Perspectives

Industry 4.0: Why does Tax matter?

Industry 4.0, also referred to as the 4th industrial revolution, has become a buzz word. Once the concept laid out, it is fairly easy to see that industry 4.0 can bring profound transformation to the business of a company. Less obvious is maybe the transformation it could also bring at the same occasion to the company’s tax landscape. This is however an aspect that should not be neglected and would be best considered upfront.

To understand the potential tax implications of Industry 4.0 on any specific business, it is important to start from the business transformation itself. Typically, it does not only include a transformation of the manufacturing process but in many cases also relate to the company’s offering. This article is considering these two major transformation plays.

1. Manufacturing processes transformation

The first level of transformation brought by Industry 4.0 occurs obviously in the factories. Through the creation of a digital link between operations and information technology, information is captured from multiple sources and locations, and then analysed to drive the physical manufacturing and distribution, resulting in improved efficiencies. What does that mean from a tax perspective?

The investment

Such a transformation is not possible without a substantial investment. In a multinational enterprise environment, all aspects of this investment (including amongst others the decision to invest, the strategic developments decisions, the actual development of the new production line, the funding, the management and control of the budget or the assumption of the related risk), will rarely be concentrated at the level of one single legal entity. Determining the role of each group entity will however be key to determine how future profits resulting from that investment should be allocated amongst group entities.

Also, typically, such investment will fall outside the usual procurement pattern of the company. It may therefore have an impact on its VAT position and cash flow: Can the company recover the VAT payable on that investment? And when? Similarly, as an increased import of specialized technology equipment may be expected, customs classification may prove to be more complex than for the products traditionally sourced by the company. But Tax can also represent an opportunity and lower the overall investment costs of the investment provided all available tax incentives (e.g. tax credit, grants) are identified and claimed in due time, that is – in most cases - in advance of the considered investment.

The supply chain changes

The information collected in the Industry 4.0 ecosystem will drive the physical supply chain of the company. For instance when a machine works slower than expected, the production planning could be adjusted automatically accordingly, e.g. by deciding to make another product at a different production line first. Or the sourcing of the products could be changed automatically to take into account freight delivery delays. But, quite often as well, we see that so-called smart factories are opened in a new jurisdiction, changing drastically the supply chain flows. Think for instance of Adidas opening a “Speedfactory” in Germany when its production had been located in Asia for decades.

It is therefore important to keep in mind that any change to the flows of goods can have a tax impact. This is the case for indirect tax, with a potential impact on the applicable VAT rate, the required supporting documentation and the VAT reporting obligations of the company. Further, modifying the sourcing of products may also have an impact on the import duties applicable on these products. And direct taxes should not be neglected either: it will be important to identify all potential legal flows (i.e. transfer of product ownership and invoicing) resulting from the different sourcing possibilities and to integrate them in the tax operating model of the company. This is key to ensure that an appropriate transfer price is applied on all intercompany transactions but also to ensure the sustainability of the model in place.

But Industry 4.0 could also bring other changes to the supply chain of a company as with the introduction of other manufacturing methods. Additive manufacturing, for instance, may well call for different raw materials than those traditionally used in the business, and different customs duties apply.

To avoid any bad surprise, all the changes brought to the supply chain of the group should therefore be considered with a tax lens in the design phase of the company’s Industry 4.0 ecosystem.

The improved efficiencies

The introduction of an Industry 4.0 ecosystem should results in an increased efficiency of the company as a whole. What entity(-ies) should actually be entitled to the related benefit? From a transfer pricing perspective, this is value creation that drives the allocation of profit between related companies. Hence, it will be important to check whether Industry 4.0 is altering the existing value chain creation within the group to determine how profit should be allocated going forward in the group. In practice, does the manufacturing function get the benefits? Or is it the supply chain management? What does it mean for the traditional manufacturing margin? Such analysis will also include a review of the technology developed in the Industry 4.0 process to determine who owns this intangible as well as the pricing to be applied for the use of this intangible by other group entities. As indicated earlier, practical questions of importance in that context will be for instance who is developing that technology, who is taking the key decisions in that respect, who is funding the project or who is bearing the risk of that investment.

Upfront considerations of these questions, before the project actually starts, will there as well avoid bad surprises.

2. Offering transformation

Industry 4.0 may in many instances also bring some changes to the traditional offering of a company. Let’s consider some of these possible changes.

After-sales services

Industry 4.0 can for instance allow to improve after-sales support provided to customers: A sensor can for example be installed on a product which signals when the product break down. In that case a mechanic can automatically be send to the customer to fix the product or to send spare parts to that customer to replace the broken part. Alternatively, a network of 3D printers could create spare parts needed, allowing to cut down inventory costs.

Besides the changes this brings to the supply chain of the company, with the consequences outlined above, this may also trigger other questions from a tax perspective. Here are some of them:

- From an indirect tax perspective, the characterization of a transaction as a sale of goods or as a service will attract a different VAT treatment. It is therefore important to consider the impact on the characterization of the transaction: to which extend can the spare parts provided still be considered as a sale of a good or as part of the repair service provided to the customer?

- Where does the sale originate and is the related profit taxable? In the country of the client or where the sale of the initial product was concluded?

- Does the new model require to have technical employees closer to the client location to reduce reaction time? If so, who is the legal entities employing them? Do these employees create a taxable presence of their employer or any other company of the group?

New products and services

In other cases, Industry 4.0 may offer new business opportunities to companies, for instances by using newly available data to offer new products and services to customers. These new revenue from the centralized used of data de-centrally collected should be considered carefully: where do they originate and where are they therefore taxable for corporate tax purposes? Are they remunerating goods or services and what is the corresponding VAT treatment?

Industry 4.0 is changing deeply the way companies operate. Inevitably, these changes have tax consequences for these companies. If not properly anticipated, these consequences may well end up destroying part of the economic value created by the new ecosystem. Integrating tax in the early planning stage of an Industry 4.0 ecosystem is therefore also one of the key to success.

Summary

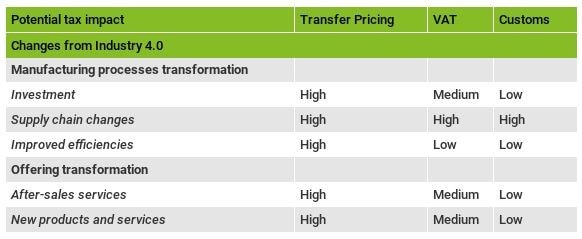

Generally speaking, the implementation of Industry 4.0 can have transfer pricing, VAT and customs impacts, which, if not considered upfront, could lead to some bad surprises. The actual impact will be different for each project. However, the acuity of the potential tax impact may schematically be summarized as follows for the different changes brought by Industry 4.0.