Key strategies

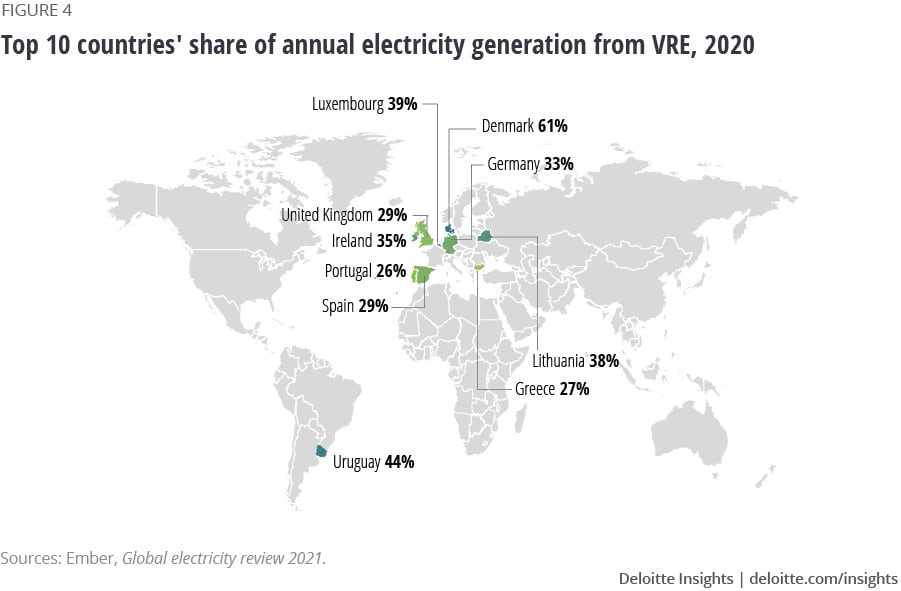

Redesigning markets: In 1999–2000, Denmark cocreated the Nord Pool power exchange, a market that helps its 16 member countries balance electricity supply and demand.23 The country also maintains four ancillary/balancing markets. In 2006, Denmark began requiring its combined heat and power (CHP) plants to settle at market prices, effectively transforming them into flexible resources to balance increasing wind output.

Tapping into dispatchable distributed energy resources (DER): Denmark has a sophisticated demand response market based largely on CHP systems, which produce nearly half of the country’s power. Fueled by gas, biomass, and waste, the CHP systems can respond to market pricing and balance output against varying wind generation. The country also encourages new DER, such as heat pumps and electric vehicles (EVs), to provide storage for excess wind output.24

Expanding/optimizing transmission: Denmark has interconnections that allow it to sell excess wind output to neighboring countries, or source its entire peak load from them if needed.25 Its electricity system operator proactively plans new transmission capacity anticipating future interconnection of wind farms.

Accessing dispatchable centralized generation resources: Denmark’s conventional power plants are designed for hourly ramping and daily cycling to quickly adjust to fluctuating output.26

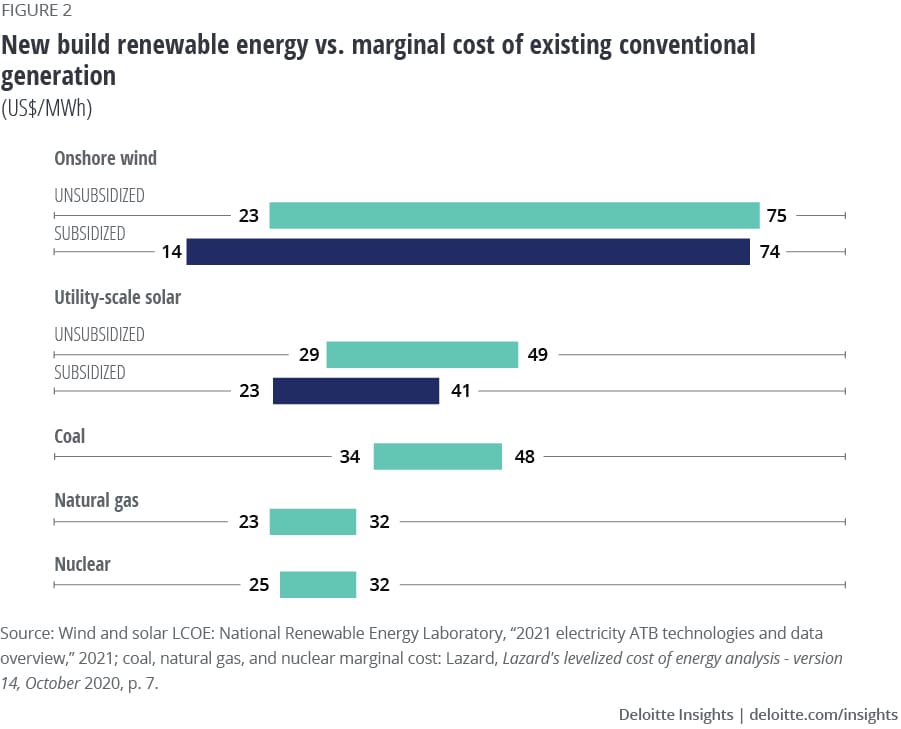

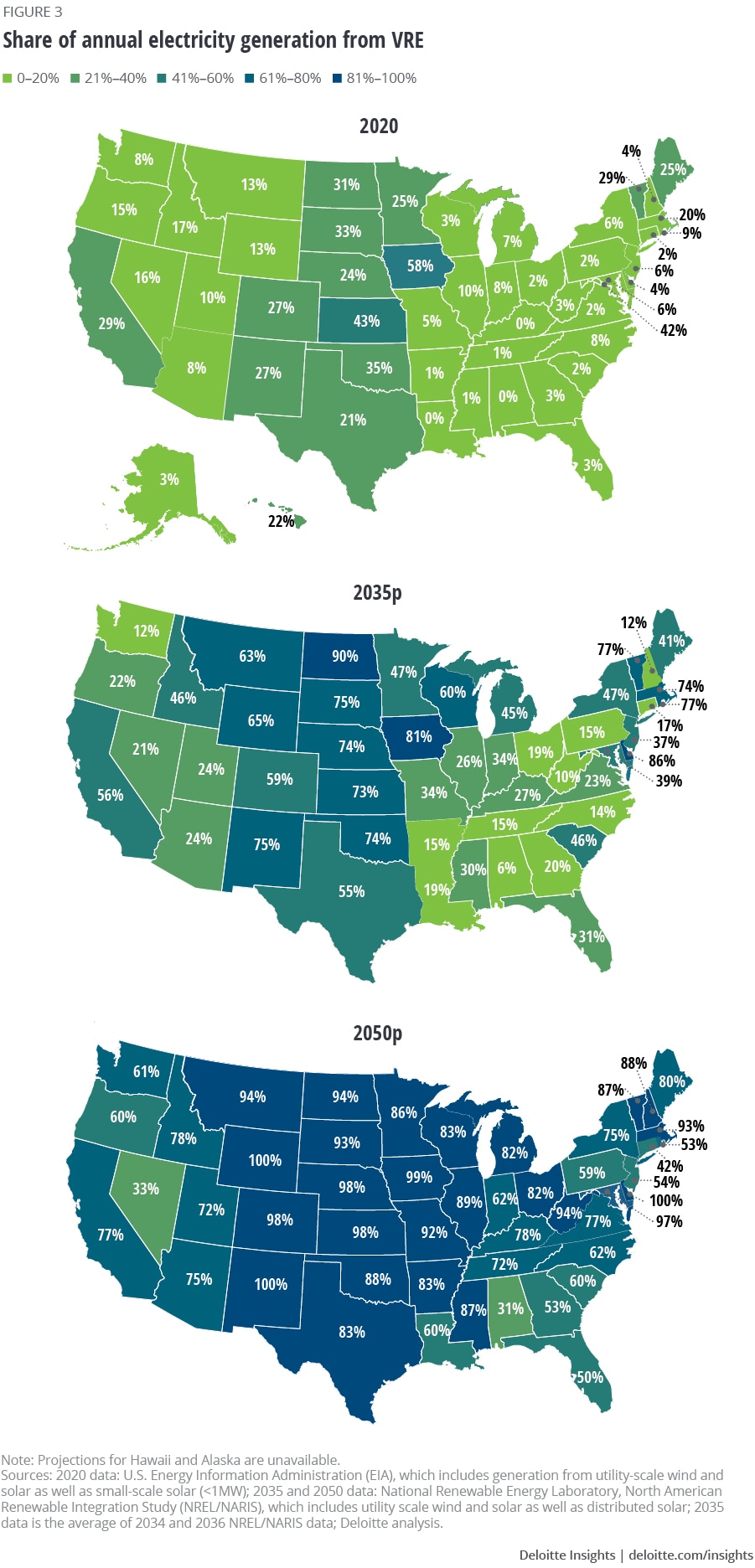

Iowa (VRE penetration: 58%)

Key strategies

Regional and interregional coordination: Iowa is part of the Midcontinent Independent System Operator (MISO), which delivers power and operates a wholesale electricity market across 15 states and one Canadian province. MISO’s real-time and day-ahead markets help balance electricity supply and demand throughout the midcontinent.

Expanding transmission: MISO’s 66,000 miles of transmission lines connect Iowa to resources across the region and to neighboring grids,27 enabling operators to send excess wind output or access additional energy as needed. The proposed SOO Green HVDC Link would link wind resources across Iowa to northern Illinois and connect MISO to mid-Atlantic grid operator PJM, further expanding those capabilities.28

Accessing centralized generation: Iowa’s 11.7 GW of wind generation capacity29 are part of 199 GW of generating capacity of all types within MISO.30 Diversified resources across a large geographic region help enable smooth integration of Iowa’s wind output. Studies show that MISO needs almost no additional fast-acting power reserves to back up the wind power on the system.31

Deploying energy storage: Iowa has approximately 6.9 MW of utility-scale battery storage32 and another 415 MW in the queue as of May 2021, while MISO has 5,625 MW in the queue.33 Green hydrogen producers are exploring production potential in Iowa, due to the abundance of low-cost wind and increasing solar output needed to produce this long-term energy storage resource.34

California (VRE penetration: 29%)

Key strategies

Improving forecasting: Recent extreme heat waves have caused electricity demand to exceed resource adequacy and planning targets. The California Independent System Operator (CAISO), the California Public Utilities Commission (CPUC), and the California Energy Commission (CEC) are collaborating to modernize load forecasting and resource planning to anticipate extreme climate events, while accounting for the state’s transition to a cleaner but potentially more variable energy resource mix.*35

Planning/optimizing location of DER: The CPUC requires the state’s investor-owned utilities (IOUs) to file and update distribution resource plans annually, which identify optimal locations for deploying DER.36 This helps the CPUC assess where DER, such as EV charging stations, can be added without costly upgrades and/or lengthy interconnection studies.37

Regional coordination: CAISO offers the Energy Imbalance Market as a real-time, energy-only market for participants anywhere in the western United States to buy and sell energy when needed. CAISO can send excess solar output to other states and potentially tap their resources when needed through this market.38

Deploying energy storage: The CPUC set targets for California’s three largest IOUs to procure and install 1.325 GW of energy storage by the end of 2020 and 2024, respectively. The IOUs exceeded the target, procuring 1.5 GW of storage by end 2020. The state set an additional target for IOUs to procure 500 MW of distributed energy storage systems.39 Additional storage can help integrate growing VRE generation.

Note: *While some have attributed California’s electricity supply shortages to VRE, the causes appear more related to demand surges from unprecedented multistate heat waves coinciding with wildfires that constrained transmission and triggered systemwide failures (for more details, read Ken Silverstein, "Green energy is not among the culprits behind California's energy crisis," Forbes, September 8, 2020). Nevertheless, California’s plans to prevent future shortages include accounting for the state’s changing generation mix.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}