Alternative data at investment management firms: From discovery to integration

The use of data from alternative sources can give investors an edge. Here’s a comprehensive road map for integrating alternative data effectively in the investment decision-making process.

Karl Ehrsam

Dimitri Tsopanakos

Jib Wilkinson

Manish Motiani

Doug Dannemiller

Mohak Bhuta

The rise of alternative data

Imagine that the volume of all data generated globally in the year 2000 was equivalent to the height and width of an apple tree. Data volume growth is so explosive that the amount of data generated in the year 2022 reaches to the height and width of Mount Everest. Due to enhancements in technologies to capture and store data, much of the new data comes from unconventional sources for investment managers such as credit card transactions, satellite images, geolocation and climate data, social media, shipping trackers, mobile app usage data, and product review data. Investment management firms will likely need to take additional measures to harness the full potential of this newly generated data since, unlike traditional data, alternative data consists of new attributes and forms of data.

According to Deloitte FSI predictions 2023, the global market for alternative data providers will likely reach US$137 billion, growing at a compound annual growth rate of 53% over the next seven years.1 Moreover, the market size of alternative data providers is expected to surpass that of traditional financial services data providers by 2029.2 Firms that do not plan to incorporate this vast repository of alternative data into their investment decision process will likely not only miss out on opportunities to generate alpha but also may attract higher risks due to suboptimal investment decision processes.

Alternative data adoption by the investment management industry

- One of Japan’s largest investment managers utilizes information posted on job review portals and recruitment websites, an alternative data source, to make a more accurate assessment of the strength of organizational culture and identify new investment picks.3

- Another large investment manager acquired an investment boutique to enhance its capability of using natural language processing (NLP) and artificial intelligence on alternative data sources to uncover thematic investment opportunities.4 In the same time frame, the firm also used natural language processing to scrape data from synthetic biology research papers available on a research paper aggregator’s website.5 This approach intended to identify leading products and brands that researchers were using, to help the company identify leading companies in the synthetic biology sector, and to predict trends.6

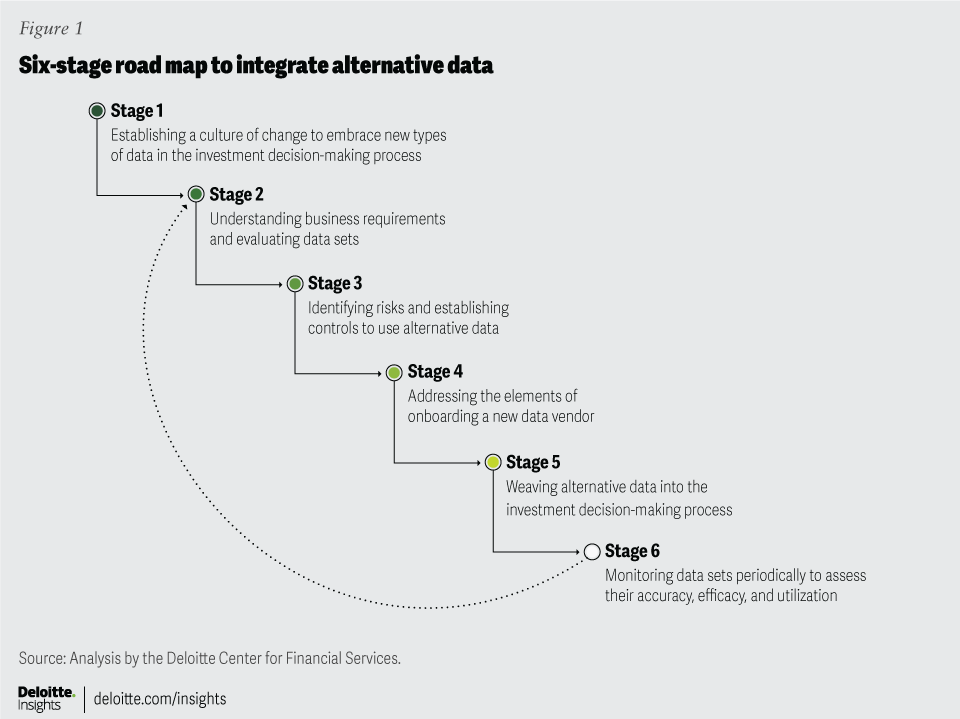

Incorporating alternative data generally involves a long-term commitment of resources as the journey from data discovery to full integration is typically spread across multiple years. A recent survey suggests that many firms are struggling to process raw alternative data into a usable format and make the best investment ideas repeatable.7 To help make this multiyear journey successful, firms should consider a structured road map to institutionalize alternative data into the investment decision process. In this paper, we provide a structured, six-stage process designed to help incorporate alternative data into investment decisions. Figure 1 highlights these six stages of the incorporation process.

Six stages of integrating alternative data in the investment process

Let’s take a deeper look into each stage to understand its purpose and learn ways to implement each.

{kind=link}

Stage 1: Establishing a culture of change to embrace new types of data in the investment decision-making process

On the surface, it may look like alternative data utilization is a technology issue, but the reality is that this process also involves strong cultural issues.8 Cultural change is one of the biggest challenges to data and analytics transformation.9 Often siloed stakeholders lack the perspective, skills, and the comprehensive understanding of other key cross-functional stakeholders needed to build effective solutions.10 Over time some of these stakeholders may lose interest in their firm's alternative data initiatives, while some may even develop passive resistance due to insufficient results.11 Furthermore, the process of fully incorporating alternative data into the investment decision process may span from two to three years.12 Such long-term projects may fail without the attention and strong backing of leadership.13 Firms may not be able to successfully drive adoption forward without establishing collective beliefs and behaviors that encourage the use of new data sources to help improve decision-making. On the other hand, according to Deloitte research, surveyed companies with strong data-driven cultures were twice as likely to exceed business goals compared to companies without that type of culture.14

In order to develop a strong culture of data, firms should have a high level of data literacy, which is the ability to read, analyze, communicate, and work with data. According to a 2019 Deloitte survey, only 37% of respondents across industries indicate that their organization scores highly on data literacy on the insights-driven organization (IDO) maturity scale, with only 10% reaching the top category.15 This higher proportion of companies with lower scores on the IDO maturity scale indicates firms are likely facing challenges with respect to data literacy. Firms also should be careful about the gap between expectations and realities across the organizational hierarchy. Another survey showed that top executives across industries expected their employees to be confident in their data literacy skills, while the reality may be far different.16 To develop a strong data-driven culture, it is important for firms to take actions aimed at improving data literacy. Data literacy can drive competitive advantage in investment management firms as the world transitions from traditional data to alternative data in the investment decision process.

To create an environment that encourages a culture of data-driven decisions, we have identified five areas where firms can take action.

Leading the way

According to the Deloitte 2023 investment management outlook report, progress in any large cross-department initiative is generally driven by leadership, which provides continued support and guidance to help achieve the firm’s vision.17 In fact, the survey findings consistently show year-over-year connections between leadership, culture, and operating results.18 Leading practices at firms with data-driven cultures include top managers setting the expectation that decisions supported with data are the norm and not the exception.19

Board members also play a role in gaining a competitive advantage in a strategic digital transformation initiative such as data and analytics.20 Board members in leading firms possess enough technology fluency to not only be able to understand technical factors but also challenge management on these matters.21 In addition to setting expectations for firm employees, firms also may need to increase the data and technology fluency of their board members through training, engagement, collaboration, and recruitment actions.22

Aligning priorities across business functions and all lines of defense

Successful implementation of alternative data is not a single-department affair. Alternative data strategy generally requires alignment of priorities and buy-in from stakeholders across functions and departments.23 Balancing the priorities of several different teams involved at different stages of the data integration process is a key ingredient for success. The requirement for new data, for example, comes from the investment team with collaboration from the data science or data operations team (to make the data operational). Following the decision to use a data set, teams such as finance, procurement, operations, legal and compliance, and risk should get involved at various stages to fully and safely onboard the data set. A lack of attention by even one of these departments can slow down the data integration efforts, or worse, fail to address potential data remediation efforts needed prior to publishing the data set(s).24 Actions aimed at improving firmwide communication, education, and coordination often help improve the cross-department alignment of priorities pertaining to alternative data and analytics.

Assigning accountability

Increasing accountability will likely lead to better cultural outcomes.25 Along with strong leadership backing, the success of alternative data strategy at investment management firms largely hinges on the presence of a passionate internal data champion, backed by a team having a deep understanding of alternative data, that helps drive the agenda and provide stewardship. Furthermore, it is important to develop a robust execution plan and assign specific responsibility for data utilization, analysis, and management to all stakeholders, helping ensure accountability extends beyond siloed functions.26 Increased accountability can also ease the pressure on the chief data officer, a role with high turnover due to poorly defined roles and complicated cross-departmental coordination.27 Turnover in this role can lead to delays in progress on the journey of implementing alternative data. Increased accountability can help drive the alternative data strategy agenda forward and improve communication and collaboration across teams.

Boosting data science capabilities

To build a data-driven culture, firms should build strong data science capacity by either partnering with or building a team that specializes in discovering, processing, analyzing, and visualizing data. In addition to investing in talent, firms should also improve the associated technology infrastructure and processes around the use of data science. Firms with limited AI resources or budgets may want to onboard third-party no-code platforms to supplement their data science capabilities. Larger firms with a highly complex organizational structure may look at a more federated model, where some of their data capability is brought together in a shared service center or outsourced to data specialist third parties.

Encouraging training

Understanding the depth of data and analytical processes is important for utilization in investment decisions. According to a Deloitte survey, 88% of companies across industries where representatives reported that all stakeholders have been trained on analytics exceeded business goals, compared to just 61% for companies where only select stakeholders were trained.28 Industry and educational institutions for the investment management industry are stepping in to support the upskilling effort. Groups such as the CFA Institute, Chartered Alternative Investment Analyst (CAIA) Association, and FISD recently launched programs around alternative data.29 These programs can help operations teams with onboarding alternative data vendors and introduce the use of alternative data for investment management professionals. Armed with knowledge of both alternative data and investment management, investment professionals with strong data experience can form robust, data-literate teams, wherein they act as a conduit to bridge the communication gap between the technology and investment teams.30

Stage 2: Understanding the business requirements and evaluating data sets

Establishing a data-driven culture should be a prerequisite to moving ahead with an alternative data-driven strategy. Firms that have made progress on the cultural aspect can continue their data adoption journey with requirement-gathering, identification, validation, and evaluation of data sets.

Understanding the business requirements and constraints

Portfolio managers and analysts should closely collaborate with the data science team to understand the firm’s requirements and constraints around alternative data sets. The requirement can broadly be broken down into five categories:

Required data attribute set: Data requirements vary based on the type of fund, the kind of analysis, the sector or company being analyzed, and the internal talent and technology infrastructure required to make the data usable. Alternative data attribute sets can include credit card data, geolocation or climate data, shipping data, satellite images, and product quality reviews. The data attribute set should be designed to model a key performance indicator in the firm’s intrinsic valuation model. Using alternative data should involve strong collaboration between the data science team, that understands the data, and the investment team, that understands the intrinsic valuation model and investment concepts. Neither party can independently initiate the process.

Required state of data: A firm’s technology and talent infrastructure helps determine whether it will be able to handle unstructured, structured, processed, or semi-processed data. Leading approaches to processing unstructured data include natural language processing, or in some cases, machine learning, a methodology that enables the processing of unstructured data in a more linear and process-friendly form. Another way of looking at the state of data may include if the firm needs point-in-time data or not. Point-in-time data (which are different than real-time data) help firms perform more accurate analysis based on the data that were available at the period being tested, either back- or forward-tested (if simulation-based).

Functional requirements: Clear and succinct data attribute sets and state may help, for example, in determining the required data format, delivery channel, frequency, timeliness, length of history, and requirement for data-ticker mapping.

Support requirements: Depending on the infrastructure and the data set, firms may need support in processing and understanding the data being funneled to the investment decision process. The support variations may include the channels of support, the hours of support required, specific time zone requirements, and the threshold for outages. Some investment managers prefer sourcing from data vendors or brokers that offer a vast variety of data sets along with the necessary support services.

Cost-versus-investment balance: Firms should find a balance between cost of data and the expected return. Typically, investment management firms spend single-digit basis points as a percent of their AUM on alternative data sets.31

Furthermore, business requirements are also influenced by regulatory requirements and constraints which are discussed in detail in Stage 3.

Identifying a data set

Once a firm understands its business requirements, the next step is typically to identify data sets that meet those requirements. Understanding the large and growing data universe can sometimes feel overwhelming, so to help make the process manageable, the research can be broken down into a few stages.

1. Learning about data sets: An efficient method to gather the necessary insights about data sets can be to leverage data brokers that provide tear sheets―which contain high-level descriptions of data sets―to reduce the number of introductory calls.32 A combination of “speed-dating” alternative data conferences, data brokers, and standardized due diligence questionnaires can also provide one of the most comprehensive views of the data universe.

2. Choosing a data set: Once firms have identified their business requirements and learned about the universe of available alternative data, they should choose a few data sets that have the potential to be most beneficial. Narrowing down to a few data sets is one of the challenges faced by investment management firms, as there are currently more than 7,000 available, and many data sets offer similar data.33 To further narrow down their search, firms can ask the following four questions:

- Does the new alternative data set answer questions that remain unanswered by the traditional data sets?

- Does the new alternative data set provide a signal earlier than the traditional data sets?

- Does the new alternative data set help verify unreliable information obtained through traditional data sets?

- If the alternative data set does not add significant value on its own, does it provide value in combination with other existing or other alternative data sets?

Once identified, the chosen data sets should then be tested, as the decision to onboard a data set may depend on positive back-testing results and successfully fulfilling compliance criteria.

3. Initial due diligence and trial: Due diligence helps investment managers to know more about the company, the product, and other regulatory information before beginning the data set trials. Firms should check the vendor’s code of ethics (including their approach to Trustworthy Artificial Intelligence, in case AI-driven algorithms and models are used), subcontractor relationships, and information-gathering process to assess how it addresses material non-public information (MNPI) and personally identifiable information (PII) risks. Firms can start their due diligence by using standardized due diligence questionnaires (DDQ), and tailor them for the data attribute sets and the terms of use they plan to pursue.34 Some firms go a step further to examine the vendor leadership’s track record. Vendors whose leadership has a background in financial services are more likely to be aware of the regulations that are applicable to the investment management industry.

Checking the quality and level of bias of data

Data science teams can assess the quality and level of bias of data (data bias is something fairly new in the world of data, which we will aim to explain in more detail in future publications), based on its accuracy, longevity, representativeness, backward compatibility, and uniqueness and breadth of adoption.

- Accuracy: To assess the accuracy of data, firms need to understand the procedures of data collection and its lineage. Understanding the lineage would require knowing how and when the data was transformed at each step and by whom.35

- Longevity: Checking for the contract duration and renewal terms between the vendor and its data sources can help understand the longevity and associated risks.

- Representativeness: The data science team should review whether the data set is a good predictor of one of the key performance indicators in the firm’s intrinsic value model. Firms can initially gauge the representativeness of a data set from the backtesting results provided by data vendors and later confirm these results when performing their own backtesting analysis.

- Backward compatibility: The data science team also should review if the new data set is compatible with the existing infrastructure and if the cost to interpret the data is within reasonable limits. Potential compatibility points may be frequency, labeling structure, language, and file format.

- Uniqueness and breadth of adoption: The uniqueness of a data set can increase its quality as it may offer insights that are not provided by any other data set. The breadth of adoption is a signal that cuts two ways: Firms may need it to understand the potential for value in the data set, but the potential for alpha may be diminished as the breadth of adoption reaches critical mass.36

Checking for the potential for return generation

If the quality of a data set is reasonable, the data science team can proceed with examining the return-generation potential through backtesting. Firms that tend to have limited data science resources, such as hedge funds or private equity firms, can leverage third-party no-code or low-code platforms to gauge the signal generation capacity of a data set.

Backtesting is not easy though, as many alternative data sets are relatively new and therefore offer a very limited historical view of data. This limited history can make it challenging to detect patterns and capture signals. Furthermore, even when historical data is available, it may not be point-in-time data, which can lead to look-ahead bias, wherein information that was not available at the time of making investment decisions gets used in the investment model.37

A lack of comprehensive data can also lead to survivorship bias, wherein only data for elements that survived an event or process are considered for making investment decisions.38 Data science teams should adjust for these biases while backtesting data sets to train models accurately and avoid overstating alpha-generating potential.

Even with positive backtest results, some data sets may be rejected. The data science team should be able to justify the estimated benefits to portfolios compared to the all-in cost of acquiring, processing, and storing an alternative data set.39

Stage 3: Identifying risks and establishing controls to use alternative data

Once investment and data teams have selected a few data sets, they can proceed with integrating them into the investment decision process. However, this can lead to additional risk for investment management firms. Here is an overview of these risks and the suggested controls to help minimize them.

Model risk

Investment and valuation models are the basic building blocks of investment management, and the introduction of any new element can introduce errors if not done cautiously. Model risk is the risk of making inconsistent or irregular investment decisions. These inconsistencies are typically due to complications caused by the introduction of a new alternative data set at any point of the model revision—input, implementation, and output.40 The primary causes for model risk include irregular updates and maintenance of existing models when ingesting new data or modifying existing data.41 Other major causes of model risk may include poor documentation, untested assumptions, faulty inputs, poorly constructed models, and incorrect linkage of output to the trading process.42 Model risk can be mitigated by implementing a comprehensive model risk management (MRM) framework that integrates roles, responsibilities, and control activities.43 Generic MRM frameworks can be used as a guide for firms to draft their own tailored framework.

Vendor risk

Given the entrepreneurial nature of the alternative data industry, vendor risks may be more common in this ecosystem. Alternative data vendor risks include risks arising due to changes in the data collection methodology or changes in the terms of use.44 Changes in the data collection methodology may impact the effectiveness of the data depending on how it is used. For example, if a data vendor for credit card transaction data changes its source after a few years, the new data generated may not be strictly comparable to the previous year’s data. A change in the terms of use of source material may also impact the validity of the initial risk assessment. Established escalation protocols, client notification practices, and processes to monitor adverse events can help curtail the impact of these vendor risks.45 In case of any adverse events, firms should pause the use of the impacted data set and involve their compliance and legal teams to assess the impact, perform further due diligence, and take necessary corrective actions.46 After the initial risk assessments, the vendors should be periodically reassessed to minimize vendor risk. The plan for the reassessing vendor risk should be documented, along with the periodic results.47

Regulatory risk

Regulatory risk largely revolves around the use of alternative data containing MNPI and PII. Because the use of alternative data is a relatively new development for investment management firms, the regulatory environment is less mature. Regulatory compliance requires firms to have written policies and procedures designed reasonably to address the potential risk of receipt and use of MNPI through alternative data.48 For example, regulators may penalize investment managers even when they unintentionally happen to use alternative data that contains PII if the firm is unable to show documented evidence that they did adequate due diligence to assess the presence of PII information before deploying the data set in question. Being selective in choosing vendors can help investment management firms minimize regulatory risks. They should look for vendors whose DDQ responses, representations, and warranties confirm their process alignment with regulatory guidelines. Lack of access to legal counsel or low levels of spending on compliance activities may be an indicator that the vendor is less informed about regulatory requirements. Firms can also train analysts on issues specific to alternative data to help reduce regulatory incidents.

Regulatory interest in alternative data is growing

The US Securities and Exchange Commission (SEC) brought the first alternative data enforcement action in 2021, penalizing an alternative data vendor for material misrepresentations about its business model to its users and providers of data.49

The following year, the SEC issued a risk alert on MNPI-related compliance issues that highlighted observed deficiencies in investment managers’ alternative data policies and procedures. According to the alert, investment managers did not appear to have adopted reasonably designed written policies and procedures to manage the potential risk of accessing and using MNPI from alternative data sources.50

The FCA, the UK-based regulator, in 2022 published a feedback statement after consolidating responses from market participants on a Call for Input. The Call for Input was to understand how data (including alternative data) and advanced analytics were being used and accessed; the value it offered to market participants; pricing and sales dynamics; and its associated risks.51 As a next step, the FCA has commissioned research to get additional information on the use of alternative data and analytics, its competitive environment, and the broader regulatory risks that come with it.52

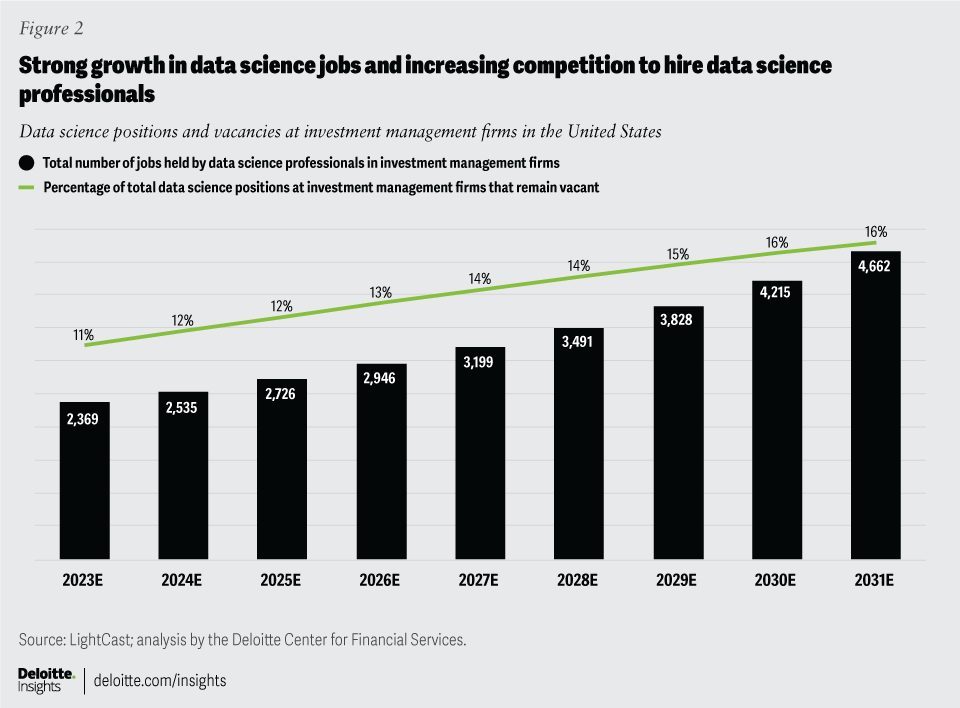

Talent risk

The data science team acts as the interface between alternative data and investment management teams, but high turnover among professionals in this discipline can risk slowing the integration process down.

One of the major factors fueling the high turnover in data science is the shortage of data science professionals. Due to the high demand for data science professionals, about 16% of job positions for data science professionals by investment management firms in the US are expected to remain vacant in 2031.53 The number of job postings by US investment management firms that included a data science or data analytics-related skill doubled over the past decade, from 12% in 2011 to 24% in 2022.54 To add to the already competitive environment, investment management firms are competing for talent not just with industry peers but also with other industries.55 Lower availability of experienced and skilled data science talent may be the primary reason for this talent gap.

{kind=link}

Methodology for calculating the shortage of data science professionals in investment management firms

Extracting historical job posting data and forecasting growth:

A job postings data set was used to extract the historical job postings for data science professionals by investment management firms. We forecasted the job postings to grow at the same CAGR as it has grown over the past five years.

Forecasting demand by estimating the number of job postings targeting new positions:

Based on our analysis of the average tenure of data science professionals, we estimate the average attrition rate of data science professionals to be 20%. Considering data science is an emerging field, we conservatively estimate the requirements of data science professionals will grow by 5% each year since the US GDP grows between 2-3%. This information leads to an estimate of 20% of all job postings for data science professionals by investment management firms being for new positions.

Estimating the shortfall in talent:

Given the demand for data science professionals, we estimate that because a data science professional typically gets multiple job offers, the success rate at hiring is about one-third of the total demand (demand was calculated in the previous step). This leads to about two-thirds of new positions being left vacant, with the unfulfilled demand flowing into the demand funnel for the following year.

To help meet the demand for data science capability in this competitive environment, firms may need to get creative. One creative approach some firms are taking is establishing close ties with universities through guest lectures, internships, and mentoring programs. This method can help create a competitive edge by essentially beginning to recruit students before they even hit the job market.57 Another way firms can deal with the shortage of data science professionals is to consider focusing on skills-first hiring, determining what the specific skills are required for the role, as opposed to focusing on academic pedigree.58

In fact, according to a Deloitte study, 90% of firms across industries are now actively experimenting with skills-based workforce practices, that focus on skills rather than degrees.59 Firms can also recruit internal talent who are ready to upskill themselves and move to a new data science role.60 Firms can also reduce the need for additional data science professionals altogether by using third-party tools that do not require much coding or by buying data sets that come bundled with analysis software.

In addition to hiring new talent, firms may also need to do more to retain existing data science talent. Even amid the competitive market for their skills, many data science professionals spend the majority of their time working on basic tasks, rather than focusing on the more interesting analytical tasks.61 To reduce turnover, investment firms can leverage technology to automate basic and repetitive tasks.62 Firms can further increase productivity and reduce turnover by communicating with the data science professionals how insights generated by them can directly impact company performance. Finally, firms can make themselves more attractive workplaces for data science professionals by hosting innovation events and setting up a robust infrastructure that helps establish a culture of experimentation.63 A robust infrastructure can handle increasingly large volumes of data and facilitate secure storge, easy access, quick retrieval, and complex analysis which are key ingredients to an advanced decision process architecture. A combination of an innovation culture, fair compensation, and meaningful work can help firms retain existing data science professionals amid the war for talent.

Stage 4: Addressing the elements of onboarding a new data vendor

Onboarding any new alternative data set involves thorough due diligence, a robust contract, price negotiations, and data storage setup. Some activities during this stage can be performed in parallel with the activities in stage three.

End-to-end due diligence

End-to-end due diligence to onboard the vendor involves a more in-depth understanding of data characteristics and sourcing details than the due diligence performed for data set trials. The procurement process for alternative data is also slightly different from how companies procure other data and technology. Unlike traditional data, which is gathered or derived from published financial information, sourcing practices can be critically important in this area. If alternative data is not ethically sourced, it can lead to regulatory risks (such as data privacy violations), or to significant reputational and financial damage. Ethically sourced data can be validated by knowing the owners of the data, the conditions of data collection, the terms of use, and by assessing the vendor’s selling rights.

It would also be prudent to assess the risk and controls implemented by the vendor to understand the reliability of their warranties and representations. In the case of web scraped data, there are two paths: freely available government data and private data. Use of government data is generally less cumbersome than privately sourced web-scraped data from a regulatory perspective. Assessing a vendor’s procedures to understand the associated legal obligations can help firms make more informed onboarding decisions. The full due diligence processes should be comprehensively documented. An effective due diligence function should confirm that the process reasonably tried to test for and eliminate vendors with significant regulatory or vendor risks.

Robust contract

An alternative data agreement may include some unique clauses such as indemnity against third-party intellectual property claims and representation and warranties around MNPI, PII, confidentiality, and data provenance.64 Some private equity firms may want to leverage alternative data generated by companies in their portfolio to make investment decisions. However, before using data from portfolio companies, private equity firms should seek legal counsel to mitigate the risk emanating from contractual obligations, corporate law, and other laws around data governance.65 A robust contract can help shield firms from risk arising due to regulatory and compliance violations.

Price negotiations

Since alternative data are not commodity products, a knowledgeable procurement team will likely be able to more thoroughly understand the different parameters of each data set and use them for effective negotiations. Leveraging the tiered pricing structure, which is used for many alternative data products, helps firms get targeted access to only the required content, frequency, or accuracy of data bringing down the cost significantly.66 Other elements of negotiation may include the pricing framework, soft dollar arrangements, and redistribution rights. Given the newness of the industry, the immaturity of some vendors, and the value of the data, price negotiation commands an important place in the onboarding process.

Data storage

Once acquired, data sets should be securely stored with the precise access rights. Locating and understanding data are the two main issues data scientists face when browsing through large repositories of data. Data set definitions and metadata are components of data storage that help firms use data effectively. Often combining the information from different data sets can lead to better insights, so effective data curation is important to deriving value from the alternative data. Furthermore, defining access rights can help organizations strengthen their cybersecurity posture as they transition to cloud data management.67 Effective data storage can help safely extract value from alternative data while mitigating cybersecurity risks.

Stage 5: Weaving alternative data into the investment decision-making process

Alternative data is a valuable resource. Firms should align people, process, and technology to truly integrate the use of alternative data in the investment decision process.

People

When stakeholders across the departments understand the purpose of the endeavor, they may be able to more effectively use alternative data. To help ensure that alternative data incorporation is optimized, the frontline data scientist and investment analyst should be brought on the same page through avenues such as leadership communication, awareness programs for new data sets, and data set tutorials. Leadership communication should include proof of alternative data’s alpha generation potential.

One way of communicating the alpha generation potential to fund managers is by providing them with a comparison of performance of actual investment decisions and hypothetical decisions on the same fund based on an artificial intelligence model that was fed with both traditional and alternative data. To help make the communication clearer, the comparison may include the number of times additional alpha could have been generated when alternative data was incorporated, and what percentage of that additional alpha could be attributed to alternative data. Technology platforms and dashboards that integrate traditional data and alternative data can help perform alpha attribution analysis. Fund managers are more likely to adopt alternative data in their investment decisions when they see its alpha-enhancing potential for their own decisions.

Other elements of integrating alternative data in the investment process include awareness programs, training, and increased opportunity to collaborate. Training programs can help investment professionals to develop skills around using specific alternative data sets. Furthermore, engagement between the data and investment teams through periodic workshops, demo sessions, and regular updates can help increase the utilization of alternative data.

Process

Investment management teams should work with the chief data officer and data science teams to draft a comprehensive process for integrating alternative data. The process should include scenarios for the applicability, the kind of analysis required, and their expected weight in investment decisions. To set reasonable expectations and increase accountability between the investment and the data teams, firms should define standard turnaround times for various types of data requests. Establishing effective communication channels that help the investment team track the progress of their data requests can reduce friction between the data science and investment teams.

To help ensure adequate governance, investment teams also should set access rights to data sets, and establish a process for documenting and storing data used for making investment decisions. A project plan with timelines to transition from the existing process to the planned process can help firms increase the uptake of alternative data. Overall, targeted process changes that helps make data more accessible to the investment team—without any major impact on their existing investment decision-making process—can help improve its adoption.

Technology

Without proper tools and technology infrastructure, it can become difficult to introduce newer elements like alternative data into the investment decision process. One way of easing the friction is to provide investment teams access to new alternative data through the already in-use analysis platforms or dashboards. Due to the unique and esoteric nature of alternative data, combining different data sets from multiple sources is one of the most frustrating challenges for investment managers.68 Data access through an already in-use dashboard may help investment teams make connections between traditional data and alternative data, perform comparisons, and encourage experimentation.

Firms may even use multiple third-party platforms, and to enable smooth switching across these multiple platforms, firms should adopt a scalable and agile data architecture.69 The majority of investment managers surveyed by Exabel, a cloud-based platform for accessing and analyzing alternative data, plan to increase their use of third-party solutions as they believe these systems are more effective for analyzing data than in-house systems.70 These technology updates can work together to increase the adoption and integration.

Stage 6: Monitoring data sets periodically to assess their accuracy, efficacy, and utilization

Once firms have institutionalized the use of alternative data, they should implement a process to periodically monitor the data sets for accuracy, efficacy, and utilization. Its performance may be impacted by changes in data collection methodology, time decay, loss of predictive capability, and other operational reasons. Data sets that do not perform well on one or more of the following parameters should be reviewed for price renegotiation or replacement.

Change in collection methodology: Regulations around alternative data are relatively new and keep changing, which can lead to changes in collection methodologies. Collection methodology may also change due to changes in data sources, changes in data format, and changes in contract terms between the vendor and their sub-contractors and data source. Changes in ways of collecting data can also lead to changes in analysis methods and may even impact the return generation potential.

Alpha decay: When a sizable number of firms get access to a particular alternative data set, it no longer provides insights that are unique enough to generate alpha.71 Over time, the data set’s information ratio falls, and firms may choose to replace the data set. Firms may also decide to continue using the data set to supplement information from other sources but to justify continuing use of the low information ratio data sets, it would be prudent to renegotiate the price.

How to manage the problem of alpha decay and increase the life span of alternative data sets?

One sustainability-focused active investment management firm, starts by sourcing data sets that are very raw with very minimal modifications done by the alternative data vendor.72 This allows the firm to transform the raw data for the specific economic problem they are trying to solve. Furthermore, the firm combines its insights and data assets to the transformed data set creating a new unique data asset.

To increase the life span of alternative data sets, one global quantitative and systematic investment management firm onboards data sets that have the potential to add long-term value.73 They add data sets that they can fully understand and integrate, favoring ones from which complex relationships can be created that support many teams and strategies across geographies.

However tempting it can be to source exclusive data sets that no other investment manager can access as a way to avoid alpha decay, firms should be wary; the data itself may have innate value rather than developing the value based on the skills applied to it. Such data sets may also have the potential for legal and regulatory risks.

Loss of predictive capability: The predictive capability of an alternative data set largely depends on two factors: its ability to model a KPI and the ability of the KPI to predict the stock price. When either of these components of predictive capability drops, reevaluation of the data set is appropriate. Firms also should ensure that most of the alpha is attributed to the alternative data set and the associated KPI.

Operational reasons: Firms may have to stop using alternative data based on vendor behaviors or operational changes. Other reasons for the lower uptake of a data set may include a difficult to use interface, bad support service, and poor data quality.

Overall, periodic monitoring can help firms track the alternative data set’s alpha generation potential, understand bottlenecks in utilization, and stay compliant with regulations.

Looking forward: Avoid being at an information disadvantage

Firms that do not incorporate alternative data will likely miss out on more information than they actually use in their investment decision, which can lead to suboptimal performance. Moreover, firms that plan to use alternative data but fail to adopt a long-term structured approach to institutionalize alternative data, may not be able to harvest the full potential of alternative data.

Using a thoughtful process for evaluating and integrating this data can help firms reduce risks, diminish roadblocks, shrink lead times, identify useful data sets, responsibly onboard vendors, establish governance procedures, and encourage exploration. This positive dynamic together can increase the chances of success for the alternative data initiatives. Firms that prioritize a strong leadership vision, a data-driven culture, cross-departmental collaboration, and a strong sense of stakeholder purpose are more likely to find themselves prepared for the challenges and opportunities ahead.