Applying for digital transformation and carbon neutrality tax incentives Bookmark has been added

Article

Applying for digital transformation and carbon neutrality tax incentives

Japan Tax & Legal Inbound Newsletter November 2021, No. 72

As part of its 2021 tax reform package, the Japanese government has introduced new tax incentives related to investments in digital transformation (DX) and carbon neutrality (CN) to help further two of its long term goals of promoting digitalization and environmental sustainability. The new incentives went into effect on 2 August 2021, which is the date the Industrial Competitiveness Enhancement Act (ICE Act) was revised. The revised ICE Act provides details on the application process for the DX and CN incentives, and companies may begin the process to claim the incentives (e.g., pre-consultation, submission of a business plan for approval, etc.).

This newsletter discusses the application procedures and timelines for implementation for the DX and CN incentives under the revised ICE Act, so that companies may plan accordingly.

Explore Content

Overview of the DX and CN tax incentives

DX incentive

Companies that qualify for the DX incentive and purchase specified assets based on a business plan certified under the ICE Act may choose to take either special depreciation of 30% or a tax credit of 3% (5% for companies that integrate internal data with that of an external third party) of the cost of such assets – up to JPY 30 billion for either option. The assets must be purchased between 2 August 2021 and 31 March 2023. Eligible assets include certain new software, machinery, and equipment, or deferred assets for investments in cloud-based systems used for business purposes in Japan. Used assets and items related to research and development are specifically excluded and not eligible for DX incentives. Similarly, DX incentives are not available for companies in the software, information technology, or internet-related services industries.

As mentioned above, purchases of eligible assets must be in accordance with a certified business plan, and the Ministry of Economy, Trade, and Industry (METI) has provided details on its website highlighting the digital and transformative requirements to be included in the plan. Under the digital requirement, companies must show how they intend to use cloud technology to efficiently and effectively integrate data. For the transformative aspect, companies must show how the investments will lead to the production of new goods or services, introduce new production methods, or introduce new methods for sales or services. Furthermore, board resolution minutes approving the business plan are required to indicate that the transformation will be a company-wide transformation. The business plan then must be approved by the relevant minister; however, in order for the plan to be approved by such minister, the taxpayer first must receive certification as “DX ready” from the Information-Technology Promotion Agency.

(428KB, PDF)

CN incentive

Companies that qualify for the CN incentive and purchase assets that make production processes more carbon efficient or that are used in production facilities for the manufacture of certain carbon-efficient products may choose to take either special depreciation of 50% or a tax credit of 5% (10% for certain assets that significantly contribute to the reduction of greenhouse gases) of the cost of such assets – up to JPY 50 billion for either option. Similar to the DX incentive described above, assets acquired for the CN incentive must be acquired based on a business plan certified under the ICE Act, which has passed a board resolution and received approval from the relevant minister. For the CN incentive, the assets must be purchased between 2 August 2021 and 31 March 2024.

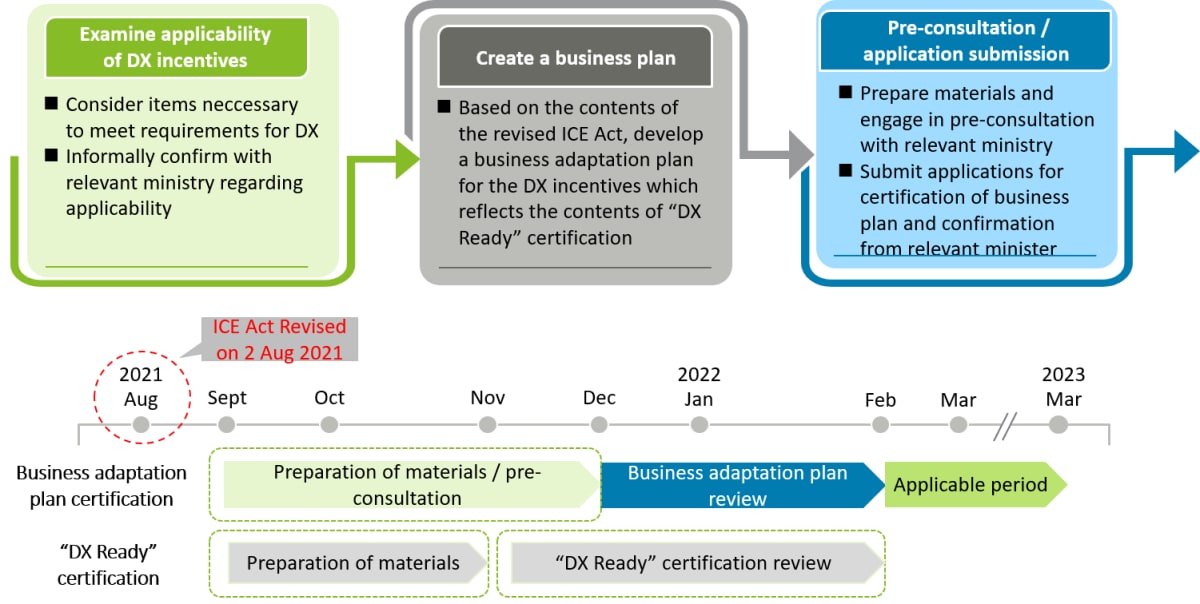

Application procedures and timelines for implementation

As noted above, the application process for the DX and CN incentives is now open, and companies looking to claim the incentives may begin pre-consultations with the relevant authorities and submit applications for approval. To apply, companies must create a business plan based on the specific requirements for either the DX or CN incentive (examples of business plans are available on the METI website (in Japanese only), and, once the business plan is developed, companies may submit an application for certification. In principle, applications should be submitted online to the local minister having jurisdiction over the company’s relevant industry for examination and approval. The example timelines below show the various steps involved in the application process for both the DX and CN incentives, as well as the general timing that companies should expect for each step.

Deloitte’s View

For many businesses, the COVID-19 pandemic has highlighted the importance of DX and having the infrastructure in place to allow remote working and the ability to communicate with colleagues, clients, and customers online. Many companies in Japan have temporary or patchwork solutions in place, such as some employees being able to telework while others cannot, or only being able to access some, but not all, applications remotely.

Companies looking to invest in a more comprehensive DX or, alternatively, invest in certain efforts to promote environmental sustainability, should consider whether taking advantage of the DX and CN incentives may be beneficial for them. Companies interested in pursuing the incentives should consult with their tax advisors to ensure that investments are made in eligible assets and begin developing a business plan that will meet the requirements for certification under the ICE Act.

As noted above, eligible assets must be purchased by 31 March 2023 and 31 March 2024 to qualify for the DX and CN incentives, respectively. While there is still time before the deadline passes, business plans must be approved before eligible assets should be purchased. Furthermore, interested companies should be aware of the overall timeline to ensure they do not miss out on this opportunity.

1 For additional detail on the DX and CN incentives, as well as the various other measures introduced in the 2021 tax reform proposal, please refer to our Tax & Legal Inbound newsletter.

* This Article is based on the relevant Japanese or specific country’s tax law and other authorities in effect on the date of this Article. This Article would not be guaranteed updating if there are any changes in Japanese tax law, any other law, or interpretations by the courts or tax authorities thereof after the date of this Article.

Professionals

Sunie Oue

Deloitte Tohmatsu Tax Co. Managing Director