Using the equity method of accounting has been saved

Perspectives

Using the equity method of accounting

On the Radar: Equity method investments and joint ventures

With equity method investments and joint ventures, investors often have questions as to when they should use the equity method of accounting. There are a number of factors to consider, including whether an investor has significant influence over an investee, as well as basis differences. As such, there are questions an investor should ask to make this determination.

Equity method of accounting: Key questions

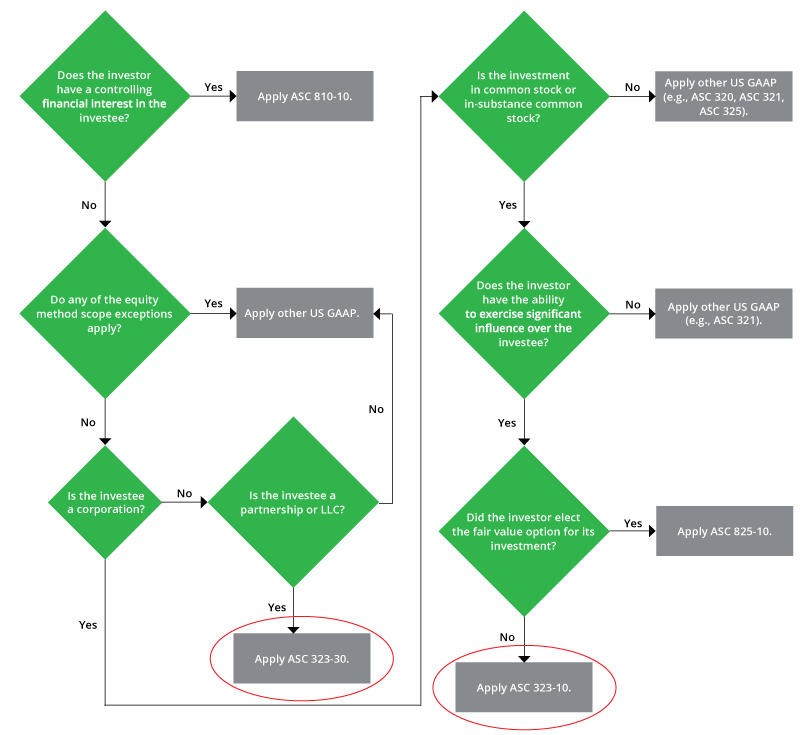

An investor must consider the substance of a transaction as well as the form of an investee when determining the appropriate accounting for its ownership interest in the investee. If the investor does not control the investee and is not required to consolidate it, the investor must evaluate whether to use the equity method to account for its interest. This evaluation frequently requires the use of significant judgment. The flowchart below illustrates the relevant questions to be considered in the determination of whether an investment should be accounted for under the equity method of accounting.

On the Radar: Equity method investments and joint ventures

When considering the questions in the decision tree, an investor must take into account the specific facts and circumstances of its investment in the investee, including its legal form. The two red circles in the decision tree highlight scenarios in which the equity method of accounting would be applied. Some of the more challenging aspects of applying the equity method of accounting and accounting for joint ventures are discussed next.

Evaluating indicators of significant influence

The guidance in ASC 323 on determining whether an investor has significant influence over an investee can be difficult to apply for corporations and limited liability companies that do not have separate capital accounts. For limited partnerships and limited liability companies with separate capital accounts, the equity method of accounting must be used if an investor owns more than 5% of the investee (see ASC 323-30-S99-1) and an evaluation of the indicators of significant influence is not performed. Consequently, there are two models in ASC 323 for applying the equity method (one in ASC 323-10, and one in ASC 323-30), depending on what type of legal entity structure the investee has.

The ability to exercise significant influence is often related to an investor’s ownership interest in the investee on the basis of common stock and in-substance common stock. While there are presumptions in ASC 323 related to whether an investor has the ability to exercise significant influence over an investee, an entity must consider other factors, such as the following, in making this determination.

None of the circumstances listed previously are necessarily determinative with respect to whether the investor is able or unable to exercise significant influence over the investee’s operating and financial policies. Rather, the investor should evaluate all facts and circumstances related to the investment when assessing whether the investor has the ability to exercise significant influence.

Other key indicators

Recent Updates

In March 2023, the FASB issued ASU 2023-02, which expands the use of the proportional amortization method to tax equity investments beyond low-income housing tax credit investments provided that the investments meet certain revised criteria in ASC 323-740-25-1. The ASU is intended to improve the accounting and disclosures for investments in tax credit structures. Although the accounting under the proportional amortization method differs from that for equity method investments, the proportional amortization method serves as an alternative accounting treatment for investments in structures that would otherwise be evaluated for accounting under the equity method.

In August 2023, the FASB issued ASU 2023-05 to address the accounting by a joint venture for the initial contribution of nonmonetary and monetary assets to the venture. Adoption of the ASU will be required for joint ventures with a formation date on or after January 1, 2025, with early adoption permitted. The FASB issued the ASU because of the absence of guidance on the recognition and measurement of the contribution of nonmonetary and monetary assets in a joint venture’s stand-alone financial statements. While the ASU does not change the definition of a joint venture, a new basis of accounting is established upon the venture’s formation. The ASU requires a joint venture, upon formation, to (1) recognize and measure the initial contributions of monetary and nonmonetary assets by the venturers at fair value and (2) measure its net assets (including goodwill) at fair value by using the fair value of the joint venture as a whole. Therefore, upon adoption of ASU 2023-05, a joint venture will measure its total net assets upon formation as the fair value of 100 percent of the joint venture’s equity immediately after formation.

Continue your equity method investments and joint ventures learning

For a comprehensive discussion of considerations related to the application of the equity method of accounting and the accounting for joint ventures, see Deloitte’s Roadmap Equity Method Investments and Joint Ventures.

Let's talk!

Learn more about this topic

|

Andrew Winters |

|

Marla Lewis |

Get in touch for service offerings

|

Jamie Davis |

|

Recommendations

What to consider as an equity method investee

On the Radar: Equity method investments & SEC reporting

Fair value measurements and disclosures

On the Radar: Financial reporting impacts of ASC 820