Lessons from pioneers to help shift failures to successes

Those who have already attempted to move the needle realize that at least part of their strategic processes used in core modernization may need to be refreshed to overcome perceived obstacles and improve success rates.

Minimize internal conflicts with an operating model redesign

The importance of aligning stakeholders to approaches and solutions has been highlighted as one of the biggest lessons learned from prior transformation execution. More than three-quarters of respondents believe better integration between business and IT is the most crucial element to the success of future modernization efforts. Ambitions often don’t translate into achievements due to function misalignment between the two groups—both business and IT know they need to minimize the friction, but often each strongly believes the fault lies with the other party.

Many carriers still work in functional and business unit silos. To achieve better cohesion, they can consider developing a value-stream structure that cuts across products and functional units. A value stream is a cross-functional team and body of work designed to deliver a specific set of business objectives; it is a sequence of steps used to deliver value, from the trigger of an important event to the delivery of value. It contains the people who do the work, the systems, the flow of information, and the alignment of business capabilities.

This construct can help pioneer a broader enterprise mindset and brings together a diversity of skills, knowledge, and experience. Given budget and authority as well as a multiyear time horizon to implement a solution or solve a business problem, this paradigm endeavors to alter company culture by dispersing siloed thinking and foster truly customer-oriented thinking.

Better alignment around modernization initiatives may also help enhance change management efforts, which could alleviate some of the concerns over the impact to talent, including challenges that may arise with training on new tools and processes, shifting long-standing mindsets, and minimizing difficulties in using new technology.

Core modernization business case design

Another significant barrier respondents said they need to overcome in core modernization initiatives is the dogma of high cost with insufficient RoI, as many carriers tend to assess payback on purely monetary terms—modernization spend versus incremental revenue or profits in a predefined time frame.

Instead, carriers should consider adopting an economic-evaluation perspective. This notion encapsulates elements such as improvement in speed to market, greater business agility, enhanced customer experience, and the ability to tackle legacy debt. Such benefits can be difficult to quantify in purely financial terms. However, the competitive advantages that come with accommodating personalization, flexibility, and rapid new product rollout could potentially in turn boost revenue over the medium-to-long term.

An enterprisewide Agile operating model

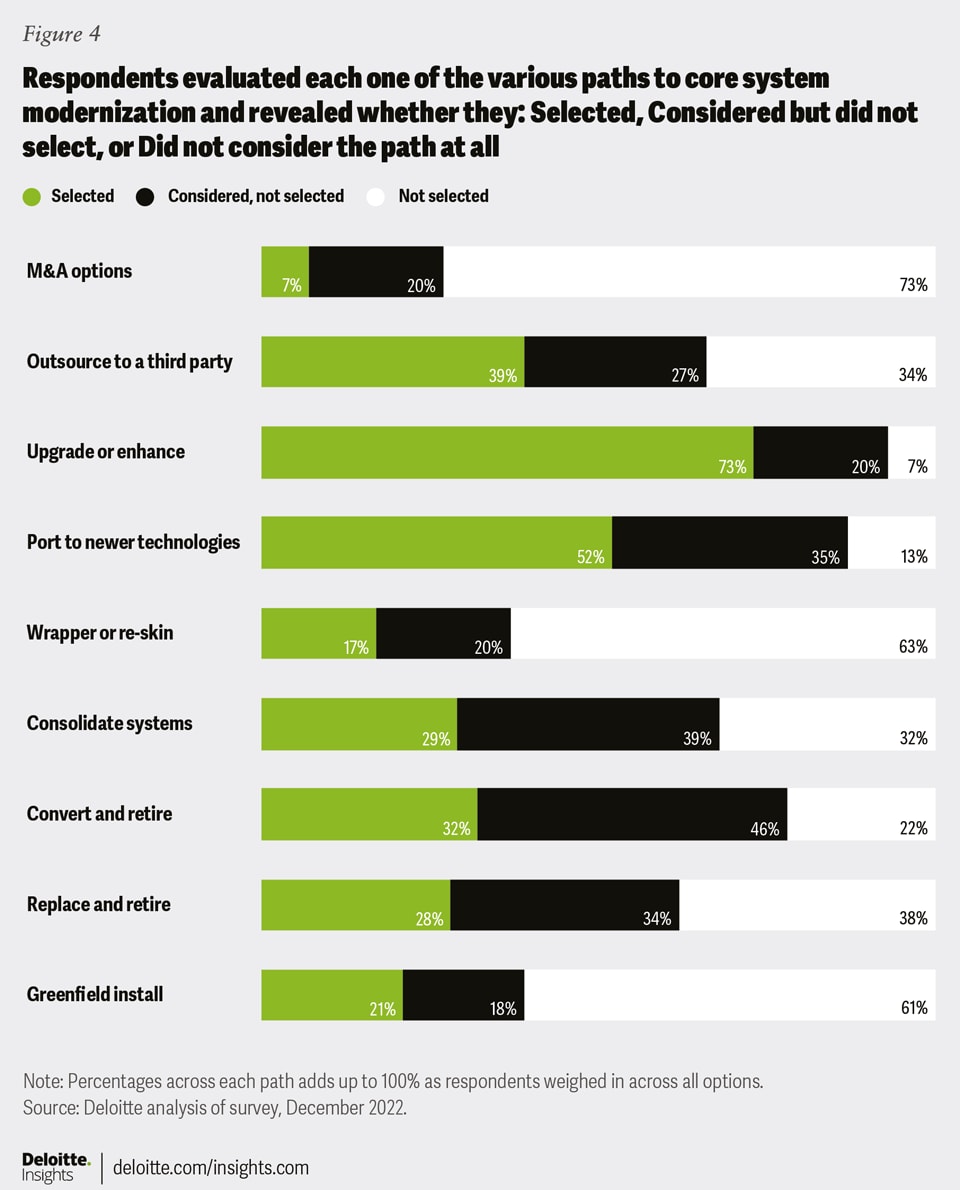

Given underwhelming success in implementing large-scale solutions in the past, 61% of respondents also believe smaller, incremental upgrades or replacements are a more pragmatic approach to modernization than overhauling everything at once.

Many insurers already use Agile methodologies in project delivery and various processes but may now consider scaling Agile across the enterprise.5 This approach could include taking incremental steps, having small autonomous teams, and fundamentally redesigning the organization in a non-hierarchical, outcome-oriented manner.

Derisk with independent due diligence

The process involved in deciding on a modernization approach and potential solution may also need to be reimagined to help derisk the renovations. One step that should be thoroughly addressed prior to undertaking a modernization project, or approaching vendors if third parties are required, is the due diligence to help ensure the full breadth of existing products and systems that will be impacted are fully considered and understood.

Carriers may believe they understand their books of business and legacy systems, but to be certain, they can consider using specialized solutions to perform independent, unbiased, and in-depth due diligence before selecting a particular platform or solution. Several InsurTechs have developed such specialized solutions that allow for validation of the data and an assessment of the underlying complexity of various blocks of business to help carriers assess the requirement needs for potential solutions and the feasibility of conversion while minimizing any bias prior to selecting a solution.

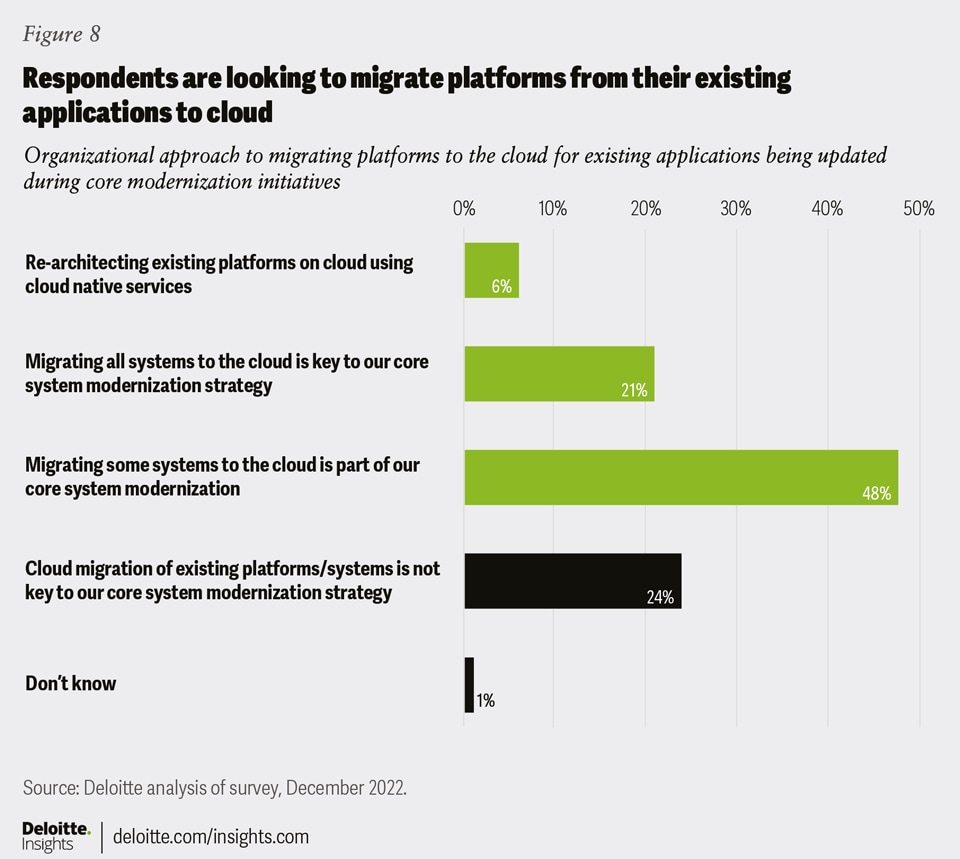

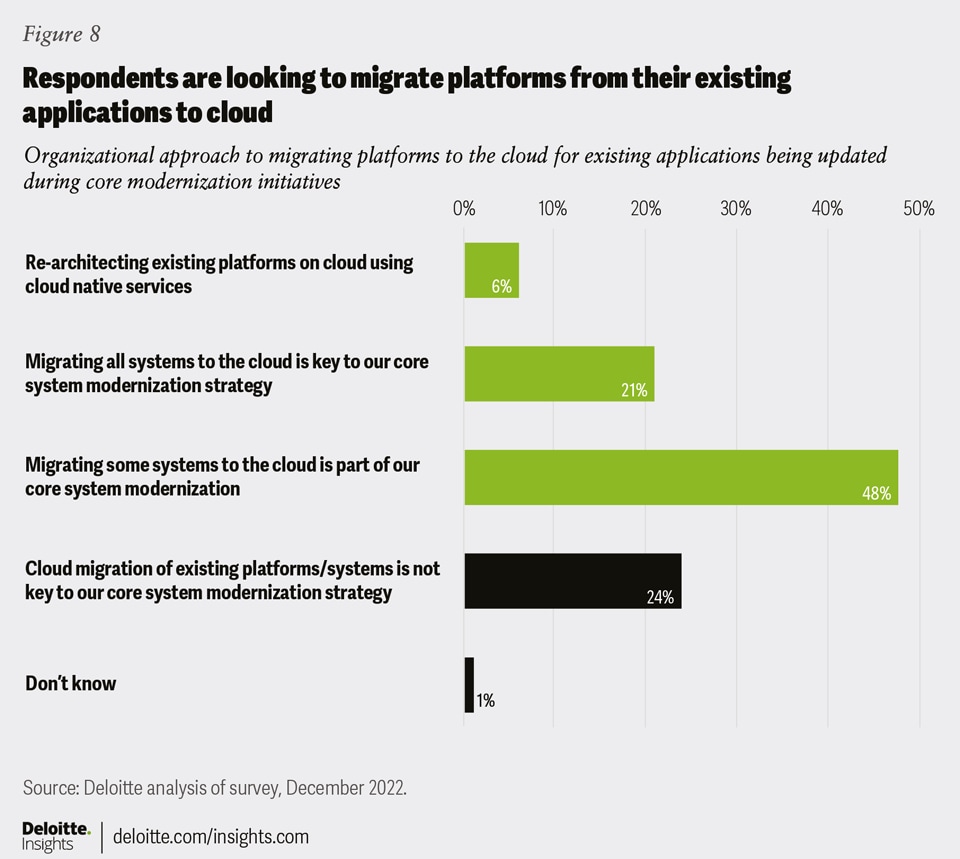

Industry cloud solutions can potentially improve integration patterns

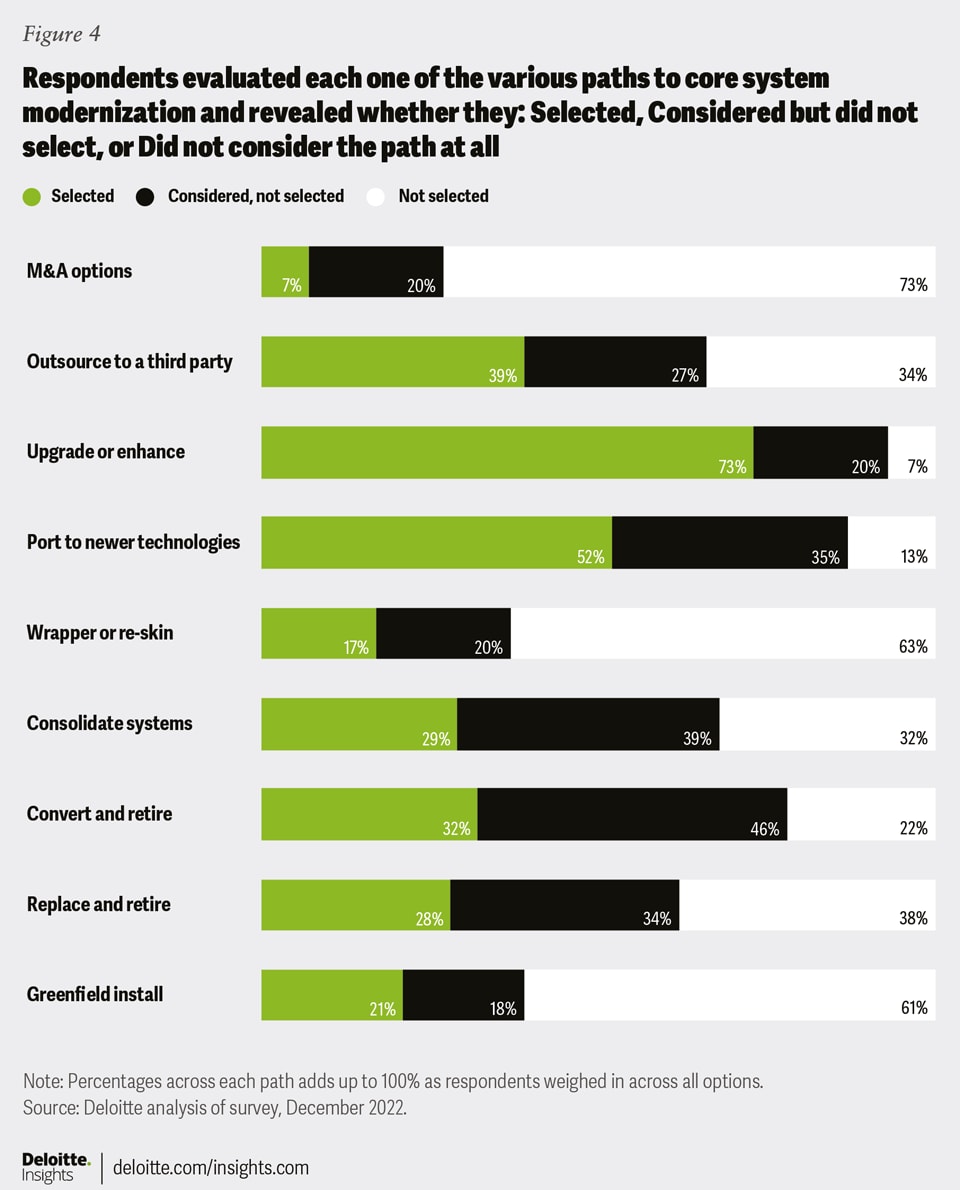

Many carriers have also come to realize that the Band-Aids they have been applying to their legacy systems over time may have created more challenges than solutions. The complexity from multiple layers of core systems and numerous point-to-point integration connections can be expensive to maintain and may impede flexibility, speed to market, and innovation. The situation does not appear to be getting better soon, as 43% of respondents said they do not intend to retire any of their legacy core systems or applications at the conclusion of their modernization initiatives; the number is even greater (77%) in the smallest revenue segment.

The merits of decluttering should not be minimized. However, for carriers that intend to preserve legacy technology but still want to improve the integration patterns and data extraction from monolithic back-end core systems, one path to consider is a prepackaged, cloud-based data extraction and integration layer that comes with common prebuilt application programming interface (API) and near real-time data-extraction processes from common legacy core applications. This solution doesn’t compromise business continuity and potentially offers easier scalability, greater agility, lower IT operating costs, and increased security.

Penetrating uncharted territory

“If you want something you have never had, you must be willing to do something you have never done.” —Thomas Jefferson6

Capabilities for digital-first, digital-native, ease of doing business, seamless processing, rapid product rollout, and omnichannel presence are moving from consumer and producer aspirations to expectations from L&A insurers. With new and more effective systems and platforms for core-process capabilities now at their disposal, insurers can benefit from fast, predictable, and transparent application and underwriting processes, as well as the ability to nimbly and swiftly launch and cross-sell products in response to rapidly evolving needs and expectations.

However, the existence of such solutions is likely only the tip of the iceberg. Having experienced largely lukewarm success from previous initiatives, it may also be necessary for L&A insurers to transform traditional mindsets, culture, and business models to reimagine an effective and impactful path to modernization and forge forward to participate in the future of financial services.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}