{kind=link}

{kind=link}

{kind=link}

{kind=link}

United Kingdom has been saved

Cover image by: Jamie Austin

Winter lockdowns and the mass vaccination programme have checked the advance of the COVID-19 pandemic in the UK. Average daily deaths are down to the single digits, from a high of around 1,250 in January, while daily new cases are now running 90% below their peak in January (figure 1).

A rise in cases due to the Delta variant, first identified in India, had made it apparent by mid-June that the UK will witness another wave of infections. But, so far, vaccines seem to be keeping hospitalisations under control, with new admissions largely restricted to a shrinking pool of unvaccinated people. Three-quarters of UK adults have already received their first jab, and our calculations suggest that the entire adult population will have been offered the first dose by mid-July and the second dose by September.

Rapid progress in vaccinations has facilitated the gradual easing of lockdown restrictions. Consumer-facing service sectors such as hospitality and accommodation, which bore the brunt of the lockdowns, have reopened, albeit with capacity limits. Travel within the UK has also restarted.

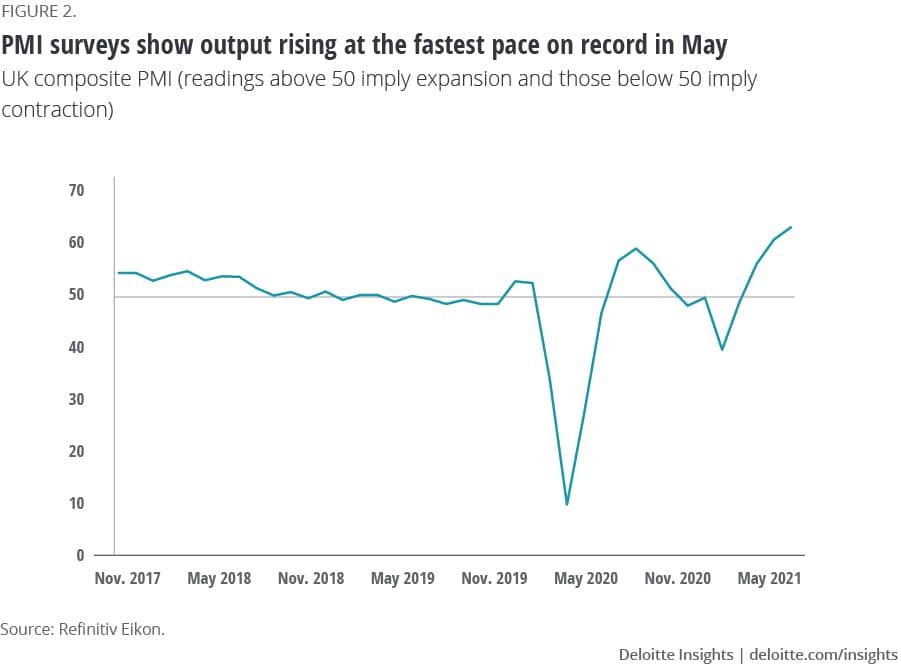

High-frequency data shows an attendant rebound in activity. The latest Purchasing Managers’ Index (PMI) surveys point to a record pickup in output in May (figure 2). Manufacturing orders are at their highest level on record, while service sector activity is growing at its fastest pace in 24 years. Retail sales have also seen strong gains.

The furlough scheme continues to cushion the blow to the labour market, with unemployment under 5% and job vacancies on the rise, especially in sectors that are reopening after a long winter freeze.

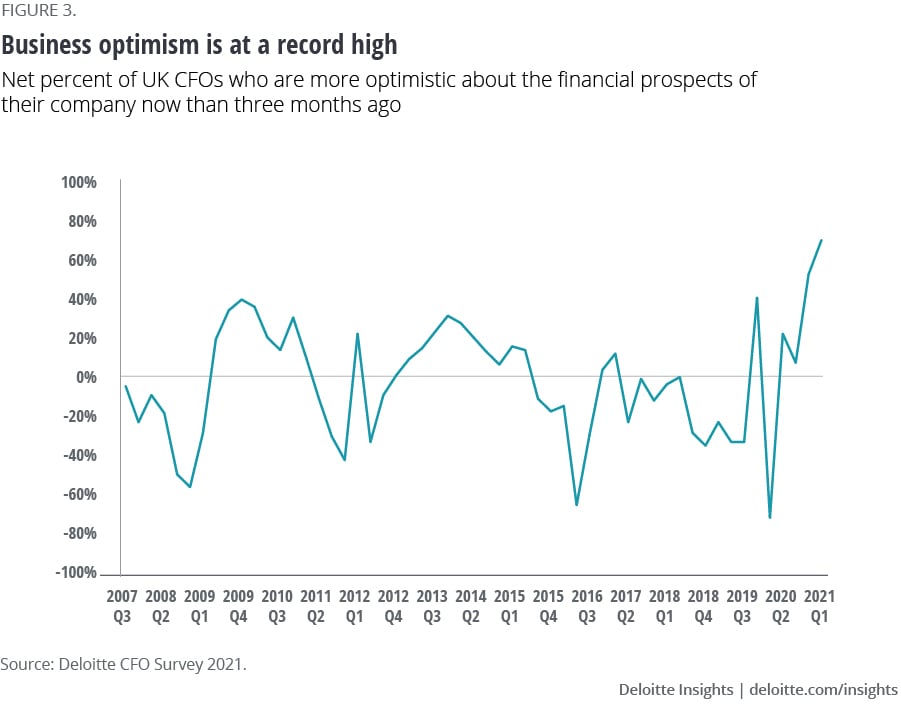

Business leaders also anticipate a strong recovery in profits. Optimism has hit a record high, according to the latest Deloitte CFO Survey (figure 3), and a brighter backdrop has tilted companies away from defensive strategies such as cost control. Businesses are adopting a more expansionary strategy stance, with CFO expectations for hiring and investment now at their highest levels in nearly six years.

This rebound is reflected in growing optimism about the UK’s economic prospects. Economists have upgraded their GDP growth forecasts for this year and the Bank of England now expects unemployment to peak at just under 5.5% during this crisis, down from expectations of 7.8% in November last year.

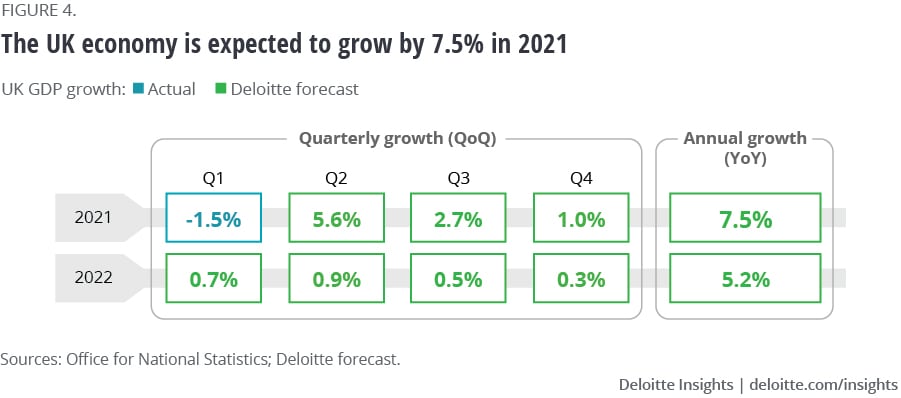

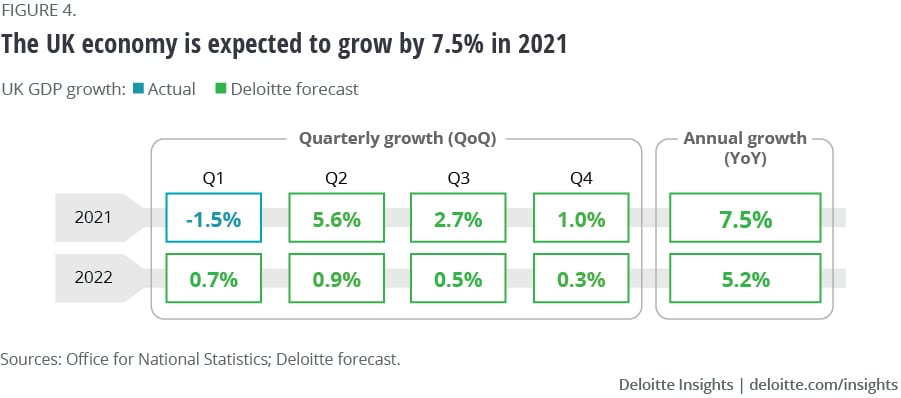

We now expect the UK economy to grow by 7.5% this year (figure 4). Most of this pickup is concentrated in the spring and summer months, which are forecast to deliver greater growth than seen in the four years before the pandemic. We also account for a potential rise in infections in the autumn and winter months, prompting mild social distancing restrictions, given high levels of vaccination and a well-established testing regime. This is reflected in a fourth-quarter slowdown, despite which activity reaches prepandemic levels by the end of this year.

The UK started this year with weaker growth prospects than Europe and the US. Since then, the market view seems to have shifted to thinking that, having suffered one of the most severe downturns among major economies, the UK will see one of the strongest upturns. Our forecasts now imply a better performance than the US and significantly faster growth than Europe this year.

But risks remain. The Delta variant is now known to be significantly more transmissible than the alpha variant, which caused the winter wave in the UK, and further community spread given future easing of restrictions could hinder a permanent and full reopening of the economy. The discovery of further mutations of the virus, especially vaccine-resistant ones, could also stop the recovery in its tracks.

The risk of a significant spike in unemployment, once government support is eased, has reduced somewhat. Instead, the recovery has exposed more immediate resource bottlenecks and labour shortages, as supply struggles to keep up with resurgent demand. This has inflated input prices and there are signs of wage pressure in specific sectors and occupations. A dramatic reversal of immigration, induced by Brexit and the pandemic, has also contributed to the immediate labour shortage.

Some worry that these factors could deliver a sustained rise in inflation, rather than a short-term spike in prices where supply eventually adjusts to renewed demand. This could force the Bank of England to raise interest rates, changing what has been a highly supportive policy stance for asset prices and government borrowing. But most policymakers and economists remain unfazed. They point to ample spare capacity and underlying labour market slack as factors that should limit inflationary spikes.

The outlook for UK growth is very positive. Markets and economists seem poised for a perfect recovery—one where rapid growth coincides with higher but limited inflation. Yet a lot could go wrong. We share in the general optimism but will be keeping a close eye on case rates and price pressures for now.

Cover image by: Jamie Austin