The next set of imperatives for CFOs in the Asia-Pacific region

Insights from the Asia-Pacific CFO Survey 2023

Introduction

Seventy-one percent of CFOs surveyed in Deloitte’s Asia-Pacific CFO Survey 2023 have seen a broadening of their responsibilities due to increased demands to lead transformation initiatives.

That’s hardly surprising. In the current global business landscape, organisations worldwide find themselves navigating a terrain marked by economic fluctuations, slowing growth, surging inflation, and elevated interest rates. Simultaneously, the imperatives of digitisation and the urgency to respond proactively to climate change have ushered in an era of profound transformation. These next few years will be defined by change, and how organisations strategically adapt to these evolving realities will determine their resilience in the face of uncertainty.

In this backdrop of unprecedented change or “business as unusual,” the modern chief financial officer (CFO) emerges as a pivotal player with an elevated role and recalibrated priorities. Emerging environmental, social, and governance (ESG) regulatory mandates worldwide are reshaping the landscape of financial reporting. Amid this disruption and uncertainty, opportunities abound, and the CFO’s role in capital allocation now blends fiscal prudence, ensuring operational sustainability, with the pursuit of growth objectives, all while continually reassessing underlying assumptions.

CFOs are grappling with a diverse array of pressing concerns, from pursuing sustainable development goals (SDGs) and ESG initiatives to navigating cutting-edge IT technologies and geopolitical risks. In these transformative times, CFOs and their financial organisations must adapt and enhance their systems and structures to fortify their readiness for new roles that lie ahead.

Naturally, the priorities and readiness levels of CFOs across the Asia-Pacific region vary as they embrace and operate within the broader contours of their evolving roles. Our inaugural study analyses regional trends in the finance function, focusing on the unique markets of Australia, China, India, Japan, and the Southeast Asia (SEA) region. Our aim is to understand CFOs’ priorities, assess how the evolving landscape impacts their roles and responsibilities, and evaluate their state of preparedness for the imperatives of the future (for more on the survey, see the sidebar, “Methodology”).

Methodology

Deloitte’s Asia-Pacific CFO Survey is an annual survey that explores the sentiments of leading CFOs in the region. In this inaugural edition, we surveyed 276 CFOs in the region to better understand their challenges, priorities, and ways they are navigating the future. The survey was conducted across five economies in Asia-Pacific, namely, Australia, China, India, Japan, and SEA, between June and July 2023. Seventy-two percent of the sample is composed of chief financial officers from companies with revenue over US$100 million, and the sectors surveyed were financial services, life sciences and health care, manufacturing, public sector, TMT, energy and resources, and consumer business.

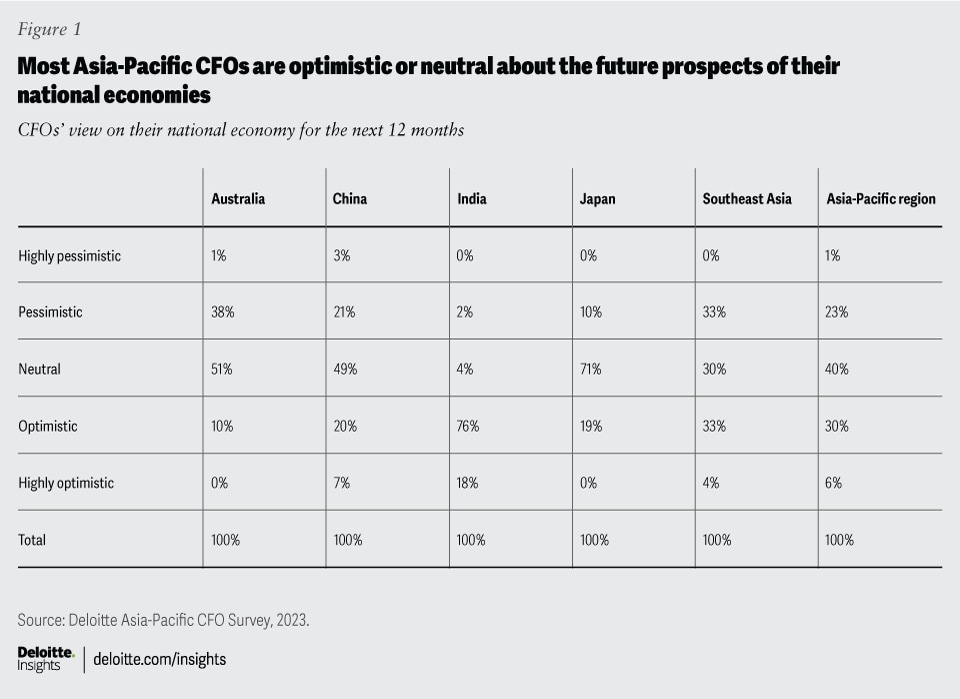

Outlook for national economies and businesses

Meet the trailblazers: Thirty percent of Asia’s CFOs see the horizon through the lens of optimism. An impressive 76% of CFOs surveyed in India expressed confidence in their nation’s economic future.

However, amid this optimism, there also exists a chorus of neutrality. In Japan, for example, a substantial 71% of CFOs take a measured stance, acknowledging the intricate nuances of their economic landscape. Simultaneously, Australia and China find themselves in a state of equilibrium, with half of their CFOs adopting a cautious outlook.

On taking a closer look into different industries, we find differing perspectives to the overall sentiment. For example, 39% of CFOs from the technology, media, and telecommunication (TMT) industry are optimistic about the future outlook of their national economies, whereas only 17% of CFOs from the energy and resources industry share the same optimism.

Overall, optimism and neutrality outweigh pessimism (figure 1). CFOs across Asia-Pacific paint a diverse picture, each adding their distinct brushstroke to the evolving economic outlook.

{kind=link}

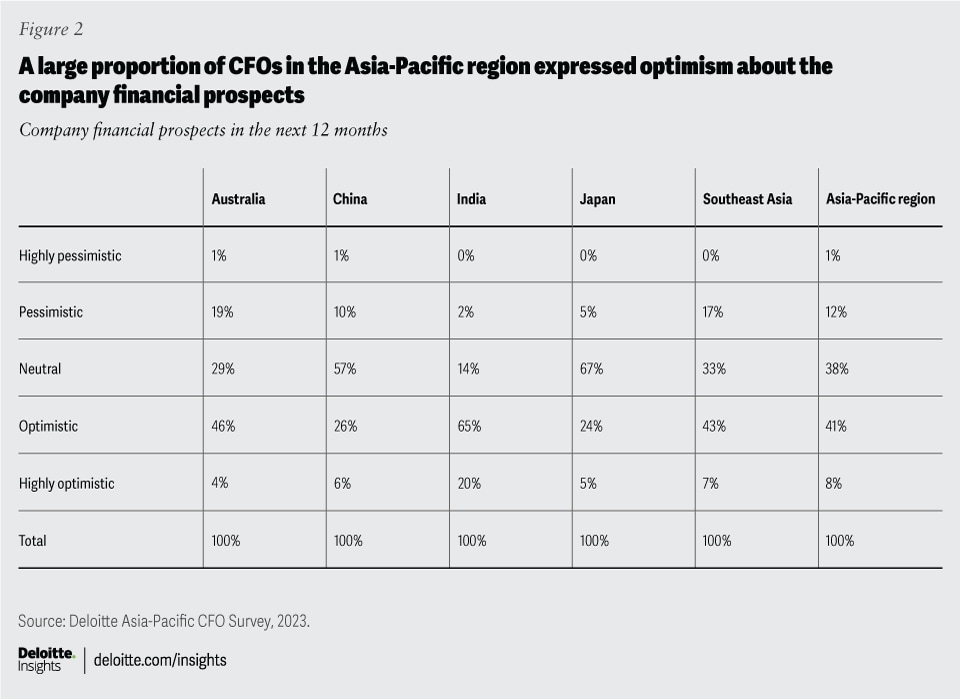

When it comes to their business outlooks over the next 12 months, a higher proportion of CFOs across the region expressed optimism (41%) than pessimism (12%) (figure 2). Sentiments about their company’s financial prospects closely mirror sentiments about the outlook of the national economies. For example, the CFOs’ level of optimism about the financial prospects of their companies is distinctly higher in India, with 65% and 20% expressing that they are optimistic and highly optimistic, respectively. Similarly, a high proportion of CFOs in Japan (67%) and China (57%) expressed neutrality about the financial prospects of their companies. Meanwhile, 46% of CFOs in Australia are optimistic about the financial prospects of their companies, outnumbering those who hold a neutral outlook.

{kind=link}

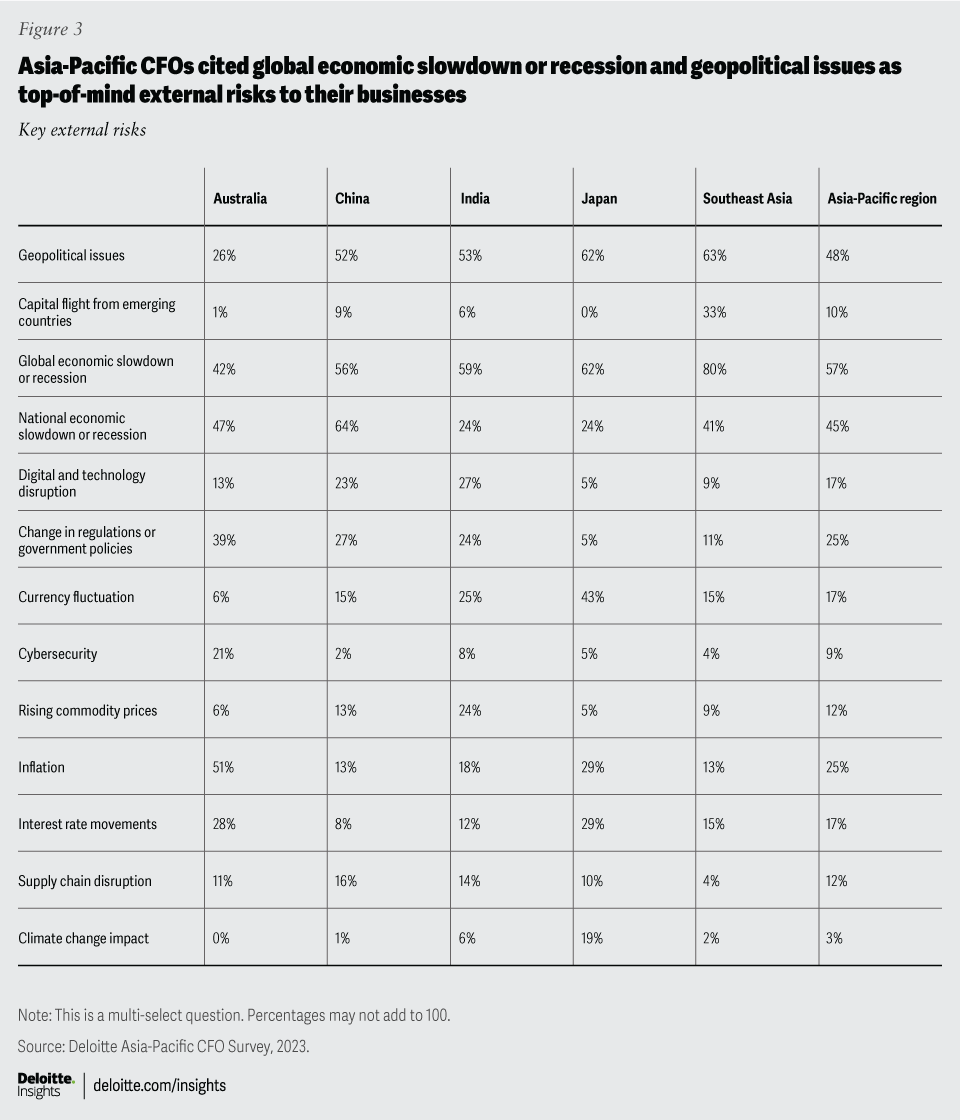

Key external risks: Global economic slowdown tops the list

- At the regional level: Across the Asia-Pacific region, 57% of CFOs viewed a global economic slowdown or recession as the top external risk. Geopolitical issues (48%) and national economic slowdown or recession (45%) follow closely.

- Unique concerns in each market: While the above-mentioned risks hold sway across the region, CFOs in Australia stand out: Fifty-one percent expressed concerns around inflation, while 39% are closely monitoring the impact of regulatory or government policy changes. Respondents in Japan (43%) highlighted currency fluctuations as a significant risk; 27% of CFOs in China expressed concern about the impact of regulatory or government policy changes; and 27% of CFOs in India viewed digital and technology disruption as a significant external risk to their business. When it comes to the SEA region, 80% of CFO respondents were worried about a global economic slowdown or recession, and 33% cited capital flight from emerging countries as a concern (figure 3).

{kind=link}

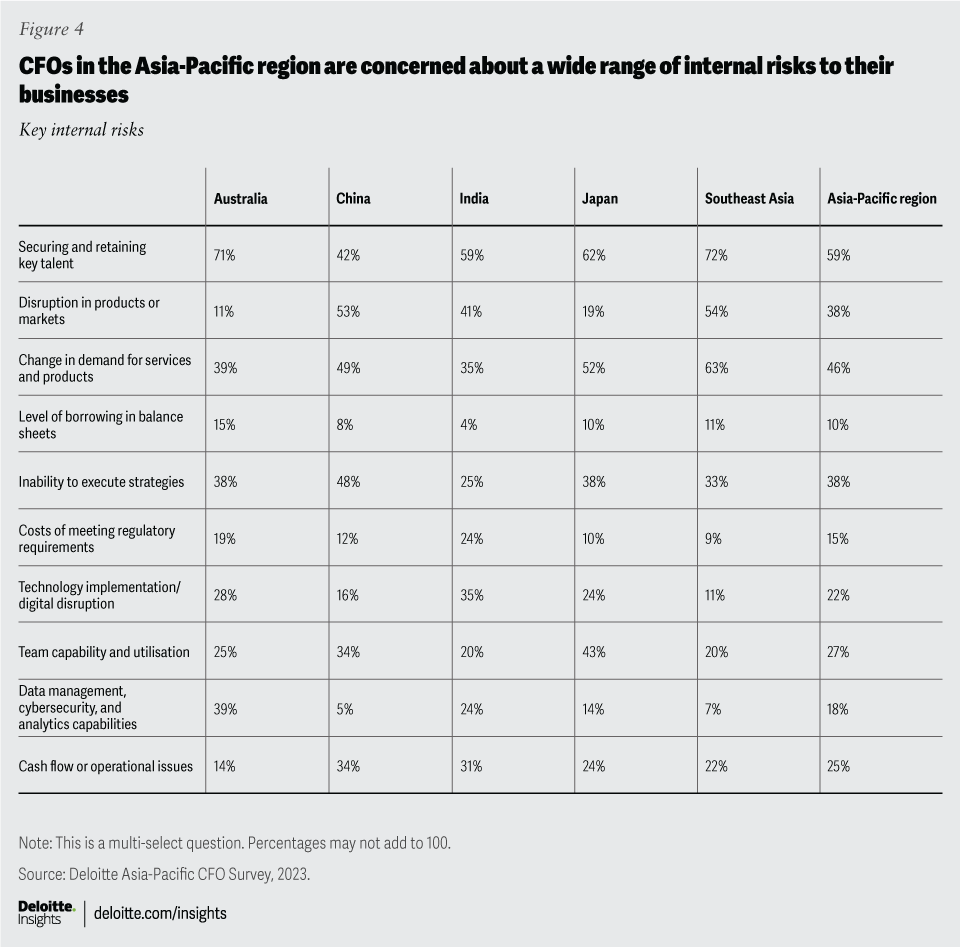

Key internal risks: Talent retention is the top priority

- At the regional level: Fifty-nine percent of CFOs considered securing and retaining key talent as their top internal risk, 46% were concerned about change in demand for services or products, and 38% were concerned about their inability to execute strategies (figure 4).

{kind=link}

- Unique concerns in each market: CFO respondents in Japan (43%) and China (34%) viewed team capability and utilisation as an internal risk. CFOs in Australia (39%) emphasised risks associated with data management, cybersecurity, and analytics capabilities, surpassing the regional average (18%). CFOs in India (35%) cited technology implementation or digital disruption as an internal risk.

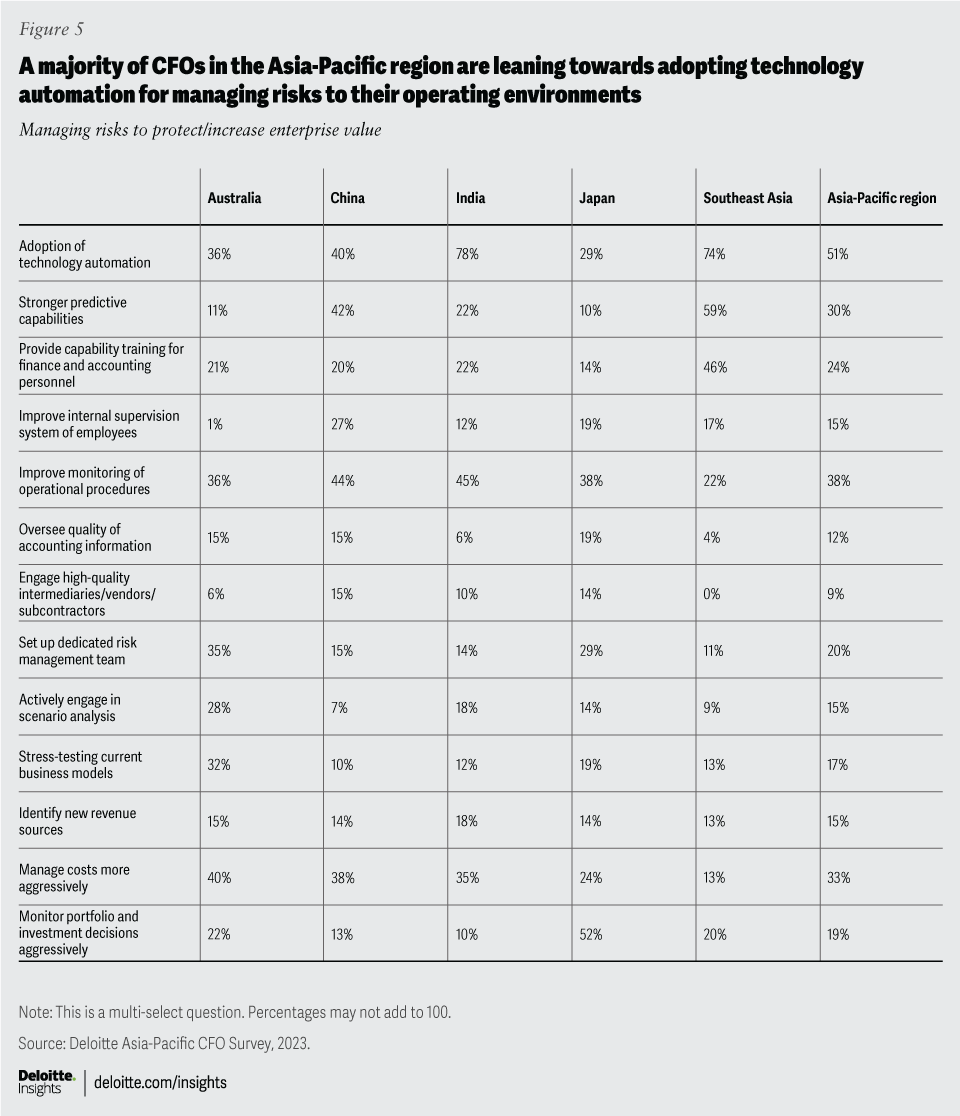

CFOs navigate a spectrum of sentiments and risks, each with its unique story to tell. In terms of managing risks facing their operating environments, at the regional level, 51% of CFOs cited adoption of technology automation as an approach to manage risks, with CFOs in India (78%) and SEA (74%) emphasising it as their favoured approach (figure 5).

{kind=link}

Additionally, 38% of CFOs at the regional level said that they are managing operating environment risks by improving the monitoring of operational procedures, a sentiment echoed by comparable proportions of CFOs in China and India. Thirty-three percent of CFOs at the regional level highlighted managing costs more aggressively, with 40% of CFOs in Australia considering it as their favoured approach. Interestingly, 52% of CFOs in Japan said that they are managing risks in their operational environments by monitoring portfolio and investment decisions aggressively, in contrast to the Asia-Pacific average of only 19%.

CFO focus areas for the next 12 months

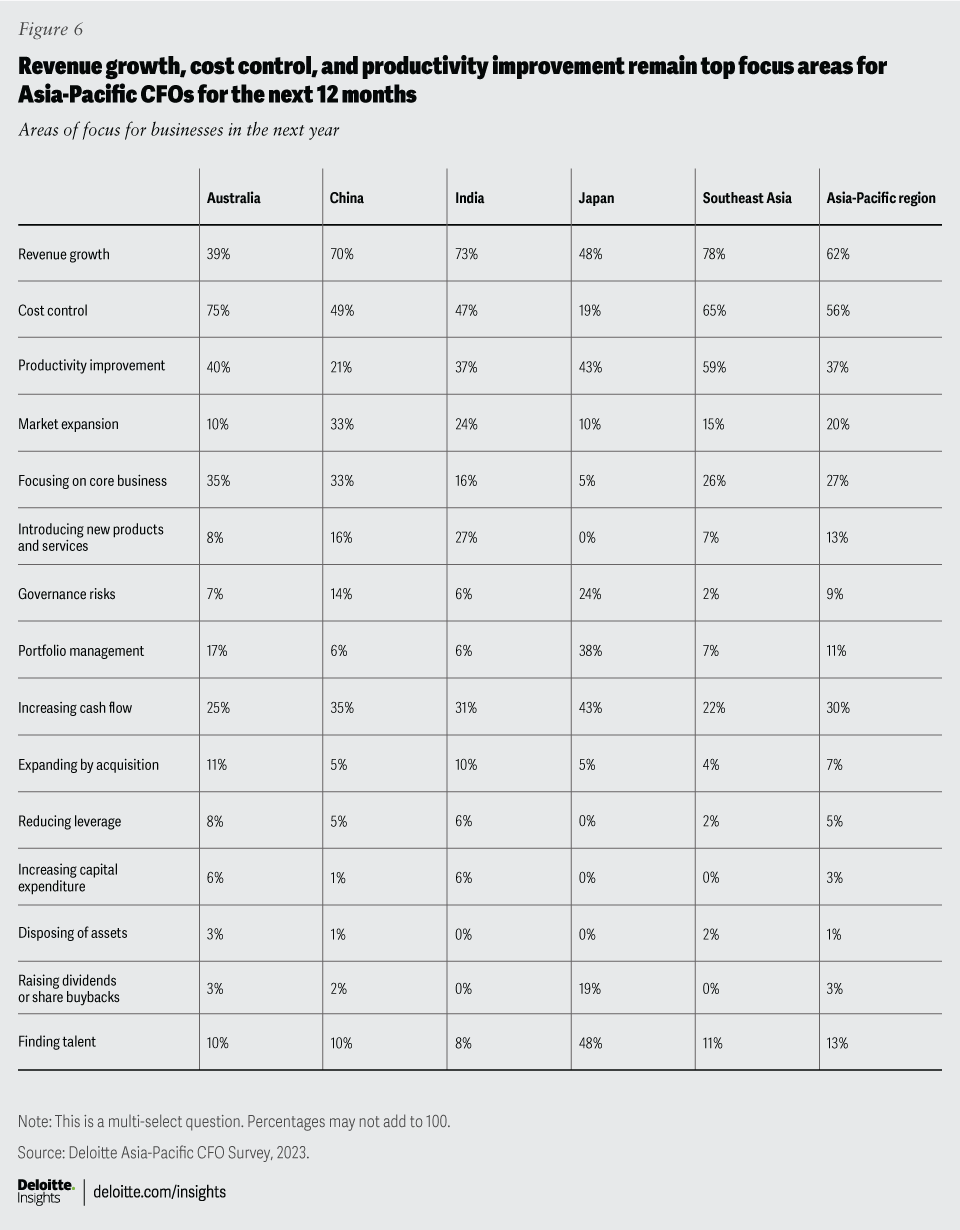

Our survey found that CFOs across the Asia-Pacific region plan to focus on revenue growth (62%), cost control (56%), and productivity improvement (37%) in the next year (figure 6). Across most markets in the region, with the exception of Australia, a substantial number of respondents consistently cited focus on revenue growth as their top priority. In Australia, however, 75% of CFOs cited cost control as their top priority. Priorities do indeed vary across the region. For example, for CFOs in Japan, in addition to revenue growth (48%), finding talent (48%) is a primary focus, which seems to be unique to Japan. For China, while revenue growth (70%) and cost control (49%) remain the top two priorities, 35% of CFOs also said that they would focus on increasing cash flow in the next year, followed by market expansion and core business, at 33% each.

{kind=link}

Changing roles and responsibilities of the CFO

The role of the CFO is now shifting focus from control to influence,1 and CFOs are finding that their role is now less about giving directions and more about aligning incentives and priorities across a variety of stakeholders. This, however, should not be taken to mean adopting a more passive stance; rather, it is about re-examining how CFOs strike a balance between influence and control. Overall, CFOs also believe that a more broad-based mindset or cultural shift is required in finance functions. They particularly noted the need to empower and motivate their finance talent to think more strategically. Depending on the specific context, this may necessitate reassigning team members, encouraging them to participate in cross-functional projects, or helping them to better connect their day-to-day activities with the overarching business strategy.

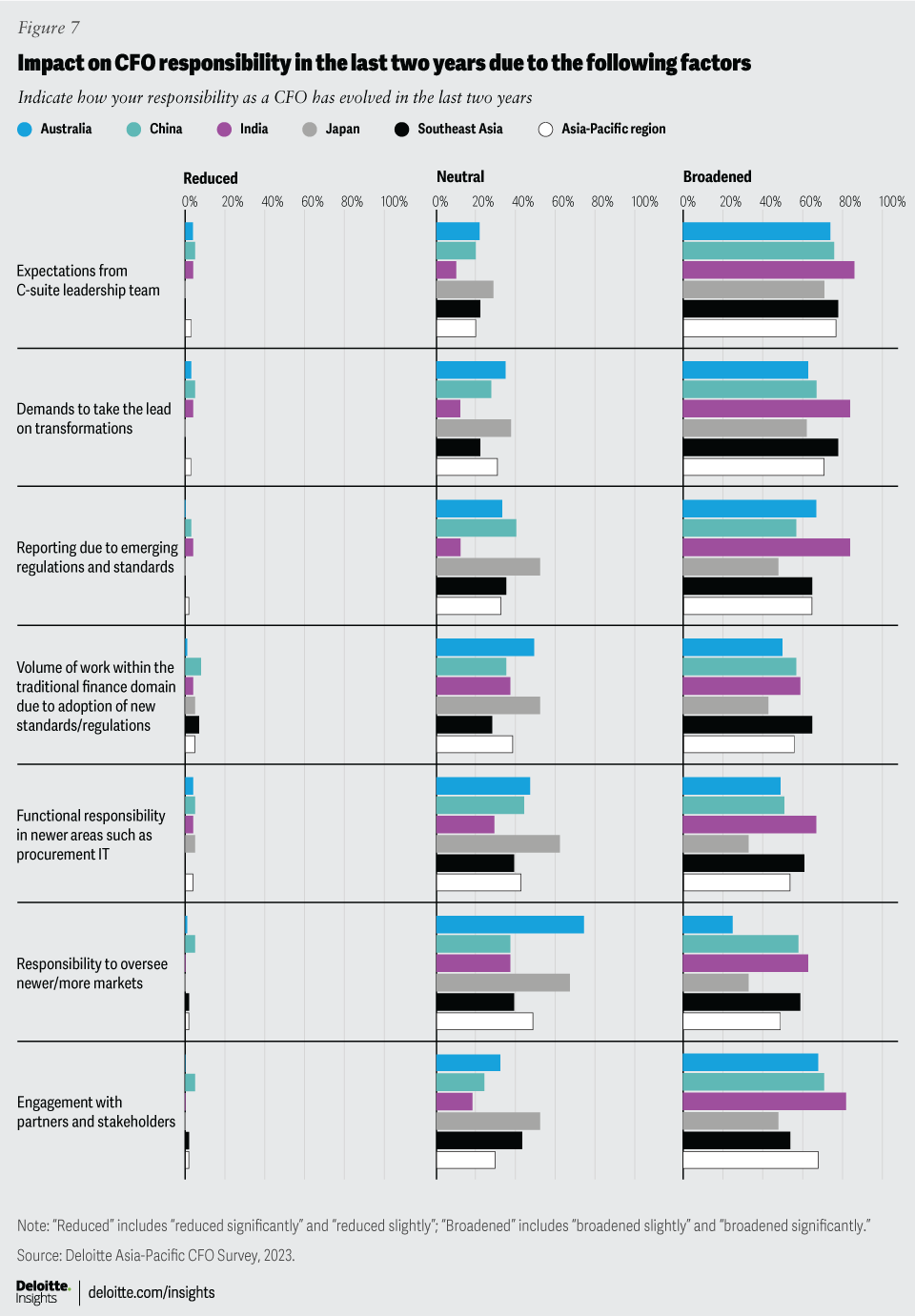

An average of 77% of surveyed CFOs at the regional level said that their responsibilities, in terms of expectations from the C-suite leadership team, have broadened slightly to significantly in the last two years (figure 7). Notably, the regional average is being influenced significantly by 86% of CFOs in India. Industry-wise, too, a large number of surveyed CFOs shared the same view.

{kind=link}

Organisations across Asia-Pacific are focused on various transformations to leapfrog their growth curves and build a more enduring position in the marketplace for the future. At the same time, it is widely acknowledged that, for the transformations to be effective, senior leadership, including CFOs, would need to lead from the front, ensure efforts are coordinated, and act as a lighthouse for the rest of the workforce.

In this context, CFOs have a pivotal role to play in spearheading transformation efforts. A substantial 71% of CFOs in Asia-Pacific have seen their responsibilities expand, in varying degrees, over the past two years when it comes to leading transformation initiatives. Notably, 84% of Indian CFOs have experienced this shift. Across all industries, respondents have witnessed increased demand to lead transformation, with the consumer business industry showing the most significant impact at 84%.

In terms of increased responsibilities due to emerging regulations and standards, 65% of CFOs at the regional level said that their responsibilities have broadened slightly to significantly in the last two years. The burden of reporting seems to be marginally higher on public companies (69%) as compared to private companies (62%). From an industry perspective, CFOs in the energy and resources (78%) and financial services industries (76%) believe that their responsibilities in terms of reporting due to emerging regulations and standards have broadened slightly to significantly in the last two years. This is not surprising as the two industries are already playing a crucial role in helping governments meet their climate targets.

Fifty-six percent of CFOs in the region said that their responsibilities in terms of volume of work within the traditional finance domain due to the adoption of new standards and regulations have broadened slightly to significantly in the last two years, with the highest shift seen in SEA (65%). The trend across industries is similar, with 66%, 65%, and 61% of respondents from the financial services, consumer business, and TMT industries, respectively, echoing the sentiment.

In terms of role expansion, 54% of CFOs in Asia-Pacific said that functional responsibility in newer areas such as procurement-IT have broadened slightly to significantly in the last two years, while 43% maintained a neutral stance. The burden of responsibility in newer areas seems to be higher on private companies (62%) compared to public companies (46%). While CFOs from all industries reported that functional responsibility in newer areas such as procurement-IT has broadened significantly in the last two years, the highest shift was reported by CFOs from the life sciences and health care industry (62%) and TMT (61%).

In terms of increased responsibilities of CFOs to oversee newer or additional markets, nearly half reported a slight to significant broadening of responsibility, while an equal proportion had a neutral stance. The pressure seems to be higher on private companies, with 56% of CFOs from this sector noting an expansion of their responsibilities, compared to only 41% of CFOs in the public sector. This trend of broadening of responsibilities due to oversight of newer/additional markets varied across industries. While 62% and 61% of CFOs from the life sciences and health care, and consumer business industries, respectively, stated the same, 67% from the energy and resources industry and 50% from TMT maintained a neutral stance.

When it comes to the impact of their engagement with partners and stakeholders, 68% of CFOs in the region reported that their responsibilities have increased slightly to significantly in the last two years, with the consumer business being impacted the most (86%).

The survey findings are not surprising. The requirements of a modern CFO to shift from cost management to strategic business partner are broadening, as are the expectations to drive the finance department’s transition from traditional accounting to value creation. The digital transformation of the finance function will eventually lead to a deeper integration of the enterprise’s business and finance functions, which will require partnering and engagement with other teams to achieve the goals.

Spotlighting the emerging imperatives for CFOs in Asia-Pacific

Talent

In this rapidly evolving landscape, where change and uncertainty are the only constants, talent remains the anchor guiding companies into the future. Traditional roles across industries are evolving, with technology advancements poised to disrupt jobs. Yet, it is important to recognise that technology is essentially an enhancer, boosting both innovation and human capabilities. It cannot replace talent. Within this framework, human thought processes and perspectives will be the catalysts empowering firms for a nimble, technology-driven future.

Many companies are re-evaluating their finance operating models, anticipating future business needs while identifying critical talent gaps. Closing these gaps often means looking beyond the traditional boundaries of finance to bring in talent with expertise in data gathering, analysis, and modelling. CFOs recognise the importance of balancing traditional accounting skills with specialised technological capabilities.

CFOs also acknowledge the need to evolve their leadership styles. In response to social movements addressing burnout and overwork, they are embracing a more human-centric approach, demonstrating greater personal empathy. In the Asia-Pacific region, in addition to recent models of working such as remote and hybrid, CFOs grapple with two critical imperatives:

- Attracting and retaining top talent

- Skilling, reskilling, and upskilling of the existing workforce

Key insights on attracting and retaining top talent

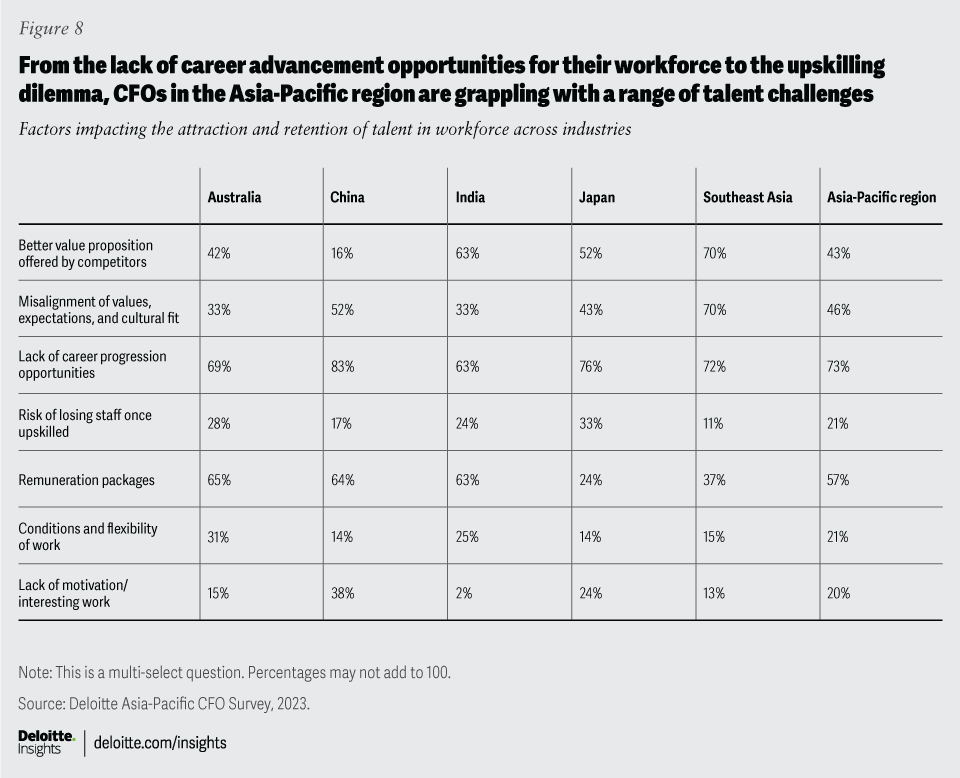

- Career progression: A resounding 73% of CFOs in Asia-Pacific pointed to lack of career advancement opportunities as their primary workforce challenge (figure 8).

{kind=link}

- Remuneration: Regionally, 57% of CFOs regarded competitive compensation packages as a secondary concern, with Australia, China, and India in close alignment.

- Regional variations: CFOs in SEA (70%), India (63%), and Japan (52%) viewed “better value proposition offered by competitors” as crucial to talent attraction and retention, whereas CFOs in China (52%) considered “cultural alignment” to be so.

- Industry lens: Surveyed CFOs across all industries cited lack of career progression as the main factor that impacts attraction and retention of talent. CFOs in the consumer business sector (84%), in particular, are grappling with lack of career progression opportunities; this sentiment resonates strongly across manufacturing, and life sciences and health care industries.

- Upskilling dilemma: Interestingly, the risk of losing upskilled staff is the lowest in the consumer industry (10%) and highest in financial services and TMT (32%).

- Values and culture: Across industries, aside from consumer goods, “misalignment of values, expectations, and cultural fit” takes precedence over competitor offerings.

Key insights on skilling, reskilling, and upskilling the existing workforce

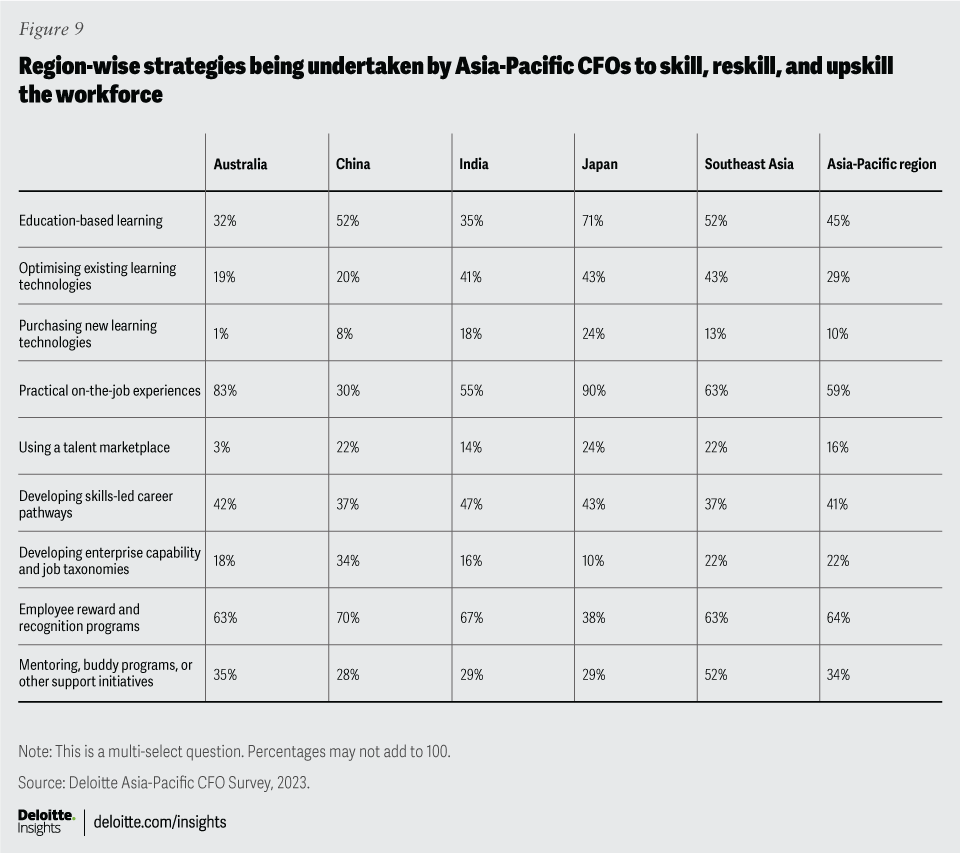

CFOs across the board are seeking to strike the right balance between generalised accounting skills and specialised technological skills in their workforce.2 Fifty-nine percent of CFOs in Asia-Pacific said that they are focused on providing practical on-the-job experience to their workforce to ensure that they build the right capabilities (figure 9). In both Australia and Japan, this strategy takes precedence over the rest, with 83% of CFOs in Australia and 90% of CFOs in Japan focused on providing practical on-the-job experience to their workforce. Moreover, 71% of CFOs in Japan stated that they are providing education-based learning to their employees for upskilling, compared to a regional average of 45%. Interestingly, neither using a talent marketplace nor purchasing new learning technologies was a popular strategy for skills upgrading.

{kind=link}

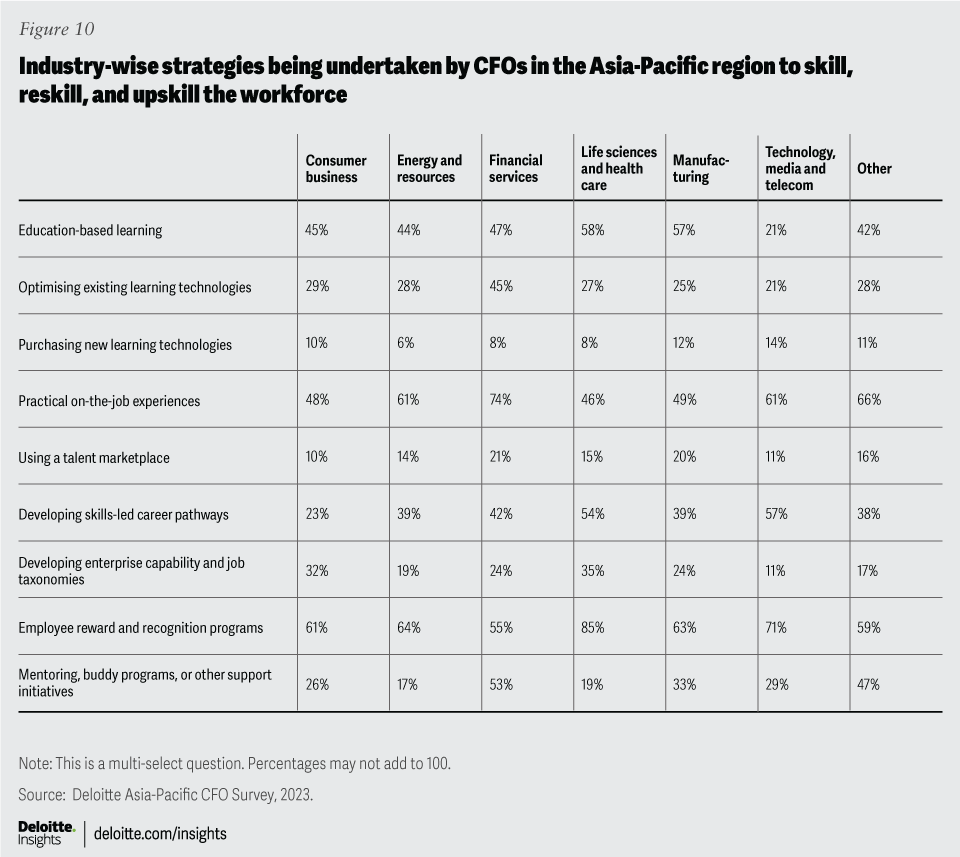

Sixty-four percent of the surveyed CFOs in the Asia-Pacific region said that they are utilising employee reward and recognition programs to motivate their workforce to upskill. Seen from the industry lens, 74% of CFOs in financial services are focused on providing practical on-the-job experiences (figure 10). Interestingly, optimising existing learning technologies did not seem to be a priority for most industries, whereas 45% of CFOs from the financial services industry are actively undertaking this approach to skill, reskill, and upskill their workforce.

{kind=link}

In response to these realities, CFOs will need to update their recruitment and upskilling strategies as they strive to attract and retain a higher-calibre workforce, ensuring competitive compensation and career progression to keep their teams motivated. Balancing generalised and specialised skills, harnessing generative AI, and strengthening data governance for increased trust and efficiencies will be crucial for transitioning and elevating the finance function to a strategic business partner of the C-suite.

Technology

CFOs across the region appreciate the inevitability of technology adoption. Digitisation is becoming a key pathway to realising long-term value. As part of this process, the digitisation of an enterprise’s finance function plays a major role in building a digitally intelligent enterprise. Automation or adoption of digital technology has been a major focus for the finance function. Faced with looming economic uncertainties, the finance function is prioritising stronger predictive capabilities and a more aggressive approach to cost management.

Furthermore, CFOs across the region are using technology as an enabler for their function (figure 11). Fifty-three percent are using technology for electronic invoicing, with China, India, and SEA leading in this strategy. Forty-eight percent of respondents in the region are leveraging this strategy for robotic process automation, while 47% are using it for finance management and mid-end data platform, including CFOs in China and Australia.

{kind=link}

It is interesting to note that a relatively low proportion of CFOs are using artificial intelligence and machine learning algorithms as enablers in finance. Given the potential of generative AI to cut costs, increase efficiencies and productivity, and improve forecasting ability, this low uptake suggests caution.

However, the use of technology continues to vary across the region. Seventy-four percent of CFOs in SEA are using technology for electronic invoicing compared to a regional average of 53%. Similarly, in Japan, 86% of CFOs are using technology for shared operating and service platform, compared to a regional average of 43%. Further, 52% of CFOs from the consumer industry are leveraging big data analytics and processing across the finance function. Take Tata Motors, a leading global automotive manufacturer based in India, for example: The company credits its data-driven approach for helping it overcome the pandemic-induced challenges to its business. This approach provides a vision of how digital transformation goes beyond survival, opening the organisation to brand-new opportunities. Tata Motors plans to incorporate telematics data from customer fleets, route optimisation data, and government regulations to optimise its operations.3

Sustainability and ESG

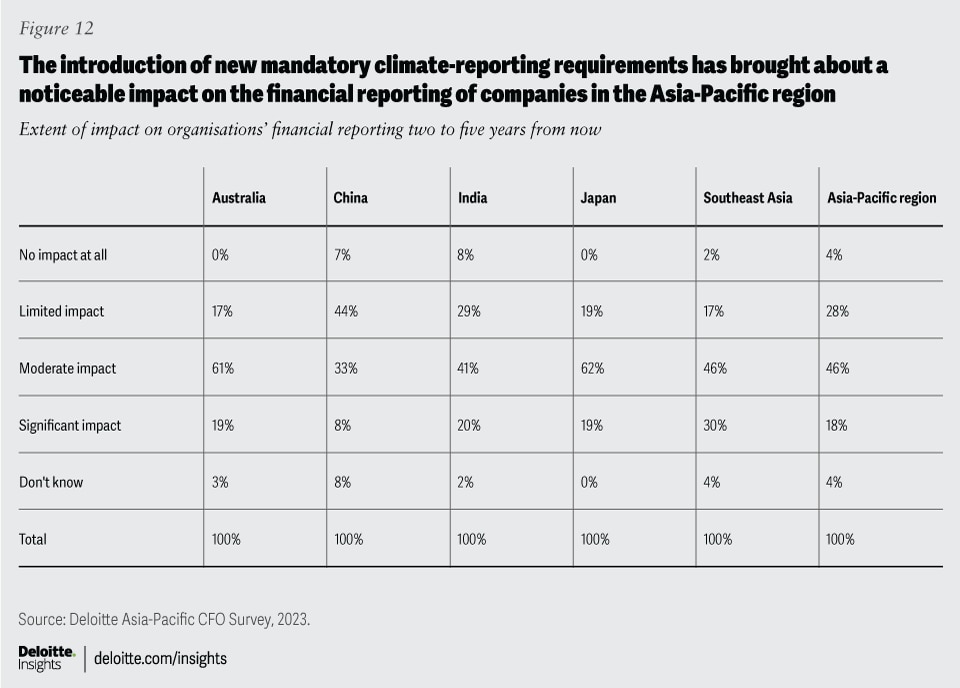

Many companies in the Asia-Pacific region are faced with an urgent challenge: addressing the imperative of climate change. The region’s regulatory landscape is undergoing a transformation as governments and policymakers transition from voluntary disclosures to comply-or-explain disclosures, to mandatory disclosures (figure 12).

{kind=link}

Australia, China, and Singapore, cognisant of their market realities, have initiated a phased approach. For example, in the initial stages, some have prioritised specific sectors and publicly listed companies to comply, while other sectors of the economy are expected to follow suit later.

In light of the new mandatory climate-reporting requirements, 46% of surveyed CFOs in Asia-Pacific believe that these requirements will have a moderate impact, while 18% believe these will have a significant impact on their organisation’s financial reporting within the next two to five years. Survey results show that while high proportions of CFOs in Australia and Japan (61% and 62%, respectively) estimate a moderate impact on the organisation’s financial reporting requirements, 44% of CFOs in China estimate a limited impact. Notably, a higher proportion of CFOs in public companies (54%) foresee a moderate impact compared to only 37% of CFOs in private companies.

This impact varies across industries: CFOs in the energy and resources (56%) and financial services (55%) sectors expect a moderate impact on their financial reporting compared to other industries.

Compliance plans: Bridging the gap

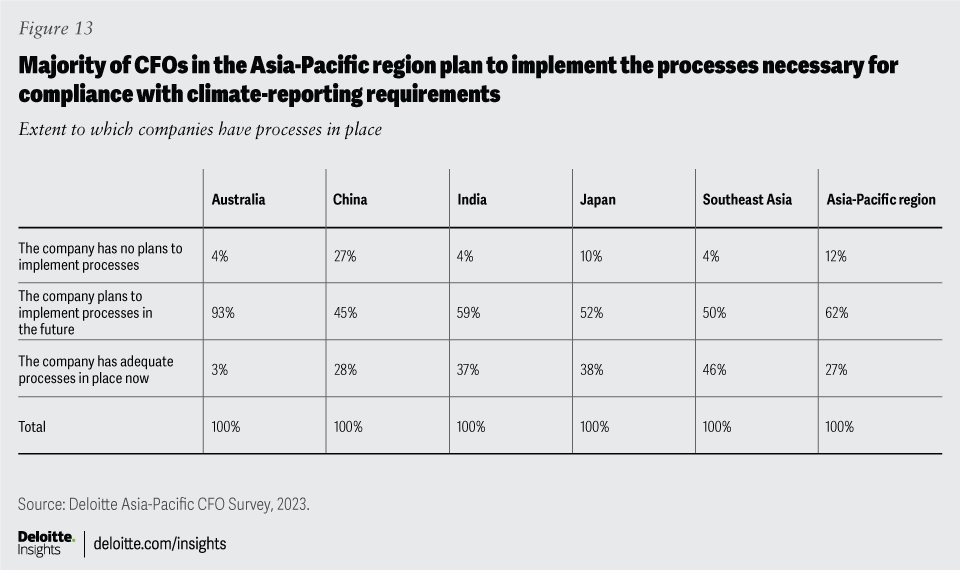

With the introduction of mandatory disclosures related to corporate actions on climate change and sustainability, and considering the extent of preparations required for compliance, survey results show a gap between the perceived burden and the adequate implementation processes in place. When it comes to implementing processes for climate-reporting compliance, currently, only 27% of CFOs in Asia-Pacific report having adequate processes in place, with Southeast Asia leading this statistic at 46% (figure 13).

{kind=link}

At the regional level, 62% of CFOs said they plan to implement the necessary processes in the future, with 93% of CFOs in Australia stating the same. Among CFOs of public companies, 9% have no plans to implement these processes, while 30% have already established them. For private companies, these numbers stand at 14% and 23%, respectively. While 31% of CFOs in the life sciences and health care sector have adequate processes in place, most CFOs across all sectors intend to implement processes in the future.

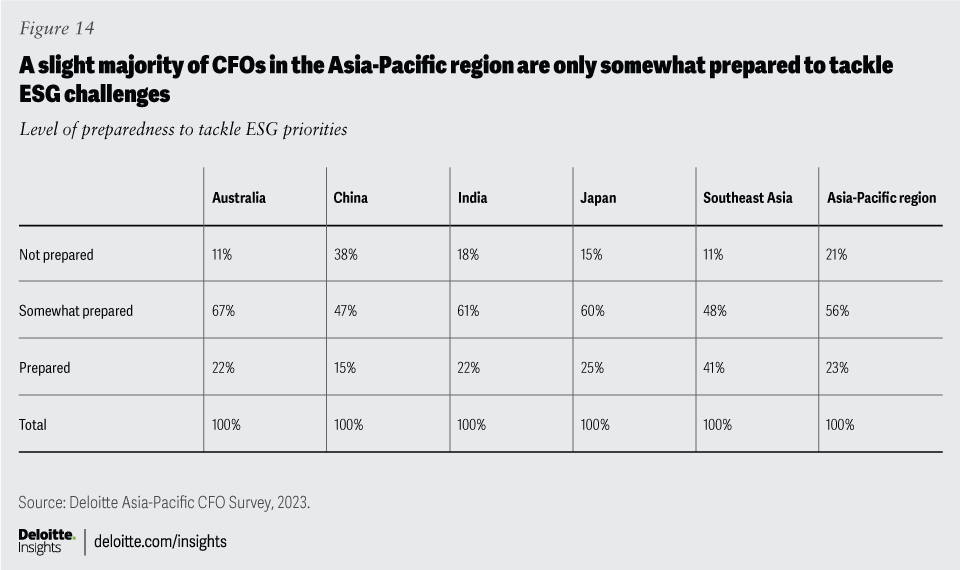

Survey results show that the companies’ level of preparedness to tackle sustainability, climate change, or ESG priorities is disparate. For example, a slight majority (56%) of CFOs in the region are somewhat prepared (figure 14). Furthermore, 38% of CFOs in China stated that they are not prepared versus a regional average of 21%; 41% of CFOs in SEA said that they are prepared versus a regional average of 23%.

{kind=link}

From an industry perspective, the level of preparedness seems the highest in financial services—34% of CFOs from this industry said they are prepared to tackle climate change, sustainability, and ESG priorities. On the other hand, the life sciences and health care industry seems to be the most unprepared—38% of CFOs from this industry said they are not prepared.

While some steps have been taken to address this, the key question now is whether CFOs in the region are well-positioned to meet new mandatory norms and to take proactive voluntary steps towards addressing climate change and sustainability. Survey results suggest that a lot more preparation needs to be done and CFOs will really need to make a significant leap if they are to optimally deliver on their new and expanded roles.

Proactive sustainability initiatives

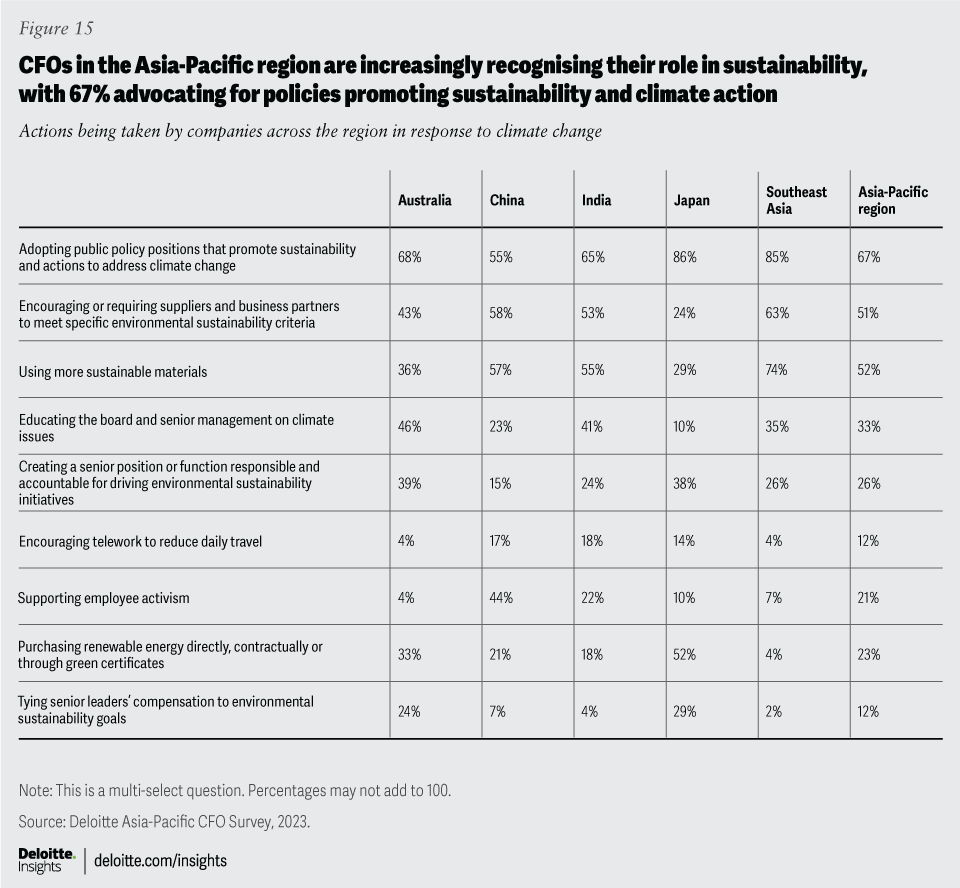

CFOs in the Asia-Pacific region are increasingly recognising their role in sustainability. A significant 67% of CFOs across the region are actively advocating for public policies that promote sustainability and climate change action (figure 15). This proactive approach is particularly strong in Japan (86%) and SEA (85%). Many companies are adopting sustainable practices, with over half of the respondents at the regional level using more sustainable materials and encouraging or requiring suppliers and business partners to meet specific environmental sustainability criteria.

{kind=link}

However, divergent paths continue to persist across the region. For example, 52% of CFOs in Japan said that they are purchasing renewable energy either directly or through green certificates, compared to a regional average of 23% (figure 16). This trend is more pronounced in the energy and resources, and life sciences and health care industries, with 33% and 31% of CFOs, respectively, stating the same. Forty-four percent of CFOs in China, meanwhile, said that they are supporting employee activism versus a regional average of 21%. From an industry perspective, there is high participation from consumer business and manufacturing in using more sustainable material and encouraging or requiring suppliers and business partners to meet specific environmental sustainability criteria. Meanwhile, 58% of CFOs from the financial services industry said that they are educating the board and senior management on climate issues. At a regional level, only 33% of CFOs prioritised this action.

{kind=link}

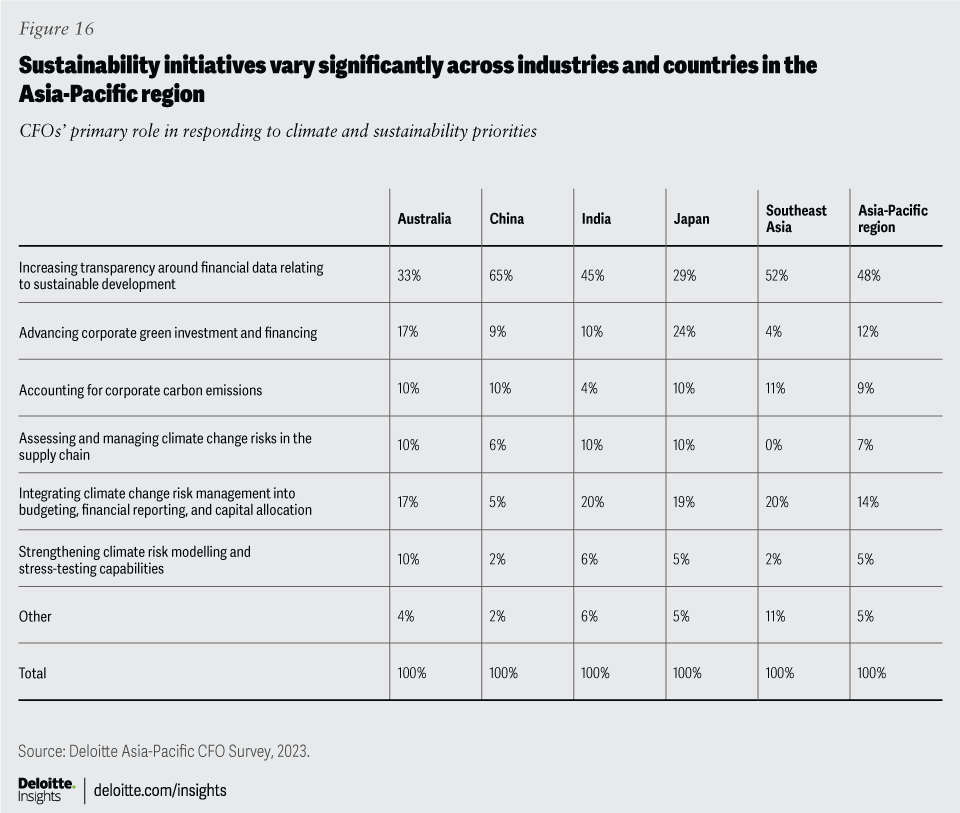

As the reporting landscape evolves and companies make bigger commitments towards climate change and sustainability, the role of the CFO will inevitably evolve and encompass new, and perhaps unique, responsibilities. Forty-eight percent of CFOs in the Asia-Pacific region said that their primary role in responding to climate change imperatives is to increase transparency around financial data relating to sustainable development. A significant majority of CFOs in China (65%) and SEA (52%) shared this view. Another 14% of CFOs in the region said that their primary role would be to integrate climate change risk management into budgeting, financial reporting, and capital allocation, whereas, for 12% of CFOs, the primary role involved advancing corporate green investment and financing.

Industry-wise, 77% of CFOs from life sciences and health care and 55% from manufacturing stated that their primary role in responding to climate change imperatives is to increase transparency around financial data. Further, 17% of CFOs from the energy and resources sector said that their primary role would be to advance corporate green investment and financing, whereas 18% of CFOs from financial services industry and the manufacturing industry each said that their primary role would entail integrating climate change risk management into budgeting, financial reporting, and capital allocation.

Trust and governance

Trust and governance are fundamental to all the other three imperatives of technology, talent, and ESG/sustainability reporting/disclosures. For any process or system transformation to be effective, it must be underpinned by trust and governed by verifiable data. Building trust hinges on robust data governance, particularly in financial reporting and finance digitisation, where ESG or sustainability reporting requires data-backed verification for credibility and substantiation of claims.

As rules and regulations around climate reporting are still evolving and can be fairly disparate across regions, it is challenging for CFOs to comprehensively attain the level of transparency that is required. Currently, the proliferation of multiple sustainability-reporting frameworks and guidelines across jurisdictions and the inconsistent manner in which data is being collected, verified, and reported have created significant disclosure challenges and resulted in poor ESG data comparability.

Further, CFOs in Asia must use data to establish common platforms of understanding and collaboration.4 Given their traditional role as guardians of financial information, CFOs in SEA acknowledged that finance functions may sometimes display a tendency to be overly protective of data. But as CFOs seek out ways to build trust and add value in times of change, a more open stance on data-sharing could go a long way towards establishing common platforms of understanding and collaboration between different business units.

For example, CFOs dealing with shadow finance organisations—where individual business units set up their own “in-house” finance teams in response to the perception that they are unable to receive the support that they require from the central finance organisation—have shared that improvements to data-sharing processes have helped to enhance overall alignment and execution, as these teams become better connected and trusting of the central finance function.

Recognising that the technology, ESG, and talent imperatives need to be built on a robust foundation of trust and governance, countries in the region are taking legislative steps to build such a foundation. For example, in Singapore, overall trust in corporate governance has reached a new high for listed firms in 2022,5 with the 2022 Singapore governance and transparency index6 showing that scores improved across two categories since the index was first compiled in 2009.

Additionally, there are several ongoing industry-level efforts in Singapore to improve trust in corporate sustainability disclosures.7 For example, the Monetary Authority of Singapore (MAS) and Singapore Exchange (SGX Group) have jointly launched ESGenome, a digital disclosure portal where companies can report ESG data in a structured and efficient manner and investors can access this data in a consistent and comparable format. Meanwhile, in Japan, several initiatives that can lead to engendering trust are being seriously taken up by companies. For example, the Japanese Corporate Governance Code and Guidelines for Investor and Company Engagement was updated in 2021, and one of the main revisions calls for the inclusion of “promoting diversity,” which is defined as companies disclosing policies and adopting voluntary targets to promote diversity in senior management through the appointment of women, non-Japanese people, and mid-career professionals.8

Recommendations to navigate the complexities ahead

Changes in technology and regulation are affecting the CFO’s priorities in Asia-Pacific, making the transformation of the finance function a necessity. Achieving a deeper integration between finance, business, and technology is essential for evolution, shifting the CFO role from traditional guardians of data and accounting to value creation. As CFOs in Asia-Pacific navigate this transition, the following four recommendations can help them anchor their efforts and create a robust foundation for the way forward:

1. Enhance organisational strategic agility through stronger scenario analyses

Survey results show that a mere 15% of CFOs at the regional level actively engage in scenario analyses. While CFOs may not serve as the first line of defence in risk management, their roles as custodians of their company’s financial well-being can be expanded to combine strategic risk management with opportunity identification. Balancing risk with opportunity would require enhancing the capability to perform scenario analysis and stress testing, given the strategic need to be more agile in a rapidly changing environment. To effectively change course when required, CFOs should consider establishing dedicated scenario analysis teams focusing on the following risks:

- Financial: As the primary overseer of the company’s capital structure, moving beyond single scenario analysis towards multi-scenario analysis to assess the collective impact of risks on the investment portfolio and overall returns becomes essential for CFOs. Survey results show that only 17% of CFOs at the regional level actively engage in stress-testing business models. To diversify financial risks, the establishment of separate capital pools in different global regions also becomes a necessity.

- Strategic: Conducting periodic stress tests on the business portfolio and the necessity to scrutinise intermediaries and subcontractors are becoming increasingly important. Both actions bear implications for the likelihood of achieving strategic objectives and business sustainability. Survey results show that a mere 9% of CFOs in the region engage high-quality intermediaries and subcontractors. Adopting a mindset of organisational strategic agility that stress tests possible headwinds and strengthening the due diligence processes could well be the preparation needed to deliver stronger results during moments of disruption and challenge.

- Climate: As the CFO role expands to encompass ESG and climate change priorities, enhancing climate risk modelling becomes imperative for CFOs in the future. The skills required for climate risk assessment may differ slightly from traditional CFO roles, necessitating the attraction of suitable talent or the reskilling of existing talent in climate risk assessment.

- Governance: Survey results indicate that only 9% of CFOs in Asia-Pacific consider governance risk a top business priority, with Japan leading in the region at 24%. As CFOs harness technology’s potential, especially generative AI, elevating trust and governance in technology across all markets and industries becomes essential.

CFOs should acknowledge their integral role within a broader ecosystem and proactively engage with legal counsel, risk management teams, and business unit leaders to simultaneously manage critical risks and balance them with harnessing opportunities.

2. Play a larger role in strengthening sustainability initiatives

Today, climate and sustainability imperatives are taking centre stage and becoming a critical part of organisational agendas. As companies across the region allocate more funds to expand their sustainability initiatives, CFOs will find themselves in a unique position—strategically balancing profitability and climate impact. CFOs’ responsibilities in terms of sustainable development mainly involve disclosing information related to climate risks, conducting environmental impact assessment, and accounting for corporate carbon emissions. For example, the expansion of China’s green finance market and increasing demand for corporate carbon emissions audit are expected to broaden the CFO’s role in the field of sustainable development.

The broadening of the CFO role could translate into two things: One, it highlights the need for CFOs to upskill or add new skills that can help them contribute to the climate imperative, especially from the data governance and data collation capacity. And two, it could lead to the impending rise of the chief finance and sustainability officer (CFSO), an emerging career pathway for the CFO.9 The CFSO is a relatively uncommon yet increasingly important position, typically seen in companies with well-developed sustainability initiatives and commitments. The CFSO, positioned above CFO and CSO functions, is responsible for overseeing the integration of finance and sustainability into the organisation’s business strategy. Individuals in this role would typically have a background in accountancy, as integrating sustainability into business operations requires intimate and in-depth knowledge of finance. This puts accountancy and finance professionals in an advantageous position to lead their organisation’s sustainability agenda and take on the role of CFSO. This presents a potential career option for today’s accountancy and finance professionals to consider for the future.

3. Invest in the finance team and align incentives beyond remuneration

As organisations grow in size and complexity, traditional roles within the C-suite are metamorphosing to become broader, with boundaries between functions becoming more fluid. To navigate the complexities of an evolving economic and business environment while optimally harnessing the power of technology, CFOs must surround themselves with top-tier talent. This means that attracting and retaining talent is no longer the bastion of the human resource function.

CFOs must continue to invest in understanding their teams and align incentives that go beyond remuneration. They must prioritise coaching, mentoring, and leadership development and help team members define clear pathways that align professional goals with the organisation’s strategic goals. In addition to spending time on individual succession planning, CFOs must also plan for key roles in the organisation, ensuring an optimal balance of technical, analytical, and leadership skills within their teams.

4. Become champions and stewards of digital technology

For organisations that are looking to thrive and lead in the next few decades, access to timely and accurate data and the ability to leverage generative AI to augment finance productivity and decision-making have become crucial. According to our survey, only a small fraction of CFOs is actually leveraging big data and analytics or actively seeking AI and machine learning solutions to enhance their function. However, even as technology is set to play an increasingly important role for the CFO, it must be underscored that success will hinge upon two factors:

- The accuracy, availability, and consistency of data

- The presence of a robust, agile, and integrated technology infrastructure

Companies that can put these foundations in place will find themselves better positioned to navigate the uncertainties of the business and economic landscape and strengthen their competitive advantage. This is where the CFO of today will come to play an integral role. Investment in digital technology, especially generative AI, will be a key orchestrator of transformation and vital to both managing complexity and driving productivity. To accomplish the many things expected of CFOs today, CFOs must learn the digital language and raise their game to make the right investments in technology at the right time, and holistically leverage technology in a way that yields optimal value for the organisation.

Appendix

Voluntary to mandatory: The following are some of the recent developments and initiatives that are being implemented across the APAC region as countries transition from voluntary to mandatory climate and ESG reporting:

- Australia: Mandatory reporting under the ISSB Climate reporting standards will be phased in progressively over three years in Australia commencing in FY25. The extent of disclosure required, and hence, the extent of preparatory work on underlying systems and processes, is extensive.

- Singapore: The Singapore Exchange has introduced a phased approach to mandatory climate reporting based on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).10 The trend of ratcheting up of the level of obligation and the scope of disclosures is likely to continue. Unfortunately, in markets where disclosures are voluntary, the progress has been slow, as the decision to disclose remains largely at the discretion of the issuer.

- China: The country has moved from a voluntary disclosure regime to a mandatory one, pushing for increased regulation on listed companies, financial institutions, state-owned enterprises, and enterprises operating in highly polluting industries. For example, in April 2022, the China Securities Regulatory Commission published new rules on Investor Relations Management Guide for listed companies, which emphasised information disclosure of ESG issues. The rules took effect from May 2022. Additionally, the Hong Kong Stock Exchange announced that it will prioritise aligning its climate disclosures standards with the recommendations of the TCFD and ISSB standards.

- India: The Business Responsibility and Sustainability Reporting (BRSR) framework is aimed at helping entities integrate sustainable and responsible practices into their business operations. Introduced in 2012 as Business Responsibility Report (BRR), the Securities and Exchange Board of India (SEBI) mandated that the top 100 listed companies in India by market capitalisation needed to file a BRR. By 2021, BRR evolved into BRSR, making it a comprehensive ESG-reporting framework mandated for India’s top 1000 listed companies (by market capitalisation). Further, select key performance indicators under the BRSR, referred to as the BRSR Core, will be subject to mandatory reasonable assurance in a glided path starting from FY23–24 until FY26–27. The BRSR shall provide disclosures about the sustainability parameters for the companies and will enhance comparability of this information.

- Japan: The Sustainability Standards Board of Japan (SSBJ) has developed a Japan-based standard equivalent to the IFRS standard (announced by the ISSB) and aims to deploy it within a few years. In addition, with the range of mandatory sustainability disclosures gradually expanding (for example, a new requirement set up in the Annual Securities Report to address the company’s perspectives and initiatives on this matter), it is expected that the finance function would need to prepare for broader-than-ever disclosures.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities, each of which is a separate and independent legal entity, provide services from more than 100 cities across the region, including Auckland, Bangkok, Beijing, Bengaluru, Hanoi, Hong Kong, Jakarta, Kuala Lumpur, Manila, Melbourne, Mumbai, New Delhi, Osaka, Seoul, Shanghai, Singapore, Sydney, Taipei and Tokyo.

None of DTTL, its member firms, related entities, employees or agents shall be responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication.

© 2023 Deloitte Asia Pacific Services Limited