The emergence and rise of alternative methods of payment and investments such as crypto-assets and e-money has heightened global regulators’ interest. This has prompted the publication of various proposals and frameworks to ensure that the recent gains on tax transparency do not get lost and due taxes are paid.

The Organisation for Economic Co-operation and Development (OECD) published in October 2022 the Crypto-Asset Reporting Framework (CARF) as well as enhancements to the OECD Common Reporting Standard (CRS).

The CARF is a global tax transparency framework that provides for the automatic exchange of tax information on transactions in Crypto-Assets and leverages existing tax and regulatory frameworks, such as the OECD’s Common Reporting Standard (CRS) and the Financial Action Tax Force (FATF). The CARF is a standalone framework and consists of rules and commentary that can be transposed into domestic law. We note however that although the G20 endorsed the CARF and recommended its implementation, no decision has yet been taken on whether it would be considered as a minimum standard or equivalent.

Following into the OECD’s footsteps, on 8 December 2022, the EU Commission issued the 7th amendment to the Directive on Administrative Co-operation (DAC) (i.e., DAC8). DAC8 builds on the Regulation on Markets in Crypto-Assets (MICA) and the Transfer of Funds Regulation (TFR), thereby avoiding imposition of additional administrative burdens for crypto-asset service providers (CASPs) but it also expands its scope allowing for reporting and automatic exchange of information between Member States. DAC8 is largely consistent with CARF and incorporates the amendments to the CRS (NB: but not the commentaries to CARF and the CRS).

However, the proposal differs from CARF in a few areas that we discuss below.

Extraterritorial reach: As it is currently written, the Directive requires all reporting CASPs (RCASPs), irrespective of their size or location, to report transactions of clients residing in the EU. The proposal covers both domestic and cross-border transactions and requires EU and non-EU CASPs with EU clients to register in a Member State to fulfil their reporting obligations. This extra-territorial reach will likely impact Swiss RCASPs serving EU clients. It remains however to be seen if and how the EU will enforce this requirement on non-EU RCASPs. If it makes its way in the final text and is enforced, Swiss RCASPs will likely need to put processes and controls in place to ensure that their EU clientele is reported as required, unless an exception applies.

Block of transactions: If a crypto-asset user does not provide the required information after two reminders following the initial request by the RCASP within 60 days, the RCASP must block the crypto-asset user from performing exchange transactions. Therefore, the RCASP needs to establish a process to ensure that it follows-up on the information request, monitors the timeline and (automatically) blocks the transactions. Additionally, when complying with this requirement, RCASPs will need to assess their legal obligations to ensure they are not in breach of their contract with their client.

GDPR and client notification considerations: RCASPs must inform each concerned customer that information relating to this individual will be collected and reported to the competent authorities at the latest before the information is reported. The RCASPs must also provide all information that data controllers are required to provide under the General Data Protection Regulation (GDPR). This provision is similar to the client CRS notification requirement applied by various jurisdictions.

Penalties: The proposal mandates that minimum penalties, ranging between EUR 20’000 and EUR 500’000, shall apply to RCASPs who have not completed the reporting after two valid administrative reminders, or when more than 25% of the reported information contains incomplete, incorrect or false data. Therefore, the RCASPs must have processes in place to ensure that all relevant information is obtained, accurate and properly recorded. While this will be a tweak in the FIs’ existing FATCA and CRS policies and procedures, it may prove a heavy burden for entities that were not subject to FATCA and CRS but are captured by CARF and DAC8.

Retroactive application: Noteworthy is also the definition of new and preexisting accounts included in the proposed Directive. As written today, DAC8 defines a new account as a Financial Account maintained by a Reporting Financial Institution opened on or after 1 January 2016 or, if the account is treated as a Financial Account solely by virtue of the amendments to the Directive 2011/16/EU, on or after 1 January 2024. This definition seems counterintuitive and in contradiction with the 2025 deadline given to the EU Member States to transpose the Directive into local law.

Notwithstanding, we have information that the draft is currently being reviewed by the EU with the aim to align the wording of the final version with CRS and to eliminate any remaining deviations. If this language is nonetheless confirmed, it will impact RCASPs, which will need to identify and apply due diligence on these accounts as of next year, to comply with the requirements of the Directive.

Deloitte's View

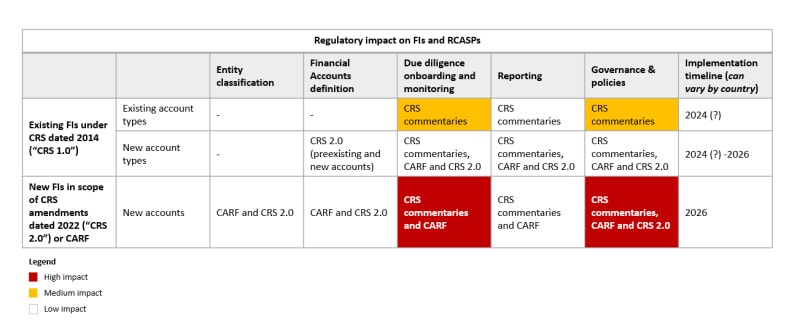

In summary, DAC8 will have an impact on several operational aspects that will affect existing FIs and new FIs/RCASPs in scope of the new regulations. The impact will of course be higher on those RCASPs that will be newly captured by the Directive. As mentioned above, the timeline for FIs/RCASPs will depend on the countries’ implementation timeline. The following table provides an overview of the relevant guidance and the impact for both existing and new FIs grouped by topic.

We note that the DAC8 proposal also includes (i) updates on the exchange of cross-border rulings for high-net-worth individuals, (ii) use of information reported and exchanged under DAC for purposes other than direct taxation, and (iii) reporting of information on tax identification numbers.

DAC8 is expected to apply from 1 January 2026 except for (i) the provisions related to identification services of service providers and taxpayers effective as of January 2025 and (ii) the TIN provisions, which will apply as of January 2027.

Lastly, we would like to reiterate that although the G20 endorsed CARF and recommended its implementation, no decision has yet been taken on whether it would be a minimum global standard or equivalent. Pending this decision, Switzerland is not yet considering the transposition of the CARF into local law. However, the State Secretariat for International Financial Matters (SIF) has established a working group to discuss the integration of the CRS amendments (expected to come into force on 1 January 2026) and their impact for Swiss financial intermediaries.

We encourage interested parties to provide feedback to the European Commission on the proposed text until 30 March 2023 and raise their questions, including requesting clarification on the potential retroactive application of the Directive.

Authors: Atila Demiraj, Olvia Plousiou

If you would like to discuss more on this topic, please do reach out to our key contacts below.

Key contacts

Brandi Caruso

Partner, Financial Services Tax & Legal

Michael Grebe

Director, Financial Services Tax

Olvia Plousiou

Senior Manager, Financial Services Tax

Atila Demiraj

Assistant Manager, Financial Services Tax