On the watchlist: The office sector in commercial real estate

The April 2024 Economics Insider explores how hybrid work models and rising vacancies have increased scrutiny on how commercial real estate is valued—especially office buildings

The abrupt failures of Silicon Valley Bank and Signature Bank in early 2023 caused regulators to increase focus on how banks were managing risk in the now higher interest rate environment. They identified commercial real estate lending, especially lending tied to office buildings, as a source of particular concern. With elevated vacancy rates and falling valuations and depending on when in the last cycle a property was financed owners of these properties might face challenges refinancing at higher rates—factors that could lead to rising defaults.

So far, large banks have had limited exposure to office properties within their loan portfolios and some have increased cash reserves as a backstop, but there is the possibility that some regional banks with outsized exposure to one sector could experience further difficulties.1 However, the hope is that enough has been done to limit impact and ensure the stability of the financial system, and it appears that lenders have been able to avoid a surge in distressed property sales, at least for now.2

Although the stability of the banking system might not be at risk, there will likely be local impacts. The health of the office sector varies considerably across metro areas and cities.

Commercial real estate is not new on banking regulators’ radar

Regulators have been closely monitoring commercial real estate (CRE) lending since the banking and thrift crisis of 1980s and early 1990s, with the level of scrutiny only increasing in the lead-up to the financial crisis.3 In December 2006, the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, and the Federal Deposit Insurance Corporation jointly issued guidance to “remind institutions that strong risk management practices and appropriate levels of capital are important elements of a sound CRE lending program, particularly when an institution has a concentration in CRE loans.”4

In 2023, the regulatory agencies again published guidance that stressed that importance of maintaining the key fundamentals—with regard to CRE loans—especially those in the office sector, to:

- Maintain strong capital levels

- Ensure that credit loss allowances are appropriate

- Manage construction and development and CRE loan portfolios closely

- Maintain updated financial and analytical information

- Bolster the loan workout infrastructure

- Maintain adequate liquidity and diverse funding sources5

Regulators’ concerns are well-placed, since the aftermath of the pandemic is proving to be particularly challenging to the office sector—the continuation of “work from home” for many office workers has reduced demand at the same time that rising interest rates have made it more expensive to refinance debt coming due.

However, we did not see the expected rise in defaults last year as lenders paid particular attention to point number 6 above and provided extensions and workouts to many 2023 maturities.6 Now with a much larger US$929 billion set to mature in 2024,7 and nearly 20% of those maturities using office properties as collateral,8 the question is whether lender forbearance will continue.

Cities across the United States face drastically different swings in office values

There is no ignoring the turbulence in office properties across the United States. With national return-to-office rates stabilizing at around 50% of their pre-pandemic levels over the past year9 and corporate work-from-home policies more defined, office tenants likely now have a much better idea of their space requirements than they did during the nascent days of the pandemic recovery.10 And as they reassess, some are reducing the square footage of their leases, thereby pushing up office vacancies.11

These fundamental challenges have taken a toll on some office-building valuations, especially compared with other property types within the CRE industry, some of which have fared better than others. Office properties only account for roughly 20% of the total square footage of the overall CRE industry,12 but offices have so far notched the largest value declines since commercial property values peaked in early 2022, falling by 20.2% (figure 1). These have been followed by apartment (–16.3%) and retail properties (–8.4%). Industrial property values are actually at all-time highs through early 2024, up 1% from the previous 2022 peak.13

{kind=link}

Real estate properties are long-term investments and benefit from appreciation over time.14 Even the recent degradation in value has likely not fully erased value gained for those who may have entered into the investment in the late 2010s or earlier.

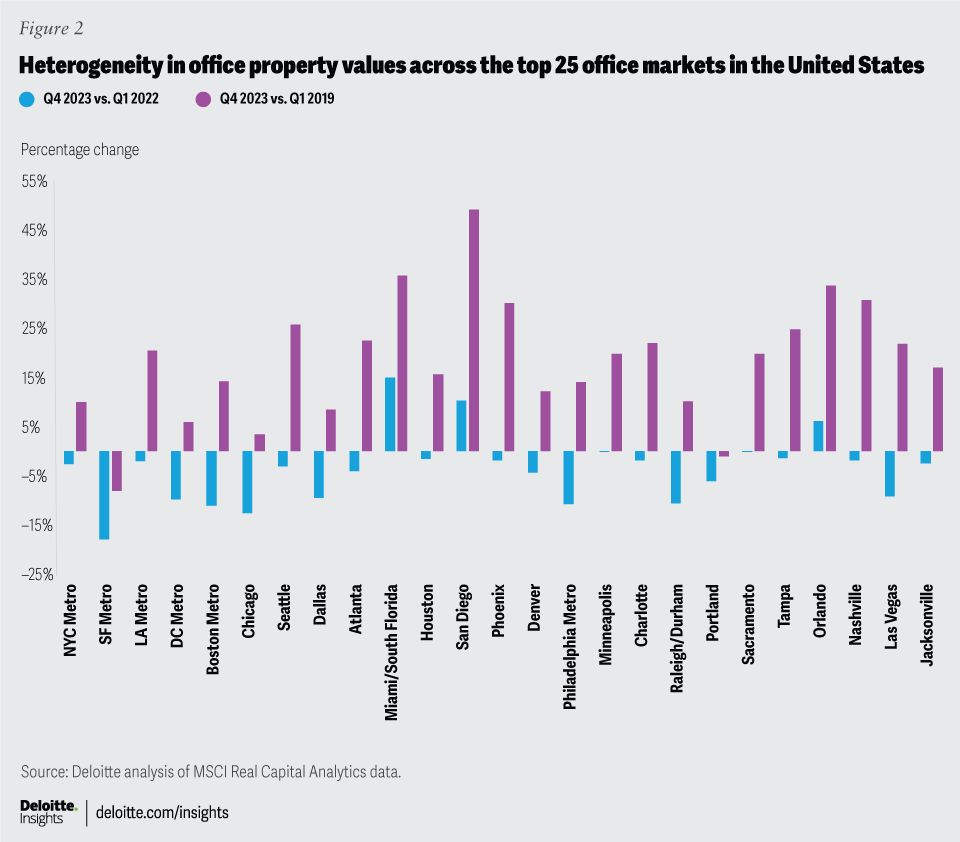

Further, the overall 20% decline in office values comes with a high degree of variance, reflecting the heterogeneity of the existing stock: The value of a newly constructed skyscraper in the heart of New York City is performing far differently from an office park in suburban Dallas. An important distinction when considering any major shift of commercial office property values is that one cannot paint the trajectory of the sector with a wide brush, as evident in MSCI Real Capital Analytics’ commercial property price index (CPPI).15

New York City, with over US$421 billion invested into its office buildings since 2001, has been the nation’s top target for office investors this century.16 It has accounted for nearly 20% of all national office investment over the past two decades, double that of the next largest office metro, San Francisco. Office valuations in the New York City metropolitan area have exhibited some resiliency and are only down 2.6% since the beginning of 2022, ranking 13 among the top 25, and up 10% from values in 2019 (figure 2). All this despite headlines predicting an impending “doom loop” for the city.17

{kind=link}

San Francisco, on the other hand, has seen 18% valuation declines since early 2022, and 8.2% declines from 2019. This can likely be attributed to the lingering effects of the city’s large concentration of technology tenants more rapidly adopting remote work during the onset of the pandemic, coupled with increased crime rates and quality-of-life concerns.18 Vacancies skyrocketed and building values decreased. The city has since rebounded slightly on the heels of the emergence of generative artificial intelligence, as nearly 20% of the technology’s total talent pool is based in the Bay Area and some large leases by AI companies were signed recently, although office vacancies as a whole still remain at all-time highs.19

Three of the top 25 metro areas—Miami, San Diego, and Orlando—have actually exhibited office valuation growth since 2022 peak values compared to most other cities. Miami has blossomed as a post-pandemic era technology hub, as talent and businesses flocked to the warm weather and lower tax burden.20 San Diego has similarly benefitted from technology company relocations to the area, adding additional players to the city’s already diverse tenant base, coupled with some notable vacant office property conversions for alternative uses.21 Orlando, despite some large blocks of vacant space and significant move-outs of late, has weathered the storm, thanks to strong foundational marketplace demographics. The metro has a diverse set of industry sectors across technology, hospitality, and health care, coupled with a strong pipeline of young talent from surrounding universities.22

With property tax comprising a substantial component of city revenues—approximately 30% of local general revenue23—the drop in office-building valuations experienced in most of these large metro areas could present challenges to their local governments. There is also the likelihood that fewer office workers in certain office-dense neighborhoods could translate into less demand for ancillary services such as restaurants, parking, and dry cleaners, further denting local government revenues.

Looking forward

With lenders showing patience thus far, the prospect of lower interest rates offers hope that the office segment of CRE can stabilize. Deloitte’s most recent economic forecast assumes two decreases in the federal funds rate of 25 basis points in the second half of this year with an additional four cuts anticipated in 2025.24 This could provide more favorable refinancing options and help “unfreeze” capital, providing some headroom in the wave of maturing loans and potentially contribute to the revitalization of the property transaction market.

The office sector is clearly in a rebalancing phase and could face more consolidation should value declines continue in some regions of the United States in the near term. But some office building owners are being proactive about their occupancy strategies to maintain tenancy and a constant flow of rental income, supporting property values. Landlords are increasingly turning to lease concessions—such as free rental periods or tenant improvement allowances—to help draw in new tenants to their buildings. The average duration of free rental periods offered in new leases has increased to 10.1 months at the end of 2023, up from 6.8 months in 2019. Tenant improvement allowances—funds provided by landlords to make alterations to floor space—are up as high as 52% from levels in 2019.25 These have been combined in lease negotiations with less costly incentives such as access to shared building services (communal conference rooms, gyms, day cares) and flexible square-footage additions/reductions earlier or more frequently during time of the lease. These incentives must all come with a balance however, as too many concessions could dig into profitability, offsetting any value gained by adding or retaining a notable tenant.

Some regional applications of these practices are as follows:26

- In New York City, some tenants have received up to 24% of their annual rent back as a concession.

- Boston landlords have upped free rent periods to 7.4 months and allowances of up to US$109 per square foot.

- In Washington, D.C., some free rental periods topped 24 months.

Converting underutilized office space for alternative use, such as for apartments or hotels, has also been employed to some effect across the country, reaching a record of 18.8 million square feet in 2023.27 However, given the high cost and complexity of converting office buildings to other uses, it is unlikely that metro areas will notice a substantial improvement to their fiscal situations from this tactic without substantive incentives or credits.28

We realize that any office recovery will be uneven. Some metro area skylines may look far different than their pre-pandemic state once the dust settles.