantially to get inflation under better control, but the BoJ has yet to make a substantive change to its monetary policy position. Indeed, it is the only central bank that has retained its negative interest rate policy.10

Japan’s monetary policy is likely to change in 2024 and central bank officials have hinted at rate hikes in the near future. For example, the deputy governor of the BoJ recently noted that the economy will be able to handle the end of negative interest rates.11 Some tightening of monetary policy makes sense given headline inflation has been running above target since April 2022, and western core has been above target since February 2023. Many investors are increasingly expecting a rate hike within the first half of 2024.12 However, the durability of above-target inflation remains a risk to that outlook.

Although BoJ officials have hinted that they are more open to raising rates, they have also stressed the importance of seeing stronger wage growth before making such a change.13 The rationale here is that inflation will sink below the 2% target if wage growth is not strong enough to create a virtuous cycle between prices and worker compensation. Raising interest rates prematurely would then risk suppressing wage growth, which would push inflation back under target.

Stronger wage growth is needed

For establishments with 30 or more employees, total cash earnings were up 2.3% from a year ago in October.14 Unfortunately, this is below the rate of inflation, and real cash earnings fell 1.6% for such establishments. At first glance, positive wage growth appears relatively durable. Scheduled earnings—excluding overtime and bonuses—were up 2.3% from a year earlier in October for such establishments with 30 or more workers.15 This rate of wage growth was tied for the highest since 1995. However, the strongest growth has gone to part-time workers. Full-time workers in these establishments saw their scheduled earnings rise by just 1.6% over the same period. Plus, smaller businesses posted weaker wage growth. Nominal cash earnings for establishments with five or more employees was up just 1.5% from a year earlier.16 More substantive wage gains will be needed for full-time workers and those employed at small businesses.

{kind=link}

Stronger wage growth will largely depend on tightness in the labor market. After declining steadily between October 2020 and January 2023, the unemployment rate has drifted upward to 2.5%.17 Although this is a low number by international standards, it is above the 2.2% rate seen just before the pandemic. Nonagricultural employment has also slipped slightly since June 2023, which suggests the labor market is loosening rather than tightening.18

Nevertheless, the trajectory of wage growth can change amid the spring wage negotiations called shunto. Large employers typically announce their wage increases in March or April, which establishes a benchmark for other employers when determining employee compensation. Historically, there is a surge in wage growth in those months, and next year should be no different. Given that inflation-adjusted wages have been falling for much of 2023, it is reasonable to expect that employers will raise wages more substantially this year to offset the negative effects inflation is having on household purchasing power. Because wage growth continues to lag behind a rate that can be considered consistent with 2% inflation, we do not expect the BoJ to raise rates before April 2023.

As the BoJ prepares to raise rates, the Japanese economy looks considerably different compared to where it was during the three decades leading up to the pandemic. Low inflation and negative interest rates had discouraged households from investing their savings in assets that would protect them from inflation. For example, households hold more than half of their financial assets in cash or deposits—far more than the 13% in the United States.19 Japanese citizens have historically been cautious when it comes to investing in equities, but the return of inflation may provoke a change of heart. Plus, the Nippon Investment Savings Account, which offers a lifetime tax exemption on equity investments, will be expanded in 2024, offering additional incentive for households to funnel money into investment assets.20

Rising interest rates may also draw concerns about Japanese government debt. Japan is one of the most indebted countries with a debt to GDP ratio well over 200%.21 Negative interest rates allowed for such a strong accumulation of debt. However, if the government’s interest expense begins to rise substantially, it could create concerns about the sustainability of that debt. This could force the government to make tough choices regarding its future budgets, leading to tax rises, expenditure cuts, or both.

Imbalances in Japan’s economy are expected to restrain growth in the near term. High inflation amid relatively low wage growth is the main challenge to a stronger recovery. We expect a reversal in these trends by the second half of 2024, but this year’s shunto will largely determine if that can happen. Without stronger wage growth, domestic demand will struggle to pick up. At the same time, foreign demand is showing few signs of improving, while higher interest rates limit the government’s ability to implement additional stimulus.