Article

Quality Cost Reduction

Impact of quality-related costs and how to reduce them sustainably

Although cost of quality typically account for up to 20% of total company sales – and thus provide a huge potential for cost savings - they are often not taken seriously enough when optimizing business or looking on cost reduction projects. Especially small and medium sized organizations struggle to realize these cost savings due to lack of transparency and sense of urgency regarding quality costs.

Inhaltsübersicht

- Quality trends & challenges

- Cost transparency as key for success

- Our approach to quality cost reduction

1 | Quality trends & challenges - Impact of quality costs

In today’s globalized and strongly competitive markets, quality is a major differentiating factor – especially small and medium sized organizations struggle to reduce costs while at the same time increase efficiency within quality. There is a need of urgency as quality costs are increasing dramatically over the past years due to poor product quality, customer complaints and product recalls.

For many small and medium sized companies seeking the right actions to steer quality and increase transparency in their quality cost structure have become a big challenge. The lack of transparency, which often is based on e.g. fragmented regional structures from different mergers, is very difficult to handle.

Today’s companies are paying high amounts – up to 68% of their total quality costs – for quality correction costs. Those costs occur internally through rework and scrap as well as externally through warranty claims and recalls. Only 32% are related to quality prevention costs. The key challenge is to reduce quality correction costs on the one hand and to shift costs from quality correction costs to quality prevention costs on the other. In order to tackle these high cost saving potentials and to focus more on defect prevention, transparency has to be created and improvement levers need to be identified. Whereas in other functional departments it is „daily-business“ to implement cost driven approaches, in quality management, companies are still facing uncertainties and challenges which often hinder them to look at Costs of Quality:

- How and where to start?

- How to slice and dice Costs of Quality and what costs are to include?

- How to prioritize the right levers to decrease Costs of Quality?

- How to prevent Costs of Quality?

2 | Cost transparency as key for success

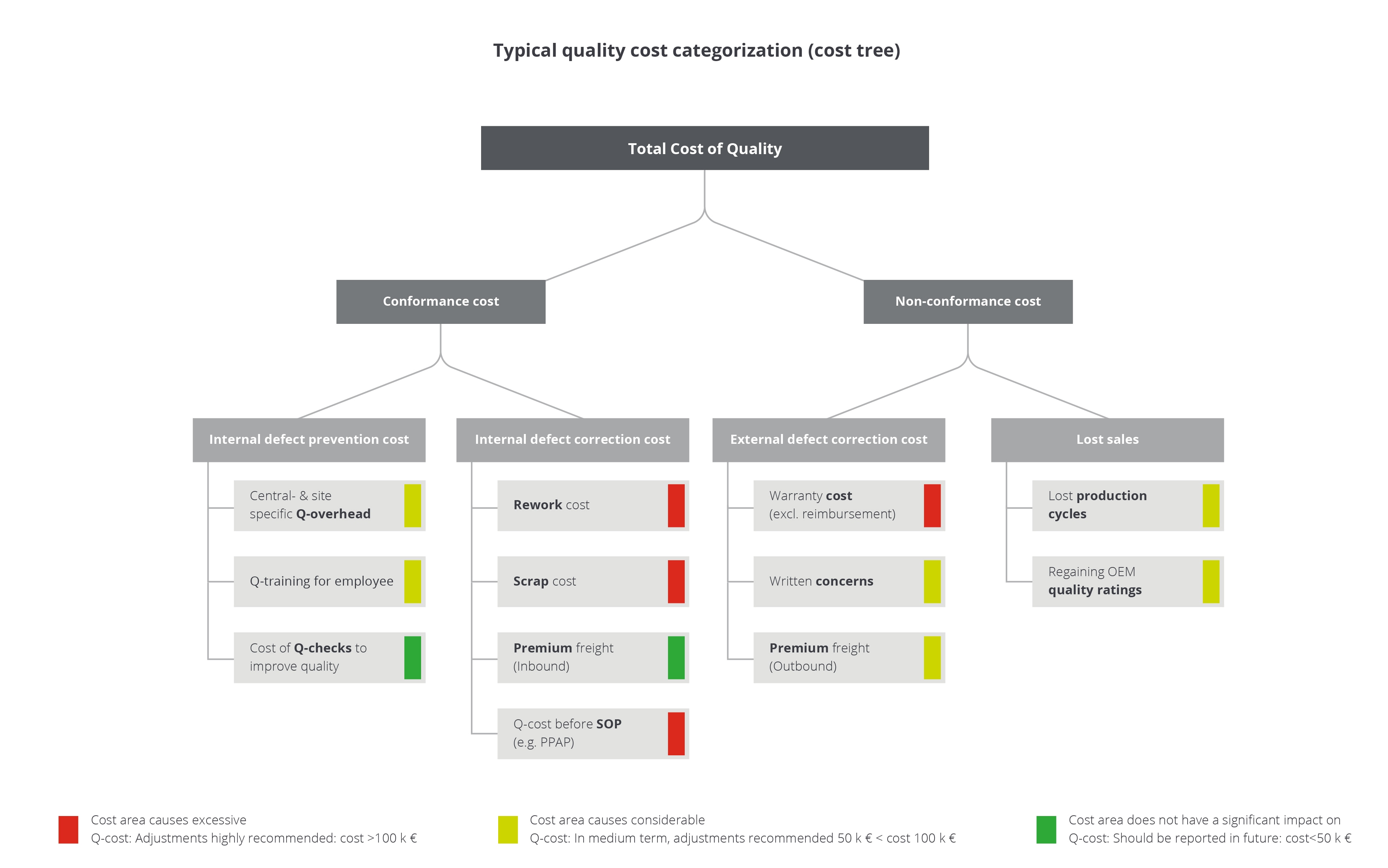

In order to increase cost transparency and identify, evaluate and implement the right measures to realize quality cost reductions, it is essential to clearly separate quality costs.

In general, we can differentiate between conformance and non-conformance costs. Conformance costs - such as quality assurance, rework or scrap - ensure that product features meet customer requirements and that failures are corrected before a product is handed over to the client. Non-conformance costs on the contrary – such as warranty, recalls and loss of sales – define the deviation of product features from customer requirements and expectation.

To achieve a clear separation of quality costs, organizations need a systematic record of all relevant quality costs and a clear quality cost overview. A holistic and similar calculation of quality related performance indicators across the entire company enables comparability. Detailed data analysis, comprehensive interviews, and shop-floor visits allow identifying critical cost areas and detect unknown quality cost drivers.

The main reasons for non-transparent quality costs based on our project experience are mainly driven through the following points:

- No holistic and similar calculation of quality-related KPIs within a company

- Non-transparent structures caused by problems in Post Merger Integrations (PMI)

- Diversity in sites due to different countries, inhomogeneous product portfolios, and quality mindset

3 | Identify the right measures for you to reduce quality cost

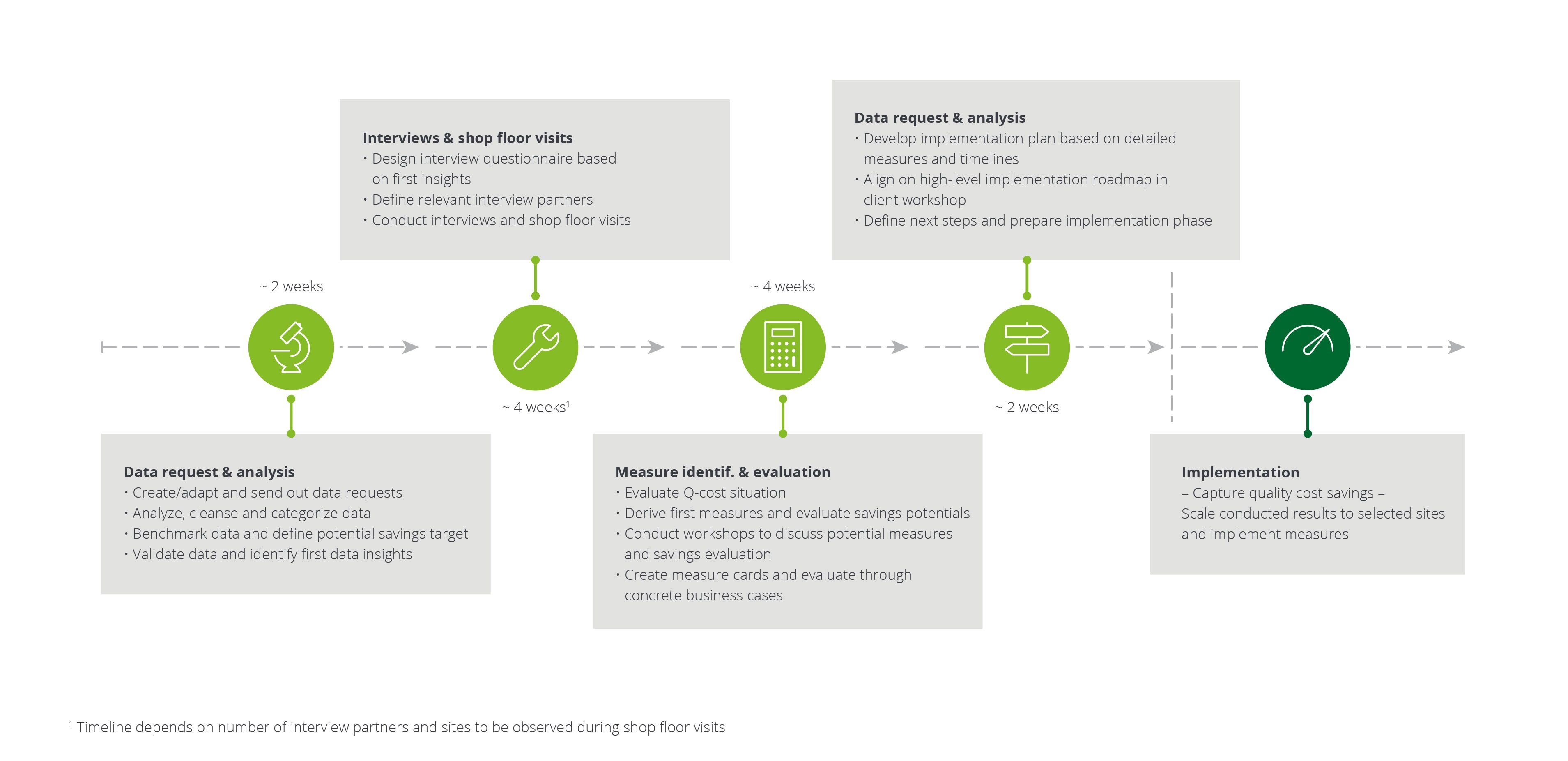

Based on our project experience, we developed our four-step approach, which will support to generate transparency, identify the right levers and savings potentials to reduce quality costs. Within 12 weeks, we are able to analyze quality related data, identify the right levers and provide potential measures.

The first step is to increase transparency regarding which types of quality costs are occurring.

Second, validate first hypotheses through focused interviews and shop floor visits.

Third, based on a comprehensive analysis (data & interviews) the right levers and measures in order to reduce quality costs should be identified.

Fourth, a comprehensive implementation roadmap is to be developed in order to tackle the identified measures and achieve cost savings potentials.

Figure 2: Deloitte Approach to quality cost reduction:

Der Autor

Clemens Ulrich

Manager Consulting

clulrich@deloitte.de

Ansprechpartner